Chapter Outline

Teaching Notes

H. Supplemental Disclosures

1. In addition to their cash flows, all companies are required

to report material investing and financing transactions

that did not have cash flow effects (called noncash

investing and financing activities).

2. These activities are not listed in the three main sections of

the statement of cash flows.

3. This important information is normally presented for users

in a supplementary schedule to the statement of cash

flows or in the financial statement notes.

4. Supplementary information must also report (for

companies using the indirect method) the amount of cash

paid for interest and for income taxes.

LO 12-5 Interpret cash flows from operating, investing, and financing activities using ratios.

III. Evaluate the Results

A. Free Cash Flow

1. An established, healthy company will show positive cash

flows from operations, which are sufficiently large to pay

for replacing existing property, plant, and equipment and

to pay dividends to stockholders.

2. Any additional cash (called free cash flow) can (a) be

used to expand the business through additional investing

activities, (b) be used for other financing activities, or (c)

simply build up the company’s cash balance.

B. Evaluating Cash Flows

2. Cash Flows from Operating Activities

a. When evaluating the operating activities section of the

statement of cash flows, consider the absolute amount

of cash, keeping in mind that operating cash flows

have to be positive over the long run for a company to

be successful.

The “Spotlight on Business

Decision” feature addresses

Lehman Brothers’ operating

cash flows and the financial

crisis

b. All other things being equal, when net income and

operating cash flows are similar, there is a high

likelihood that revenues are realized in cash and that

expenses are associated with cash outflows; any major

deviations should be investigated.

c. Four potential causes of deviations to consider

include:

i. Seasonality

ii. The corporate life cycle (growth in sales)

iii. Changes in revenue and expense recognition

iv. Changes in working capital management

Chapter Outline

Teaching Notes

3. Cash Flows from Investing Activities

a. Healthy companies tend to show negative cash flows

in the investing section of the statement of cash flows.

b. A negative total for this section means the company is

spending more to acquire new long-term assets than it

is taking in from selling its existing long-term assets.

c. Positive total cash flow in the investing activities

section can raise concerns because it could mean the

company is selling off its long-term assets just to

generate cash inflows.

4. Cash Flows from Financing Activities

a. The financing activities section does not have an

obvious expected direction for cash flows.

b. Detailed line items within this section need to be

considered to assess the company’s overall financing

strategy. (Is the company moving toward greater

reliance on risky debt financing?)

5. Overall Patterns of Cash Flows

a. Corporate lifecycle phases include:

Illustrated in Exhibit 12.8

i. An introductory phase when the company is being

established.

ii. A growth phase when the company’s presence

expands.

iii. A maturity phase when the company stabilizes.

iv. A decline phase when the company loses its way.

b. During each of these phases, a company is likely to

show different patterns of net cash flows from

operating, investing, and financing activities.

i. Introductory (start-up) phase—Most companies

experience negative net operating cash flows.

ii. Growth phase—Operating cash flows turn positive

because the company has improved its cash inflows

from customers.

iii. Maturity phase—The company generates positive

operating cash flows, but no longer has

opportunities for expanding the business, so it

stops spending cash on investing activities and

instead uses its cash for financing activities.

iv. Decline phase—A company’s operating cash flows

again become negative.

Chapter Outline

Teaching Notes

LO 12-6 Report and interpret cash flows from operating activities, using the direct method.

C. Reporting Operating Cash Flows with the Direct Method

✓ Activity #3

1. Direct method presents a summary of all operating

transactions that result in either a debit or a credit to cash.

Illustrated in Exhibit 12.9

2. Prepared by adjusting each revenue and expense on the

income statement from the accrual basis to the cash basis.

3. The following adjustments must commonly be made to

convert income statement items to the related operating

cash flow amounts:

a. Converting Sales Revenues to Cash Inflows:

Sales Revenue + Decrease in Accounts Receivable (A)

(or – Increase in Accounts Receivable (A)) =

Collections from customers.

b. Converting Cost of Goods Sold to Cash Paid to

Suppliers:

Cost of Goods Sold + Increase in Inventory (A) (or –

Decrease in Inventory (A)) – Increase in Accounts

Payable (L) (or + Decrease in Accounts Payable (L)) =

Payments to suppliers of inventory.

c. Converting Operating Expense to Cash Outflow:

Other Expenses + Increase in Prepaid Expenses (A)

(or – Decrease in Prepaid Expenses (A)) – Increase in

Accrued Expenses (L) (or + Decrease in Accrued

Expenses (L)) = Payments to suppliers of services

(e.g., rent, utilities, wages, interest).

IV. Supplement 12A: Report cash flows from Property, Plant, and

Equipment (Indirect Method)

LO 12-S1 Report cash flows from PPE disposals using the indirect method.

A. Whenever a company sells property, plant, and equipment

(PPE), it records three things:

1. Decreases in the PPE accounts for the assets sold,

2. An increase in the Cash account for the cash received on

disposal, and

3. A gain if the cash received is more than the book value of

the assets sold (or a loss if the cash received is less than

the book value of the assets sold).

B. The only part of this transaction that qualifies for the

statement of cash flows is the cash received on disposal.

1. This cash inflow is classified as an investing activity, just

like the original equipment purchase.

2. Since a gain on sale are included in net income, the gain

on sale is subtracted (or the loss is added) as an

adjustment to net income in the operating activities

section as an adjustment to net income in the operating

activities section.

3. The proceeds from the disposal or sale are listed as a cash

inflow in the investing activities section.

V. Supplement 12B: T-Account Approach (Indirect Method)

LO 12–S2 Use the T-account approach for preparing an indirect method statement of cash flows.

A. Cash T-account

1. Instead of creating separate schedules for each section of

the statement, many accountants prefer to prepare a single

large T-account to represent the changes that have taken

place in cash subdivided into the three sections of the

cash flow statement.

Illustrated in Panel A of

Exhibit 12B.1

2. The cash account in Panel A shows increases in cash as

debits and decreases in cash as credits; each section

matches the three schedules that we prepared for Under

Armour’s cash flows presented in Exhibits 12.4, 12.5, and

12.6.

3. Panel B includes the same T-accounts for the noncash

balance sheet accounts we used in our discussion of each

cash flow statement section in the body of the chapter;

each change in the noncash balance sheet accounts has a

number referencing the change in the cash account that it

accompanies.

Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 12–1

Use Handout 12–1 for an in-class activity designed to review the reporting of various items in the

three cash flow statement categories. The solution follows the handout master.

2. Handout 12–2

Use Handout 12–2 for an in-class activity designed to review the preparation of the statement of cash

flows using the indirect method. The solution follows the handout master.

3. Handout 12–3

Use Handout 12–3 for an in-class activity designed to review the preparation of the statement of cash

flows using the direct method. The solution follows the handout master.

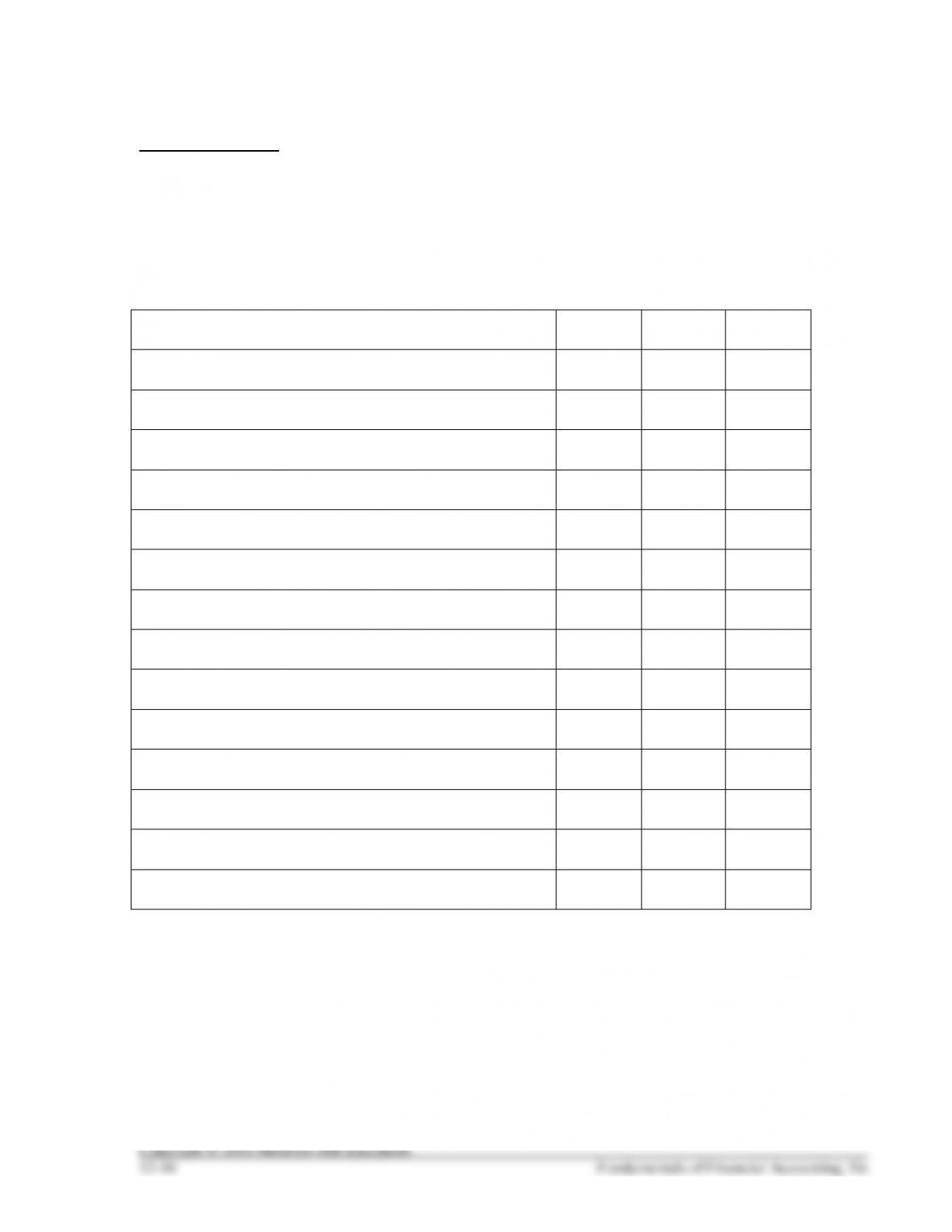

HANDOUT 12–1

CASH FLOW CATEGORIES

Maya Corporation reports the following items in its statement of cash flows prepared using the direct

method. Indicate whether each item is disclosed in the operating, investing, or financing activities section

of the statement.

Operating

Investing

Financing

Cash paid for salaries and wages

Cash paid to purchase property, plant, and equipment

Cash received from issuing common stock to owners

Cash paid for income taxes

Cash paid to purchase investments in securities

Dividends paid to owners

Interest paid on liabilities

Cash received from sale of property, plant, and equipment

Cash used for repaying principal to lenders

Cash used to repurchase stock from owners

Cash provided by dividends and interest on investments

Cash received from customers

Cash from sale or maturity of investments in securities

Cash provided by borrowing from a bank

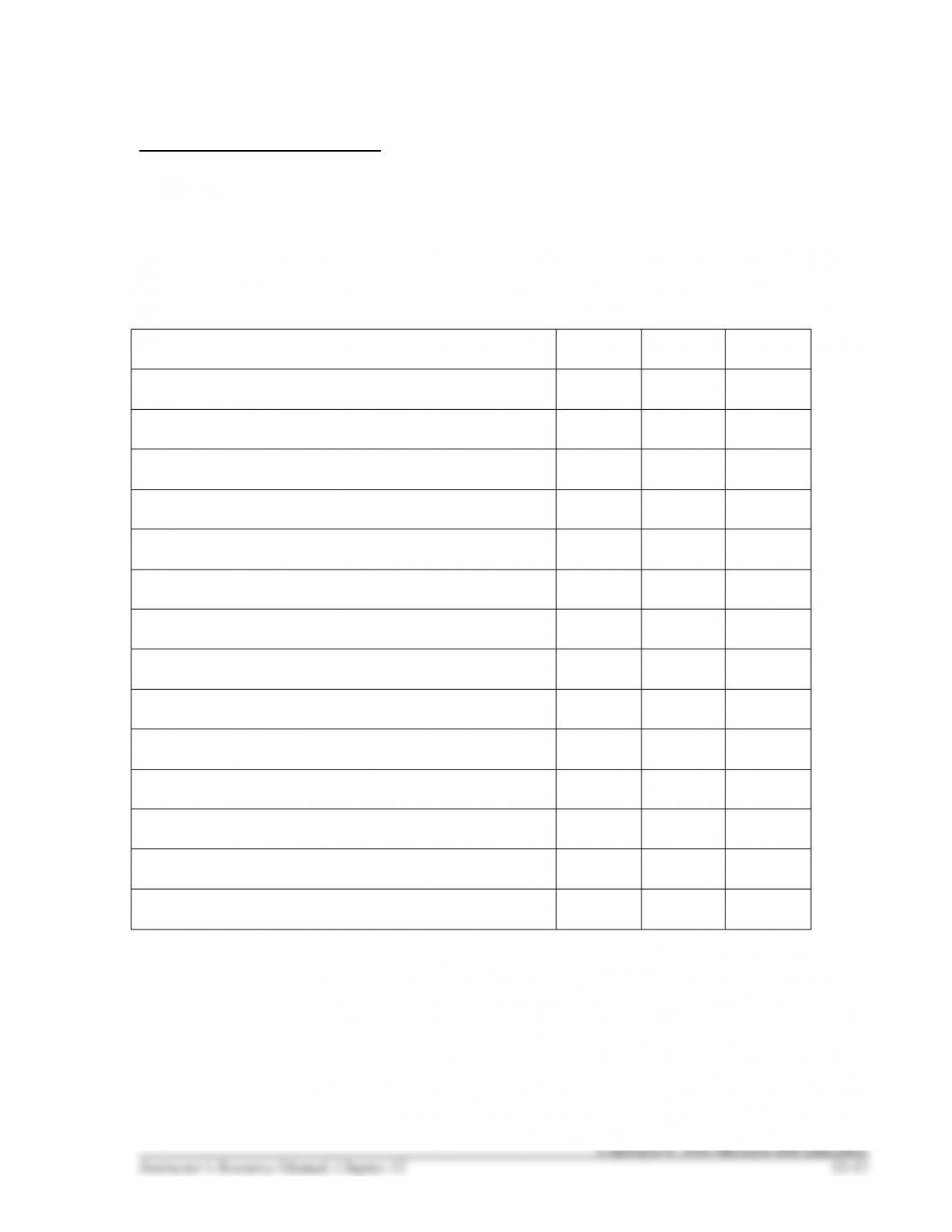

HANDOUT 12–1 SOLUTION

CASH FLOW CATEGORIES

Maya Corporation reports the following items in its statement of cash flows prepared using the direct

method. Indicate whether each item is disclosed in the operating, investing, or financing activities section

of the statement.

Operating

Investing

Financing

Cash paid for salaries and wages

X

Cash paid to purchase property, plant, and equipment

X

Cash received from issuing common stock to owners

X

Cash paid for income taxes

X

Cash paid to purchase investments in securities

X

Dividends paid to owners

X

Interest paid on liabilities

X

Cash received from sale of property, plant, and equipment

X

Cash used for repaying principal to lenders

X

Cash used to repurchase stock from owners

X

Cash provided by dividends and interest on investments

X

Cash received from customers

X

Cash from sale or maturity of investments in securities

X

Cash provided by borrowing from a bank

X

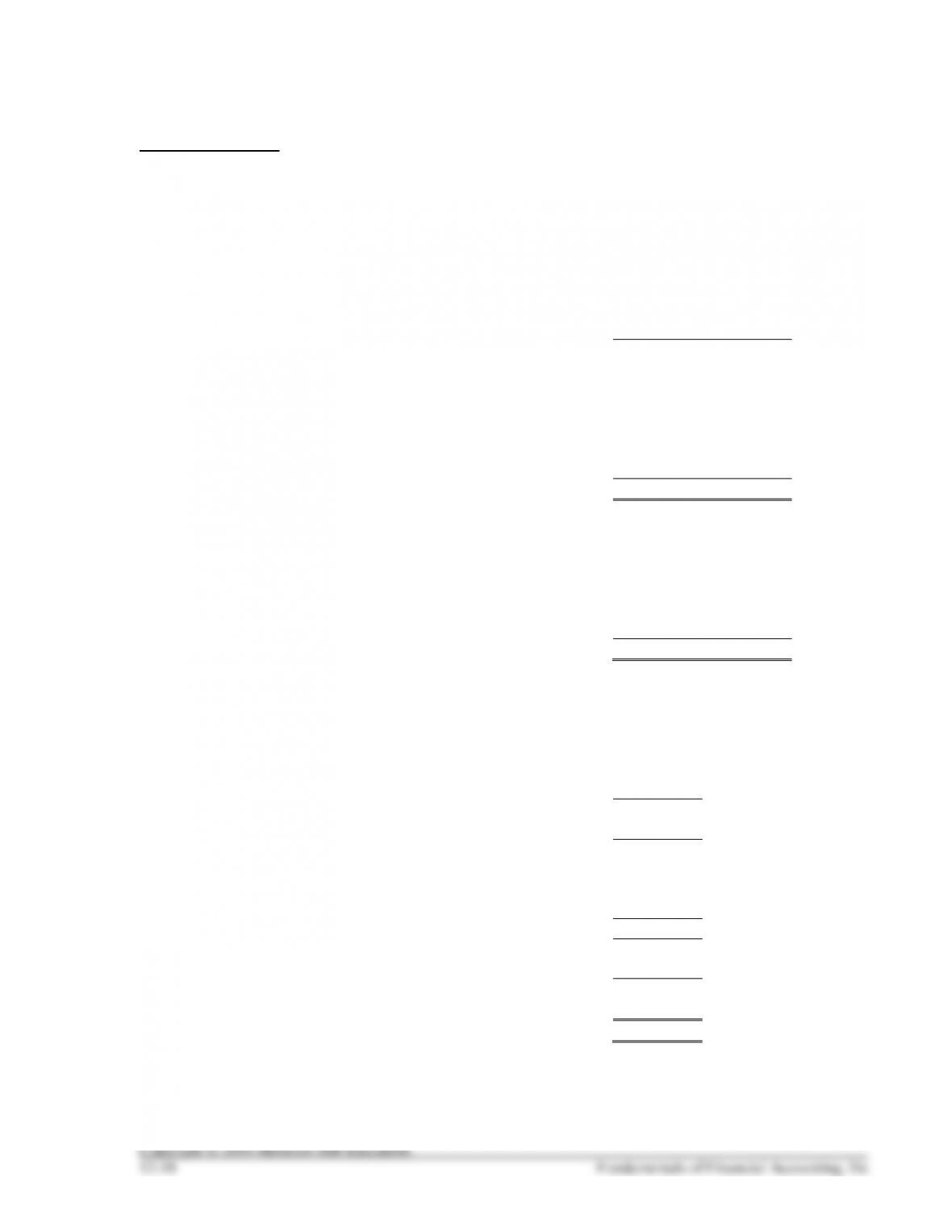

HANDOUT 12–2

STATEMENT OF CASH FLOWS (INDIRECT METHOD)

The Group, Inc.

Consolidated Balance Sheet

December 31

(in thousands)

Current

Year

Prior

Year

ASSETS

Cash and Cash Equivalents

$92,069

$72,634

Accounts Receivables, Net

55,947

75,492

Inventories

50,784

53,129

Prepaid Expenses

12,112

13,057

Equipment

145,444

134,312

Accumulated Depreciation

(50,515)

(36,689)

Total Assets

$305,841

$311,935

LIABILITIES AND STOCKHOLDERS’ EQUITY

Accounts Payable

$25,466

$34,879

Accrued Liabilities

40,574

40,722

Long-Term Debt

10,422

10,206

Common Stock

1,662

1,284

Retained Earnings

227,717

224,844

Total Liabilities And Stockholders’ Equity

$305,841

$311,935

Consolidated Statement of Income

Year Ended December 31

(in thousands)

Current

Year

Net Sales

$130,896

Cost of Sales

74,040

Gross Profit

56,856

Operating Expenses:

Selling, General & Administrative Expenses

33,211

Depreciation Expense

13,826

Total Operating Expenses

47,037

Operating Income

9,819

Interest Income

239

Income Before Income Taxes

10,058

Income Tax Expense

3,621

Net Income

$6,437