E12–14 (continued)

Req. 5

Under the indirect method, to convert from the cash basis to the accrual basis, you must

make the following adjustments to net income: subtract increases in inventory (a current

asset) and add increases in accounts payable (a current liability).

Aztec Corporation

Bikes Unlimited

Campus Cycles

Subtract inventory

increase

$ (25)

$ (25)

$ (50)

Add accounts

payable increase

0

40

40

Total

$ (25)

$ 15

$ (10)

Req. 6

Answers to requirements 3 and 5 should be identical for each company. The reason

they should be the same is that requirement 3 identifies the differences between accrual

and cash based amounts by examining amounts that were recorded during the year,

whereas requirement 5 identifies these differences by examining the changes in year-

end balances of accounts affected by inventory purchases. The two requirements

approach the same goal (i.e., the adjustment needed to convert accrual to cash basis)

from different directions.

E12–15

The investing and financing sections of the statement of cash flows for Rowe Furniture:

Cash flows from investing activities:

Purchase of equipment ……………………………………………….

(871)

Sale of investments …………………………………………………

134

Proceeds from sale of equipment ………………………………..

6,594

Net cash provided by investing activities …………………

5,857

Cash flows from financing activities:

Borrowings under line of credit …………………………………….

1,417

Proceeds from issuance of common stock …………………..

11

Payments on notes payable (long-term) ………………………

(46)

Payment of dividends ………………………………………………….

(277)

Net cash provided by financing activities…………………

1,105

E12–16

The investing and financing sections of the statement of cash flows for Gibraltar

Industries, Inc.:

Cash flows from investing activities:

Purchase of equipment ……………………………………………….

(14,940)

Proceeds from sale of equipment ………………………………..

12,610

Net cash provided by (used in) investing activities …..

(2,330)

Cash flows from financing activities:

Proceeds from notes payable (bank) …………………………...

210,000

Net proceeds from stock issuance ……………………………….

648

Payments on notes payable (bank) ……………………………..

(205,094)

Net cash provided by (used in) financing activities ….

5,554

E12–17

Req. 1

Disney’s cash from operations was greater than its net income in each of the three

years. This difference occurs because Disney’s large investment in capital assets

E12–18

E12–19

Req. 1

Cash flows from operating activities—direct method

Cash collected from customers1

$78,000

Cash payments to employees2

(33,000

)

Cash paid for other expenses3

(11,950

)

Net cash provided by operating activities …………………………………….

$33,050

E12–20

Req. 1

Cash flows from operating activities—direct method

Cash collected from customers1

$136,330

Cash payments to suppliers2

(47,139)

Cash payments to employees

(56,835)

Cash payments for other expenses3

(9,164)

Cash payments for income tax4

(700)

Net cash provided by operating activities

$22,492

1 Cash collected from customers: $136,500 – $170 = $136,330

2 Cash payments to suppliers: $45,500 – $643 + $2,282 = $47,139

3 Cash payments for office expenses: $7,781 + $664 + $719 = $9,164

4 Cash payments for income taxes: $2,561 – $1,861 = $700

Req. 2

The primary reason for the net loss was the depreciation expense. Depreciation

expense is a noncash expense so it is excluded when computing cash flow from

operating activities (when using the direct method).

E12–21

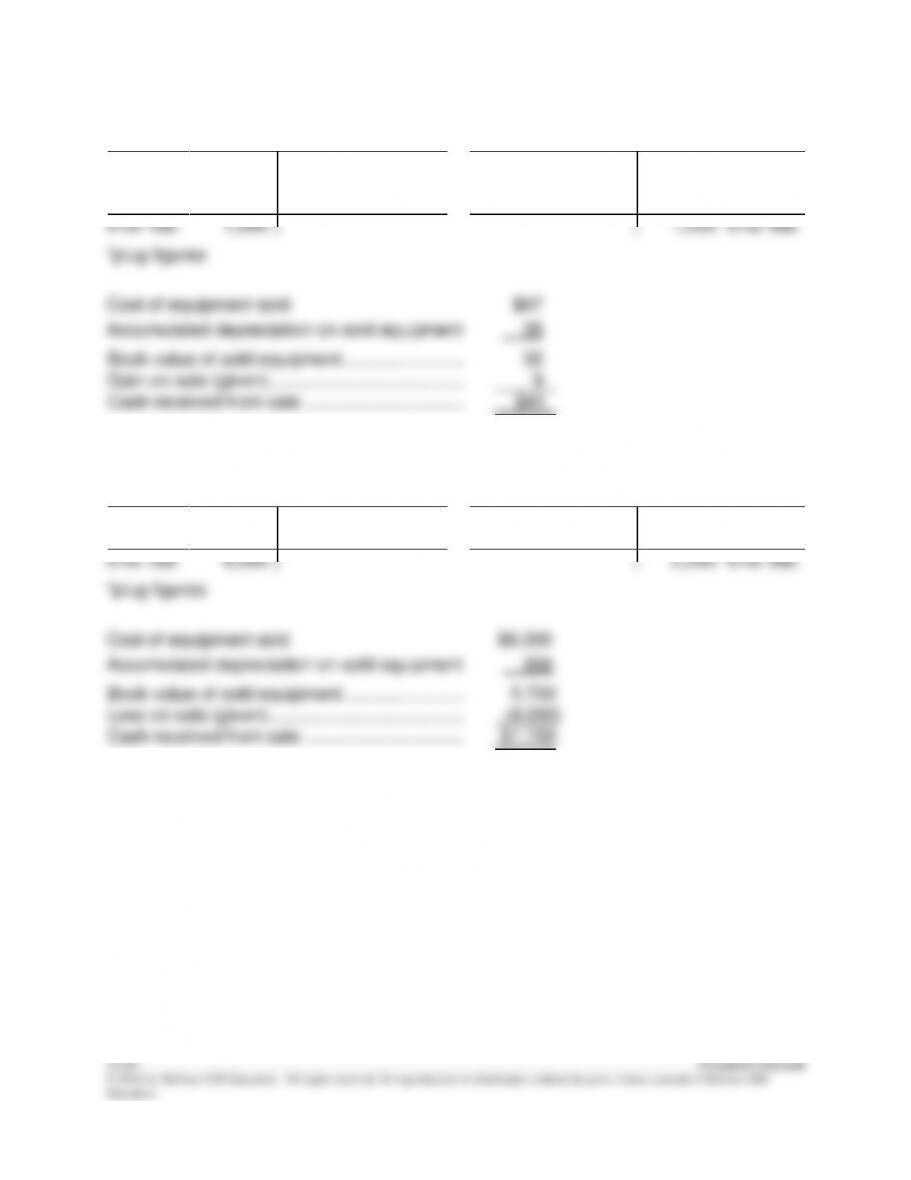

Equipment

Accumulated Depreciation–Equipment

Beg. Bal.

1,450

1,160

Beg. Bal.

Purchase

120

3

67*

Impair.

Sold

Sold

35*

125

Dep. Exp.

End. Bal.

1,500

1,250

End. Bal.

Gain on sale (given) …………………………………

Cash received from sale …………………………..

Equipment

Accumulated Depreciation–Equipment

Beg. Bal.

2,000

Beg. Bal.

Sold

Dep. Exp.

End. Bal.

End. Bal.

Loss on sale (given) …………………………………

(4,000

)

Cash received from sale …………………………..

E12–23

Req. 1

E12-23

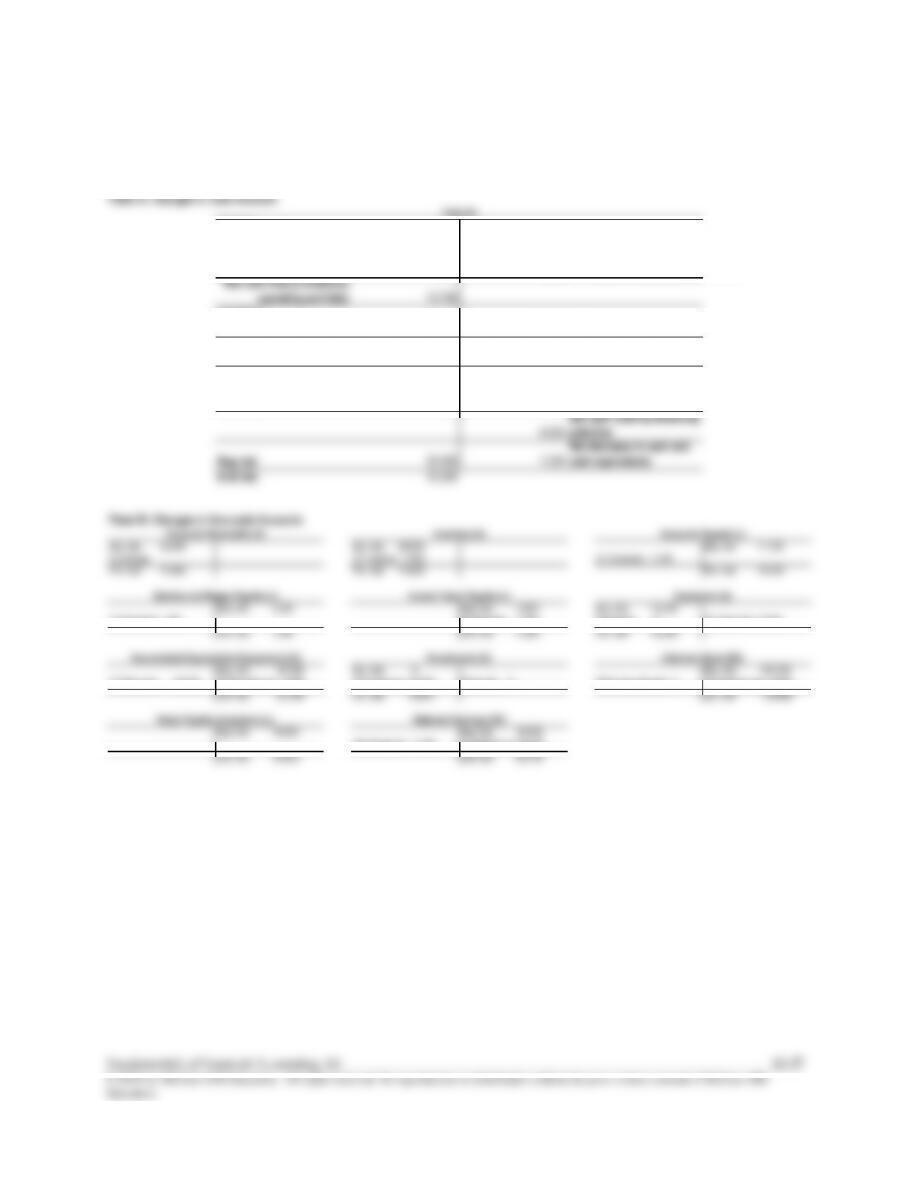

Panel A: Changes in Cash Account

Operating

(1) Net Income

20,200 7,000 (3) Inventory

(2) Depreciation Expense

3,000 3,000 (4) Accounts Payable

(6) Income Taxes Payable

1,500 1,000 (5) Salaries and Wages Payable

13,700

Investing

(7) Sale of Equipment

6,000 15,000 (8) Purchased Investment

9,000

Financing

6,000 12,000

(10) Payment of

dividends

6,000

20,500 1,300

End. bal. 19,200

Panel B: Changes in Non-cash Accounts

Beg. bal. 22,000 Beg. bal. 68,000 Beg. bal. 17,000

No change (3) Increase 7,000 (4) Decrease 3,000

End. bal. 22,000 End. bal. 75,000 End. bal. 14,000

Beg. bal. 2,500 Beg. bal. 3,000 Beg. bal. 114,500

(5) Decrease 1,000 (6) Increase 1,500 Purchases 0 (7) Disposals 21,000

End. bal. 1,500 End. bal. 4,500 End. bal. 93,500

Beg. bal. 32,000 Beg. bal. 0 Beg. bal. 100,000

(7) Disposals 15,000 (2) Depreciation 3,000 (8) Purchases 15,000 Disposals 0 Stock repurchased 0 (9) Stock issued 6,000

End. bal. 20,000 End. bal. 15,000 End. bal. 106,000

Beg. bal. 54,000 Beg. bal. 16,500

(10) Dividends 12,000 (1) Net income 20,200

End. bal. 54,000 End. bal. 24,700

Investments (A)

Common Stock (SE)

Notes Payable (long-term) (L)

Retained Earnings (SE)

Accumulated Depreciation-Equipment (xA)

Cash (A)

Net cash flow provided by

operating activities

Net cash used in investing

activities

(9) Proceeds from stock

issuance

Net cash used by financing

activities

Beg. bal.

Accounts Receivable (A)

Inventory (A)

Accounts Payable (L)

Salaries and Wages Payable (L)

Income Taxes Payable (L)

Equipment (A)

Net decrease in cash and

cash equivalents

E12–23 (continued)

Req. 2

GOLF UNIVERSE STORE

Statement of Cash Flows

For the Year Ended December 31

Cash flows from operating activities:

Net income

$ 20,200

Depreciation expense

3,000

Changes in current assets and current liabilities

Inventory

(7,000

)

Accounts payable

(3,000

)

Salaries and wages payable

(1,000

)

Income taxes payable

1,500

Cash flows provided by operating activities

13,700

Cash flows from investing activities:

Purchase of investment

(15,000

)

Proceeds from sale of equipment

6,000

Cash flows provided by (used in) investing activities

(9,000

)

Cash flows from financing activities:

Issuance of common stock

6,000

Dividends paid

(12,000

)

Cash flows provided by (used in) financing activities

(6,000

)

Net increase (decrease) in cash

(1,300

)

Cash, beginning of year

20,500

Cash, end of year

$ 19,200

Fundamentals of Financial Accounting, 5/e 12-29

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO COACHED PROBLEMS

CP12–1

Activity

Cash

Flow

I

–

1

Purchased new equipment with cash.

O

–

2

Recorded and paid income taxes to the federal government.

F

+

3

Issued shares of stock for cash.

O

–

4

Prepaid rent for the following period.

I

–

5

Paid cash to purchase new equipment.

F

+

6

Issued long-term promissory notes for cash.

O

+

7

Collected payments on account from customers.

O

–

8

Recorded and paid salaries and wages to employees.

CP12–2

HAMBURGER HEAVEN

Statement of Cash Flows

For the Year Ended December 31, 2015

Cash flows from operating activities:

Net income…………………………………………………………….

$ 20

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense …………………………………………….

$200

Decrease in accounts receivable ……………………………..

70

Increase in inventory …………………………..………………….

(22

)

Decrease in prepaid rent…………………………………………

8

Increase in prepaid insurance ………………………………….

(9

)

Decrease in accounts payable …………………………..…….

(10)

Increase in salaries and wages payable ……………………

9

Decrease in utilities payable ……………………………………

(40

)

Total adjustments …………………………………………………

206

Net cash provided by operating activities ………………

$226

CP12–3

Req.1

Related

Cash

Balance Sheet at December 31

Flow

Section

2015

2014

Change

Cash

Cash

$ 44,000

$ 18,000

+26,000

11

Net increase in cash

O

Accounts receivable

27,000

29,000

-2,000

3

Add to net income the decrease in A/R

O

Inventory

30,000

36,000

-6,000

4

Add to net income the decrease in Inventory

I

Equipment

111,000

102,000

+9,000

7

Payment in cash for equipment

O

Accumulated

Depreciation–

Equipment

(36,000)

(30,000)

-6,000

2

Add to net income because depreciation expense does not

affect cash

$176,000

$155,000

O

Accounts payable

$ 25,000

$ 22,000

+3,000

5

Add to net income the increase in Accounts Payable

O

Salaries and wages

payable

800

1,000

–200

6

Subtract from net income the decrease in Wages Payable

F

Note payable (long-term)

38,000

48,000

-10,000

8

Cash used in repayment of note principal

F

Common Stock

80,000

60,000

+20,000

9

Issuance of stock for cash

O,F

Retained earnings

32,200

24,000

+8,200

1,10

Increased for net income +12,000 (see income statement

below) and decreased by cash dividends paid -3,800

$176,000

$155,000

Income Statement for 2015

Sales revenue

$100,000

Cost of goods sold

61,000

Other expenses

27,000

Net Income

$12,000