Education.

E13–14

Current Assets

(CA)

Current Liabilities

(CL)

Current

Ratio

(CA ÷ CL)

Start

$500,000

($500,000 ÷ 2)

$250,000

2.00

Transaction (1)

A/R

+15,000

Inventory

-12,000

Subtotal

503,000

250,000

2.01

Transaction (2)

Dividends pay.

+50,000

Subtotal

503,000

300,000

1.68

Transaction (3)

Cash

Prepaid

-12,000

+12,000

Subtotal

503,000

300,000

1.68

Transaction (4)

Cash

-50,000

Dividends pay.

-50,000

Subtotal

453,000

250,000

1.81

Transaction (5)

Cash

+12,000

-12,000

A/R

Subtotal

453,000

250,000

1.81

Transaction (6)

Reclassify Liab.

+40,000

453,000

290,000

1.56

E13–15

The exercise states that both companies are exactly alike except for the impact of the

alternative methods to cost inventory. Use of LIFO (compared to FIFO), during a period

2. LIFO → higher inventory and total assets → lower debt-to-assets → Company A.

3. LIFO → lower cost of goods sold → higher EPS → Company B.

13-22 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO COACHED PROBLEMS

CP13–1

Req. 1

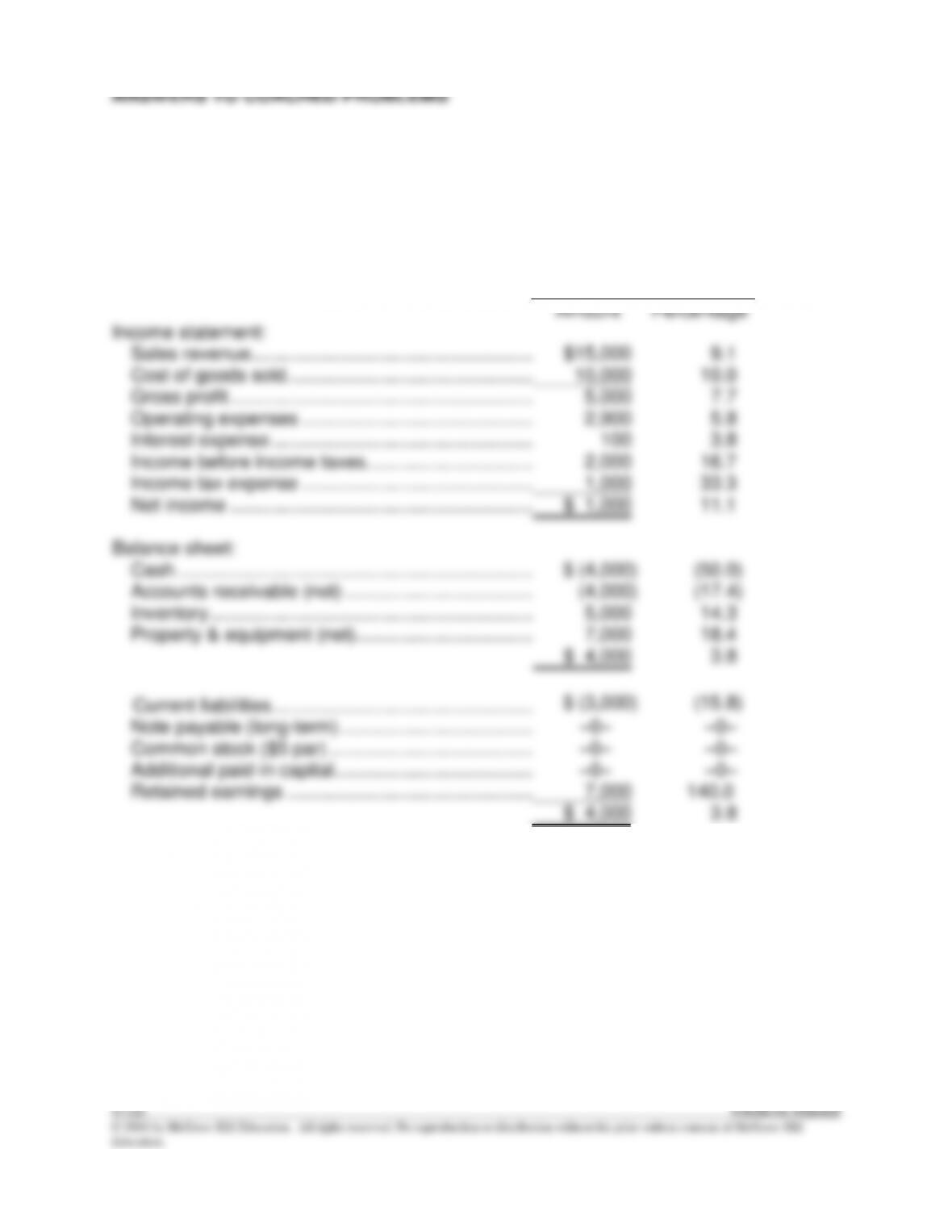

Golden Corporation

Horizontal Analysis

Increase (Decrease)

in the current year (versus

previous year)

Amount

Percentage

Income statement:

Sales revenue……………………………………………………….

$15,000

9.1

Cost of goods sold ………………………………………..…………..

10,000

10.0

Gross profit ………………………………………………….……

5,000

7.7

Operating expenses ……………………………………..…………..

2,900

5.8

Interest expense …………………………..…………………………..

100

3.8

Income before income taxes…………………………..…………..

2,000

16.7

Income tax expense ……………………………………..…………..

1,000

33.3

Net income ………………………………………………….……

$ 1,000

11.1

Balance sheet:

Cash …………………………………………………………..…………..

$ (4,000

)

(50.0

)

Accounts receivable (net) …………………………………………..

(4,000

)

(17.4

)

Inventory ……………………………………………………....

5,000

14.3

Property & equipment (net)…………………………….…………..

7,000

18.4

$ 4,000

3.8

Current liabilities …………………………………………..…………..

$ (3,000

)

(15.8

)

Note payable (long-term) ……………………………….…………..

–0–

–0–

Common stock ($5 par) ……………………………………………..

–0–

–0–

Additional paid-in capital ………………………………..…………..

–0–

–0–

Retained earnings ………………………………………..…………..

7,000

140.0

$ 4,000

3.8

=

=

CP13–1 (continued)

Req. 2

(a) The percentage change in Cash (50%) is big but it results from a small dollar

by 9.1%, accounts receivable decreased by 17.4%. Typically, an increase in sales

would be accompanied by an increase in accounts receivable. One potential

CP13–2

Req. 1

Gross Profit Percentage =

Net Sales Revenue – Cost of Goods Sold

Net Sales Revenue

Current Year =

$180,000 – $110,000

=

0.389 or

38.9%

$180,000

Previous Year =

$165,000 – $100,000

=

0.394 or

39.4%

$165,000

The slight decrease in the Gross Profit Percentage from the prior year to the current

CP13–2 (continued)

Req. 3

EPS =

Net Income – Preferred

Dividends

Average Number of

Shares of Common Stock

Outstanding*

Current Year=

$10,000 – 0

= $1.67

6,000

Previous Year=

$9,000 – 0

= $1.50

6,000

*

6,000 = ($30,000÷ $5)

The Earnings per Share has increased from $1.50 per share in the previous year to

$1.67 per share in the current year. This suggests that the company is doing better this

year and the improvement looks good for the stockholders.

Req. 4

Return on Equity (ROE) =

Net Income – Preferred Dividends

Average Common Stockholders‘ Equity

Current Year =

$10,000 – 0

=

0.230 or 23.0%

$43,500*

Previous Year =

$9,000 – 0

=

0.257 or 25.7%

$35,000**

* $43,500 = ($47,000 + $40,000) ÷ 2

**$35,000 = ($40,000 + $30,000) ÷ 2

The dollar amount of average stockholders’ equity increased more dramatically over last

year (from $35,000 to $43,500) than did net income (from $9,000 to $10,000). Because

the ROE denominator increased more dramatically than the numerator, the overall

return on equity declined (from 25.7% to 23.0%). The 2.7% drop from the previous year

to the current year indicates that the company’s ROE is worse this year.

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CP13–2 (continued)

Req. 5

Fixed Asset Turnover =

Net Revenue

Average Net Fixed Assets

Current Year =

$180,000

=

4.34

($38,000 + $45,000) ÷ 2

Previous Year =

$165,000

=

4.52

($35,000 + $38,000) ÷ 2

The company better used its fixed assets in the previous year with a fixed asset

turnover ratio of 4.52 versus a ratio of 4.34 in the current year. The company appears

to be doing worse this year because Golden was able to earn 18 cents more sales per

dollar of fixed assets in the previous year than it was able to earn in the current year.

Req. 6

Debt-to–Assets =

Total Liabilities

Total Assets

Current Year =

$61,000

= 0.56

$108,000

Previous Year =

$64,000

= 0.62

$104,000

The ratio decreased from the previous year to the current year, which indicates that

debt is providing financing for a smaller proportion of the company’s assets. This trend

suggests that the company is doing better this year.

CP13–2 (continued)

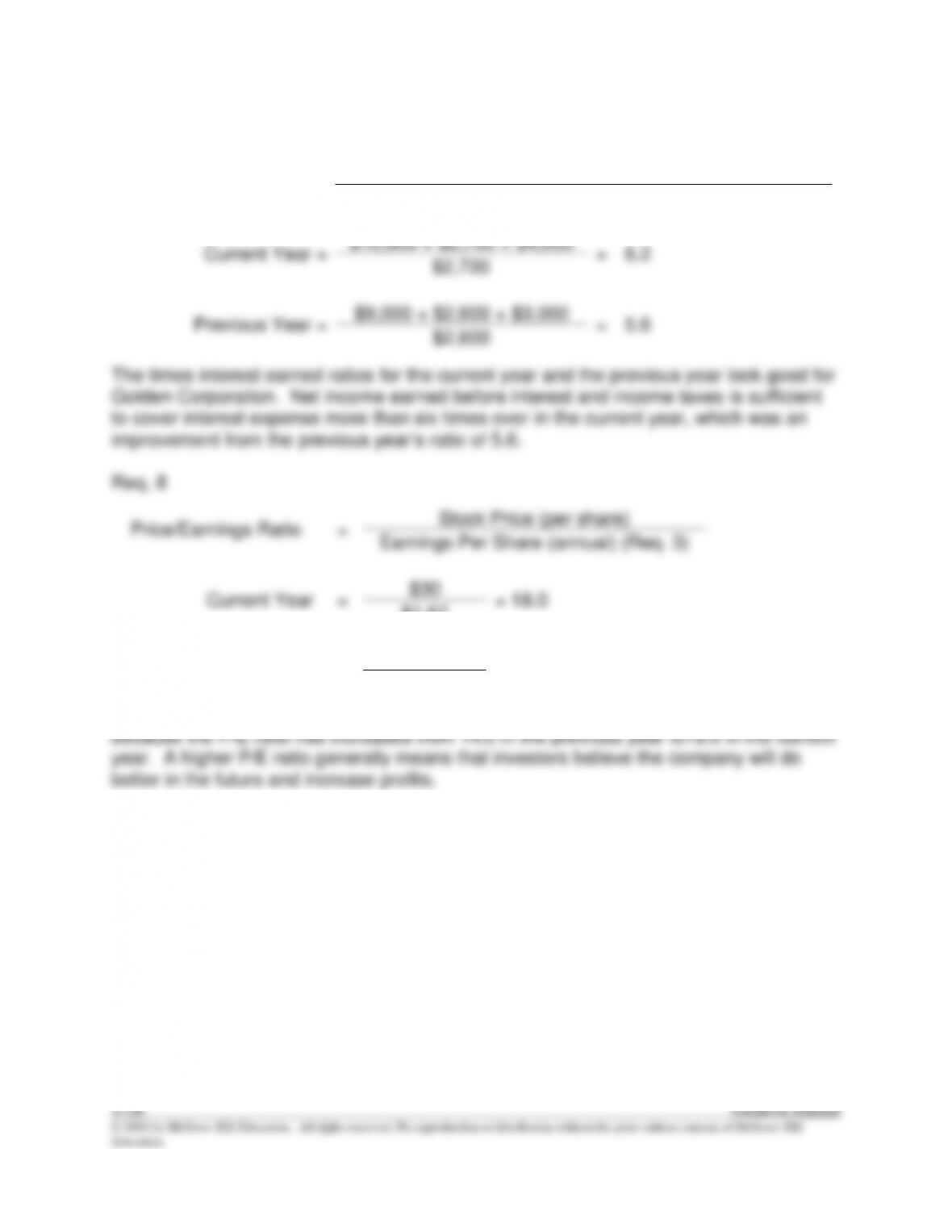

Req. 7

Times Interest Earned =

Net Income + Interest Expense + Income Tax Expense

Interest Expense

Current Year =

$10,000 + $2,700 + $4,000

=

6.2

$2,700

Previous Year =

$9,000 + $2,600 + $3,000

=

5.6

$2,600

The times interest earned ratios for the current year and the previous year look good for

Golden Corporation. Net income earned before interest and income taxes is sufficient

to cover interest expense more than six times over in the current year, which was an

improvement from the previous year’s ratio of 5.6.

Req. 8

Price/Earnings Ratio

=

Stock Price (per share)

Earnings Per Share (annual) (Req. 3)

Current Year

=

$30

= 18.0

$1.67

Previous Year

=

$21

= 14.0

$1.50

It appears that investors have become more optimistic about Golden’s future success

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CP13–3

Req. 1

a.

Other current assets

=

$291

=

6%

Total assets

$5,070

b.

Intangibles

=

$1,974

=

39%

Total assets

$5,070

c.

Property and equipment

=

$548

=

11%

Total assets

$5,070

d.

Accrued liabilities

=

$658

=

13%

Total assets

$5,070

e.

Total liabilities

=

$2,803

=

55%

Total assets

$5,070

CP13–4

Req. 1

a.

Research and development expense

=

$1,153

=

30%

Net revenues

$3,797

b.

Sales and marketing expense

=

$788

=

21%

Net revenues

$3,797

c.

General and administrative expense

=

$347

=

9%

Net revenues

$3,797

d.

Net income

=

$98

=

3%

Net revenues

$3,797

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CP13–5

Req. 1

Kohl’s has a higher gross profit percentage, net profit margin and return on equity in

comparison to Macy’s. Thus, it appears on an overall basis that Kohl’s is more

(1) inventory turnover ratio, and (2) current ratio. Therefore, it suggests that Macy’s has

a better ability to generate cash to be used in paying current liabilities.

Req. 3

Only the debt-to-assets ratio is available to evaluate solvency. Based on this ratio alone,

CP13–6

Req. 1

Ratio

Armstrong Company

Blair Company

Tests of profitability:

1.

Net profit margin

($45,000 ÷ $450,000) x 100 = 10.00%

($90,000 ÷ $810,000) x 100 = 11.11%

2.

Gross profit percentage

[($450,000 – $245,000) ÷ $450,000] x

100 = 45.56%

[($810,000 – $405,000) ÷ $810,000] x 100

= 50.00%

3.

Fixed asset turnover

$450,000 ÷ $180,000* = 2.50

$810,000 ÷ $300,000* = 2.70

4.

Return on equity

($45,000 – 0) ÷ [($240,000 + $231,000)

÷ 2] x 100 = 19.11%

($90,000 – 0) ÷ [($380,000 + $440,000) ÷ 2]

x 100 = 21.95%

5.

Earnings per share

$45,000 ÷ 15,000 shares = $3.00

$90,000 ÷ 20,000 shares = $4.50

6.

Price/earnings ratio

$18 ÷ $3.00 = 6.00

$27 ÷ $4.50 = 6.00

Tests of liquidity:

7.

Receivables turnover

$450,000 ÷

[($20,000 + $40,000) ÷ 2] = 15.00

$810,000 ÷ [($38,000 + $30,000) ÷ 2]

= 23.82

Days to collect

365 ÷ 15.0 = 24.33

365 ÷ 23.82 = 15.32

8.

Inventory turnover

$245,000 ÷

[($92,000 + $100,000) ÷ 2] = 2.55

$405,000 ÷ [($45,000 + $40,000) ÷ 2]

= 9.53

Days to sell

365 ÷ 2.55 = 143.14

365 ÷ 9.53 = 38.30

9.

Current ratio

$175,000 ÷ $100,000 = 1.75

$92,000 ÷ $50,000 = 1.84

Tests of solvency:

10.

Debt-to-assets

$160,000 ÷ $400,000 = 0.40

$420,000 ÷ $800,000 = 0.53

* The problem indicates that the end–of-year ending balance approximates the average

for the year.

Note: Data are not available for calculating the Times Interest Earned Ratio.

Req. 2