E2–11

Req. 1

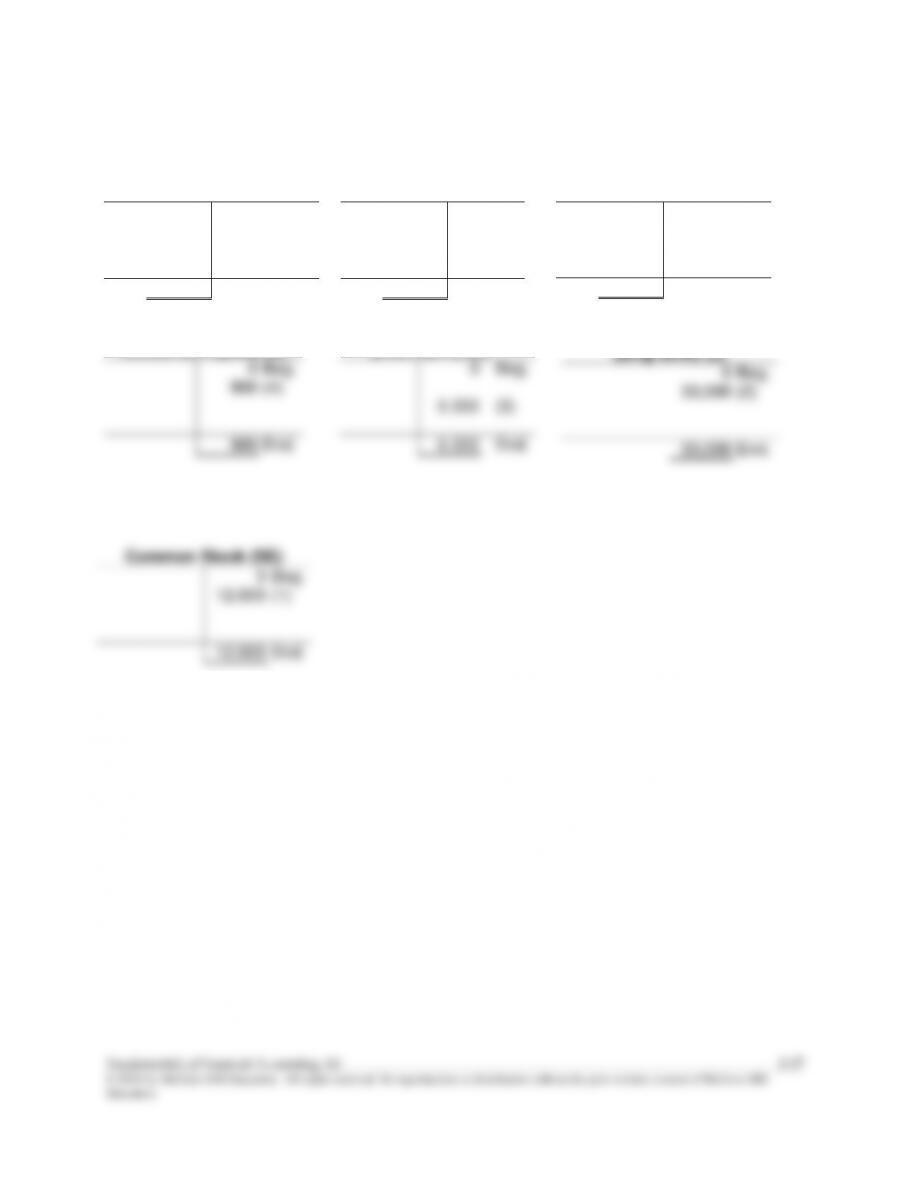

Assets

Liabilities

Stockholders’ Equity

Cash

Equipment

Accounts

Payable

ST Notes

Payable

LT Notes

Payable

Common Stock

Beg.

0

0

0

0

0

0

a.

+60,000

+60,000

b.

+20,000

+20,000

c.

No transaction, therefore no financial effects to record.

d.

-2,000

+9,000

+7,000

e.

-8,000

+16,000

+8,000

End.

70,000

25,000

8,000

7,000

20,000

60,000

Req 2:

a.

Cash (+A) ………………………………………………………………….

60,000

Common Stock (+SE) …………………………………………….

60,000

Cash (+A) ………………………………………………………………….

Equipment (+A) …………………………………………………………

Note Payable (short-term) (+L)…………………………………

Equipment (+A) ………………………………………………………….

Accounts Payable (+L) ……………………………………………

Fundamentals of Financial Accounting, 5/e 2-22

E2-11 (continued)

Req. 3:

DOWN.COM

Balance Sheet

At May 31

Assets

Liabilities

Current Assets

Current Liabilities

Cash

$ 70,000

Accounts Payable

Note Payable (short-term)

$ 8,000

7,000

Total Current Assets

70,000

Total Current Liabilities

15,000

Noncurrent Assets

Note Payable (long-term)

20,000

Equipment

25,000

Total Liabilities

35,000

Total Assets

$ 95,000

Stockholders’ Equity

Common Stock

Retained Earnings

60,000

0

Total Stockholders’ Equity

60,000

Total Liabilities & Stockholders’

Equity

$ 95,000

Fundamentals of Financial Accounting, 5/e 2-23

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

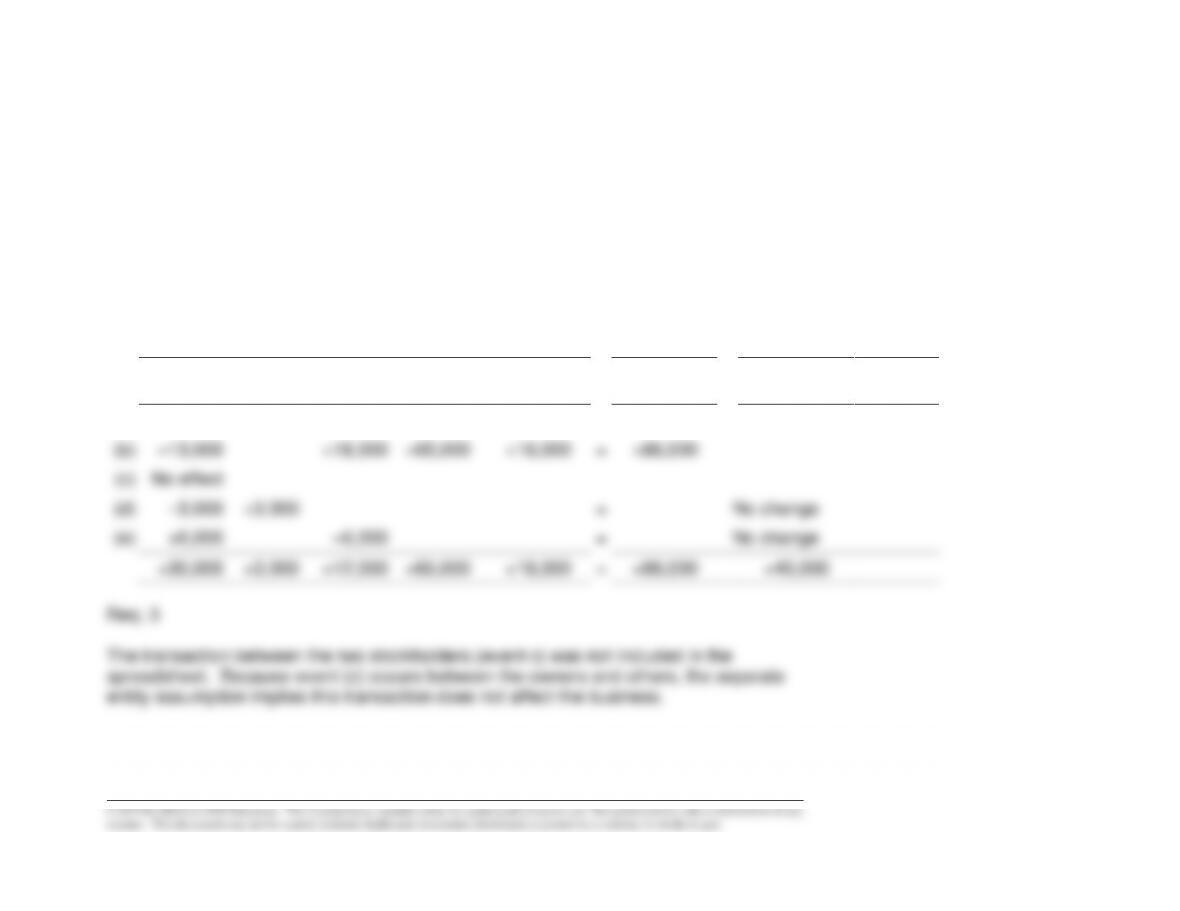

E2–12

Req. 1

Assets

=

Liabilities

+

Stockholders’

Equity

Cash

Equipment

Land

Accounts

Payable

Notes

Payable

Common Stock

(a)

+40,000

=

+40,000

(b)

+12,000

=

+12,000

(c)

-2,000

+20,000

=

+18,000

(d)

-2,000

+2,000

=

(e)

No change*

No change

+36,000

+22,000

+12,000

=

+30,000

+40,000

*Event (e) is not considered a transaction of the company because the separate entity

assumption (from Chapter 1) states that transactions of the owners are separate from

transactions of the business.

Req. 2

a.

Cash (+A) ………………………………………………………………….

40,000

Common Stock (+SE) …………………………………………….

40,000

b.

Land (+A) …………………………………………………………………..

12,000

Note Payable (long-term) (+L) ………………………………….

12,000

c.

Equipment (+A) …………………………………………………………

20,000

Cash (-A) ………………………………………………………………

2,000

Note Payable (long-term) (+L) ………………………………….

18,000

d.

Equipment (+A) …………………………………………………………

2,000

Cash (-A) ………………………………………………………………

2,000

e.

This is not a transaction of the business, so a journal entry is not needed.

E2-12 (continued)

Req. 3

Cash (A)

Equipment (A)

Beg.

0

Beg.

0

(a)

40,000

2,000

(c)

(c)

20,000

2,000

(d)

(d)

2,000

End.

36,000

End.

22,000

Land (A)

Beg.

0

(b)

12,000

End.

12,000

0

Beg.

Beg.

12,000

(b)

(a)

18,000

(c)

30,000

End.

End.

Assets

Liabilities

Current Assets

Notes Payable (long-term)

Equipment

Fundamentals of Financial Accounting, 5/e 2-25

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E2–13

Transaction

Brief Explanation

(a)

Issued common stock for $17,000 cash.

(b)

Purchased a building for $50,000; paid $10,000 cash and gave a

$40,000 note payable for the balance.

(c)

Used cash to purchase supplies costing $1,500.

E2–14

Req. 1

September 30, 2013 December 31, 2012

Current Ratio = $1,180,200 = 4.36 Current Ratio = $1,122,600 = 4.45

$ 270,700 $ 252,100

Req. 2

E2–15

Req. 1

Assets

=

Liabilities

+

Stockholders’ Equity

1.

Cash

+12,000

=

Common

Stock

+12,000

2.

Cash

+30,000

=

Note Payable

(long–term)

+30,000

3.

Equipment

Cash

+40,000

– 35,000

=

Note Payable

(short-term)

+5,000

4.

Supplies

+900

=

Accounts Payable

+900

Req. 2

1.

Cash (+A) ………………………………………………………………….

12,000

Common Stock (+SE) …………………………………………….

12,000

2.

Cash (+A) ………………………………………………………………….

30,000

Note Payable (long-term) (+L) ………………………………….

30,000

Equipment (+A) …………………………………………………………

Note Payable (short-term) (+L)…………………………………

Supplies (+A) ……………………………………………………………..

E2–15 (continued)

Req. 2 (continued)

Cash (A)

Supplies (A)

Beg.

0

Beg.

0

(1)

12,000

35,000

(3)

(4)

900

(2)

30,000

End.

7,000

End.

900

Accounts Payable (L)

Notes Payable

(short-term) (L)

0

Beg.

0

Beg.

900

(4)

5,000

(3)

900

End.

5,000

End.

Equipment (A)

Beg.

0

(3)

40,000

End.

40,000

Common Stock (SE)

0

Beg.

12,000

(1)

12,000

End.

Notes Payable

(long-term) (L)

0

Beg.

30,000

(2)

30,000

End.

Fundamentals of Financial Accounting, 5/e 2-28

E2–15 (continued)

Req. 3 BUSINESS SIM CORP.

Balance Sheet

At September 30

Assets

Liabilities

Current Assets

Current Liabilities

Cash

$ 7,000

Accounts Payable

$ 900

Supplies

900

Note Payable

5,000

Total Current Assets

7,900

Total Current Liabilities

5,900

Note Payable

30,000

Total Liabilities

35,900

Stockholders’ Equity

Equipment

40,000

Common Stock

12,000

Retained Earnings

0

Total Stockholders’ Equity

12,000

Total Assets

$ 47,900

Total Liabilities &

Stockholders’ Equity

$ 47,900

Req. 4

At September 30, BSC reported $7,900 of current assets and $5,900 of current

Fundamentals of Financial Accounting, 5/e 2-29

ANSWERS TO COACHED PROBLEMS

CP2-1

Req. 1

Ag BioTech was organized as a corporation. Only a corporation issues shares of stock

to its owners in exchange for their investment, as ABT did in transaction (a).

Req. 2

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Supplies

Land

Building

Equipment

Note

Payable

Common

Stock

Retained

Earnings

(a)

+40,000

=

+40,000

(b)

–13,000

+18,000

+65,000

+16,000

=

+86,000

(c)

No effect

(d)

–3,000

+3,000

=

No change

(e)

+6,000

–6,000

=

No change

+30,000

+3,000

+12,000

+65,000

+16,000

=

+86,000

+40,000

Req. 3

The transaction between the two stockholders (event c) was not included in the

spreadsheet. Because event (c) occurs between the owners and others, the separate

entity assumption implies this transaction does not affect the business.

Fundamentals of Financial Accounting, 5/e 2-30

CP2-1 (Continued)

Req. 4

(a) Total assets = $30,000 + $3,000 + $12,000 + $65,000 + $16,000

= $126,000

CP2-2

Req. 1

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Supplies

Building

Equip

Land

Accounts

Payable

Notes

Payable

Common

Stock

Retained

Earnings

16,000

5,000

200,000

18,000

90,000

=

4,000

17,000

308,000

0

a.

+200,000

=

+200,000

b.

+30,000

=

+30,000

c.

–41,000

+141,000

=

+100,000

d.

–100,000

+100,000

=

e.

+10,000

+10,000

105,000

15,000

341,000

118,000

90,000

=

14,000

147,000

508,000

0