Chapter Outline

Teaching Notes

IV. Supplement 13A: Nonrecurring and Other Special Items

LO 13-S1 Describe how nonrecurring and other comprehensive income items are reported.

A. Nonrecurring Items

1. Until 2005, three different types of nonrecurring items

were reported in income statements: discontinued

operations, extraordinary items, and the cumulative

effects of changes in accounting methods.

2. New accounting standards have nearly eliminated income

statement reporting of extraordinary items and the

cumulative effects of changes in accounting methods.

3. The cumulative effects of changes in accounting methods

are reported as adjustments to Retained Earnings rather

than as part of the income statement in the period when

the change is made.

Covered in Intermediate

Accounting.

4. Discontinued operations––Result from the disposal of a

major component of the business and are reported net of

income tax effects.

Illustrated in Exhibit 13A.1

a. The results of an abandoned or sold business unit for

the current year are reported on a separate line of the

income statement immediately after Income Tax

Expense.

b. This discontinued operations line includes any gain or

loss on disposal of the discontinued operation as well

as any operating income generated before its disposal.

c. Because it appears below the Income Tax Expense

line, any additional tax effects related to the gains or

losses are included in the reported amounts.

B. Other Items in Comprehensive Income

1. Comprehensive income = Net Income + Other

Comprehensive Income (OCI); OCI includes gains and

losses arising from changes in the values of certain assets

and liabilities.

Covered in Intermediate

Accounting courses.

a. These items represent gains or losses relating to

changes in the value of certain balance sheet accounts.

b. While most gains and losses are included in the

computation of net income, some (relating to changes

in foreign currency exchange rates and the value of

certain investments, for example) are excluded from

net income and included only in comprehensive

income.

V. Supplement 13B: Reviewing and Contrasting IFRS and GAAP

LO 13-S2 Describe significant differences between GAAP and IFRS.

A. Overview

1. Generally speaking, IFRS and GAAP are similar.

a. Both aim to guide businesses in reporting financial

information that is relevant and that faithfully

represents the underlying activities of businesses.

Chapter Outline

Teaching Notes

b. At a basic level, these accounting rules describe:

i. When an item should be recognized.

ii. How that item should be classified (e.g., asset or

expense, revenue or liability).

iii. How the amount at which each item should be

measured.

c. Although some exceptions exist, both IFRS and

GAAP require that items be recorded only after an

exchange between the company and another party.

i. Initially, these items are recorded at the value they

enter the company (called the entry price or

historical cost).

ii. Later, this value may be revised (upwards or

downwards) as a result of events or changes in

circumstances.

iii. The new value may be

(a) The entry price adjusted for items such as

interest, depreciation, and amortization,

(b) A current market price, or

(c) Another computed amount (such as the fair

value or exit price that the company would

receive or pay in the future for that item).

d. Many differences between IFRS and GAAP relate to

cases where IFRS requires or allows companies to

report items using values that differ from those

required or allowed by GAAP.

B. Specific Topics Integrated in Earlier Chapters

1. Chapter 1: Discusses the joint work of the Financial

Accounting Standards Board and the International

Accounting Standards Board to establish accounting rules

and a unified conceptual framework.

2. Chapter 7: Explains that IFRS prohibits LIFO and

discusses the potential financial impact of switching to

from FIFO to LIFO.

3. Chapter 9:

a. Discusses IFRS’s accounting for component costs.

b. Discusses IFRS’s accounting for R&D and revaluation

at fair value.

4. Chapter 10:

a. Discusses IFRS’s current classification of long-term

debt involving violated loan covenants.

b. Discusses IFRS’s threshold for accruing contingent

liabilities.

5. Chapter 11: Discusses classification of certain preferred

stock as a liability.

6. Chapter 12: Illustrates differences in classification of

dividends and interest received and paid, under IFRS and

GAAP.

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Unless you used it in connection with Chapter 1, consider showing the first segment of following

video in class; most students will be able to identify with the “fraudster.” Lively discussion of the

manner in which the fraud was perpetrated will follow.

The National Association of Certified Fraud Examiners produced a video in 1991 called “Cooking the

Books: What Every Accountant Should Know about Fraud.” If you do not have the tape, the toll free

number to order it is 1-800-245-3321, or visit the web site at http://www.cfenet.com. At this writing,

the cost to a college or university is $139.00 for nonmembers. Three frauds are overviewed: ZZZZ

Best Carpet, Regina Vacuum Cleaner Company, and ESM Group, Inc. (ESM Government Securities).

ZZZZ Best Carpet might be the best one to use. Barry Minkow, the CEO and major stockholder, is

interviewed in prison. The video segment discusses revenue overstatements, deferred costs, asset

valuations, inadequate disclosures, and horizontal and vertical analysis. It is very well done.

2. Handout 13–1

Use Handout 13–1 for an in-class activity designed to review the classification of financial ratios. The

solution follows the handout master.

3. Handout 13–2

Use Handout 13–2 for an in-class activity designed to review the formulas of financial ratios. The

solution follows the handout master.

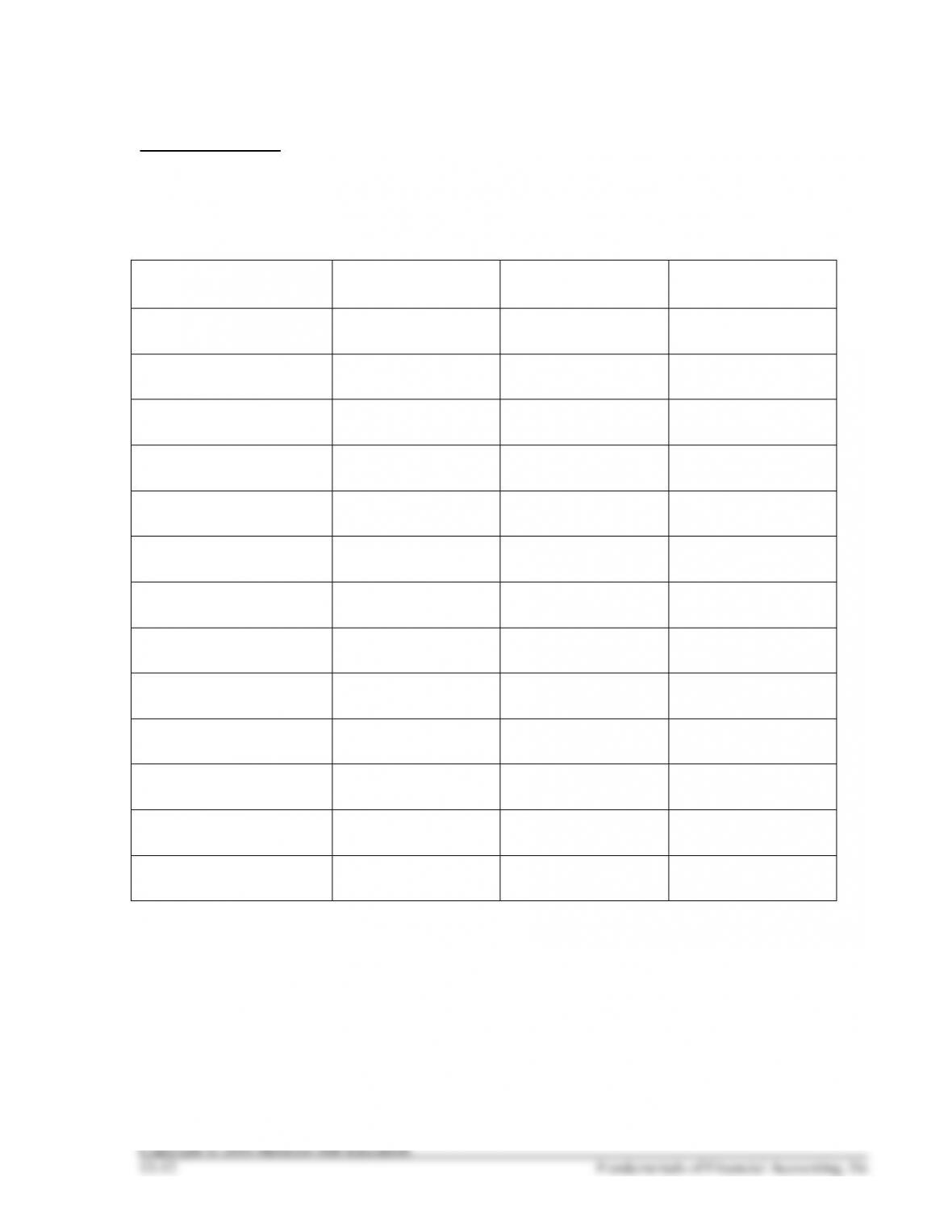

HANDOUT 13–1

CLASSIFICIATON OF FINANCIAL RATIOS

Indicate whether each of the following financial ratios would be classified as a profitability, liquidity, or

solvency ratio when performing ratio analysis.

Financial Ratio

Profitability Ratio

Liquidity Ratio

Solvency Ratio

Current Ratio

Days to Collect

Days to Sell

Debt-to–Assets

Earnings per Share (EPS)

Fixed Asset Turnover

Gross Profit Percentage

Inventory Turnover

Net Profit Margin

Price/ Earnings Ratio

Receivables Turnover

Return on Equity (ROE)

Times Interest Earned

HANDOUT 13–1 SOLUTION

CLASSIFICIATON OF FINANCIAL RATIOS

Indicate whether each of the following financial ratios would be classified as a profitability, liquidity, or

solvency ratio when performing ratio analysis.

Financial Ratio

Profitability Ratio

Liquidity Ratio

Solvency Ratio

Current Ratio

X

Days to Collect

X

Days to Sell

X

Debt-to–Assets

X

Earnings per Share (EPS)

X

Fixed Asset Turnover

X

Gross Profit Percentage

X

Inventory Turnover

X

Net Profit Margin

X

Price/ Earnings Ratio

X

Receivables Turnover

X

Return on Equity (ROE)

X

Times Interest Earned

X

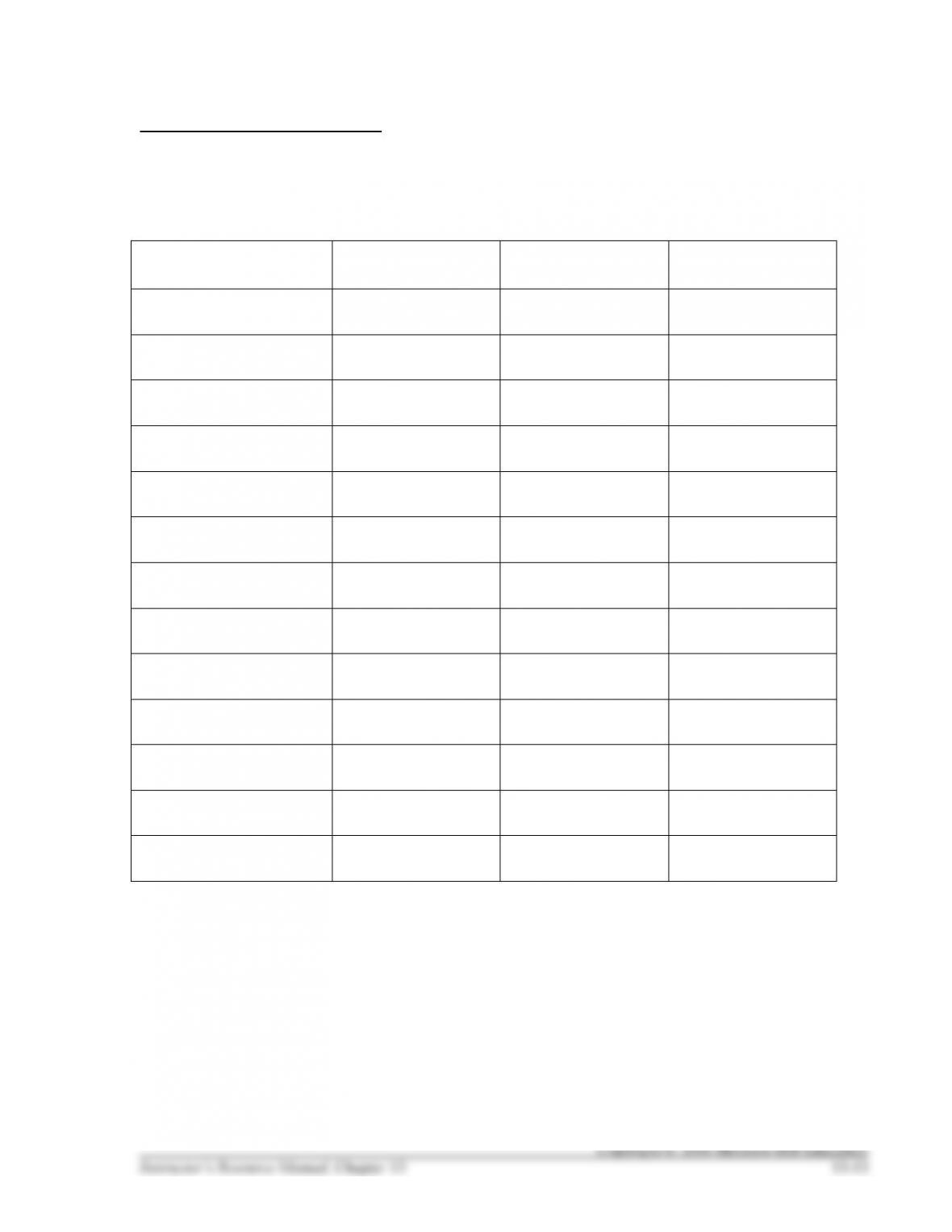

HANDOUT 13–2

FINANCIAL RATIO FORMULAS

Match each of the following financial ratios with its formula:

Ratios:

Current Ratio

Inventory Turnover

Days to Collect

Net Profit Margin

Days to Sell

Price/Earnings (P/E) Ratio

Debt-to–Assets

Receivables Turnover

Earnings Per Share (EPS)

Return on Equity (ROE)

Fixed Asset Turnover

Times Interest Earned

Gross Profit Percentage

Formulas:

A. Cost of sales divided by Average inventory

B. Current assets divided by Current liabilities

C. Stock price divided by EPS

D. Total liabilities divided by Total assets

E. 365 divided by Inventory turnover ratio

F. (Net income minus Preferred dividends) divided by Average number of common shares

G. (Net income minus Preferred dividends) divided by Average common stockholders’ equity

H. (Net income divided by Net sales revenue) × 100

I. (Net income + Interest expense + Income tax expense) divided by Interest expense

J. [(Net sales revenue − Cost of goods sold) divided by Net sales revenue] × 100

K. Total revenue divided by Average net fixed assets

L. Net sales revenue divided by Average net receivables

M. 365 divided by Receivables turnover ratio

HANDOUT 13–2 SOLUTION

FINANCIAL RATIO FORMULAS

Match each of the following financial ratios with its formula:

Ratios:

B

Current Ratio

A

Inventory Turnover

M

Days to Collect

H

Net Profit Margin

E

Days to Sell

C

Price/Earnings (P/E) Ratio

D

Debt-to–Assets

L

Receivables Turnover

F

Earnings Per Share (EPS)

G

Return on Equity (ROE)

K

Fixed Asset Turnover

I

Times Interest Earned

J

Gross Profit Percentage

Formulas:

A. Cost of sales divided by Average inventory

B. Current assets divided by Current liabilities

C. Stock price divided by EPS

D. Total liabilities divided by Total assets

E. 365 divided by Inventory turnover ratio

F. (Net income minus Preferred dividends) divided by Average number of common shares

G. (Net income minus Preferred dividends) divided by Average common stockholders’ equity

H. (Net income divided by Net sales revenue) × 100

I. (Net income + Interest expense + Income tax expense) divided by Interest expense

J. [(Net sales revenue ÷ Cost of goods sold) divided by Net sales revenue] × 100

K. Total revenue divided by Average net fixed assets

L. Net sales revenue divided by Average net receivables

M. 365 divided by Receivables turnover ratio