Chapter Outline

Teaching Notes

d. To find ending account balance, express the T-account

as equations:

Start with beginning balance

Add “+” side

Subtract “–” side

Equals ending balance

“Spotlight on Financial

Reporting” feature addresses

the impact of needing extra

time to prepare financial

statements

e. Ending balance is double underscored to distinguish it.

E. SonicGateway’s Accounting Records

(a) Issue Stock to Owners––Scott incorporates

SonicGateway and the company issues common stock to

Scott and Angus as evidence of their contribution of

$10,000 cash, which is deposited in the company’s bank

account.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) +10,000 = Common Stock (SE) +10,000

Refer to illustrations of

transactions (a) through (g)

2. Record:

in textbook for Step 3—

Debit

Credit

Cash (+A)

10,000

Common Stock (+SE)

10,000

Summarize (which includes

posting to T-accounts).

(b) Invest in Equipment––SonicGateway pays $300 cash for

the company’s logo.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) –300; Logo and Trademarks (A) +300 = 0

2. Record:

Debit

Credit

Logo and Trademarks (+A)

300

Cash (–A)

300

(c) Obtain Loan from Bank––SonicGateway borrows

$20,000 from a bank and signs a formal agreement to

repay the loan in two years (on September 1, 2017).

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) +20,000 = Note Payable (long-term) (L)

+20,000

2. Record:

Debit

Credit

Cash (+A)

20,000

Note Payable (long-term) (+L)

20,000

(d) Invest in Equipment––SonicGateway purchases and

receives $9,600 in computers, printers, and desks, signing

a purchase order to indicate its promise to pay $9,600 at

the end of the month.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Equipment (A) +9,600 = Accounts Payable +9,600

2. Record:

Debit

Credit

Equipment (+A)

9,600

Accounts Payable (+L)

9,600

Chapter Outline

Teaching Notes

(e) Pay Supplier––SonicGateway pays $5,000 to the

equipment supplier in (d).

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash –5,000 = Accounts Payable –5,000

2. Record:

Debit

Credit

Accounts Payable (–L)

5,000

Cash (–A)

5,000

(f) Order Software for App––SonicGateway signs a contract

with a programmer for program code for the Static

Charge game app for $9,000. No code has been received

yet.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

No change = No change

2. Record––No journal entry is needed.

(g) Receive Software––SonicGateway receives the $9,000 of

app game code ordered in (f); pays $4,000 cash, and

promises to pay the remaining $5,000 next month.

1. Analyze: Assets = Liabilities + Stockholders’ Equity

Cash (A) –4,000 + Software (A) +9,000 = Accounts

Payable (L) +5,000

2. Record:

Debit

Credit

Software (+A)

9,000

Cash (–A)

4,000

Accounts Payable (+L)

5,000

(h) Receive Supplies––SonicGateway receives supplies

costing $600 on account.

1. Analyze:

Assets = Liabilities + Stockholders’ Equity

Supplies (A) +600 = Accounts Payable (L) +600

2. Record:

Debit

Credit

Supplies (+A)

600

Accounts Payable (+L)

600

LO 2-4 Prepare a trial balance and a classified balance sheet.

F. Preparing a Trial Balance and a Balance Sheet

✓ Activity #6

1. The trial balance lists the ending balance in every T-

account and then computes total debits and total credits;

when the column totals are equal, a balance sheet can be

prepared.

2. Classified balance sheet––A balance sheet that shows a

subtotal for current assets and current liabilities.

a. Current assets––To be used up or converted into cash

within 12 months of the balance sheet date.

Chapter Outline

Teaching Notes

b. Current liabilities––Debts and obligations that will

be paid, settled, or fulfilled within 12 months of the

balance sheet date.

c. Noncurrent (or long-term)––Assets and liabilities

that do not meet the definition of current.

III. Evaluate the Results

LO 2-5 Interpret the balance sheet using the current ratio and an understanding of related

concepts.

A. Assessing the Ability to Pay

1. The classified balance sheet format makes it easy to see

whether current assets are sufficient to pay current

liabilities.

The “Spotlight on Financial

Reporting” feature explains

how analysts reacted to

2. The only problem with this approach is that looking at

total dollar amounts can be awkward, especially if we

want to compare across several companies.

Facebook’s high current ratio

and Expedia’s low current

ratio

3. Current Ratio

✓ Activity #7

a. Current assets divided by current liabilities.

b. Used to evaluate the ability to pay liabilities as they

come due in the short run.

c. Generally speaking, a high ratio suggests good

liquidity.

B. Balance Sheet Concepts and Values

1. Some mistakenly believe that the balance sheet reports

what a business is actually worth.

2. In fact, net worth is a term that many accountants and

analysts use when referring to stockholders’ equity.

3. The answer comes from knowing that accounting is based

on recording and reporting transactions:

a. What is (and is not) recorded?

i. Only measurable exchanges are recorded.

ii. Items not acquired in an exchange are not listed on

the balance sheet.

b. What amounts are assigned to recorded items?

i. Following the cost principle, assets and liabilities

are first recorded at cost, which is their cash

equivalent value on the date of the transaction;

later, if an asset’s value:

• Increases––The increase is generally not

recorded under GAAP

• Falls––It is generally reported at that lower

value.

ii. Thus, the amount reported on the balance sheet

may not be the asset’s current value.

Chapter Outline

Teaching Notes

C. A Review of the Accounting Cycle

Summarized in Exhibit 2.15

1. During the accounting period, transactions take place.

a. Picture the documented activity.

b. Name what’s exchanged.

c. Analyze the financial effects.

d. Record a journal entry.

e. Summarize in T-accounts.

2. At the end of accounting period:

a. Prepare a trial balance.

b. Adjust the accounts.

Covered in Chapter 4

c. Prepare financial statements from the trial balance and

distribute to users. (Because the company does not

report any operations here, it prepares only the

balance sheet.)

d. Close the books

Covered in Chapter 4

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 2–1

Use this handout for an in-class activity designed to review the analysis of various business

transactions that affect the balance sheet. The solution follows the handout master.

2. Handout 2–2

This activity is a continuation of Activity #1. Use this handout for an in-class activity designed to

continue the review of the analysis of various business transactions that affect the balance sheet. The

solution follows the handout master.

3. Handout 2–3

Use Handout 2-3 for an in-class activity designed to review the debit/credit framework. Note that

these transactions are the same as those analyzed on Handout 2-1. However, it can be assigned even if

Activity #1 was not assigned. The solution follows the handout master.

4. Handout 2–4

This activity is a continuation of Activity #3. Use this handout for an in-class activity designed to

review the debit/credit framework. Note that these transactions are the same as those analyzed on

Handout 2–2. However, it can be assigned even if Activity #2 was not assigned. The solution follows

the handout master.

5. Handout 2–5

Use this handout for an in-class activity designed to review the posting of various balance sheet

transactions to T-accounts. This activity is a continuation of Activity #3 and Activity #4; it should be

assigned only if both of those activities were assigned. The solution follows the handout master.

6. Handout 2–6

Use this handout for an in-class activity designed to review the preparation of a trial balance and a

classified balance sheet. This activity is a continuation of Activity #5; it should be assigned only if

that activity was assigned. The solution follows the handout master.

7. Use Handout 2–7

Use this handout for an in-class activity designed to review the calculation and interpretation of the

current ratio. This activity is a continuation of Activity #6; it should be assigned only if that activity

was assigned. The solution follows the handout master.

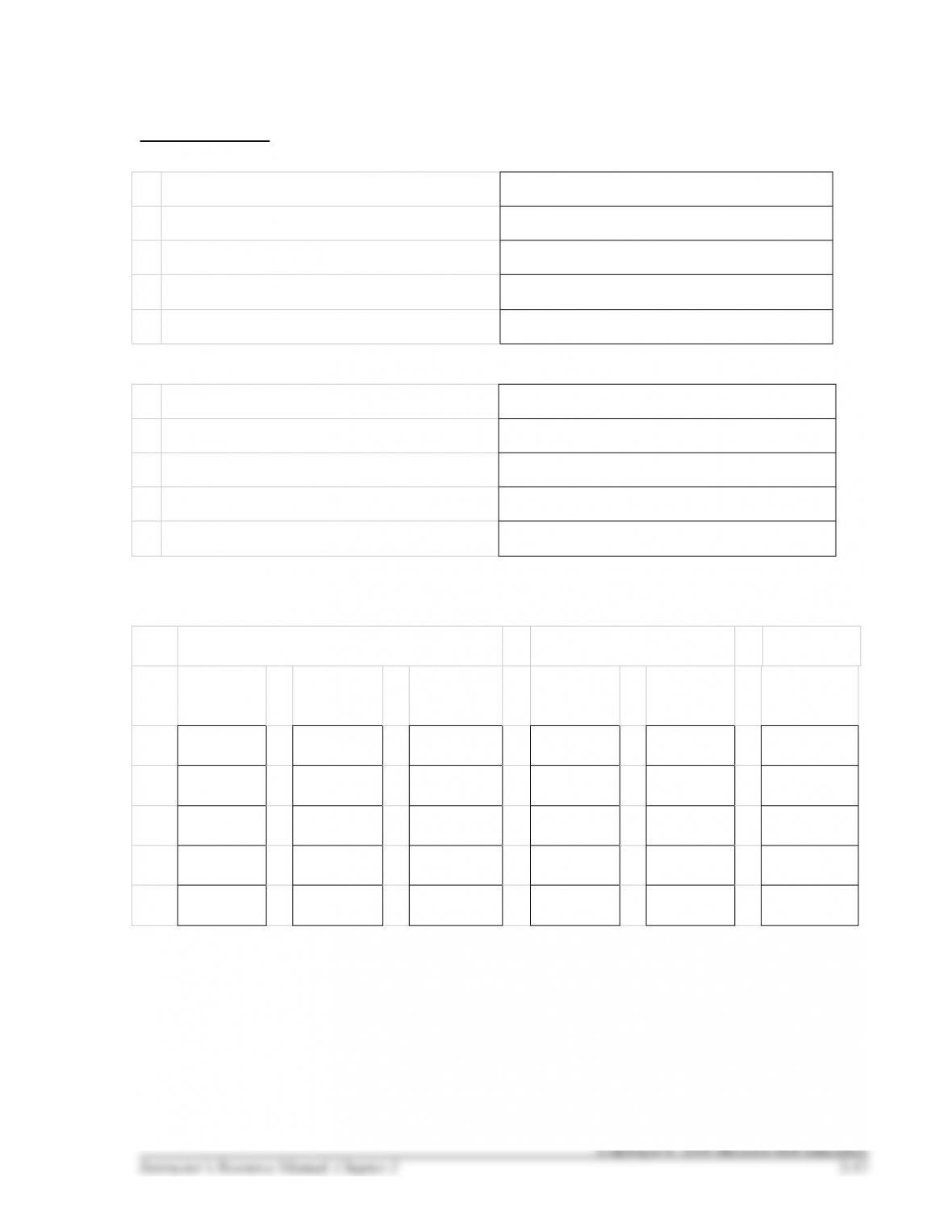

HANDOUT 2–1

ANALYZING TRANSACTIONS

Analyze each of the following transactions by answering each of the questions. Use the spreadsheet on

the following page to keep track of the amount in each account:

(a) Stockholder invests $10,000 into the business in exchange for common stock.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(b) Company borrows $15,000 signing a note payable to the bank that is due in three months.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(c) Receives and pays for a $15,000 truck and $5,000 of equipment.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

HANDOUT 2–1, continued

(d) Purchases $300 of supplies on account.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(e) Signs contract for first website design for $10,000.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

Spreadsheet

Assets

=

Liabilities

+

SE

Ref.

Cash

+

Supplies

+

Property,

Plant &

Equipment

=

Accounts

Payable

+

Notes

Payable

+

Common

Stock

(a)

(b)

(c)

(d)

(e)

HANDOUT 2–1 SOLUTION, continued

ANALYZING TRANSACTIONS

Analyze each of the following transactions by answering each of the questions. Use the spreadsheet on

the following page to keep track of the amount in each account:

(a) Stockholder invests $10,000 into the business in exchange for common stock.

1.

Does a transaction exist?

Yes—received cash and gave stock.

2.

Examine it for accounts affected.

Cash and Common Stock

3.

Classify each account affected.

Cash is an Asset (A) and Common Stock is

Stockholders’ Equity (SE)

4.

Identify direction and amount.

Cash (A) + $10,000 = Stockholders’ Equity (SE) +

$10,000.

5.

Ensure the equation still balances.

Yes—see below.

(b) Company borrows $15,000 signing a note payable to the bank that is due in three months.

1.

Does a transaction exist?

Yes—received cash and gave a note payable.

2.

Examine it for accounts affected.

Cash and Notes Payable

3.

Classify each account affected.

Cash is an Asset (A) and Notes Payable is a Liability (L)

4.

Identify direction and amount.

Cash (A) + $15,000 = Notes payable + $15,000.

5.

Ensure the equation still balances.

Yes—see below.

(c) Receives and pays for a $15,000 truck and $5,000 of equipment.

1.

Does a transaction exist?

Yes—paid cash and received truck and equipment.

2.

Examine it for accounts affected.

Cash and Equipment

3.

Classify each account affected.

Cash is an Asset (A) and Equipment is an Asset (A)

4.

Identify direction and amount.

Cash (A) − $20,000 and Equipment (A) + 20,000

5.

Ensure the equation still balances.

Yes—see below.

HANDOUT 2–1 SOLUTION, continued

(d) Purchases $300 of supplies on account.

1.

Does a transaction exist?

Yes—received supplies and obligated to pay for them.

2.

Examine it for accounts affected.

Supplies and Accounts Payable

3.

Classify each account affected.

Supplies is an Asset (A) and Accounts Payable is a

Liability (L)

4.

Identify direction and amount.

Supplies (A) + $300 and Accounts Payable (L) + $300.

5.

Ensure the equation still balances.

Yes—see below.

(e) Signs contract for first website design for $10,000.

1.

Does a transaction exist?

No—no exchange took place.

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

Spreadsheet

Assets

=

Liabilities

+

Stockholders’

Equity

Ref.

Cash

+

Supplies

+

Equipment

=

Accounts

Payable

+

Notes

Payable

+

Common Stock

(a)

+10,000

=

+10,000

(b)

+15,000

=

+15,000

(c)

–20,000

+20,000

=

(d)

+300

=

+300

Total

5,000

300

20,000

300

15,000

10,000

$25,300

$15,300

$10,000

HANDOUT 2–2

ANALYZING TRANSACTIONS

Analyze the following transactions as set forth below. Use the spreadsheet on the next page to keep track

of the amount in each account:

(f) Pays $300 to the supplier in (d).

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(g) Purchases and pays for $600 of supplies.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(h) Purchases and pays for equipment costing $1,000.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.

(i) Orders a $900 lawn mower, to be delivered next month.

1.

Does a transaction exist?

2.

Examine it for accounts affected.

3.

Classify each account affected.

4.

Identify direction and amount.

5.

Ensure the equation still balances.