© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E13–2

Req. 1

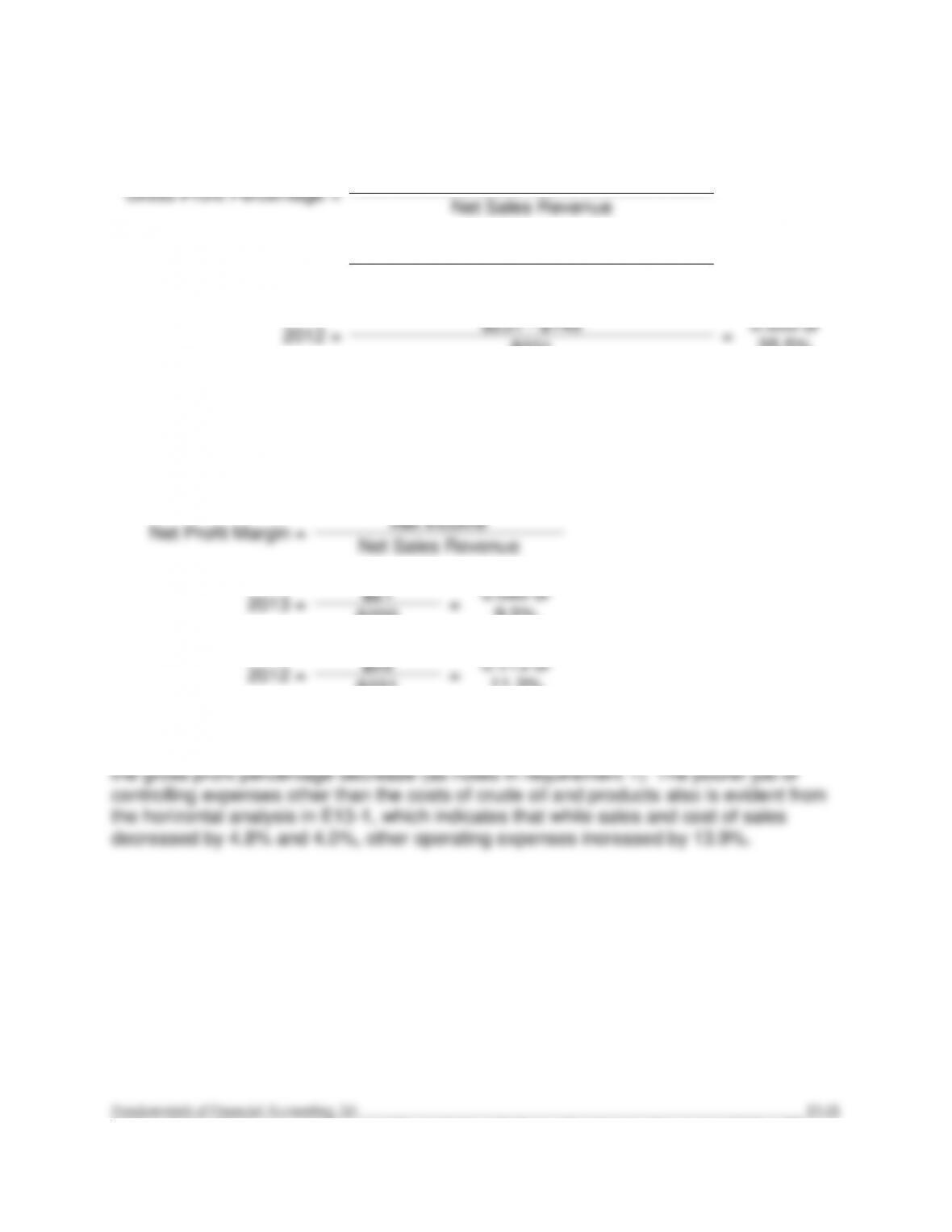

Gross Profit Percentage =

Net Sales Revenue – Cost of Goods Sold

Net Sales Revenue

2013 =

$220 – $143

=

0.350 or

35.0%

$220

2012 =

$231 – $149

=

0.355 or

35.5%

$231

The gross profit percentage of 35.0% means that the company generated 35.0 cents of

gross profit on each dollar of sales in 2013, which was a decrease of 0.5 cents from

2012. If this trend continues, the company could be expected to generate less gross

profit from each dollar of sales in 2014.

Req. 2

Net Profit Margin =

Net Income

Net Sales Revenue

2013 =

$21

=

0.095 or

9.5%

$220

2012 =

$26

=

0.113 or

11.3%

$231

Chevron did a worse job of controlling expenses in 2013 relative to 2012 because the

net profit margin decreased 1.8% (11.3 – 9.5), of which only 0.5% was attributable to

E13–2 (continued)

Req. 3

Fixed Asset Turnover =

Net Revenue

Average Net Fixed Assets

2013 =

$220 billion

=

1.47

$150 billion

2012 =

$231 billion

=

1.78

$130 billion

Return on Equity (ROE) =

=

=

E13–3

Req. 1

2013 2012 Dollars Percentage

Sales Revenue 100,000$ 120,000$ (20,000)$ -16.7%

Cost of Goods Sold 60,000 71,500 (11,500) -16.1%

Gross Profit 40,000 48,500 (8,500) -17.5%

Selling, General, and Admin. 36,000 37,000 (1,000) -2.7%

Interest Expense 500 475 25 5.3%

Income before Income Tax 3,500 11,025 (7,525) -68.3%

Income Tax Expense 1,000 5,000 (4,000) -80.0%

Net Income 2,500$ 6,025$ (3,525) -58.5%

Income Statements

Year Ended December 31

COMPUTER TYCOON, INC.

Change in

16.7% decrease in total revenues. It appears from this analysis that the 8.1% decrease

16.7%.

Req. 2

Sales Revenue 100,000$ 100.0% 120,000$ 100.0%

Cost of Goods Sold 60,000 60.0% 71,500 59.6%

Gross Profit 40,000 40.0% 48,500 40.4%

Selling, General, and Admin. 36,000 36.0% 37,000 30.8%

Interest Expense 500 0.5% 475 0.4%

Income before Income Tax 3,500 3.5% 11,025 9.2%

Income Tax Expense 1,000 1.0% 5,000 4.2%

Net Income 2,500$ 2.5% 6,025$ 5.0%

COMPUTER TYCOON, INC.

2013

2012

Income Statements

Year Ended December 31

40.4% in 2012. In other words, Computer Tycoon earned 0.4 cents less (40.0 – 40.4)

E13–4

Req. 1

Gross Profit Percentage =

Net Sales Revenue – Cost of Goods Sold

Net Sales Revenue

2012 =

$120,000 – $71,500

=

0.404 or

40.4%

$120,000

2013 =

$100,000 – $60,000

=

0.40 or

40.0%

$100,000

The gross profit percentage of 40.0% means that the company generated 40.0 cents of

=

=

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E13–4 (continued)

Req. 3

Fixed Asset Turnover =

Net Revenue

Average Net Fixed Assets

2012 =

$120,000

=

2.66

$45,100

2013 =

$100,000

=

1.85

$54,200

The company better utilized its investment in fixed assets in 2012. Its fixed asset

turnover ratio fell from 2.66 in 2012 to 1.85 in 2013. The 2013 ratio means that the

company generated $1.85 of sales revenue for every dollar invested in fixed assets.

Req. 4

Return on Equity (ROE) =

Net Income – Preferred Dividends

Average Common Stockholders‘ Equity

2012 =

$6,025 – 0

=

0.148 or 14.8%

$40,800

2013 =

$2,500 – 0

=

0.046 or 4.6%

$54,000

The company generated better returns for common stockholders in 2012 (14.8%) than

in 2013 (4.6%).

E13–5

Times Interest

Earned =

Net Income + Interest Expense + Income Tax Expense

Interest Expense

2012 =

$6,025 + $475 + $5,000

=

24.2

$475

2013 =

$2,500 + $500 + $1,000

=

8.0

$500

In both years, Computer Tycoon generated enough income before interest expense and

income tax expense to cover the cost of debt financing (although the declining trend

across the two years is troubling).

E13–6

1)

C

7)

H

2)

A

8)

G

3)

D

9)

I

4)

B

10)

E

5)

K

11)

F

6)

J

E13–7

Req. 1

Receivables turnover ratio = Net credit sales ÷ Average accounts receivable

= $300,000 ÷ [($45,000 + $55,000) ÷ 2]

= 6.0

Inventory turnover ratio = Cost of goods sold ÷ average inventory

= ($300,000 x .6) ÷ [($60,000 + $40,000) ÷ 2]

= 3.6

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

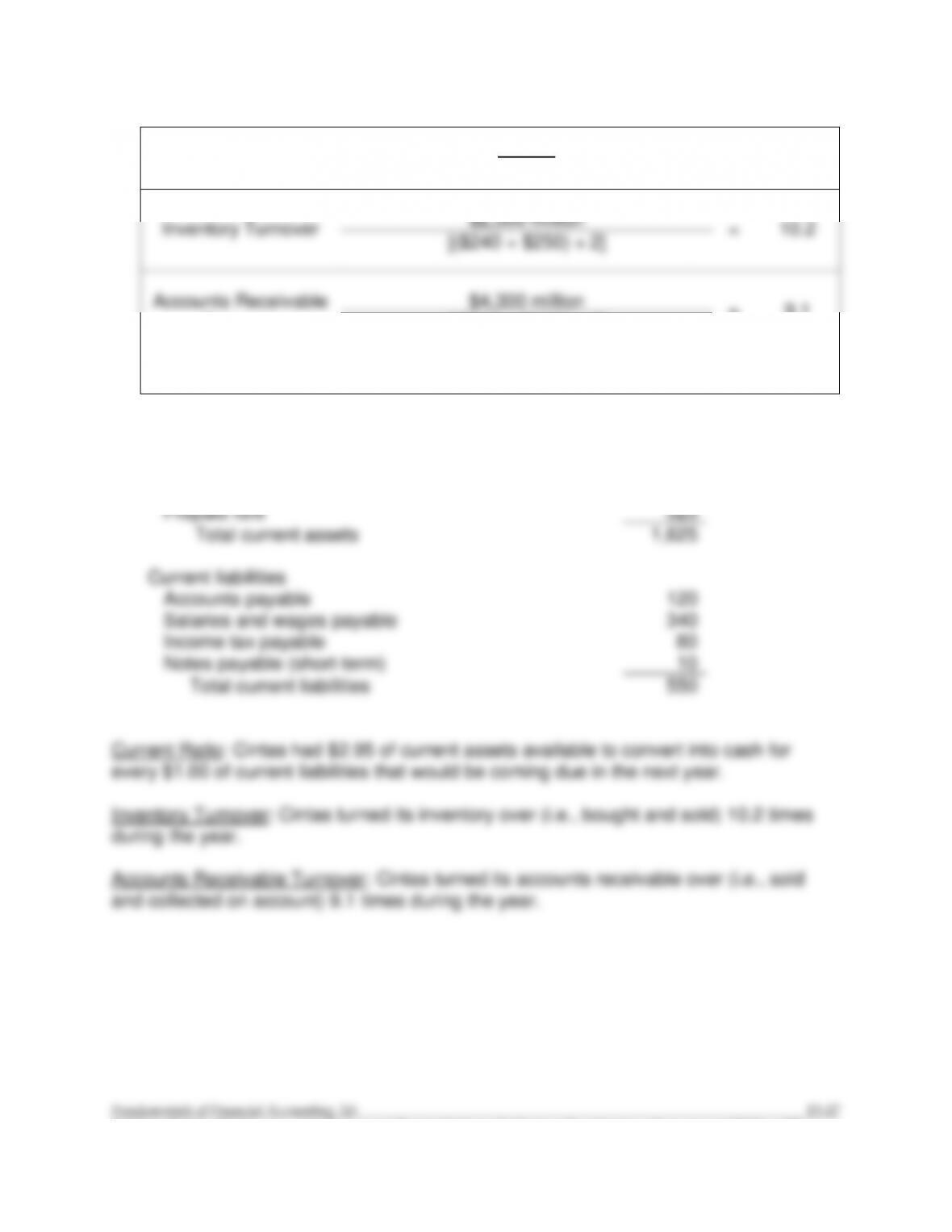

E13–8

Current Ratio

$1,625

$550

=

2.95

Inventory Turnover

$2,500 million

=

10.2

[($240 + $250) ÷ 2]

Accounts Receivable

Turnover

$4,300 million

=

9.1

[($500 + $450) ÷ 2]

Current Assets:

Cash

$ 360

Accounts receivable

500

Inventory

240

Prepaid rent

525

Total current assets

1,625

Current liabilities

Accounts payable

120

Salaries and wages payable

340

Income tax payable

80

Notes payable (short-term)

10

Total current liabilities

550

(See below)

E13–9

Req. 1

Receivables turnover ratio = Net credit sales ÷ Average accounts receivable

= $84,000 ÷ [($6,100 + $6,500) ÷ 2]

= 13.3

Inventory turnover ratio = Cost of goods sold ÷ Average inventory

= ($84,000 x 0.504) ÷ [($6,700 + $6,900) ÷ 2]

= 6.2

Days to collect = 365 days ÷ Receivable turnover ratio

= 365 days ÷ 13.3 = 27.4 days

Days to sell = 365 days ÷ Inventory turnover ratio

= 365 days ÷ 6.2 = 58.9 days

Req. 3

Procter & Gamble turned over its receivables 13.3 times and its inventory 6.2 times

during 2013. This means that it took, on average, 27.4 days to collect on its

receivables and 58.9 days to sell its inventory. In total, this implies 86.3 total days

from the time inventory was bought to when cash was collected from sales of

inventory.

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E13–10

Req. 1

Gross profit percentage = (Net sales – Cost of goods sold) ÷ Net sales

8.41 x $2,080,000,000 = Net sales

4.89 = Cost of goods sold ÷ $2,475,000,000

4.89 x $2,475,000,000 = Cost of goods sold

$12,102,750,000 = Cost of goods sold

E13–11

Current Assets

(CA)

Current Liabilities

(CL)

Current

Ratio

(CA ÷ CL)

Start

$54,000

($54,000 ÷ 1.8)

$30,000

1.80

Transaction (1)

Inventory

+ 6,000

Accts. Pay.

+ 6,000

Subtotal

60,000

36,000

1.67

Transaction (2)*

Cash

– 1,000

$59,000

$36,000

1.64

*Debt and truck are noncurrent items.

E13–12

Effect on:

Current Assets

Current Liabilities

Current Ratio

1.

Increase

No change

Increase

2.

No change

Increase

Decrease

3.

Decrease

No change

Decrease

4.

Increase

No change

Increase

E13–13

Current Assets

(CA)

Current Liabilities

(CL)

Current

Ratio

(CA ÷ CL)

Start

$88,000

($88,000 ÷ 1.75)

$50,286

1.75

Transaction (1)

Cash

–6,000

Accts. pay.

–6,000

Subtotal

82,000

44,286

1.85

Transaction (2)

Cash

–10,000

Subtotal

72,000

44,286

1.63

Transaction (3)

No

impact*

Subtotal

72,000

44,286

1.63

Transaction (4)

Cash

–25,000

Dividends pay.

–25,000

Subtotal

$ 47,000

$19,286

2.44

* An accounts receivable write-off causes decreases in both Accounts Receivable and

the Allowance for Doubtful Accounts, which offset one another, resulting in no impact on

total current assets.