PA12–6

Req. 1 HEADS UP COMPANY

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Cash collected from customers1 ………………………………..

$ 38,350

Cash paid for wages to employees2 …………………………..

(35,250

)

Cash paid for other operating expenses3 …………………….

(500

)

Cash paid for income tax ………………………………………….

(1,000

)

Net cash provided by operating activities ……………….

1,600

Cash flows from investing activities:

Cash payments to purchase equipment …………………….

(500

)

Net cash provided by (used in) investing activities ….

(500

)

Cash flows from financing activities:

Cash proceeds from bank loan …………………………………

1,200

Net cash provided by financing activities ………………..

1,200

Net increase in cash during the year ……………………………….

2,300

Cash balance, January 1 ………………………………………………

4,000

Cash balance, December 31 ………………………………………….

$6,300

1 $37,500 + 1,750 – 900 = $38,350

2 $35,000 + 750 – 500 = $35,250

3 $1,000 – 500 = $500 decrease in accounts payable for operating expenses

Req. 2

Heads Up Company appears to be in a good cash position, with an ending cash

balance of $6,300. This balance is $2,300 greater than the prior year because the

company generated positive cash flows from operations (+$1,600) and obtained

additional funding from the bank, enabling the company to acquire additional equipment

with cash. The company is well positioned to continue expanding its business in the

upcoming year.

PA12–7

Req. 1 HEADS UP COMPANY

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Net income…………………………………………………………….

$1,250

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense …………………………………………….

500

Loss on disposal of equipment ………………………………..

550

Decrease in accounts receivable ……………………………..

850

Decrease in accounts payable …………………………………

(500

)

Decrease in salaries and wages payable…………………..

(250

)

Net cash provided by operating activities ………………

2,400

Cash flows from investing activities:

Cash proceeds from disposal of equipment ………………..

500

Cash payments to purchase equipment …………………….

(1,800

)

Net cash provided by (used in) investing activities ….

(1,300

)

Cash flows from financing activities:

Cash proceeds from bank loan …………………………………

1,200

Net cash provided by financing activities ………………..

1,200

Net increase in cash during the year ……………………………….

2,300

Cash balance, January 1 ………………………………………………

4,000

Cash balance, December 31 ………………………………………….

$6,300

ANSWERS TO GROUP B PROBLEMS

PB12–1

Activity

Cash Flow

O

+

1

Received deposits from customers for products

to be delivered the following period.

F

–

2

Principal repayments on loan.

I

–

3

Paid cash to purchase new equipment.

F

+

4

Received proceeds from loan.

O

+

5

Collected payments on account from customers.

O

–

6

Recorded and paid salaries and wages to

employees.

I

–

7

Paid cash for building construction.

O

–

8

Recorded and paid interest to debt holders.

PB12–2

CALENDARS INCORPORATED

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Net income…………………………………………………………….

$ 10,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense …………………………………………….

$16,000

Increase in accounts receivable ……………………………….

(300

)

Decrease in inventory …………………………………………….

60

Decrease in accounts payable …………………………………

(100

)

Decrease in prepaid rent…………………………………………

20

Decrease in prepaid insurance ………………………………..

20

Increase in salaries and wages payable ……………………

200

Increase in utilities payable ……………………………………..

100

16,000

Net cash provided by operating activities ………………

$26,000

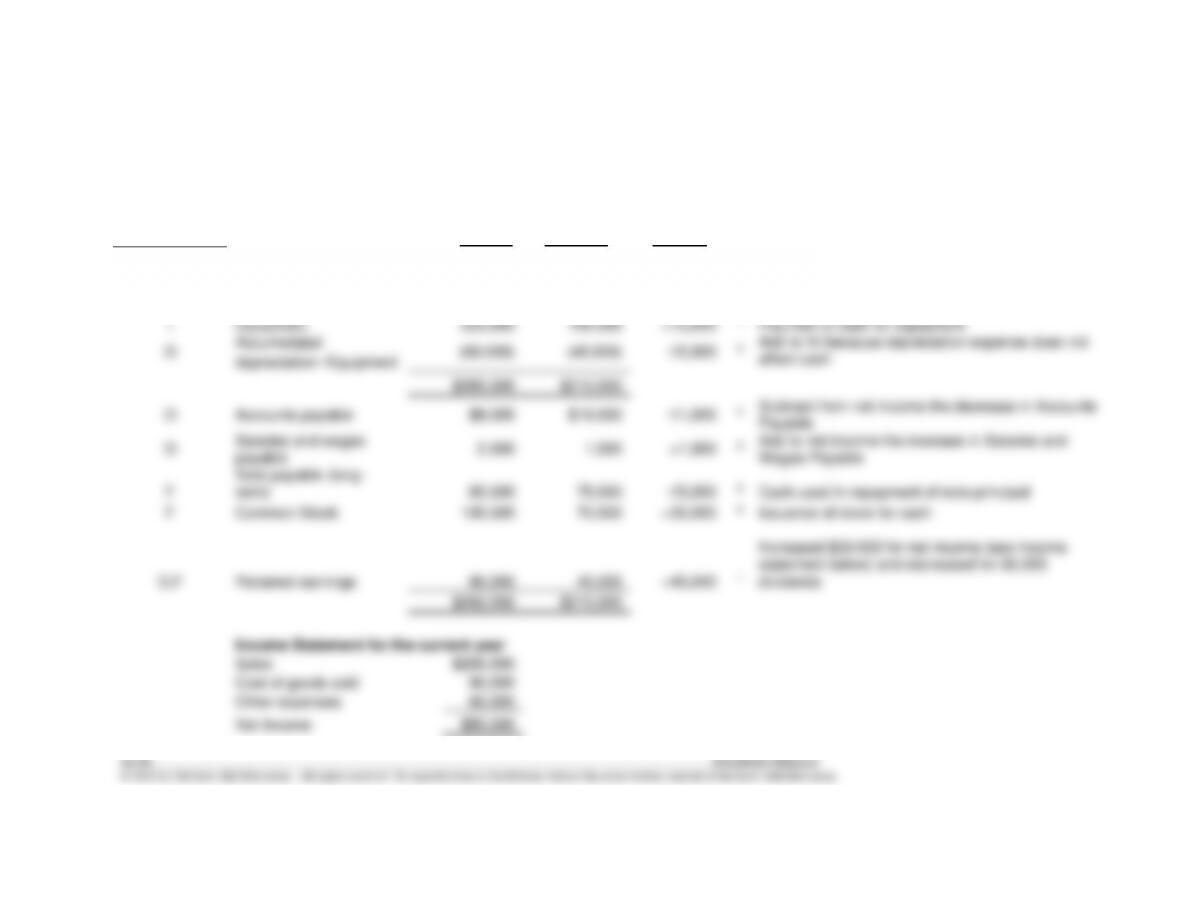

PB12–3

Req.1

Related Cash

Balance Sheet at December 31

Flow Section

Current

Previous

Change

Δ in Cash

Cash

$60,000

$65,000

-5,000

10

Net decrease in cash

O

Accounts receivable

15,000

20,000

-5,000

3

Add to net income the decrease in A/R

O

Inventory

22,000

20,000

+2,000

4

Subtract from net income the increase in Inventory

I

Equipment

223,000

150,000

+73,000

7

Payment in cash for equipment

O

Accumulated

depreciation–Equipment

(60,000)

(45,000)

-15,000

2

Add to NI because depreciation expense does not

affect cash

$260,000

$210,000

O

Accounts payable

$8,000

$19,000

-11,000

5

Subtract from net income the decrease in Accounts

Payable

O

Salaries and wages

payable

2,000

1,000

+1,000

6

Add to net income the increase in Salaries and

Wages Payable

F

Note payable (long–

term)

60,000

75,000

-15,000

8

Cash used in repayment of note principal

F

Common Stock

100,000

70,000

+30,000

9

Issuance of stock for cash

O,F

Retained earnings

90,000

45,000

+45,000

1

Increased $50,000 for net income (see income

statement below) and decreased for $5,000

dividends

$260,000

$210,000

Income Statement for the current year

Sales

$200,000

Cost of goods sold

90,000

Other expenses

60,000

Net Income

$50,000

PB12–3 (continued)

Req. 1 (continued)

Audio City Inc.

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Net income

$50,000

1

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation expense

$15,000

2

Decrease in accounts receivable

5,000

3

Increase in inventory

(2,000)

4

Decrease in accounts payable

(11,000)

5

Increase in salaries and wages payable

1,000

6

8,000

Net cash provided by operating activities

58,000

Cash flows from investing activities:

Cash payments to purchase equipment

(73,000)

7

Net cash provided by (used in) investing activities

(73,000)

Cash flows from financing activities:

Cash payments on note payable (long–

term)

(15,000)

8

Cash receipts from issuing stock

30,000

9

Cash dividends paid

( 5,000)

1

Net cash provided by financing activities

10,000

Net decrease in cash during the year

(5,000)

10

Cash balance, January 1

65,000

Cash balance, December 31

$ 60,000

Req. 2

An overall decrease in cash of $5,000 came from a positive inflow of $58,000 from

operating activities and a stock issuance of $30,000. A large percentage of the cash

inflow was invested in equipment ($73,000), with $15,000 used to pay down long-term

financing and $5,000 paid as dividends.

PB12–4

Req. 1 DIVE IN COMPANY

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Net income…………………………………………………………….

$ 300

Adjustments to reconcile net income to net cash

provided by operating activities:

Increase in accounts receivable ……………………………….

(500

)

Increase in prepaid rent …………………………………………

(50

)

Decrease in salaries and wages payable…………………..

(750

)

Net cash provided by (used in) operating activities …

(1,000

)

Cash flows from financing activities:

Cash proceeds from issuing stock …………………………….

200

Net cash provided by financing activities ………………..

200

Net increase (decrease) in cash during the year ……………….

(800

)

Cash balance, January 1 ………………………………………………

4,000

Cash balance, December 31 ………………………………………….

$3,200

Req. 2

Dive In Company appears to be in a satisfactory cash position, with an ending cash

balance of $3,200. However, this balance is down $800 from the prior year because the

company’s cash flows from operations were negative (-$1,000). Much of the negative

cash flow was caused by delayed collection of accounts receivable and earlier payment

of wages in comparison to the prior year. The company needs to work at improving its

operating cash flows.

PB12–5

CALENDARS INCORPORATED

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Cash receipts from customers1 ………………………………………………………

$77,700

Cash payments to suppliers2 …………………………………………………………

(36,040

)

Cash payments for salaries and wages3 ………………………………………….

(9,800

)

Cash payments for rent4 ……………………………………………………………….

(2,480

)

Cash payments for insurance5 ……………………………………………………….

(1,280

)

Cash payments for utilities6 …………………………………………………………..

(900

)

Cash payments for interest …………………………..……………………………….

(1,200

)

Net cash provided by operating activities …………………………………..

$ 26,000

Note 1: $78,000 + $1,500 – $1,800 = $77,700

Note 2: $36,000 + ($1,300 – $1,200) – ($490-430) = $36,040

Note 3: $10,000 + $250 – $450 = $9,800

Note 4: $2,500 + ($80 – $100) = $2,480

Note 5: $1,300 + ($70 – $90) = $1,280

Note 6: $1000 – $100 = $900