PB12–6

Req. 1 DIVE IN COMPANY

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Cash collected from customers1 ………………………………..

$ 33,450

Cash paid for salaries and wages to employees2 …………

(30,750

)

Cash paid for rent and office expenses3 ……………………..

(3,700

)

Net cash provided by (used in) operating activities …

(1,000

)

Cash flows from financing activities:

Cash proceeds from issuing stock …………………………….

200

Net cash provided by financing activities ………………..

200

Net increase (decrease) in cash during the year ……………….

(800

)

Cash balance, January 1 ………………………………………………

4,000

Cash balance, December 31 ………………………………………….

$3,200

1 $33,950 + (500 – 1,000) = $33,450

2 $30,000 + (1,100 – 350) = $30,750

3 $3,650 + (100 – 50) = $3,700

Req. 2

Dive In Company appears to be in a satisfactory cash position, with an ending cash

balance of $3,200. However, this balance is down $800 from the prior year because the

company’s cash flows from operations were negative (-$1,000), which was offset

somewhat by issuing additional stock. The company needs to work at improving its

operating cash flows.

ANSWERS TO SKILLS DEVELOPMENT CASES

S12–1

1. B

2. B

3. D

S12–2

Req. 1

Lowe’s uses the indirect method to report the cash flows from operating activities on its

Statement of Cash Flows. This is the same method used by The Home Depot.

Req. 2

Lowe’s received $985 million from issuing long-term debt during the year ended

million.)

S12–3

The solutions to this project will depend on the company and/or accounting period

S12–4

Req. 1

The payment from Merrill Lynch to Enron does not automatically make the Nigerian

barge transaction a sale. When a loan is established between a lender and borrower, a

similar cash payment is made between the two parties. Two other features of the

Nigerian barge transaction resemble a loan. First, the requirement that Enron arrange

for Merrill Lynch to be paid only six months after the “sale” is similar to a possible

S12–5

Req. 1

The sale of accounts receivable to generate cash does not harm or mislead anyone

provided that this event is fully disclosed to users of the financial statements. If the

reason for the improvement in accounts receivable is not reported, financial statement

users might incorrectly assume that the company has permanently improved its

customer screening and collection processes, rather than temporarily improved them

future benefits did not exist.

It is not appropriate to make a decision about how to account for a transaction based on

the impact it could have on operating cash flows. Decisions should be drawn based on

the facts of the situation, not on whether it will make the club’s financial situation look

better or worse.

Req. 4

S12–6

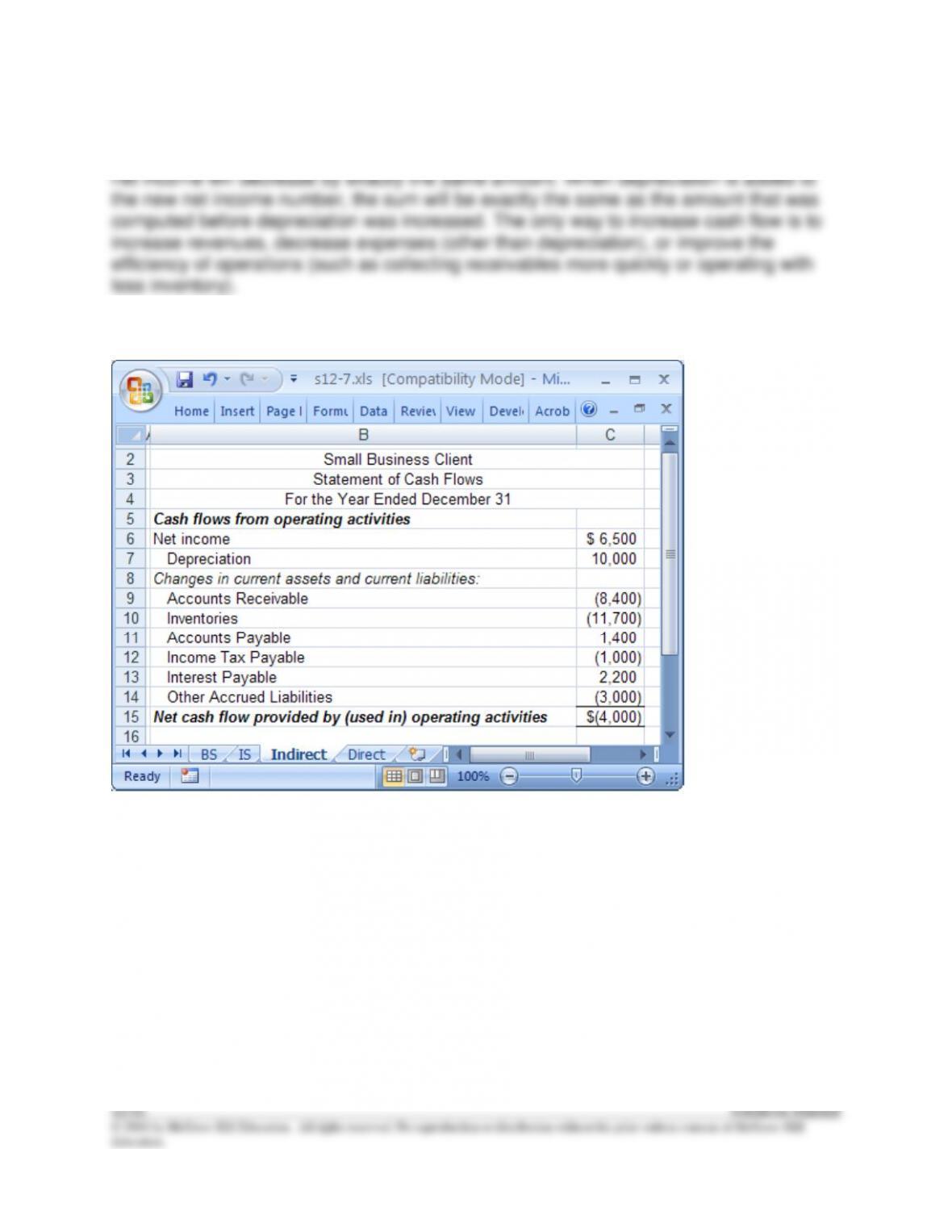

While depreciation is indeed added to net income to compute cash flow from operating

activities, the new controller’s idea will not work. If depreciation expense is increased,

S12–7

S12–8

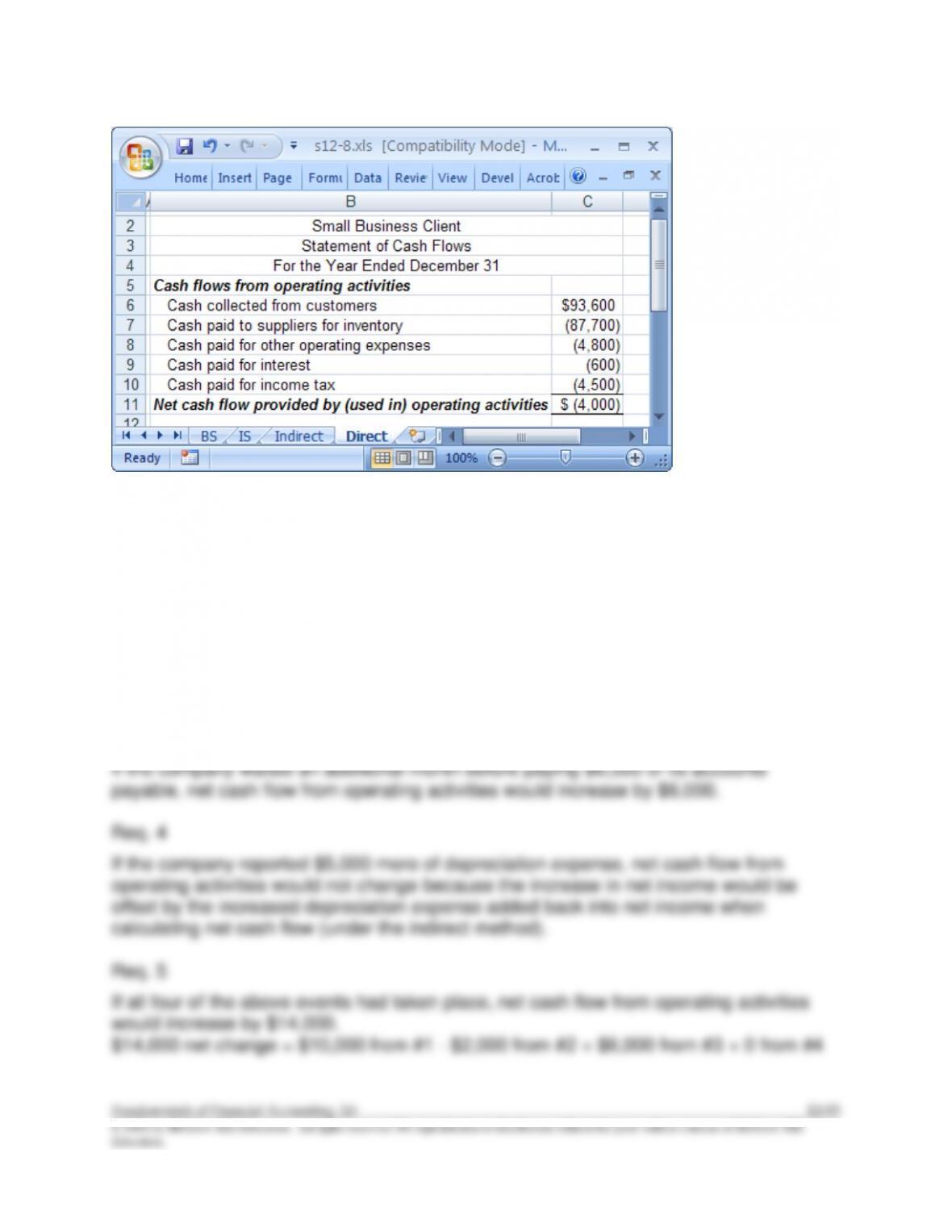

S12–9

Req. 1

If the company collected $10,000 of the accounts receivable, net cash flow from

operating activities would increase by $10,000.

Req. 2

If the company paid down its interest payable by an extra $2,000, net cash flow from

operating activities would decrease by $2,000.

Req. 3

CC12-1

Req. 1

NICOLE’S GETAWAY SPA

Statement of Cash Flows

For the year ended December 31

Cash Flows from Operating Activities

Net Income

Depreciation

Changes in current assets and current liabilities

Accounts Receivable

Inventory

Prepaid Expenses

Accounts Payable

$

2,300

3,000

859

(400)

(2,170)

(320)

Cash Provided by Operating Activities

3,269

Cash Flow from Investing Activities

Purchased new spa equipment

(7,582)

Cash Provided by (Used in) Investing Activities

(7,582)

Cash Flow from Financing Activities

Payments on note payably (long-term)

Issued new company stock

(4,600)

10,000

Cash Provided by Financing Activities

5,400

Net Change in Cash

Beginning Cash

1,087

7,000

Ending Cash

$

8,087

CC12-2