Chapter 4

Adjustments, Financial Statements, and

Financial Results

ANSWERS TO QUESTIONS

1. Adjusting entries are made at the end of the accounting period to record all

2. (a) The time period assumption states that the long life of a company can be

divided into shorter time periods. Adjustments are required by GAAP to

ensure that a company’s financial statements include all the transactions of the

period.

3. The two different types of adjusting journal entries are:

(1) Deferral adjustments:

(2) Accrual adjustments:

(a) Revenues – revenues that have been earned by the end of the accounting

4. Adjusting entries have no effect on cash. For unearned revenues and

5. A contra–asset is an account related to an asset that is an offset or reduction to the

6. Depreciation expense is reported on the income statement. It indicates the amount

7. An adjusted trial balance is a list of the individual accounts, usually in financial

8.

Assets

=

Liabilities

+

Stockholders’ Equity

Dec

31

Cash

Prepaid Rent

−9,000

+9,000

=

Jan

31

Prepaid Rent

−3,000

=

Rent

Expense (+E)

−3,000

Feb

28

Prepaid Rent

−3,000

=

Rent

Expense (+E)

−3,000

Mar

31

Prepaid Rent

−3,000

=

Rent

Expense (+E)

−3,000

9. Balance sheet accounts at January 31:

Prepaid rent $6,000

10.

12/31

Prepaid Rent (+A) …………………………………………..

9,000

Cash (−A) ……………………………………………….

9,000

1/31

Rent Expense (+E, −SE) ………………………………….

3,000

Prepaid Rent (−A) …………………………………….

3,000

2/28

Rent Expense (+E, −SE) ………………………………….

3,000

Prepaid Rent (−A) …………………………………….

3,000

3/31

Rent Expense (+E, −SE) ………………………………….

3,000

Prepaid Rent (−A) …………………………………….

3,000

11. (a) Income statement: Revenues − Expenses = Net Income

12. The net income from the income statement is included on the statement of retained

13. Closing journal entries are made at the end of the accounting period to transfer the

balances in the temporary accounts to retained earnings. The closing journal entries

14. Permanent accounts are balance sheet accounts (for assets, liabilities, and

stockholders’ equity accounts). These accounts are not closed at the end of

15. The income statement accounts are closed at the end of the accounting period

because, in effect, they are temporary sub–accounts to retained earnings (i.e., a

part of stockholders’ equity). They are used only for accumulation during the

accounting period. When the period ends, these accumulated accounts must be

16. A post–closing trial balance is a list of all the accounts and their balances taken from

the ledger, after the adjusting and closing journal entries have been journalized and

17. The owner is correct; the adjustment process does consume a lot of time and it

delays month–end reporting of financial results. However, prior to adjustments, the

financial results are not complete or up–to–date. Important information relating to

assets, liabilities, revenues, and expenses has not yet been incorporated into the

accounting records. Without this information, the owner may make decisions that

Authors’ Recommended Solution Time

(Time in minutes)

Mini–exercises

Exercises

Problems

Skills

Development

Cases*

Continuing

Case

No.

Time

No.

Time

No.

Time

No.

Time

No. Time

1

5

1

10

CP4–1

20

1

20

1

45

2

5

2

10

CP4–2

20

2

20

3

5

3

15

CP4–3

15

3

30

4

5

4

10

CP4–4

45

4

25

5

5

5

20

PA4–1

20

5

25

6

5

6

20

PA4–2

20

6

40

7

5

7

20

PA4–3

15

7

45

8

5

8

15

PA4–4

45

9

5

9

15

PB4–1

20

10

5

10

20

PB4–2

20

11

10

11

5

PB4–3

15

12

5

12

15

PB4–4

45

13

5

13

10

C4–1

45

14

5

14

20

C4–2

60

15

5

15

20

C4–3

60

16

10

16

10

C4–4

60

17

5

17

15

C4–5

45

18

5

18

10

C4–6

45

19

5

19

20

20

5

21

5

22

10

23

10

24

10

25

10

26

10

* Due to the nature of cases, it is very difficult to estimate the amount of time students

will need to complete them. As with any open–ended project, it is possible for students

to devote a large amount of time to these assignments. While students often benefit

Fundamentals of Financial Accounting, 5/e 4–6

Case

Financial

Analysis

Research

Ethical

Reasoning

Critical

Thinking

Technology

Writing

Teamwork

1

x

2

x

3

x

X

x

x

x

4

x

x

x

5

x

x

x

x

6

x

x

x

7

x

x

Fundamentals of Financial Accounting, 5/e 4–7

ANSWERS TO MINI–EXERCISES

M4–1

1. A, D

M4–2

1. A, E

M4–4

(1)

Supplies Expense (+E –SE)

400

Supplies (–A)

400

(2)

Interest Receivable (+A)

250

Interest Revenue (+R +SE)

250

(3)

Salaries and Wages Expense (+E, –SE)

3,600

Salaries and Wages Payable (+L)

3,600

(4)

Accounts Receivable (+A)

1,000

Service Revenue (+R, +SE)

1,000

(5)

Unearned Revenue (–L)

600

Service Revenue (+R, +SE)

600

Fundamentals of Financial Accounting, 5/e 4–8

M4–5

Assets

=

Liabilities

+

Stockholders’ Equity

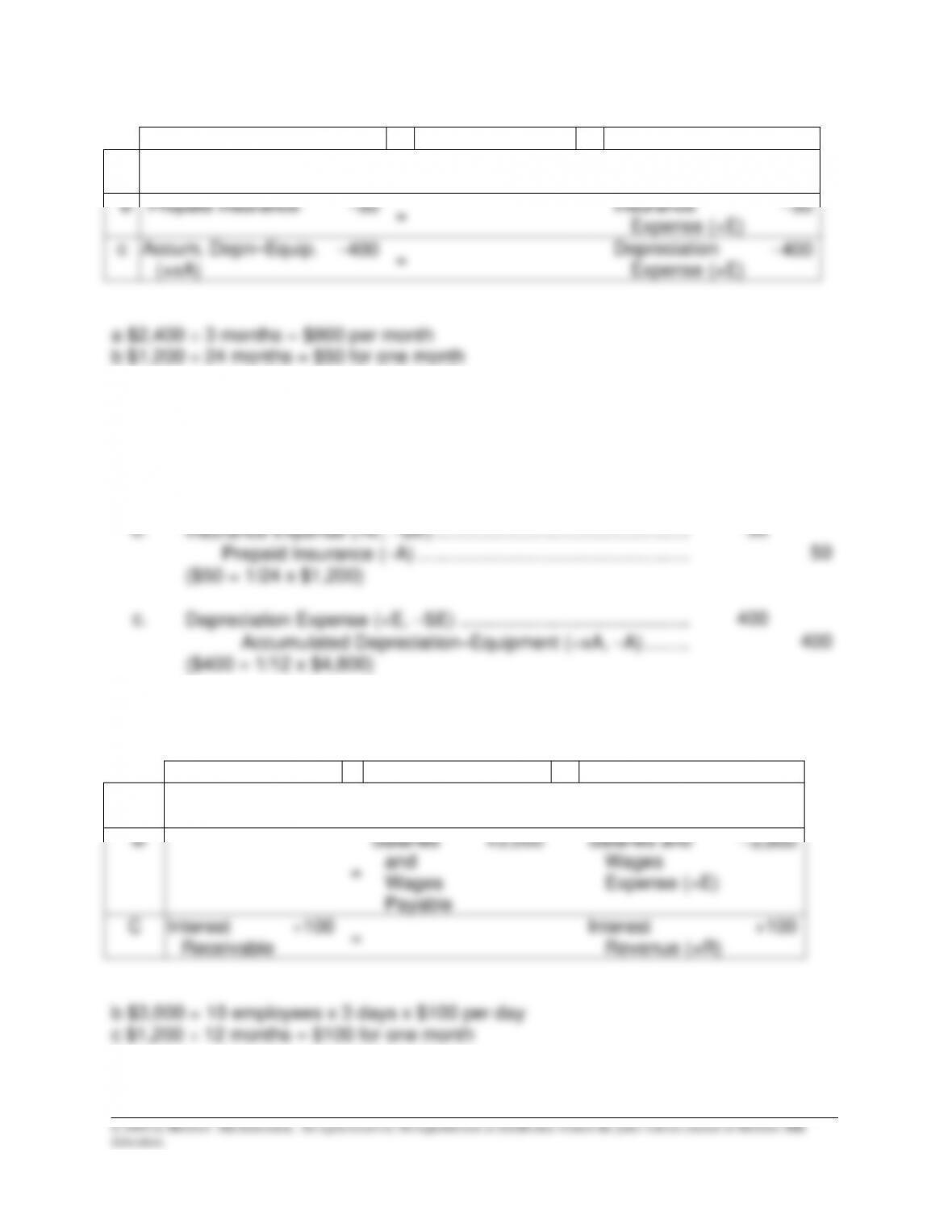

a

=

Unearned

Revenue

−800

Rent

Revenue (+R)

+800

b

Prepaid Insurance

−50

=

Insurance

Expense (+E)

−50

c

Accum. Depn–Equip.

(+xA)

−400

=

Depreciation

Expense (+E)

−400

a $2,400 ÷ 3 months = $800 per month

b $1,200 ÷ 24 months = $50 for one month

M4–6

a.

Unearned Revenue (−L) ………………………………………………….

800

Rent Revenue (+R, +SE) ………………………………………….

800

($800 = 1/3 x $2,400)

b.

Insurance Expense (+E, −SE) ………………………………………….

50

Prepaid Insurance (−A) …………………………………………….

50

($50 = 1/24 x $1,200)

c.

Depreciation Expense (+E, −SE) ……………………………………..

400

Accumulated Depreciation–Equipment (+xA, −A) ………

400

($400 = 1/12 x $4,800)

M4–7

Assets

=

Liabilities

+

Stockholders’ Equity

A

=

Accounts

Payable

+600

Utilities

Expense (+E)

−600

B

=

Salaries

and

Wages

Payable

+3,000

Salaries and

Wages

Expense (+E)

−3,000

C

Interest

Receivable

+100

=

Interest

Revenue (+R)

+100

b $3,000 = 10 employees x 3 days x $100 per day

c $1,200 ÷ 12 months = $100 for one month

M4–8

Fundamentals of Financial Accounting, 5/e 4–9

(a)

Utilities Expense (+E, −SE)…………………………..

600

Accounts Payable (+L)………………………..

600

To record utilities expense incurred but not yet paid.

(b)

Salaries and Wages Expense (+E, −SE) ………..

3,000

Salaries and Wages Payable (+L) ………..

3,000

To record Salaries and Wages Expense incurred but not yet paid,

calculated as 10 employees x 3 days x $100 per day.

(c)

Interest Receivable (+A) ………………………………

100

Interest Revenue (+R, +SE) ………………..

100

To record interest earned but not yet collected,

calculated as $1,200 x 1/12.

M4–9

a)

Sept. 30 Prepaid Rent (+A) 4,000

Cash (–A) 4,000

Oct. 31 AJE Rent Expense (+E –SE) 2,000

M4–10

a)

Dec. 31 Cash (+A) 12,000

Unearned Revenue (+L) 12,000

Jan. 31 AJE Unearned Revenue (–L) 1,000

M4–11

(a)

Prepaid Insurance (+A) ………………………………..

2,275

Insurance Expense (−E, +SE) ……………..

2,275

(b)

Service Revenue (−R, −SE) ………………………….

1,000

Unearned Revenue (+L) ……………………..

1,000

(c)

Income Tax Expense (+E, −SE) ……………………

2,000

Income Tax Payable (+L)…………………….

2,000