Chapter Outline

Teaching Notes

LO 4-5 Explain the closing process.

E. Closing Temporary Accounts

1. Last step of accounting cycle is referred to as closing

process; performed only at the end of the year after the

financial statements have been prepared.

2. Cleans up the records to get them ready to begin tracking

the results in the following year.

3. Closing Income Statement and Dividend Accounts

✓ Activity #4

a. Permanent accounts––Accounts that track financial

results from year to year by carrying their ending

balances into the next year; the Retained Earnings

account, like all other balance sheet accounts, is a

permanent account because its ending balance from

one year becomes its beginning balance for the

following year.

b. Temporary accounts––Accounts that track financial

results for a limited period of time by having their

balances zeroed out at the end of each accounting

year; all revenue, expense, and the dividends accounts

are temporary accounts because they are used to track

only the current period’s results and then are closed

before the next year’s activities are recorded.

c. Closing process serves two purposes:

i. Transfer net income (or loss) and dividends to

Retained Earnings. The balance in the Retained

Earnings account will then agree with the statement

of retained earnings and the balance sheet.

ii. Establish zero balances in all income statement and

dividend accounts. The balances in the temporary

accounts are reset to zero to start accumulating

next year’s results.

d. Two closing journal entries are needed:

Illustrated in Exhibit 4.13

i. Debit each revenue account for the amount of its

credit balance, credit each expense account for the

amount of its debit balance, and record the

difference in Retained Earnings. (If the company

has a net loss, Retained Earnings will be debited.)

Stress that the amount

credited to Retained Earnings

should equal net income on

the income statement.

ii. Credit the Dividends account for the amount of its

debit balance and debit Retained Earnings for the

same amount.

Chapter Outline

Teaching Notes

F. Post-Closing Trial Balance

1. After the closing journal entries are posted, all temporary

accounts should have zero balances. These accounts will

be ready for recording transactions next year.

Illustrated in Exhibit 4.14

2. The ending balance in Retained Earnings is now up to

date (it matches the year-end amount on the statement of

retained earnings and balance sheet) and is carried

forward as the beginning balance for the next year.

In this context, post means

3. Post-closing trial balance––An internal report prepared

to check that total debits still equal total credits and that

all temporary accounts have been closed.

“after,” so a post-closing

trial balance is an “after–

closing” trial balance.

III. Evaluate the Results

LO 4-6 Explain how adjustments affect financial results.

A. Adjusted Financial Results

1. Adjustments help to ensure that all revenues and expenses

are reported in the period in which they are earned and

incurred.

2. As a result of adjustments, the financial statements

present the best picture of whether the company’s

business activities were profitable that period and what

economic resources the company owns and owes at the

end of that period.

The “Spotlight on Financial

Reporting” feature addresses

the failure of Circuit City.

3. Without these adjustments, the financial statements

present an incomplete and misleading picture of the

company’s financial performance.

❖ Spotlight Video Series—

Chapter 4

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 4–1

Use Handout 4–1 for an in-class activity designed to review transaction analysis (preparation of

adjusting entries and impact on the accounting equation) and the posting to T-accounts. The solution

follows the handout master.

2. Handout 4–2

If you used Handout 4–1, use Handout 4-2 for an in-class activity designed to review the preparation

of an adjusted trial balance. The solution follows the handout master.

3. Handout 4–3

If you used Handout 4–2, use Handout 4–3 for an in-class activity designed to review the preparation

of financial statements. The solution follows the handout master.

4. Handout 4–4

If you used Handout 4–2, use Handout 4–4 for an in-class activity designed to review the preparation

of closing entries and a post-close trial balance. The solution follows the handout master.

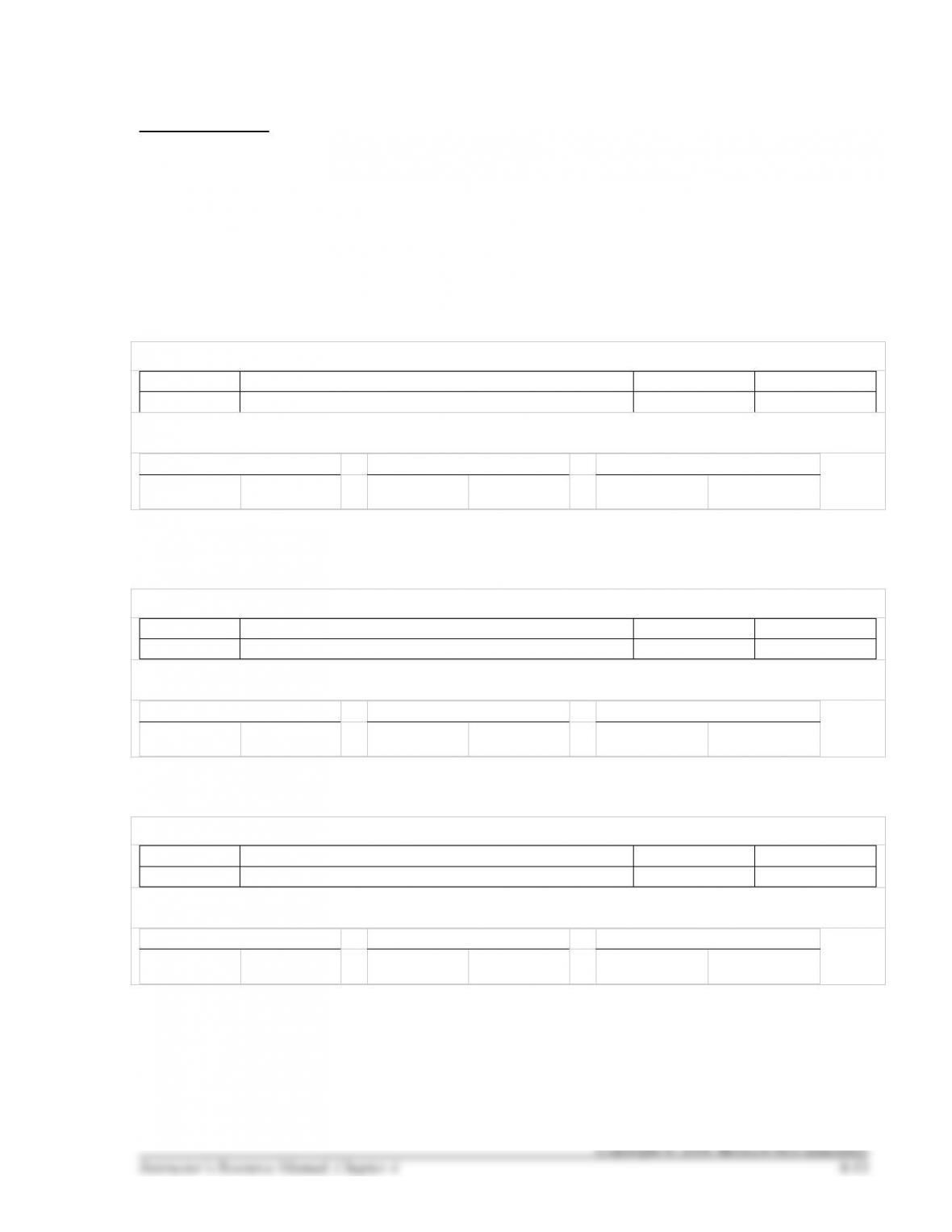

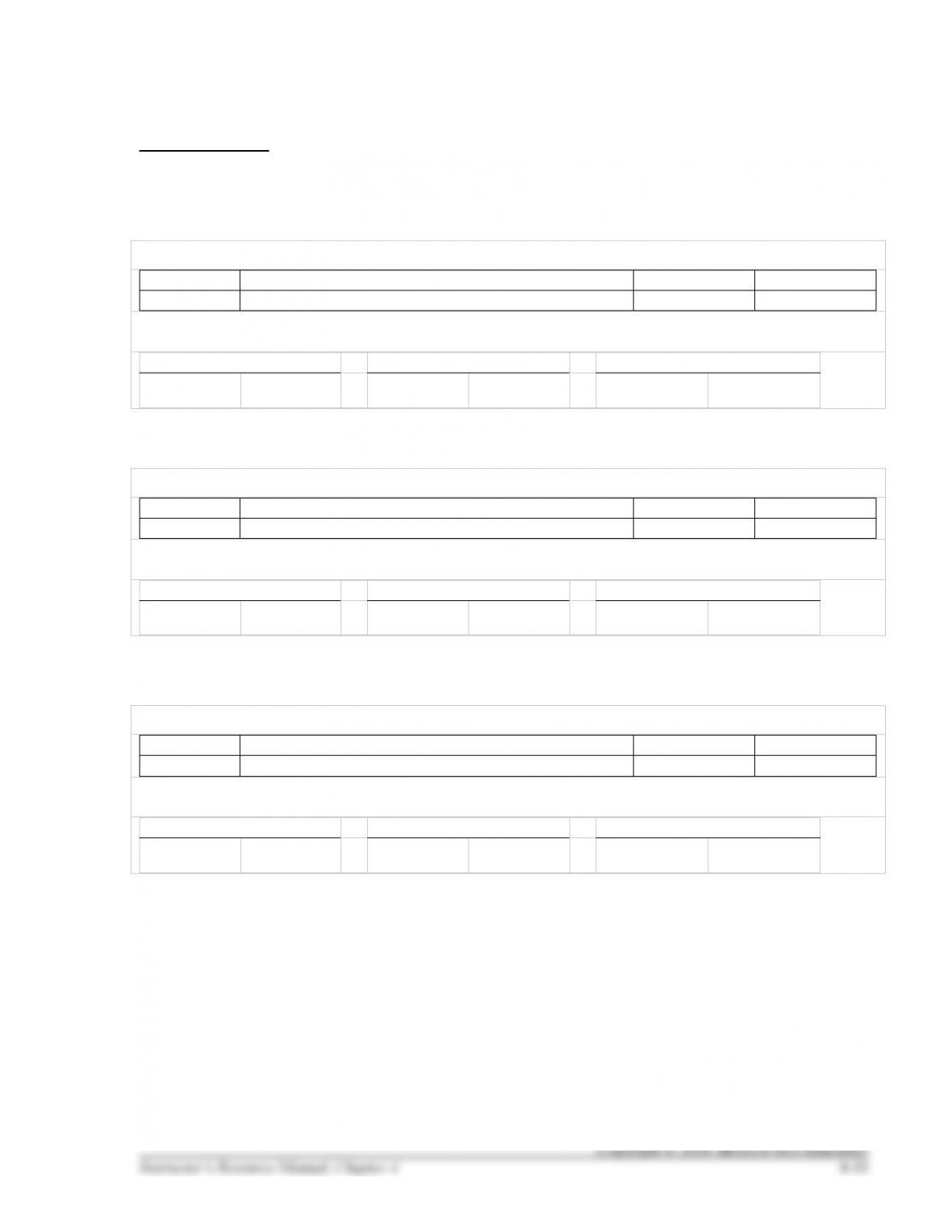

HANDOUT 4–1

ADJUSTING ENTRIES AND

POSTING TO T-ACCOUNTS

Prepare the required adjusting journal entry for each situation as of December 31, 2016. See the last page

for the unadjusted account balances shown in T-accounts.

(a) Deana’s Decorating had $1,800 of supplies on hand on December 1, 2016. When counting the

supplies on December 31, 2016, Deana’s found only $800 worth of supplies on hand.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(b) Deana’s had paid $12,000 for six months’ rent on November 1, 2016. As of December, 31, 2016, two

months’ (November & December) prepaid rent has expired.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(c) Deana’s had paid $6,000 for one year’s insurance on June 1, 2016.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

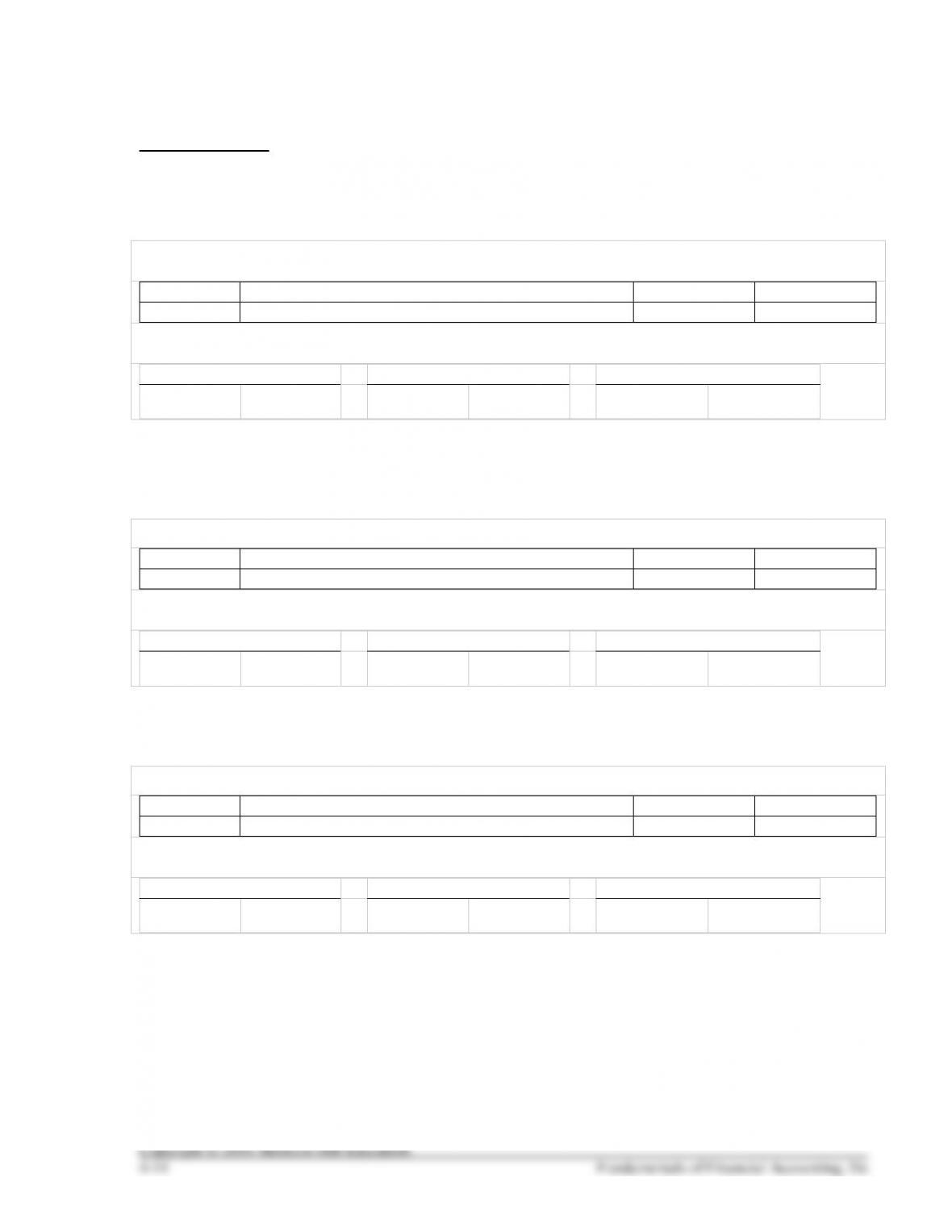

HANDOUT 4–1, continued

(d) The company had acquired equipment costing $40,000 on January 1, 2016. The depreciation on this

equipment was calculated to be $2,000 for 2016.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(e) On December 1, 2016, the company had sold $500 in gift certificates for decorating services to a

customer. On December 31, 2016, the accountant received an envelope containing $400 worth of

redeemed gift certificates, not yet recorded in the company’s books.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(f) On June 30, 2016, the company invested $20,000 in a certificate of deposit that will yield 12% interest

at the end of one year.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

HANDOUT 4–1, continued

(g) The company borrowed a note payable from the bank for $30,000 on January 1, 2016, due with all

interest on June 30, 2017. The note payable requires 10% interest.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(h) The company calculated its income taxes as $26,110 for the year ended December 31, 2016.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

(i) On December 15, 2016, the company declared a $750 dividend, payable January 15, 2017.

Debit and credit the accounts affected.

Dec. 31

2016

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Post the adjusting entries above to the T-accounts on the following page.

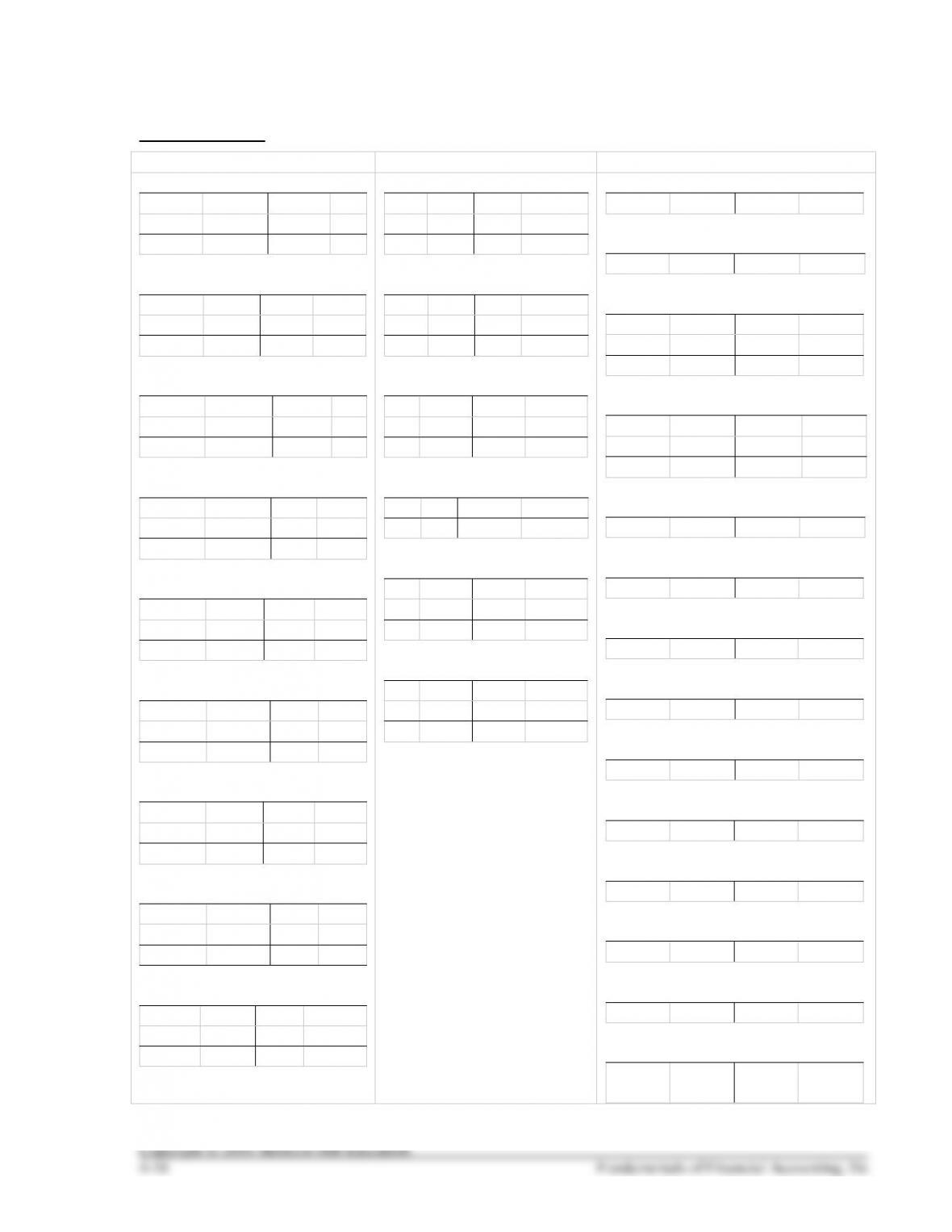

HANDOUT 4-1, continued

Assets

Liabilities

Stockholders’ Equity

+ Cash –

Unadj.

43,450

+ Supplies –

Unadj.

1,800

(a)

+ Accounts Receivable –

Unadj.

4,000

+ Prepaid Rent –

Unadj.

12,000

(b)

+ Prepaid Insurance –

Unadj.

6,000

(c)

+ Certificate of Deposit –

Unadj.

20,000

+ Interest Receivable –

Unadj.

0

+ Property, Plant & Equipment –

Unadj.

40,000

− Accumulated Depreciation +

0

Unadj.

− Accounts Payable +

250

Unadj.

− Dividend Payable +

0

Unadj.

− Unearned Revenue +

500

Unadj.

− Notes Payable +

30,000

Unadj.

− Interest Payable +

0

Unadj.

− Income Taxes Payable +

0

Unadj.

+ Contributed Capital –

10,000

Unadj.

− Retained Earnings +

0

Unadj.

+ Dividends –

Unadj.

0

− Service Revenue +

120,000

Unadj.

+ Interest Revenue –

+ Salaries and Wage Expense –

Unadj.

32,000

+ Utilities Expense –

Unadj.

1,000

+ Telephone Expense –

Unadj.

500

+ Supplies Expense –

+ Rent Expense –

+ Insurance Expense –

+ Depreciation Expense –

+ Interest Expense –

+ Income Tax Expense –

HANDOUT 4–1 SOLUTION

ADJUSTING ENTRIES AND

POSTING TO T-ACCOUNTS

Prepare the required adjusting journal entry for each situation as of December 31, 2016. See the last page

for the unadjusted account balances shown in T-accounts.

(a) Deana’s Decorating had $1,800 of supplies on hand on December 1, 2016. When counting the

supplies on December 31, 2016, Deana’s found only $800 worth of supplies on hand.

Debit and credit the accounts affected.

Dec. 31

Supplies Expense (+E, –SE)

1,000

2016

Supplies (–A)

1,000

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Supplies

–1,000

Supplies

Expense

–1,000

(b) Deana’s had paid $12,000 for six months’ rent on November 1, 2016. As of December, 31, 2016, two

months’ (November & December) prepaid rent has expired.

Debit and credit the accounts affected.

Dec. 31

Rent Expense (+E, –SE)

4,000

2016

Prepaid Rent (–A)

4,000

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Prepaid

Rent

–4,000

Rent Expense

–4,000

(c) Deana’s had paid $6,000 for one year’s insurance on June 1, 2016.

Debit and credit the accounts affected.

Dec. 31

Insurance Expense (+E, –SE)

3,500

2016

Prepaid Insurance (–A)

3,500

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Prepaid

Insurance

–3,500

Insurance

Expense

–3,500

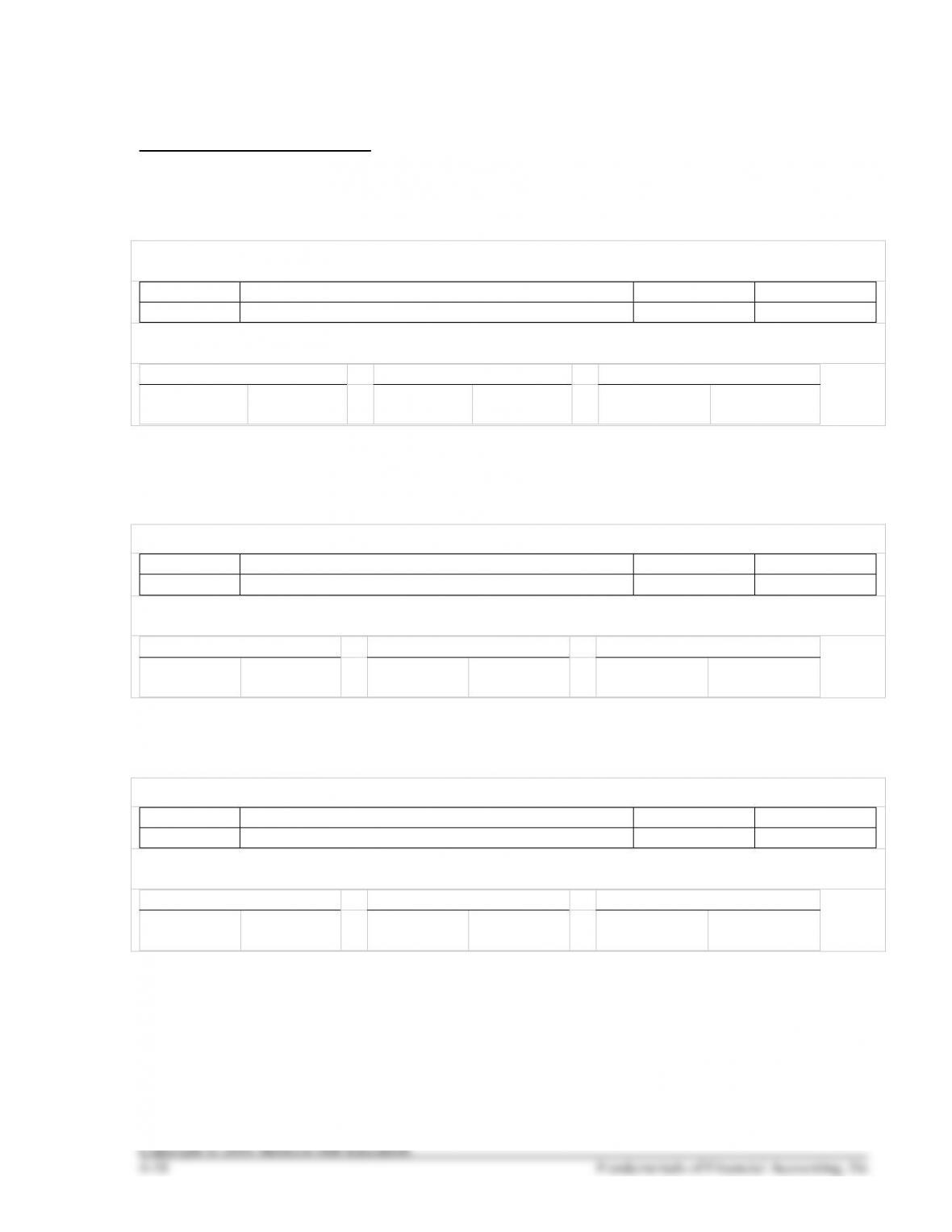

HANDOUT 4–1 SOLUTION, continued

(d) The company had acquired equipment costing $40,000 on January 1, 2016. The depreciation on this

Equipment was calculated to be $2,000 for 2016.

Debit and credit the accounts affected.

Dec. 31

Depreciation Expense (+E, –SE)

2,000

2016

Accumulated Depreciation (+xA, –A)

2,000

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Accumulated

Depreciation

–2,000

Depreciation

Expense

–2,000

(e) On December 1, 2016, the company had sold $500 in gift certificates for decorating services to a

customer. On December 31, 2016, the accountant received an envelope containing $400 worth of

redeemed gift certificates, not yet recorded in the company’s books.

Debit and credit the accounts affected.

Dec. 31

Unearned Revenue (–L)

400

2016

Service Revenue (+R, +SE)

400

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Unearned

Revenue

–400

Service

Revenue

+400

(f) On June 30, 2016, the company invested $20,000 in a certificate of deposit that will yield 12% interest

at the end of one year.

Debit and credit the accounts affected..

Dec. 31

Interest Receivable (+A)

1,200

2016

Interest Revenue (+R, +SE)

1,200

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Interest

Receivable

+1,200

Interest

Revenue

+1,200

HANDOUT 4–1 SOLUTION, continued

(g) The company borrowed a note payable from the bank for $30,000 on January 1, 2016, due with all

interest on June 30, 2017. The note payable requires 10% interest.

Debit and credit the accounts affected.

Dec. 31

Interest Expense (+E, –SE)

3,000

2016

Interest Payable (+L)

3,000

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Interest

Payable

+3,000

Interest

Expense

–3,000

(h) The company calculated its income taxes as $26,110 for the year ended December 31, 2016.

Debit and credit the accounts affected.

Dec. 31

Income Tax Expense (+E, –SE)

26,110

2016

Income Tax Payable (+L)

26,110

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Income Tax

Payable

+26,110

Income Tax

Expense

–26,110

(i) On December 15, 2016, the company declared a $750 dividend, payable January 15, 2017.

Debit and credit the accounts affected.

Dec. 31

Dividends (+D, –SE)

750

2016

Dividend Payable (+L)

750

Ensure the equation still balances and debits = credits.

Assets

=

Liabilities

+

Stockholders’ Equity

Income Tax

Payable

+750

Dividends

–750

HANDOUT 4-1 SOLUTION, continued

Assets

Liabilities

Stockholders’ Equity

+ Cash –

Unadj.

43,450

Adj.

43,450

+ Supplies –

Unadj.

1,800

1,000

(a)

Adj.

800

+ Accounts Receivable –

Unadj.

4,000

Adj.

4,000

+ Prepaid Rent –

Unadj.

12,000

4,000

(b)

Adj.

8,000

+ Prepaid Insurance –

Unadj.

6,000

3,500

(c)

Adj.

2,500

+ Certificate of Deposit –

Unadj.

20,000

Adj.

20,000

+ Interest Receivable –

Unadj.

0

(f)

1,200

Adj.

1,200

+ Property, Plant & Equipment –

Unadj.

40,000

Adj.

40,000

− Accumulated Depreciation +

0

Unadj.

2,000

(d)

2,000

− Accounts Payable +

250

Unadj.

250

Adj.

− Dividend Payable +

0

Unadj.

750

(i)

750

Adj.

− Unearned Revenue +

500

Unadj.

(e)

400

Adj.

100

− Notes Payable +

30,000

Unadj.

30,000

Adj.

− Interest Payable +

0

Unadj.

3,000

(g)

3,000

Adj.

− Income Taxes Payable +

0

Unadj.

26,110

(h)

26,110

Adj.

+ Contributed Capital –

10,000

Unadj.

− Retained Earnings +

0

Unadj.

+ Dividends –

Unadj.

0

(i)

750

Adj.

750

− Service Revenue +

120,000

Unadj.

400

(e)

120,400

Adj.

+ Interest Revenue –

1,200

(f)

+ Salaries and Wage Expense –

Unadj.

32,000

+ Utilities Expense –

Unadj.

1,000

+ Telephone Expense –

Unadj.

500

+ Supplies Expense –

(a)

1,000

+ Rent Expense –

(b)

4,000

+ Insurance Expense –

(c)

3,500

+ Depreciation Expense –

(d)

2,000

+ Interest Expense –

(g)

3,000

+ Income Tax Expense –

(h)

26,110