13-50 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO SKILLS DEVELOPMENT CASES

S13–1

Answer: D

Calculations:

Fixed Asset Turnover =

Net Revenue

Average Net Fixed Assets

=

$78,812

=

3.32

($23,348 + $24,069) ÷ 2

Days to Sell =

365

Inventory Turnover Ratio

=

365

=

77.3

4.72*

* Inventory Turnover Ratio =

Cost of Goods Sold

Average Inventory

=

$51,422

=

4.72

($11,057 + $10,710) ÷ 2

Debt to Assets =

Total Liabilities

Total Assets

=

$27,996

= 0.69

$40,518

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

S13–2

Req. 1

Lumber

Liquidators

Lowe’s

Difference

Gross Profit

Percentage

41.1%

34.6%

6.5%

The Gross Profit Margin for Lumber Liquidators exceeds that for Lowe’s by 6.5%

Req. 2

Lumber

Liquidators

Lowe’s

Difference

Net Profit Margin

7.7%

4.3%

3.4%

The Net Profit Margin for Lumber Liquidators exceeds that for Lowe’s by 3.4%

Req. 3

Given that the difference between Lumber Liquidators and Lowe’s drops from 6.5% in

requirement 1 (before considering expenses other than cost of goods sold) to 3.4% in

requirement 2 (after considering cost of goods sold), the analyses suggest Lowe’s

controls operating expenses other than cost of goods sold better than Lumber

Liquidators.

S13–3

The solutions to this project will depend on the company and/or accounting period

S13–4

This case encourages thinking critically about evaluating going concern problems.

Many critics who contend that auditors do a poor job of predicting business failures tend

to focus on only the failure to accurately predict instances where businesses do in fact

fail. These critics do not consider the problems that would arise if auditors predicted

business failures that were not likely to occur.

financing that would otherwise help it to survive difficult financial problems. The

company could be forced to accept unfavorable purchase terms from creditors (e.g.,

shorter repayment periods, higher interest rates), which would further amplify the

company’s problems and make it less profitable and less liquid. Essentially, an audit

report that inaccurately predicts business failure could become a “self-fulfilling

S13–5

The current ratio for Capital Investments Corporation (CIC) increased as the result of

S13–6

Req. 1

The ratios that are likely to be affected by alternative depreciation methods are:

1.

Return on equity

5.

Debt to assets

2.

Fixed asset turnover

6.

Price/earnings ratio (P/E ratio)

3.

Earnings per share (EPS)

7.

Times interest earned

4.

Net profit margin

Alternative depreciation methods affect reported noncurrent assets, net income, and

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

S13–7

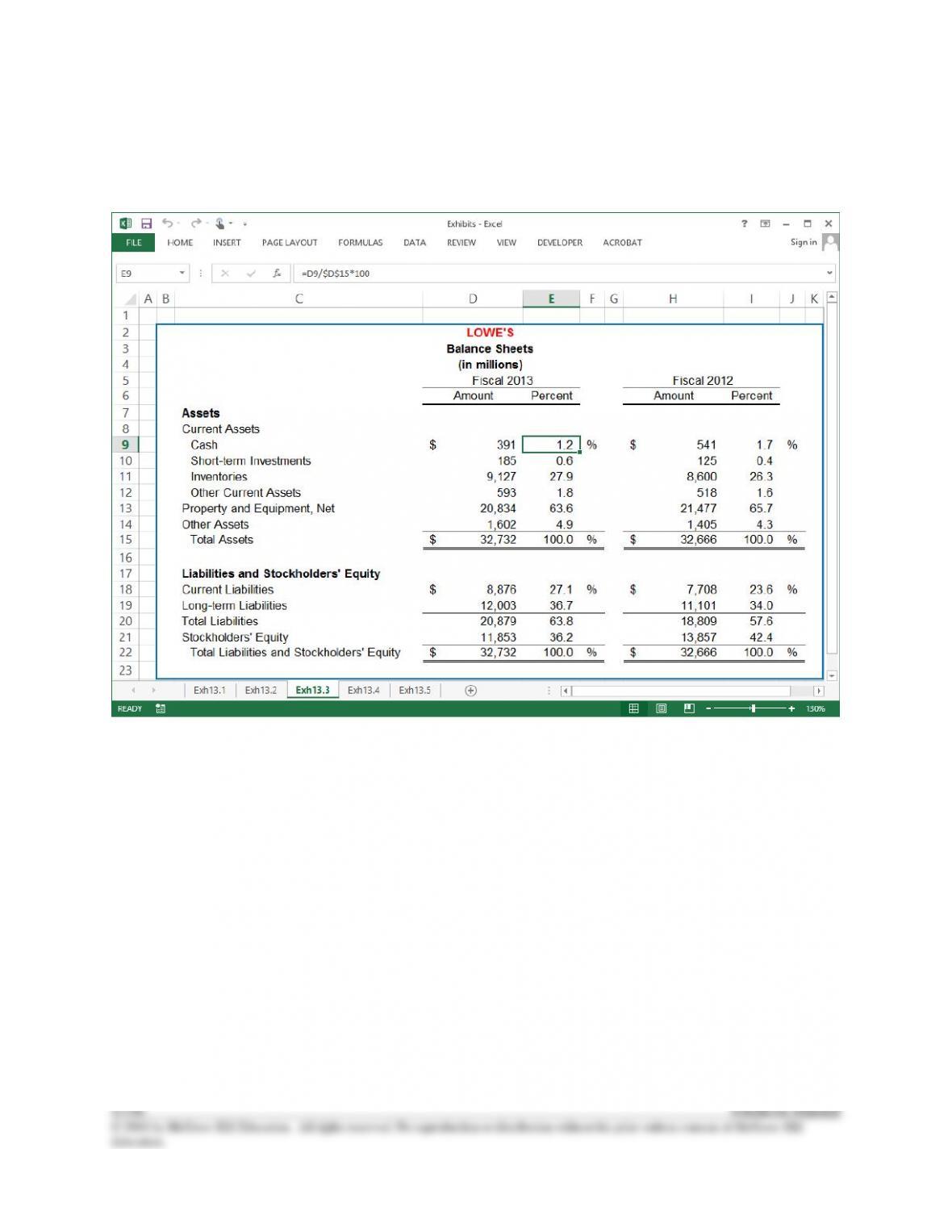

Req. 1

S13–7 (continued)

Req. 2

The formula to calculate the percent of total assets is shown in the formula bar.

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CC13-1

Req. 1

2015

Gross Profit

Percentage

=

Net sales revenue-

Cost of goods sold

x100 =

(56,000 – 48,000)

x 100

= 14.29%

Net sales revenue

56,000

2016

=

(80,000 – 65,000)

x 100

= 18.75%

80,000

2015

Return on

Equity

=

Net income –

Preferred Dividends

x100 =

2,100

x100

= 9.61%

Average

stockholders’ equity

(32,100 +

11,600)/2

2016

=

6,950

x100

= 21.70%

(31,950 +

32,100)/2

2015

Fixed

Asset

Turnover

=

Net revenue

=

56,000

= 1.06

Average net fixed assets

(79,000 + 27,000)/2

2016

=

80,000

= 1.12

(64,000 + 79,000)/2

NGS appears to be more profitable in 2016. The gross profit percentage analysis

2015. The fixed asset turnover ratio was slightly higher in 2016 indicating that NGS was

13-58 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CC13-1 (continued)

Req. 2

2015

Current

Ratio

=

Current Assets

=

11,100

=1.39

Current Liabilities

8,000

2016

=

10,950

=1.37

8,000

By looking at the current ratio, it is difficult to determine in which year NGS was more

2015

Debt to

Assets

=

Total Liabilities

=

58,000

=0.64

Total Assets

90,100

2016

=

43,000

=0.57

74,950

2015

Times

interest

earned

=

Net income + Interest expense

+ Income tax expense

=

(2,100 + 3,100 + 800)

=1.94

Interest expense

3,100

2016

=

(6,950 + 1,000 + 3,050)

=11.00

1,000

NGS was more solvent in 2016. The times interest earned ratio indicates that NGS was