CHAPTER 3

THE INCOME STATEMENT

Student Learning Objectives and Related Assignment Materials

Student Learning

Objectives

Mini–

Exercises

Exercises

Coached

Problems

Problems

(Groups

A & B)

Compre–

hensive

Problem

Skills

Develop-

ment

Cases

Continuing

Case

LO 3-1 Describe

common

operating

transactions and

select appropriate

income statement

account titles.

8, 19,

20, 21

1, 2, 3,

4, 5, 6,

15

1, 3

A1, A3,

B1, B3

1, 2, 3,

4, 5, 6

LO 3-2 Explain and

apply the revenue

and expense

recognition

principles.

1, 2*,

3*, 6, 7,

9, 10,

17, 18

3, 4, 5,

6, 7, 8,

9, 10,

11, 12,

14^, 15,

16

1, 2, 3

A1, A2,

A3, B1,

B2, B3

1

4, 5, 6, 7

1†

LO 3-3 Analyze,

record, and

summarize the

effects of

operating

transactions, using

the accounting

equation, journal

entries, and T-

accounts.

4*, 5*,

6, 7, 11,

12, 13*,

14*, 15,

16, 17,

18

7, 8, 9,

10, 11,

12, 14^,

15, 16,

17, 18,

20, 21

1, 2, 3,

4^

A1, A2,

A3, A4^,

B1, B2,

B3, B4^

1

4, 7

1†

LO 3-4 Prepare an

unadjusted trial

balance.

20, 21

13, 19

3

A3, B3

1

6, 7

LO 3-5 Evaluate net

profit margin, but

beware of income

statement

limitations.

8, 19,

21, 22,

23^

11, 20,

21

3, 4^

A3,A4^,

B3, B4^

1

3, 4, 5

1†

* Animated solution included in the PowerPoint Slides.

^ Particularly challenging; requires students to combine multiple concepts in order to advance to the

next level of accounting knowledge.

† Continuing Case 3-1 builds on the story of Nicole’s Getaway Spa, introduced in earlier chapters. This

case focuses on analyzing transactions and preparing journal entries, calculating the company’s

preliminary net income and net profit margin for the month, and identifying the adjustment(s) that will

have to be made before the income statement is finalized. This case will be extended in future

chapters.

Overview

The entrepreneur from Chapters 1 and 2 opens his doors to customers and completes daily operating

transactions.

Students learn how to analyze and record operating transactions involving revenues and expenses and

distinguish cash basis from accrual basis.

Synopsis of Chapter Revisions

• New contemporary focus company: replaced pizza company with SonicGateway, thereby allowing

revenue recognition to be illustrated when game app icon shows “installation completed”

• New illustrations to compare timing of revenue recognition and cash receipt (Exhibit 3.5)

• New Spotlight on Financial Reporting to illustrate revenue recognition policy of Take-Two

Interactive (software maker of Grand Theft Auto)

• New illustrations to compare timing of expense recognition and cash payment (Exhibit 3.6)

• New transactions to illustrate contemporary technology, such as online Facebook advertising,

automated monthly disbursements, and e-commerce sales with online receipts similar to PayPal

• New format for accounting equation effects to illustrate link between income statement and balance

sheet

• New Spotlight on Financial Reporting to focus on technology companies, including Electronic Arts,

Activision Blizzard, Facebook, and LinkedIn

• Updated demonstration case featuring Carnival Corporation

• Reviewed and updated all end-of-chapter material, including new problem formats that automatically

post journal entries to T-accounts and prepare trial balances

PowerPoint Slides

Student Learning Objective

PowerPoint® Slides

LO 3-1 Describe common operating transactions and select appropriate income

statement account titles.

3-2 through 3-5

LO 3-2 Explain and apply the revenue and expense recognition principles.

3-6 through 3-9

LO 3-3 Analyze, record, and summarize the effects of operating transactions,

using the accounting equation, journal entries, and T-accounts.

3-10 through 3-19

LO 3-4 Prepare an unadjusted trial balance.

3-20 through 3-23

LO 3-5 Evaluate net profit margin, but beware of income statement limitations.

3-24 through 3-26

Animated Builds and Animated Solutions

PowerPoint® Slides

Mini-Exercise 3-2

3-28

Mini-Exercise 3-3

3-29

Mini-Exercise 3-4

3-30

Mini-Exercise 3-5

3-31

Mini-Exercise 3-13

3-32 through 3-33

Mini-Exercise 3-14

3-34 through 3-35

Summary of Related Video Program

Spotlight Video Series

Chapter 3 – Time is Money (approximately 4:00)

This video program covers time period assumption. In 2000 and 2001, Computer Associates violated the

time period assumption to present a picture of smooth steady growth. This video illustrates the effect of

shifting sales from one period to another and asks students to discuss its impact.

Chapter Summary

LO 3-1 Describe common operating transactions and select appropriate income statement account

titles.

• The income statement reports the effects of transactions that affect net income, which includes

Revenues—amounts charged to customers for sales of goods or services provided.

Expenses—costs of business activities undertaken to earn revenues.

• See Exhibit 3.2 for basic income statement format.

LO 3-2 Explain and apply the revenue and expense recognition principles.

• The two key concepts underlying accrual basis accounting and the income statement are

Revenue recognition principle—recognize revenues when they are earned, regardless of

when cash is received.

Expense recognition (“matching”) principle—recognize expenses when they are incurred in

generating revenue, regardless of when cash is paid.

LO 3-3 Analyze, record, and summarize the effects of operating transactions, using the accounting

equation, journal entries, and T-accounts.

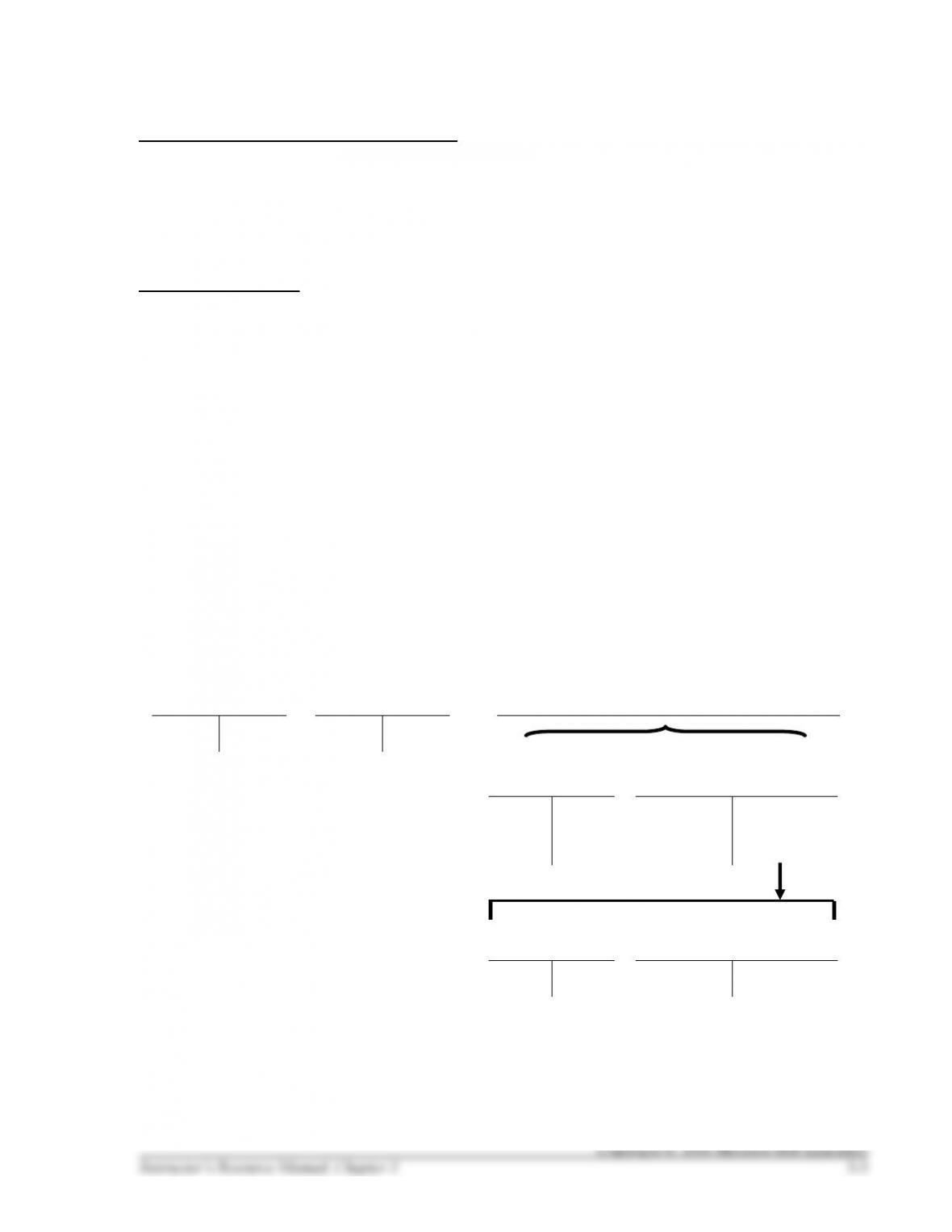

• The expanded transaction analysis model includes revenues and expenses as subcategories of

Retained Earnings. Increases, decreases, and normal account balances (dr or cr) are shown below:

ASSETS

=

LIABILITIES

+

STOCKHOLDERS’ EQUITY

+

dr

–

cr

–

dr

+

cr

Common

Stock

Retained Earnings

–

dr

+

cr

–

dr

+

cr

Net

Income

Revenues

(and Gains)

Expenses

(and Losses)

–

dr

+

cr

+

dr

–

cr

Chapter Summary, continued

LO 3-4 Prepare an unadjusted trial balance.

• The unadjusted trial balance is a list of all accounts and their unadjusted balances, and is used to

check on the equality of recorded debits and credits.

LO 3-5 Evaluate net profit margin, but beware of income statement limitations.

• Net profit margin expresses net income as a percentage of total revenues.

• The income statement indicates whether the company is profitable, but this might not explain

whether cash increased or decreased.

• Does not directly measure the change in value of a company during the period.

• Estimation plays a key role when measuring income.

Accounting Decision Tools

Net Profit Margin = Net Income ÷ Total Revenues

• It tells you how much profit is earned from each dollar of revenue.

• A higher ratio means better performance.

Chapter Outline

Teaching Notes

I. Understand the Business

LO 3-1 Describe common operating transactions and select appropriate income statement account

titles.

A. Operating Activities

1. Operating activities—The day-to-day functions involved

in running a business; include:

Illustrated in Exhibit 3.1

a. Buying goods and services from suppliers and

employees.

b. Selling goods and services to customers and collecting

cash from them.

2. Most businesses have the same steps in their operating

cycles; however, the length of time for each step varies

from company to company.

3. Operating activities are the primary source of revenues

and expenses and, thus, can determine whether a

company earns a profit (or incurs a loss).

B. Income Statement Accounts

Examples provided in

1. Revenues––Amounts earned by selling goods or services

to customers; reported first in the income statement.

Exhibit 3.2

2. Expenses––Costs of operating the business that are

incurred to earn revenues; reported after revenues in the

income statement.

3. Net income––The excess of revenues over expenses;

amount by which stockholders’ equity increases as a

result of profitable operations.

Stress that net income is a

total and not an account

C. The time period assumption assumes that the long life of a

company can be divided into shorter time periods, such as

months, quarters, and years.

The “Stoplight on Ethics”

feature notes that some

managers haven’t learned the

1. Key distinction between the income statement and the

balance sheet:

time period assumption

a. The revenues and expenses on an income statement

report the financial impact of activities in just the

current period.

b. Items on a balance sheet will continue to have a

financial impact beyond the end of the current period.

2. Balance sheet accounts are considered permanent

whereas income statement accounts are considered

temporary.

II. Study the Accounting Methods

A. Cash Basis Accounting

1. Cash basis accounting––Reports revenues when cash is

received and expenses when cash is paid.

2. Doesn’t measure financial performance very well when

transactions are conducted using credit rather than cash.

3. Not likely to correspond to the business activities that

actually occur during a given period; leads to a rather

distorted view of the company’s financial performance.

Chapter Outline

Teaching Notes

B. Accrual Basis Accounting

1. Accrual basis accounting––Reports revenues when they

are earned and expenses when they are incurred,

regardless of the timing of cash receipts or payments.

a. Produces a better measure of the profits arising from

the company’s activities.

b. Only acceptable method for external reporting of

income according to GAAP and IFRS.

c. The cash basis is sometimes used by some small

companies.

LO 3-2 Explain and apply the revenue and expense recognition principles.

2. Revenue Recognition Principle

a. Revenue principle—The requirement under accrual

basis accounting to record revenues when they are

earned, not necessarily when cash is received for

them.

❖ Spotlight Video Series –

Chapter 3

i. Recognized means revenues are measured and

recorded in the accounting system.

ii. Earned means the company has fulfilled its

performance obligation to the customer by doing

what it promised to do.

b. All companies expect to receive cash in exchange for

providing goods and services; timing of cash receipts

does not dictate when revenues are recognized.

Timing of reporting revenue

versus cash receipts

illustrated in Exhibit 3.5

c. Timing of related transactions:

i. Cash before sale/service—Cash received is

reported but company hasn’t provided the

promised goods or services, so no revenue is

recorded yet.

• The obligation to provide the promised goods

or service is a liability called Unearned

Revenue.

• Unearned Revenue––A liability representing

a company’s obligation to provide goods or

services to customers in the future.

• Revenue will be reported later, when the goods

or services are provided.

ii. Cash with sale/service—Cash and revenue are

reported at the same time.

The “Spotlight on Financial

Reporting” feature sets forth

iii. Sale/service before, and cash after—Revenue is

reported since the company has provided the

promised goods or services, but cash hasn’t been

received.

The revenue recognition

policy of Take-Two

Interactive Software, Inc.

• Occurs when a company sells on account.

• The company provides goods or services to a

customer for the right to collect cash in the

future; right is the asset Accounts Receivable.

Chapter Outline

Teaching Notes

3. Expense Recognition Principle

a. Expense recognition principle (“matching”)—The

practice under accrual basis accounting to record

expenses in the same period as the revenues they

generate, not necessarily the period in which cash is

paid for them.

Timing of reporting expenses

versus cash payments

illustrated in Exhibit 3.6

b. If an expense cannot be directly associated with

revenues, it is recorded in the period that the

underlying business activity occurs.

c. Timing of related transactions:

i. Cash before expense—It is common for businesses

to pay for something that provides benefits only in

future periods.

• The company might buy office supplies now

but not use them until next month.

• The expense from using these supplies is

reported next month, when the supplies are

used; this month, the supplies represent an

asset (Supplies).

• Similar situations arise when a company

prepays rent or insurance this month and uses

up these assets in a later month.

ii. Cash with expense—Expenses are sometimes paid

for in the period that they arise.

• The company may arrange to make automatic

payments to a utility company at the end of

each month.

• Because the electricity is used up in the current

month, it is an expense of the current month.

iii. Expense before, and cash after—Many costs are

paid after receiving and using goods or services.

• Because the cost of the goods or services

obtained relates to revenues earned this month,

it represents an expense that will be reported

on this month’s income statement.

• Because the cost has not yet been paid at the

end of the month, the balance sheet reports a

corresponding liability called Accounts

Payable.

• Similar situations arise when employees work

in the current period but are not paid until the

following period; this period’s wages are

reported as Wages Expense on the income

statement and any unpaid wages are reported

as Wages Payable on the balance sheet.

Chapter Outline

Teaching Notes

LO 3-3 Analyze, record, and summarize the effects of operating transactions, using the accounting

equation, journal entries, and T-accounts.

C. The Expanded Accounting Equation

1. Stockholders’ equity includes:

a. Common Stock, given to stockholders when they

contribute capital to the company.

b. Retained earnings, generated by the company itself

through profitable operations.

2. Because revenues and expenses as subcategories within

retained earnings, they are affected by debits and credits

in the same way as all stockholders’ equity accounts:

a. Increases in stockholders’ equity are on the right.

Revenues increase stockholders’ equity, so revenues

are recorded on the right (credit).

Illustrated in Exhibit 3.7

b. Decreases in stockholders’ equity are recorded on the

left. Expenses decrease net income and retained

earnings, so expenses are recorded on the left (debit).

D. Transactions Analysis, Recording, and Summarizing

(a) Provide services for cash—In September, SonicGateway

sold $3,000 of games at its online store; customers paid

when the games were downloaded.

✓ Supplemental Enrichment

Activity (Activity) #1

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) +3,000 = Sales Revenue (R, SE) +3,000

2. Record:

Refer to illustrations of

Cash (+A)

3,000

Sales Revenue (+R, +SE)

3,000

transactions in textbook for

Step 3 – Summarize (which

(b) Receive cash for future services – SonicGateway sold

three $100 gift cards at the beginning of September.

includes posting to T–

accounts).

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) + 300 = Unearned Revenue (L) + 300

2. Record:

Cash (+A)

300

Unearned Revenue (+L)

300

(c) Sells apps on credit—SonicGateway sold $9,000 of apps

on the App Store and on Google Play; Apple and Google

will release customer payments to SonicGateway later in

the month.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Accounts Receivable (A) +9,000 = Sales Revenue (R,

SE) +9,000

2. Record:

Accounts Receivable (+A)

9,000

Sales Revenue (+R, +SE)

9,000

Chapter Outline

Teaching Notes

(d) Receive payment on account—SonicGateway received

checks totaling $8,500 from Apple and Google, on

account.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) +8,500 + Accounts Receivable (A) –8,500

= 0

2. Record:

Cash (+A)

8,500

Accounts Receivable (–A)

8,500

(e) Pay cash to employees—SonicGateway wrote checks to

employees, totaling $7,800 for wages related to hours

worked in September.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) –7,800 = Salaries and Wages Expense (E,

SE) –7,800

2. Record:

Salaries and Wages Expense

(+E, –SE)

7,800

Cash (–A)

7,800

(f) Pay cash in advance—On September 1, SonicGateway

paid $7,200 in advance for September, October, and

November rent.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) –7,200 + Prepaid Rent (A) +7,200 = 0

2. Record:

Prepaid Rent (+A)

7,200

Cash (–A)

7,200

(g) Incur cost to be paid later—SonicGateway displayed

Facebook sidebar ads in September, and received a bill

for $500 to be paid in October.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

0 = Accounts Payable (L) +500 + Advertising

Expense (E, SE) –500

2. Record:

dr Advertising Expense (+E, –SE)

500

cr Accounts Payable (+L)

500

(h) Pay cash for expenses—SonicGateway was notified by its

bank that an automatic payment of $600 was transmitted

to its utility company for electricity use in September.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) –600 = Utility Expense (E, SE) –600

2. Record:

Utilities Expense. (+E, –SE)

600

Accounts Payable (+L)

600

Chapter Outline

Teaching Notes

E. Calculating Account Balances

1. After entering (“posting”) the effects of each journal

entry into the T-accounts, the ending balances are

calculated.

2. Ending balance in each account is amount by which the

total of the increase (+) side exceeds the total of the

decrease (–) side.

LO 3-4 Prepare an unadjusted trial balance.

F. Unadjusted Trial Balance

✓ Activity #2

1. After summarizing journal entries in the various accounts

and then calculating ending balances for each account, an

unadjusted trial balance is prepared.

2. Trial balance––An internal report that lists all accounts

and their balances to check on the equality of the total

recorded debits and total recorded credits.

Illustrated in Exhibit 3.9

3. Income statement accounts follow balance sheet

accounts.

4. Ending balances obtained from ledger (T-accounts) are

listed in the appropriate debit or credit column and

columns are totaled.

a. If the trial balance does not balance, look at the

difference between total debits and credits.

b. If the trial balance does balance, it’s still possible that

you’ve made an error. An entry might include the

wrong account or have been posted to the wrong

account in the general ledger.

5. If title says “unadjusted trial balance” then several

adjustments will have to be made at the end of the

accounting period to update the accounts.

The adjustments will be

covered in chapter 4.

G. Review of Revenues and Expenses

1. Remember that revenues are recorded when the business

fulfills its promise to provide goods or services to

customers, which is not necessarily the same time that

cash is received.

2. Under accrual accounting, expenses are recorded when

incurred (by using up the economic benefits of acquired

items). Expenses are not necessarily incurred at the same

time that cash is paid.