Education.

CP13–6 (continued)

(1.84 vs. 1.75), faster receivables turnover (23.82 vs. 15.00; 15.32 vs. 24.33 days to

collect), and faster inventory turnover (9.53 vs. 2.55; 38 vs. 143 days to sell). These

achievements are particularly noteworthy because they have not come at the expense

of reduced profits (as noted above).

CP13–7

1. Company A has a high level of liquidity as shown by the current ratio but

because the inventory turnover is low it is likely that much of the current assets

2. In addition to liquidity concerns, Company A shows a high debt–to-assets ratio

3. Company A does not seem to have good growth opportunities. The market has

valued Company A at a low price/earnings ratio.

13-32 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO GROUP A PROBLEMS

PA13–1

Req. 1

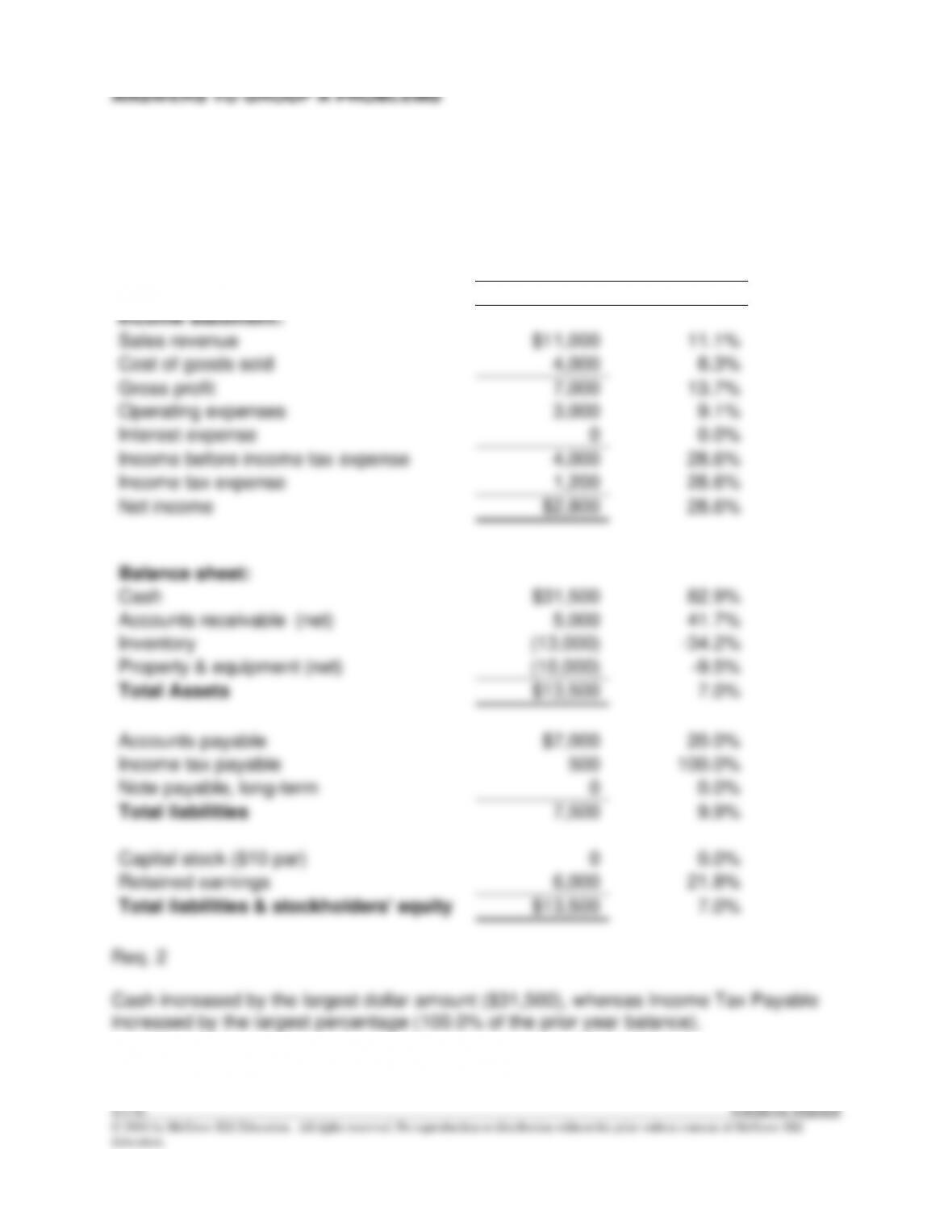

Pinnacle Plus Horizontal Analysis

Increase (Decrease)

in the current year (versus

the previous year)

Amount

Percentage

Income statement:

Sales revenue

$11,000

11.1%

Cost of goods sold

4,000

8.3%

Gross profit

7,000

13.7%

Operating expenses

3,000

9.1%

Interest expense

0

0.0%

Income before income tax expense

4,000

28.6%

Income tax expense

1,200

28.6%

Net income

$2,800

28.6%

Balance sheet:

Cash

$31,500

82.9%

Accounts receivable (net)

5,000

41.7%

Inventory

(13,000)

-34.2%

Property & equipment (net)

(10,000)

-9.5%

Total Assets

$13,500

7.0%

Accounts payable

$7,000

20.0%

Income tax payable

500

100.0%

Note payable, long-term

0

0.0%

Total liabilities

7,500

9.9%

Capital stock ($10 par)

0

0.0%

Retained earnings

6,000

21.8%

Total liabilities & stockholders’ equity

$13,500

7.0%

Req. 2

Cash increased by the largest dollar amount ($31,500), whereas Income Tax Payable

increased by the largest percentage (100.0% of the prior year balance).

=

=

PA13–2

Req. 1

Gross Profit Percentage =

Net Sales Revenue – Cost of Goods Sold

Net Sales Revenue

Current Year =

$110,000 – $52,000

=

0.527 or

52.7%

$110,000

Previous Year =

$99,000 – $48,000

=

0.515 or

51.5%

$99,000

The increase from 51.5% in the prior year to 52.7% in the current year recognizes that

PA13–2 (continued)

Req. 4

Return on Equity (ROE) =

Net Income – Preferred Dividends

Average Stockholders’ Equity

Current Year =

$12,600 – 0

=

0.105 or

10.5%

$120,500*

Previous Year =

$9,800 – 0

=

0.090 or

9.0%

$108,750**

* $120,500 = ($123,500 + $117,500) ÷ 2

**$108,750 = ($117,500 + $100,000) ÷ 2

The return on equity improved by 1.5% from the previous year to the current year

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PA13–2 (continued)

Req. 6

Debt-to–Assets =

Total Liabilities

Total Assets

Current Year =

$83,000

= 0.40

$206,500

Previous Year =

$75,500

= 0.39

$193,000

The debt-to-assets ratio indicates that creditors have contributed 40% of the financing

used by Pinnacle Plus in the current year, which is up only slightly over the prior year.

Pinnacle Plus appears to be maintaining the same balance between debt and equity

financing that was evident in the prior year.

Req. 7

Times Interest

Earned =

Net Income + Interest Expense + Income Tax Expense

Interest Expense

Current Year =

$12,600 + $4,000 + $5,400

=

5.5

$4,000

Previous Year =

$9,800 + $4,000 + $4,200

=

4.5

$4,000

The times interest earned ratio improved from the prior year to the current year and, at

5.5, the ratio indicates that sufficient net income is earned (before interest and income

PA13–2 (continued)

Req. 8

Price/Earnings

Ratio

=

Stock Price (per share)

Earnings Per Share (annual)

Current Year

=

$18

= 12.9

$1.40

Previous Year

=

$15

= 13.8

$1.09

It appears that investors have become less optimistic about the future success of

Pinnacle Plus because the P/E ratio has decreased from 13.8 in the prior year to 12.9 in

PA13–3

Req. 1

a.

Other current assets

=

$109

=

7%

Total assets

$1,514

b.

Total liabilities

=

$904

=

60%

Total assets

$1,514

c.

Common Stock

=

$118

=

8%

Total assets

$1,514

d.

Total stockholders’ equity

=

$610

=

40%

Total assets

$1,514

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PA13–4

Req. 1

a.

Selling, general, and administrative expenses

=

$333

=

16%

Sales revenues

$2,062

b.

Interest expense

=

$22

=

1%

Sales revenues

$2,062

c.

Net income

=

$11

=

1%

Sales revenues

$2,062

d.

Cost of goods sold

=

$1,721

=

78%

Sales revenues

$2,200

e.

Income before income taxes

=

$95

=

4%

Sales revenues

$2,200

f.

Net income

=

$62

=

3%

Sales revenues

$2,200

PA13–5

Req. 1

In terms of generating profits, Coca-Cola appears to be the more profitable company

with a higher gross profit percentage and net profit margin. Earnings per share (EPS) is

excluded from between-company comparisons because it could be affected by

differences in stock structure that do not reflect differences in profitability.

Req. 2

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PA13–6

Req. 1

Ratio

Royale Company

Cavalier Company

Tests of profitability:

1.

Net profit margin

($80,000 ÷ $800,000) x 100 = 10.00%

($35,000 ÷ $280,000) x 100 = 12.50%

2.

Gross profit percentage

[($800,000 – $480,000) ÷ $800,000] x

100 = 40.00%

($280,000 – $150,000) ÷ $280,000 x

100 = 46.43%

3.

Fixed asset turnover

$800,000 ÷ $550,000* = 1.45

$280,000 ÷ $160,000* = 1.75

4.

Return on equity

($80,000 – 0) ÷ [($570,000 + $570,000) ÷

2] x 100 = 14.04%

($35,000 – 0) ÷ [($202,000 +

$222,000)÷2] x 100 = 16.51%

5.

Earnings per share

($80,000 – 0) ÷ 24,000 shares = $3.33

($35,000 – 0) ÷ 10,500 shares = $3.33

6.

Price/earnings ratio

$14.00 ÷ $3.33 = 4.20

$11.00 ÷ $3.33 = 3.30

Tests of liquidity:

7.

Receivables turnover

$800,000 ÷

[($47,000 + $55,000) ÷ 2] = 15.69

$280,000 ÷

[($14,000 + $16,000) 2] = 18.67

Days to collect

365 ÷ 15.69 = 23.26 days

365 ÷ 18.67 = 19.55 days

8.

Inventory turnover

$480,000 ÷ [($95,000 + $110,000) ÷ 2]

= 4.68

$150,000 ÷ [($38,000 + $25,000) 2]

= 4.76

Days to sell

365 ÷ 4.68 = 77.99 days

365 ÷ 4.76 = 76.68 days

9.

Current ratio

$190,000 ÷ $120,000 = 1.58

$86,000 ÷ $15,000 = 5.73

Tests of Solvency:

10.

Debt-to-assets

$310,000 ÷ $880,000 = 0.35

$70,000 ÷ $292,000 = 0.24

* The problem indicates that the end–of-year ending balance approximates the average

1. Each set of financial statements is audited and each received an unqualified

opinion; therefore, there is no preference in terms of credibility of information.

10.00%). Cavalier Company earned a return on equity of 16.51% compared with

3. Liquidity—Cavalier Company has higher liquidity than Royale Company as

evidenced by the current ratio (5.73 compared with 1.58), receivables turnover

(18.67 versus 15.69, which is 20 days versus 23 days) and inventory turnover (4.76

13-40 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PA13–6 (continued)

4. Solvency—Cavalier Company clearly is in a less risky position on this factor.

Cavalier Company financed its operations by obtaining only 24% of its total assets

5. The price/earnings ratio provides little evidence in favor of either company.

6. Constraint—The above analysis is based on only one year. Although this year is

relevant (it is the most recent), it limits the ability to conduct trend analyses.

7. Accounting decisions—Cavalier’s higher bad debt estimates reduced its profitability

ratios (net profit margin, return on equity, earnings per share) relative to Royale.

Despite this, the company still appeared more profitable. The higher bad debt

PA13–7

1. Company A’s low current ratio, combined with its high inventory turnover ratio,

2. The price/earnings ratio for Company A suggests a profitable company with

good growth prospects.

3. The low debt-to-assets ratio and high times interest earned ratio suggests