© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP B PROBLEMS

PB13–1

Req. 1

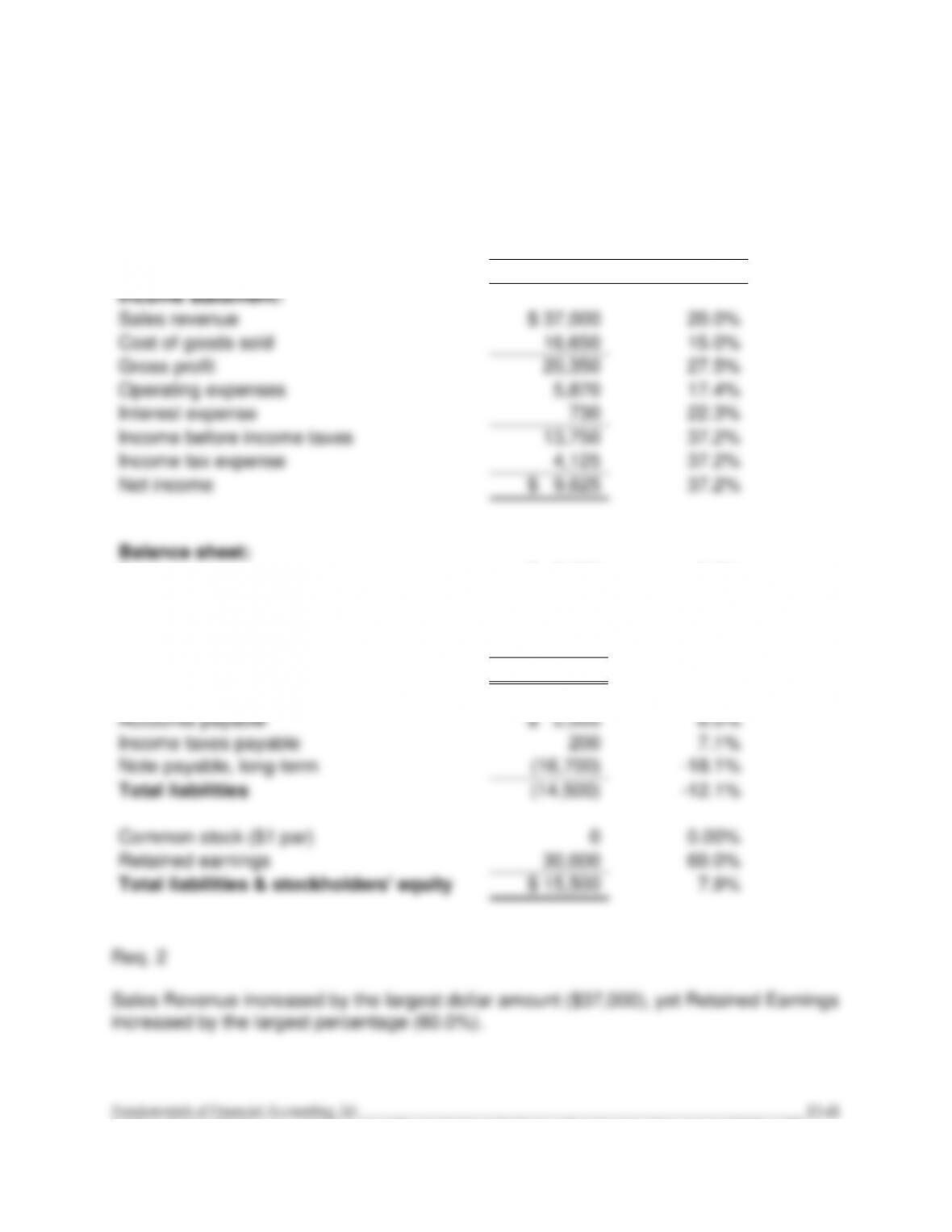

Tiger Audio Horizontal Analysis

Increase (Decrease)

in the current year (versus

the previous year)

Amount

Percentage

Income statement:

Sales revenue

$ 37,000

20.0%

Cost of goods sold

16,650

15.0%

Gross profit

20,350

27.5%

Operating expenses

5,870

17.4%

Interest expense

730

22.3%

Income before income taxes

13,750

37.2%

Income tax expense

4,125

37.2%

Net income

$ 9,625

37.2%

Balance sheet:

Cash

$ 2,000

5.3%

Accounts receivable (net)

2,500

15.6%

Inventory

3,000

13.6%

Property & equipment (net)

8,000

6.7%

Total Assets

$ 15,500

7.9%

Accounts payable

$ 2,000

8.0%

Income taxes payable

200

7.1%

Note payable, long-term

(16,700)

-18.1%

Total liabilities

(14,500)

–12.1%

Common stock ($1 par)

0

0.00%

Retained earnings

30,000

60.0%

Total liabilities & stockholders’ equity

$ 15,500

7.9%

Req. 2

Sales Revenue increased by the largest dollar amount ($37,000), yet Retained Earnings

increased by the largest percentage (60.0%).

PB13–2

Req. 1

Gross Profit Percentage =

Net Sales Revenue – Cost of Goods Sold

Net Sales Revenue

Current Year =

$222,000 – $127,650

=

42.5%

$222,000

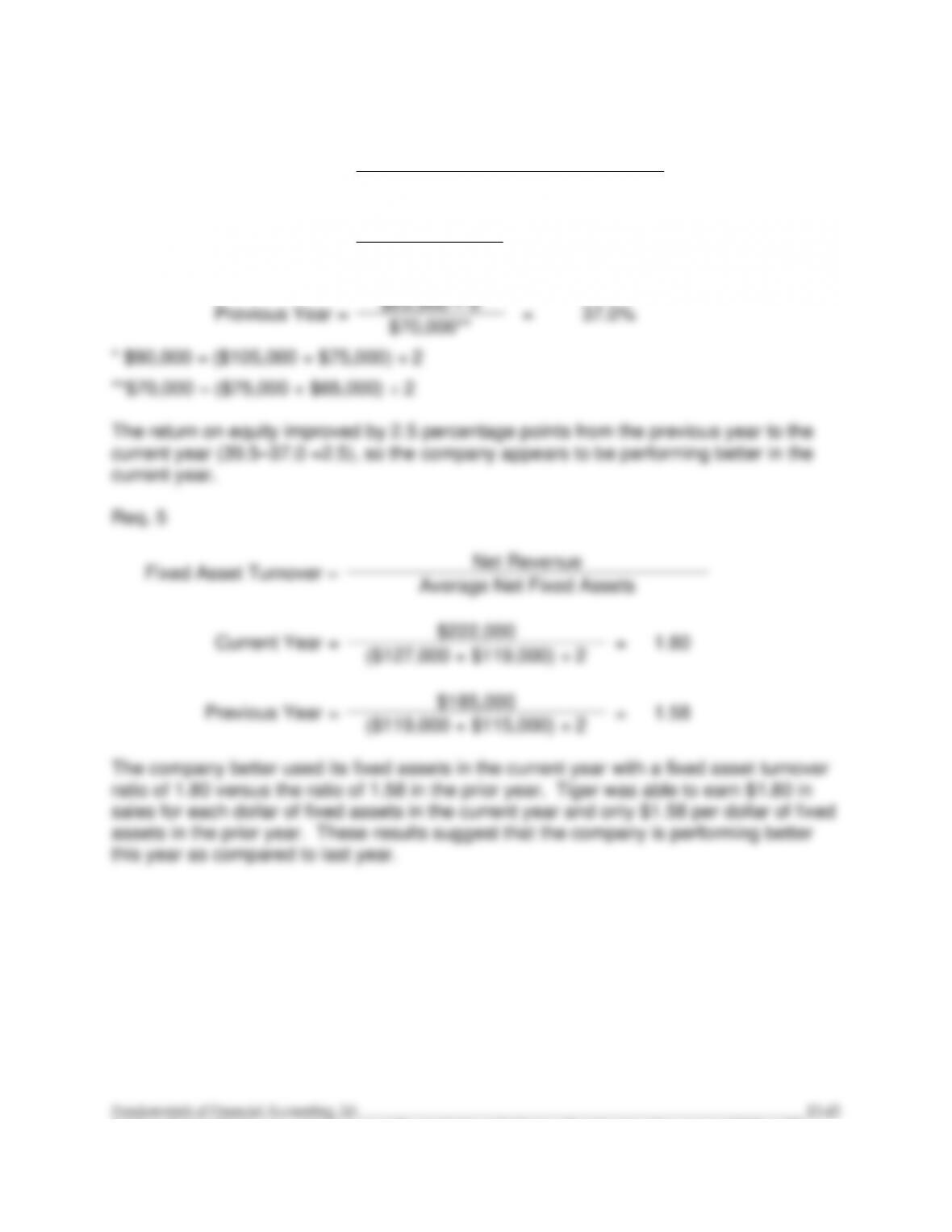

Previous Year =

$185,000 – $111,000

=

40.0%

$185,000

The increase from 40.0% in the prior year to 42.5% in the current year indicates that the

current year results are better than the prior year’s.

Req. 2

Net Profit Margin =

Net Income

Revenues

Current Year =

$35,525

=

16.0%

$222,000

Previous Year =

$25,900

=

14.0%

$185,000

The net profit margin increased and therefore is better this year as compared to the

previous year.

Req. 3

EPS =

Net Income – Preferred Dividends

Average Number of Shares of

Common Stock Outstanding*

Current Year =

$35,525 – 0

= $1.42

25,000

Previous Year =

$25,900 – 0

= $1.04

25,000

* 25,000 = ($25,000 ÷ $1)

PB13–2 (continued)

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Req. 4

Return on Equity (ROE) =

Net Income – Preferred Dividends

Average Stockholders’ Equity

Current Year =

$35,525 – 0

=

39.5%

$90,000*

Previous Year =

$25,900 – 0

=

37.0%

$70,000**

* $90,000 = ($105,000 + $75,000) ÷ 2

**$70,000 = ($75,000 + $65,000) ÷ 2

The return on equity improved by 2.5 percentage points from the previous year to the

current year (39.5–37.0 =2.5), so the company appears to be performing better in the

current year.

Req. 5

Fixed Asset Turnover =

Net Revenue

Average Net Fixed Assets

Current Year =

$222,000

=

1.80

($127,000 + $119,000) ÷ 2

Previous Year =

$185,000

=

1.58

($119,000 + $115,000) ÷ 2

The company better used its fixed assets in the current year with a fixed asset turnover

ratio of 1.80 versus the ratio of 1.58 in the prior year. Tiger was able to earn $1.80 in

sales for each dollar of fixed assets in the current year and only $1.58 per dollar of fixed

assets in the prior year. These results suggest that the company is performing better

this year as compared to last year.

PB13–2 (continued)

Req. 6

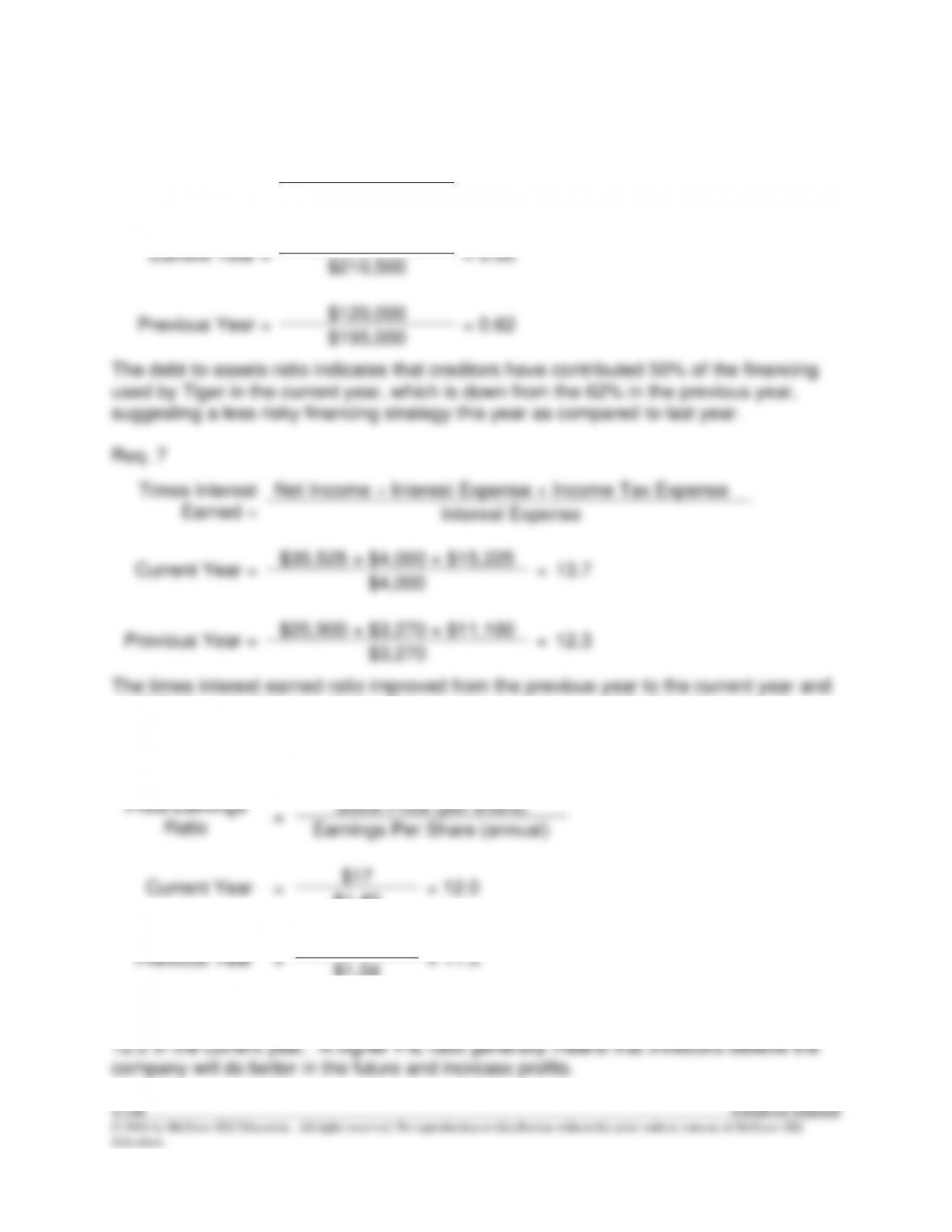

Debt-to–Assets =

Total Liabilities

Total Assets

Current Year =

$105,500

= 0.50

$210,500

Previous Year =

$120,000

= 0.62

$195,000

Net Income + Interest Expense + Income Tax Expense

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB13–3

Req. 1

a.

Inventory of Parts and Supplies

=

$467

=

2%

Total assets

$19,345

b.

Property and Equipment, Net

=

$13,389

=

69%

Total assets

$19,345

c.

Long-term liabilities

=

$6,333

=

33%

Total assets

$19,345

PB13–4

Req. 1

a.

Fuel, oil, repairs, and maintenance

=

$6,843

=

39%

Sales revenues

$17,699

b.

Other operating expenses

=

$4,543

=

26%

Sales revenues

$17,699

c.

Net income

=

$754

=

4%

Sales revenues

$17,699

d.

Salaries, and wages expense

=

$4,749

=

28%

Sales revenues

$17,088

e.

Fuel, oil, repairs, and maintenance

=

$7,252

=

42%

Sales revenues

$17,088

f.

Net income

=

$421

=

2%

Sales revenues

$17,088

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB13–5

Req. 1

Three profitability ratios to be considered are (1) Gross profit percentage, (2) Net profit

margin, and (3) Return on equity. Hasbro’s gross profit percentage exceeds Mattel’s,

but Mattel’s “bottom line” net income is greater, as indicated by its larger net profit

(2) Inventory turnover ratio, and (3) Current ratio. Mattel has faster receivables turnover,

inventory turnover and current ratio, indicating that Mattel is more liquid than Hasbro.

Req. 3

Only the debt-to-assets ratio is available to evaluate solvency. This ratio indicates the

proportion of total assets that are financed by creditors, and indicates that Mattel has

PB13–6

Req. 1

Ratio

Thor Company

Gunnar Company

Tests of profitability:

1.

Net profit margin

($112,000 ÷ $1,120,000) x 100 = 10.00%

($42,000 ÷ $336,000) x 100 = 12.50%

2.

Gross profit percentage

[($1,120,000 – $672,000) ÷ $1,120,000] x

100 = 40.00%

[($336,000 – $180,000) ÷ $336,000] x

100 = 46.43%

3.

Fixed asset turnover

$1,120,000 ÷ $770,000* = 1.45

$336,000 ÷ $192,000* = 1.75

4.

Return on equity

($112,000 – 0) ÷ [($798,000 + $798,000) ÷

2] x 100 = 14.04%

($42,000 – 0) ÷ [($266,400 +

$266,400) ÷ 2] x 100 = 15.77%

5.

Earnings per share

$112,000 ÷ 33,600** sh. = $3.33

$42,000 ÷ 12,600 sh. = $3.33

6.

Price/earnings ratio

$13.20 ÷ $3.33 = 3.96

$19.60 ÷ $3.33 = 5.89

Tests of liquidity:

7.

Receivables turnover

$1,120,000 ÷

[($77,000 + $65,800) ÷ 2] = 15.69

$336,000 ÷

[($28,000 + $27,200) ÷ 2] = 12.17

Days to collect

365 ÷ 15.69 = 23.27 days

365 ÷ 12.17 = 29.99 days

8.

Inventory turnover

$672,000 ÷

[($154,000 + $133,000) ÷ 2] = 4.68

$180,000 ÷ [($30,000 + $45,600) ÷ 2]

= 4.76

Days to sell

365 ÷ 4.68 = 77.99 days

365 ÷ 4.76 = 76.68 days

9.

Current ratio

$266,000 ÷ $168,000 = 1.58

$90,000 ÷ $18,000 = 5.00

Tests of solvency:

10.

Debt-to-assets ratio

$434,000 ÷ $1,232,000 = 0.35

$84,000 ÷ $350,400 = 0.24

* The problem indicates that the end-of-year ending balance approximates the average for the year.

1. Each set of financial statements is audited and each received an unqualified

opinion; therefore, there is no preference in terms of credibility of information.

2. Profitability—Gunnar Company had a higher gross profit percentage (46.43%

versus 40.00%) and net profit margin than Thor Company (12.50% versus 10.00%).

4.68; 77 days versus 78 days). Thor Company has a higher receivables turnover

(15.69 versus 12.17; 23 days versus 30 days), which indicates that Thor does

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB13–6 (continued)

4. Solvency—Gunnar Company clearly is in a less risky position on this factor. Gunnar

Company financed its operations by obtaining only 24% of its total assets using

5. A higher price/earnings ratio indicates that investors in the stock market believe

6. Constraint—The above analysis is based on only one year. Although this year is

relevant (it is the most recent), it limits the ability to conduct trend analyses.

PB13–7

1. Company A shows high EPS, high debt to assets, and high return on equity.

This suggests that Company A has a high level of debt, but is able to use it to

2. The low level of liquidity for Company A (low current ratio) is a concern given its

high debt-to-assets ratio.

3. Company A has a low price/earnings ratio. This often is an indication of limited

growth opportunities or concern in the market. In contrast, Company B has a