Fundamentals of Financial Accounting, 5/e 2-50

PB2-3 (continued)

Req. 7

Starbucks Apple

Current Ratio = $5,460* = 1.01 Current Ratio = $73,300 = 1.68

$5,380** $43,700

ANSWERS TO SKILLS DEVELOPMENT CASES

S2-1

1. D

S2-2

Req. 1

Lowe’s:

Assets = Liabilities + Shareholders’ Equity

$32,732,000,000 = $20,879,000,000 + $11,853,000,000

The Home Depot:

Assets = Liabilities + Shareholders’ Equity

S2-2 (continued)

Req. 4

Financing for the Lowe’s investment in assets has come more from liabilities than

stockholders’ equity. Lowe’s liabilities have financed $20,879,000,000 of the total

assets of the company and stockholders’ equity has financed $11,853,000,000.

The more the company has in assets and the less it has in liabilities, the more likely the

S2-3

S2-4

Req. 1

Assets = Liabilities + Stockholders’ Equity

$15,000 = $15,000 + 0

Ponzi received $15,000 cash ($5,000 from each of the three lenders) in exchange for a

promise to repay that money in 90 days. The 50% interest that Ponzi is paying is not a

S2-5

Req. 1

The president is concerned with the amount of assets that are reported on the balance

sheet because investors and creditors judge the riskiness of the company by comparing

the amount of recorded assets to liabilities. The greater the amount of the company’s

assets for a given amount of liabilities, the less risky the company appears to investors

and creditors.

Req. 2

Fundamentals of Financial Accounting, 5/e 2-55

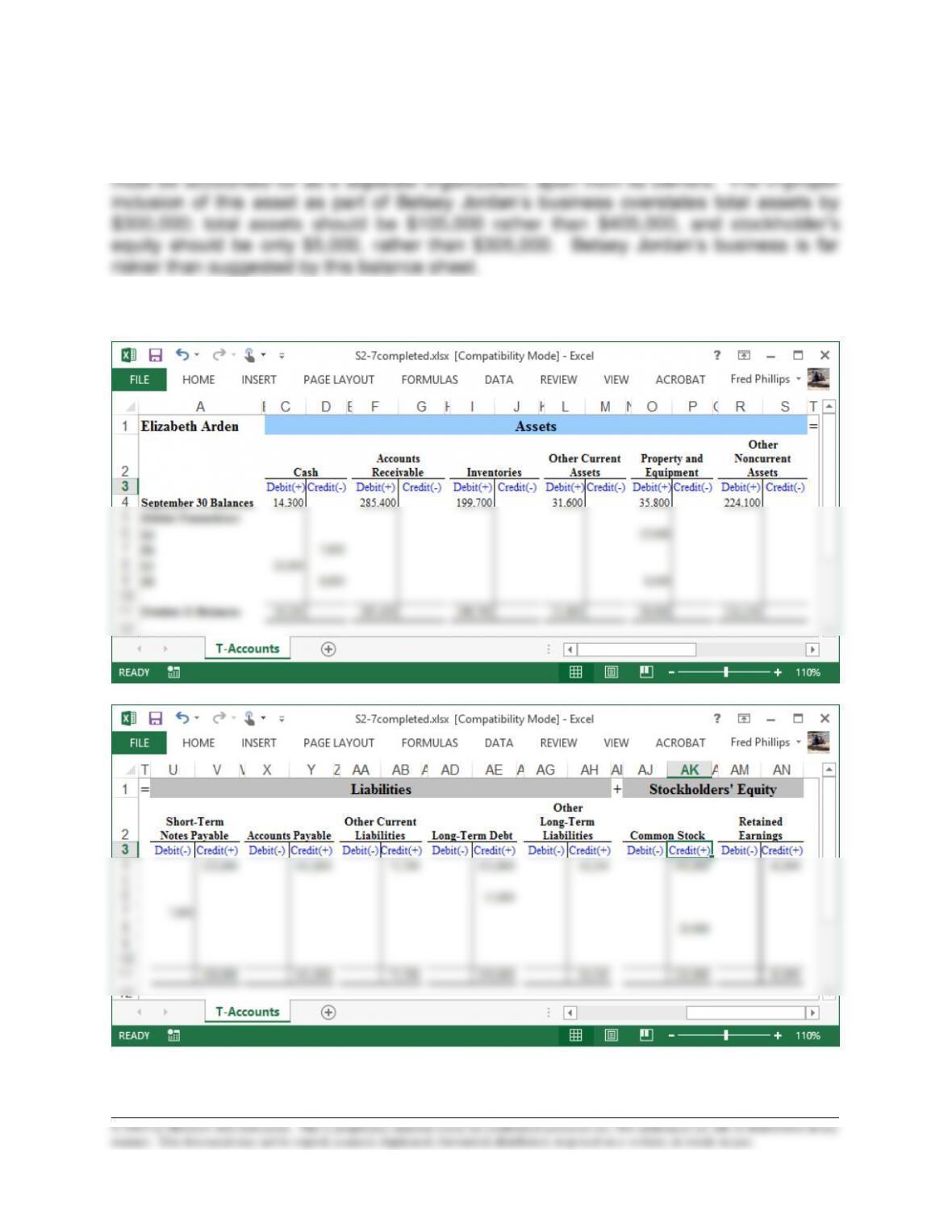

S2-6

The major deficiency in this balance sheet is the inclusion of the owner’s personal

residence as a business asset. Under the separate entity assumption, each business

S2-7

ANSWERS TO CONTINUING CASE

CC2-1

Req. 1

a.

Cash (+A) …………………………………………………………………

80,000

Common Stock (+SE) ……………………………………………

80,000

b.

Land (+A) ………………………………………………………………….

9,000

Cash (-A) ………………………………………………………………

2,000

Note Payable (long-term) (+L) …………………………..……..

7,000

c.

This is an exchange of only promises, so it is not a

transaction.

d.

Equipment (+A) …………………………………………………………

18,000

Cash (-A) ……………………………………………………………..

18,000

e.

Supplies (+A) ……………………………………………………………..

1,000

Accounts Payable (+L) ………………………………………

1,000

f.

Accounts Payable (-L) …………………………………………………

350

Cash (-A) …………………………………………………………

350

g.

No transaction. Separate entity assumption.

Cash (A)

Supplies (A)

Equipment (A)

Beg.

0

Beg.

0

Beg.

0

(a)

80,000

2,000

(b)

(e)

1,000

(d)

18,000

18,000

(d)

350

(f)

End.

59,650

End.

1,000

End.

18,000

Land (A)

Beg.

0

(b)

9,000

End.

9,000

Accounts Payable (L)

0

Beg.

(f)

350

1,000

(e)

650

End.

Notes Payable

(long-term) (L)

0

Beg.

7,000

(b)

7,000

End.

Common Stock (SE)

0

Beg.

80,000

(a)

80,000

End.

Fundamentals of Financial Accounting, 5/e 2-57

CC2-1 (Continued)

Req. 3

NICOLE’S GETAWAY SPA

Balance Sheet

At April 30

Assets

Current Assets

Cash

Supplies

Total Current Assets

Equipment

Land

Total Assets

$ 59,650

1,000

60,650

18,000

9,000

$ 87,650

Liabilities

Current Liabilities

Accounts Payable

Total Current Liabilities

Notes Payable

Total Liabilities

$ 650

650

7,000

7,650

Stockholders’ Equity:

Common Stock

Retained Earnings

Total Stockholders’ Equity

80,000

0

80,000

Total Liabilities and Stockholders’ Equity

$ 87,650

Req. 4

The current ratio indicates the proportion of current assets relative to current liabilities.