© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 13

1. Trend analysis compares individual financial statement line items over time, with the

2. A year-over-year percentage simply expresses the change in the current year as a

percentage of the prior year total, using the following calculation:

Year-over-

year

change (%)

=

Change this year

x

100

=

(Current year’s total – prior year’s total)

x

100

Prior year’s total

Prior year’s total

3. Ratio analysis is conducted to understand relationships among various items

reported in the financial statements. It involves comparing an amount for one or

5. The three categories of performance into which most financial ratios are reported

include:

(2) Liquidity – relates to the company’s short-term survival. The specific focus is

(3) Solvency – relates to the company’s long–run survival. The specific focus is

6. The names “horizontal” and “vertical” represent the direction to which a financial

statement item is compared. Horizontal analyses involve comparing an item

7. A favorable interpretation of an increase in the current ratio is that the company has

8. The decrease in inventory turnover and increase in the current ratio suggests a

9. An increase in Gross Profit could be caused by either (or both) an increase in sales

volume and an increase in gross profit per sale. This year, net Sales increased by

$100,000 ($400,000 – $300,000), which is an increase of 33.3 percent ($100,000 ÷

10. The following explanations are based on typical circumstances: (a) an increase in

gross profit percentage would be favorable because it implies greater profit per

dollar of sales, (b) a decrease in the inventory turnover ratio would be unfavorable

11. The two essential characteristics of useful financial information are relevance and

12. The primary objective of financial reporting is to provide useful financial information

about a business to help external users make decisions.

13. The principle of full disclosure is that financial reports should present all information

that is needed to properly interpret the results of the company’s business activities.

14. The going-concern assumption states that a business is assumed capable of

continuing its operations long enough to meet its obligations. A going-concern

problem arises if a company runs into severe financial difficulty, casting substantial

doubt on the ability of the company to continue its operations long enough to meet

15. If reported, the financial results of discontinued operations appear on the income

16. The inventory costing method will differ because IFRS prohibits LIFO, but since

GAAP allows LIFO, Techgear has chosen to use LIFO. Differences between

inventory costing methods affect Inventory, Cost of Goods Sold, Gross Profit, and

Net Income. Consequently, the following ratios will be affected: net profit margin,

gross profit percentage, return on equity, earnings per share, price/earnings,

Revealed by Financial Analyses

Revealed by Other Analyses

• Declining sales

• Declining gross margin

• Significant one-time expenses

• Fluctuating net income

• Insufficient current assets

• Excessive reliance on debt financing

• Negative operating cash flows

• Loss of a key supplier or customer

• Insufficient product innovation/quality

• Significant barriers to expansion

• Loss of key personnel without replacement

• Unfavorable long-term commitments

• Inadequate maintenance of long-lived

assets

• Loss of a key franchise, license, or patent

Authors’ Recommended Solution Time

(Time in minutes)

Mini-exercises

Exercises

Problems

Skills

Development

Cases*

Continuing

Case

No.

Time

No.

Time

No.

Time

No.

Time

No.

Time

1

7

1

20

CP1

45

1

60

1

15

2

7

2

20

CP2

60

2

60

3

5

3

20

CP3

20

3

40

4

5

4

20

CP4

20

4

25

5

5

5

10

CP5

40

5

25

6

5

6

10

CP6

50

6

25

7

5

7

10

CP7

20

7

20

8

5

8

20

PA1

45

9

5

9

10

PA2

60

10

5

10

20

PA3

20

11

5

11

20

PA4

20

12

5

12

20

PA5

40

13

5

13

15

PA6

50

14

5

14

20

PA7

20

15

25

PB1

45

PB2

60

PB3

20

PB4

20

PB5

40

PB6

50

PB7

20

M13–1

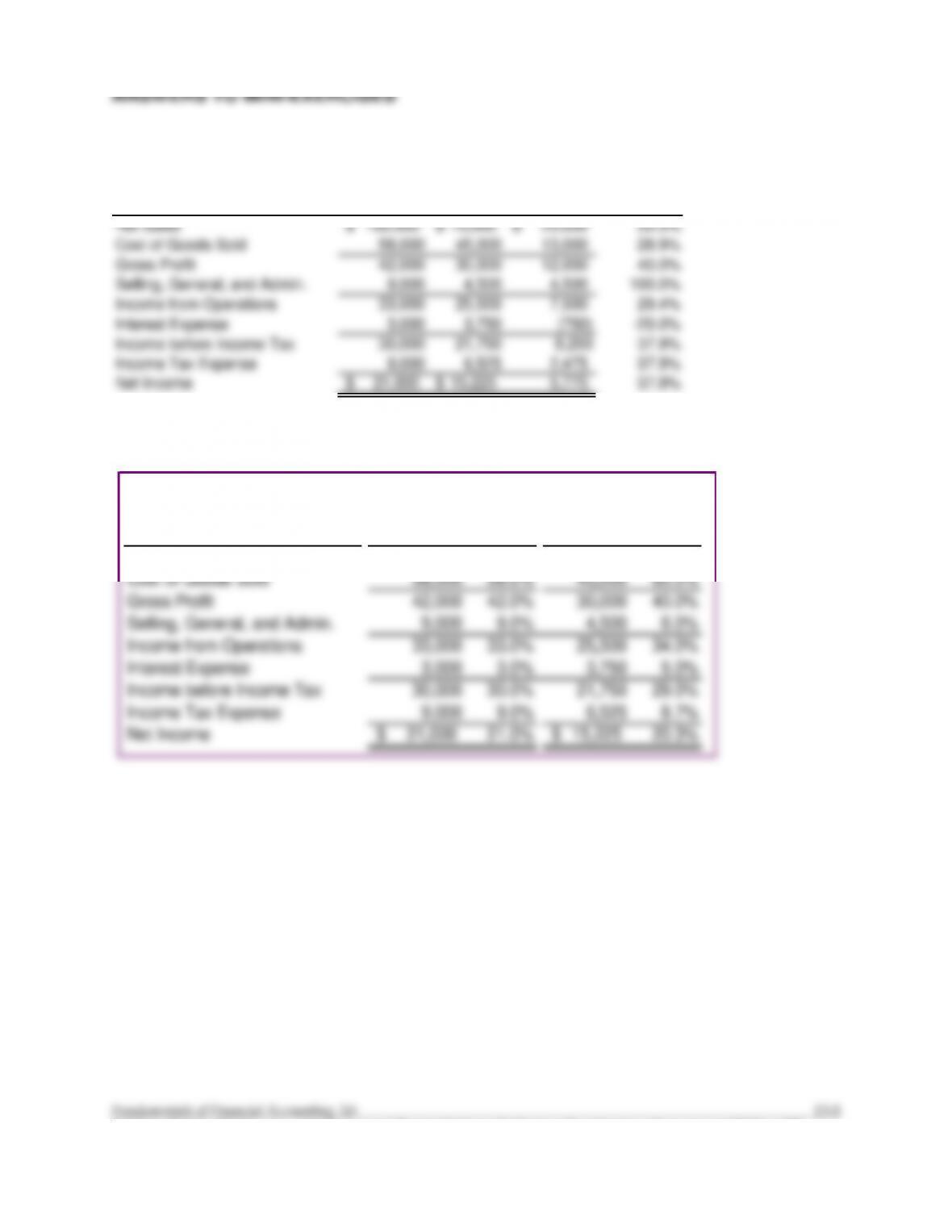

Current Previous Dollars Percentage

Net Sales 100,000$ 75,000$ 25,000$ 33.3%

Cost of Goods Sold 58,000 45,000 13,000 28.9%

Gross Profit 42,000 30,000 12,000 40.0%

Selling, General, and Admin. 9,000 4,500 4,500 100.0%

Income from Operations 33,000 25,500 7,500 29.4%

Interest Expense 3,000 3,750 (750) -20.0%

Income before Income Tax 30,000 21,750 8,250 37.9%

Income Tax Expense 9,000 6,525 2,475 37.9%

Net Income 21,000$ 15,225$ 5,775 37.9%

Income Statements

Year Ended December 31

LOCKEY FENCING CORPORATION

Change in

M13–2

Net Sales 100,000$ 100.0% 75,000$ 100.0%

Cost of Goods Sold 58,000 58.0% 45,000 60.0%

Gross Profit 42,000 42.0% 30,000 40.0%

Selling, General, and Admin. 9,000 9.0% 4,500 6.0%

Income from Operations 33,000 33.0% 25,500 34.0%

Interest Expense 3,000 3.0% 3,750 5.0%

Income before Income Tax 30,000 30.0% 21,750 29.0%

Income Tax Expense 9,000 9.0% 6,525 8.7%

Net Income 21,000$ 21.0% 15,225$ 20.3%

LOCKEY FENCING CORPORATION

Current

Previous

Income Statements

Year Ended December 31

M13–3

The two most significant year-over-year changes, in terms of dollar amounts, are the

increase in net sales (+$25,000) and increase in cost of goods sold (+$13,000). In terms

of percentages, the two most significant changes are the increases in gross profit

(+40%) and selling, general, and administrative expenses (+100%).

M13–4

The vertical analyses include comparisons of net income to net sales (which is the net

M13–5

Gross profit percentage = Gross profit

Net sales

So, 60% = Gross profit

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

M13–6

Sales

$250,000 *

Cost of Goods Sold (given)

(150,000)

Gross Profit

$100,000

Gross Profit Percentage = Gross profit ÷ Sales x 100

= $100,000 ÷ $250,000 x 100

= 40.0%

*This year’s sales: $200,000 x 1.25 = $250,000

M13–7

M13–8

The inventory turnover ratio is calculated as cost of goods sold divided by average

inventory. If the sales volume remains the same, then the cost of goods sold will also be

M13–9

Current Assets $ X

+ Noncurrent Assets + 1,480,000

Total Assets =11,200,000

M13–10

Previous Year: P/E Ratio = Market Price per Share ÷ Earnings per Share

= $50.00 ÷ $2.50

M13–11

a) Net profit margin

b) Debt-to-assets ratio

M13–12

a) Good

b) Good

c) Good

d) Bad

e) Good

M13–13

In most circumstances when costs are falling, a change from FIFO to LIFO will cause

inventory to increase and cost of good sold to decrease. These changes cause:

• Net Profit Margin to increase

• Fixed Asset Turnover to be unaffected

• Current Ratio to increase

Education.

M13–14

1. a) straight-line yields lower depreciation, which yields higher net income and net

2. a) FIFO yields lower cost of goods sold when costs and inventory levels are

3. a) 7-year useful life yields lower depreciation, which yields higher net income and

net profit margin

13-10 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

ANSWERS TO EXERCISES

E13–1

Req. 1

(dollars in billions)

2013 2012 Dollars Percentage

Revenues 220$ 231$ (11)$ –4.8%

Costs of Crude Oil and Products 143 149 (6) -4.0%

Other Operating Costs 41 36 5 13.9%

Income before Income Tax 36 46 -10 -21.7%

Income Tax Expense 15 20 (5) -25.0%

Net Income 21$ 26$ (5)$ -19.2%

Income Statements

Year Ended December 31

Chevron Corporation

Change in

(65.0%) than in 2012 (64.5%). This implies that Chevron earned less profit (excluding

income tax and other operating costs) per dollar of revenues in 2013 than in 2012.