C4–6 (continued)

Req. 2

Cash (A) Accounts Receivable (A) Supplies (A) Prepaid Insurance (A)

Beg. 10,900

Beg. 800

Beg. 400

Beg. 0

5,700 (1)

(9)10,400

600 (7)

(6) 1,000

(1) 5,700

4,200 (2)

4,500 (25)

Bal. 1,400

Bal. 5,700

(3) 30,000

24,000 (4)

Bal. 6,100

(5) 6,000

Prepaid Rent (A)

Equipment (A)

Accum. Depreciation (xA)

(7) 600

(10) 7,600

(20) 3,500

400 (8)

2,200 (16)

Beg. 0

(2) 4,200

Bal. 4,200

Beg. 0

(4) 24,000

Bal. 24,000

0 Beg.

(25) 4,500

Bal. 26,600

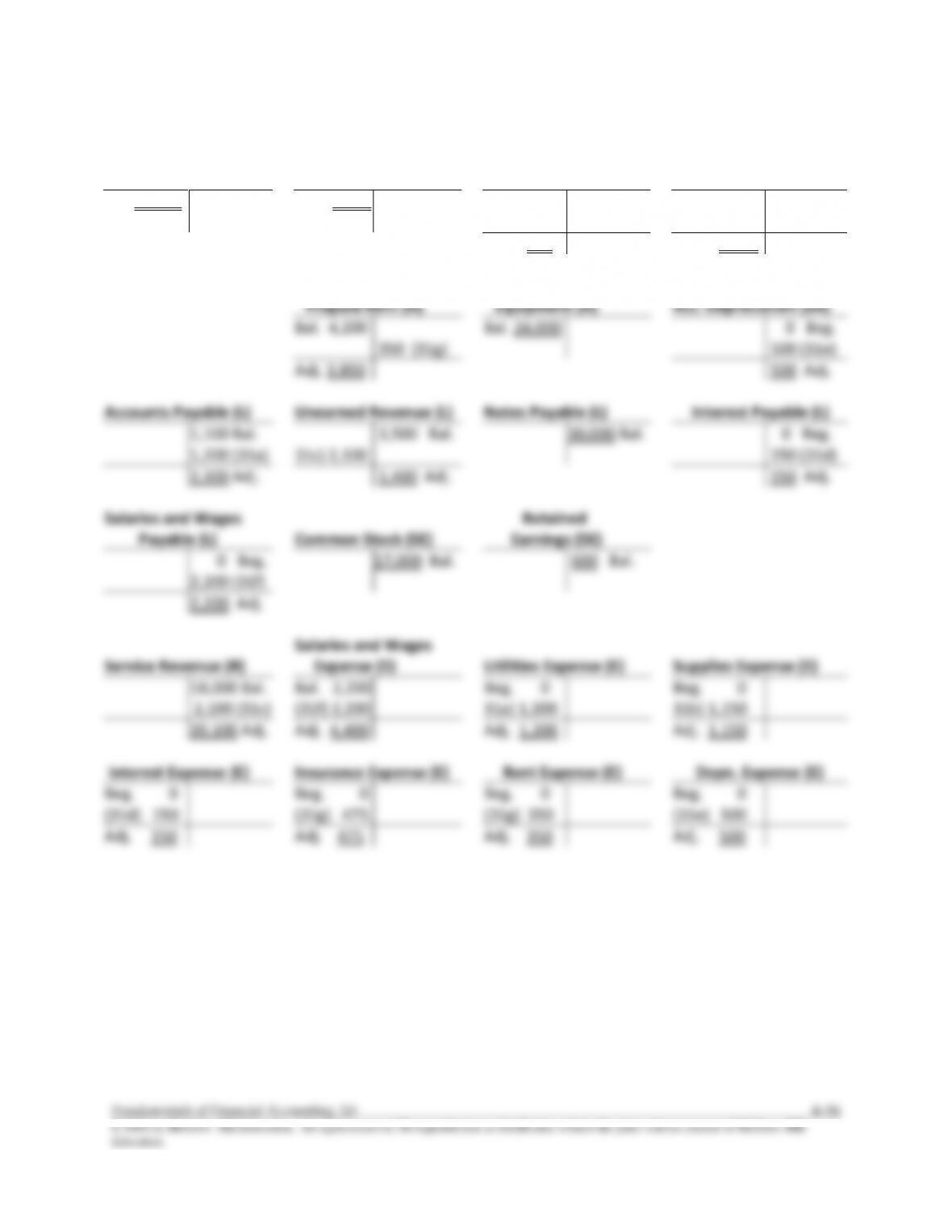

Accounts Payable (L)

Unearned Revenue (L)

Notes Payable (L)

Interest Payable (L)

500 Beg.

0 Beg.

0 Beg.

0 Beg.

(8) 400

1,000 (6)

3,500 (20)

30,000 (3)

1,100 Bal.

3,500 Bal.

30,000 Bal.

Salaries and Wages

Payable (L)

Common Stock (SE)

Retained

Earnings (SE)

0 Beg.

11,000 Beg.

600 Beg.

6,000 (5)

17,000 Bal.

Service Revenue (R)

Salaries and Wages

Expense (E)

Utilities Expense (E)

Supplies Expense (E)

0 Beg.

10,400 (9)

7,600 (10)

Beg. 0

(16) 2,200

Bal. 2,200

Beg. 0

Beg. 0

18,000 Bal.

Interest Expense (E)

Insurance Expense (E)

Rent Expense (E)

Depreciation Expense (E)

Beg. 0

Beg. 0

Beg. 0

Beg. 0

C4–6 (continued)

Req. 2 (continued)

FAST DELIVERIES, INC.

Unadjusted Trial Balance

January 31

Account Titles

Debit

Credit

Cash

$ 26,600

Accounts Receivable

6,100

Supplies

1,400

Prepaid Insurance

5,700

Prepaid Rent

4,200

Equipment

24,000

Accumulated Depreciation–Equipment

$ 0

Accounts Payable

1,100

Unearned Revenue

3,500

Notes Payable

30,000

Salaries and Wages Payable

0

Interest Payable

0

Common Stock

17,000

Retained Earnings

600

Service Revenue

18,000

Salaries and Wages Expense

2,200

Supplies Expenses

0

Depreciation Expense

0

Interest Expense

0

Totals

$ 70,200

$ 70,200

C4–6 (continued)

Req. 3

Jan. 31a)

Utilities Expense (+E, –SE)

1,200

Accounts Payable (–A)

1,200

31b)

Supplies Expense (+E, –SE)

1,150

Supplies (–A)

1,150

($1,400 unadjusted – $1,150 AJE = $250 on hand)

31c)

Unearned Revenue (–L)

2,100

Service Revenue (+R, +SE)

2,100

($3,500 x 0.60 = $2,100 now earned)

31d)

Interest Expense (+E, –SE)

150

Interest Payable (+L)

150

($30,000 x .06 x 1/12 = $150)

31e)

Depreciation Expense (+E, –SE)

500

Accumulate Depreciation—Equipment (+xA, –A)

500

($24,000 x ¼ x 1/12 = $500)

31f)

Salaries and Wages Expense (+E, –SE)

2,200

Salaries and Wages Payable (+L)

2,200

31g)

Insurance Expense (+E, –SE)

475

Prepaid Insurance (–A)

475

($5,700 x 1/12 = $475)

Rent Expense (+E, –SE)

350

Prepaid Rent (–A)

350

($4,200 x 1/12 = $475)

C4–6 (continued)

Req. 4

Cash (A) Accounts Receivable (A) Supplies (A) Prepaid Insurance (A)

Bal. 26,600

Bal. 6,100

Bal. 1,400

Bal. 5,700

1,150 (31b)

475 (31g)

Adj. 250

Adj. 5,225

Prepaid Rent (A)

Equipment (A)

Acc. Depreciation (xA)

Bal. 4,200

Bal. 24,000

0 Beg.

350 (31g)

500 (31e)

Adj. 3,850

500 Adj.

Accounts Payable (L)

Unearned Revenue (L)

Notes Payable (L)

Interest Payable (L)

1,100 Bal.

3,500 Bal.

30,000 Bal.

0 Beg.

1,200 (31a)

31c) 2,100

150 (31d)

2,300 Adj.

1,400 Adj.

150 Adj.

Salaries and Wages

Payable (L)

Common Stock (SE)

Retained

Earnings (SE)

0 Beg.

17,000 Bal.

600 Bal.

2,200 (31f)

2,200 Adj.

Service Revenue (R)

Salaries and Wages

Expense (E)

Utilities Expense (E)

Supplies Expense (E)

18,000 Bal.

2,100 (31c)

Bal. 2,200

(31f) 2,200

Beg. 0

31a) 1,200

Beg. 0

31b) 1,150

20,100 Adj.

Adj. 4,400

Adj. 1,200

Adj. 1,150

Interest Expense (E)

Insurance Expense (E)

Rent Expense (E)

Depn. Expense (E)

Beg. 0

(31d) 150

Beg. 0

(31g) 475

Beg. 0

(31g) 350

Beg. 0

(31e) 500

Adj. 150

Adj. 475

Adj. 350

Adj. 500

C4–6 (continued)

Req. 4 (continued)

FAST DELIVERIES, INC.

Adjusted Trial Balance

January 31

Account Titles

Debit

Credit

Cash

$ 26,600

Accounts Receivable

6,100

Supplies

250

Prepaid Rent

3,850

Prepaid Insurance

5,225

Equipment

24,000

Accumulated Depreciation–Equipment

$ 500

Accounts Payable

2,300

Unearned Revenue

1,400

Salaries and Wages Payable

2,200

Interest Payable

150

Notes Payable

30,000

Common Stock

17,000

Retained Earnings

600

Service Revenue

20,100

Salaries and Wages Expenses

4,400

Utilities Expense

1,200

Supplies Expenses

1,150

Depreciation Expense

500

Insurance Expense

475

Rent Expense

350

Interest Expense

150

Totals

$ 74,250

$ 74,250

C4–6 (continued)

Req. 5

Fast Deliveries, Inc.

Income Statement

For the month ended January 31

Fast Deliveries, Inc.

Statement of Retained Earnings

For the month ended January 31

Service Revenue

$20,100

Retained earnings, beginning of period

$ 600

Expenses

Add: Net Income

11,875

Salaries and Wages

4,400

Less: Dividends

0

Utilities

1,200

Retained earnings, end of period

$ 12,475

Supplies

1,150

Depreciation

500

Insurance

475

Rent

350

Interest

150

Net income

$11,875

Fundamentals of Financial Accounting, 5/e 4–97

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO SKILLS DEVELOPMENT CASES

S4–1

1. A

2. D

3. B

S4–2

Req. 1

The Home Depot had $865,000,000 in Advertising Expense whereas Lowe’s had

$811,000,000 in Advertising Expenses for fiscal 2013 (as reported in Note 1).

Req. 2

S4–3

The solutions to this project will depend on the company and/or accounting period

S4–4

Req.1

Q1).

Req. 2

To capitalize an expense is to record its cost as an asset rather than an expense. It is

appropriate to capitalize a cost if it produces a probable future economic benefit.

7.6 M

Bonus Payable (−L) ……………………………………

7.6 M

Bonus Expense (−E,+SE) ……………………

7.6 M

2000 (Q1)

Bonus Expense (+E, −SE) …………………………..

7.6 M

Cash (−A) ………………………………………..

7.6 M