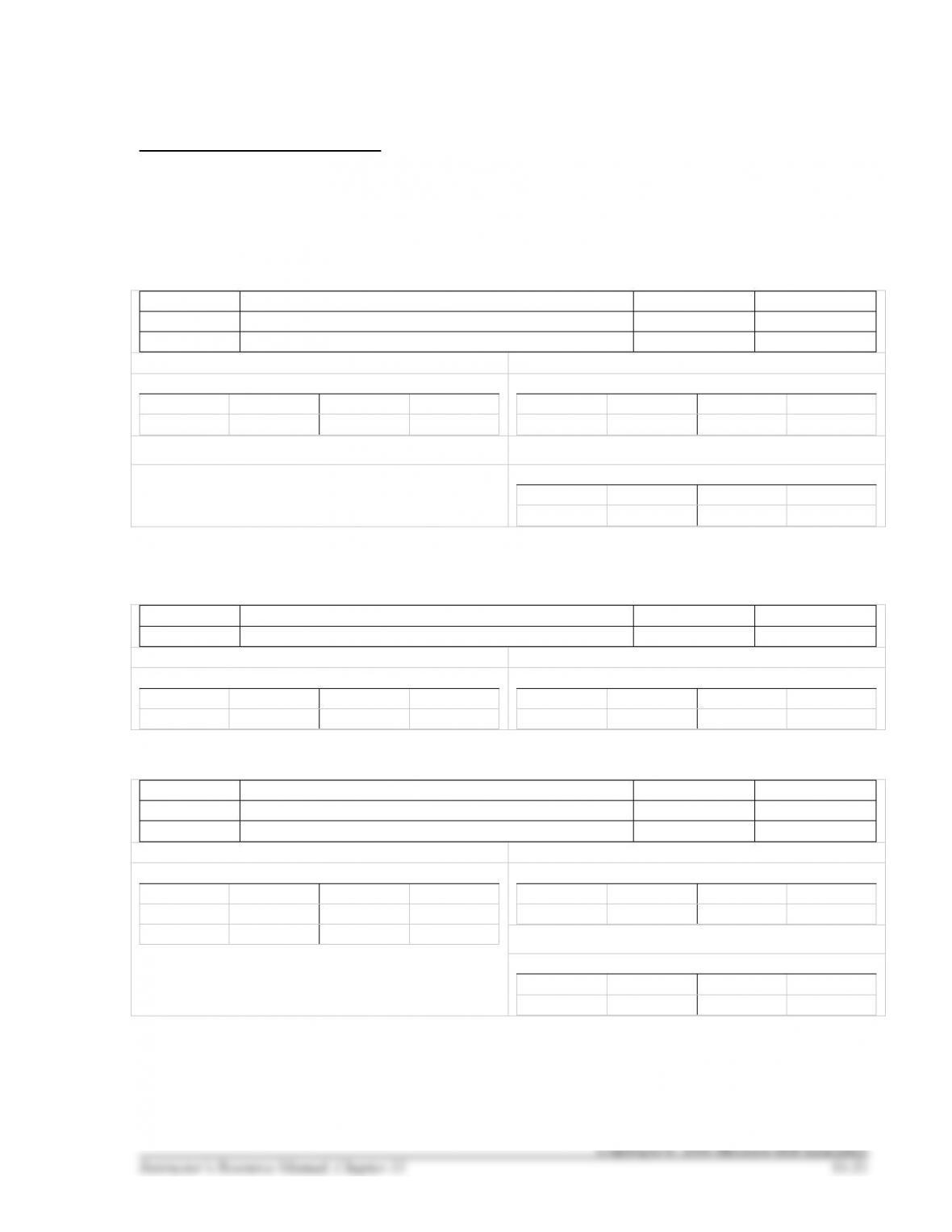

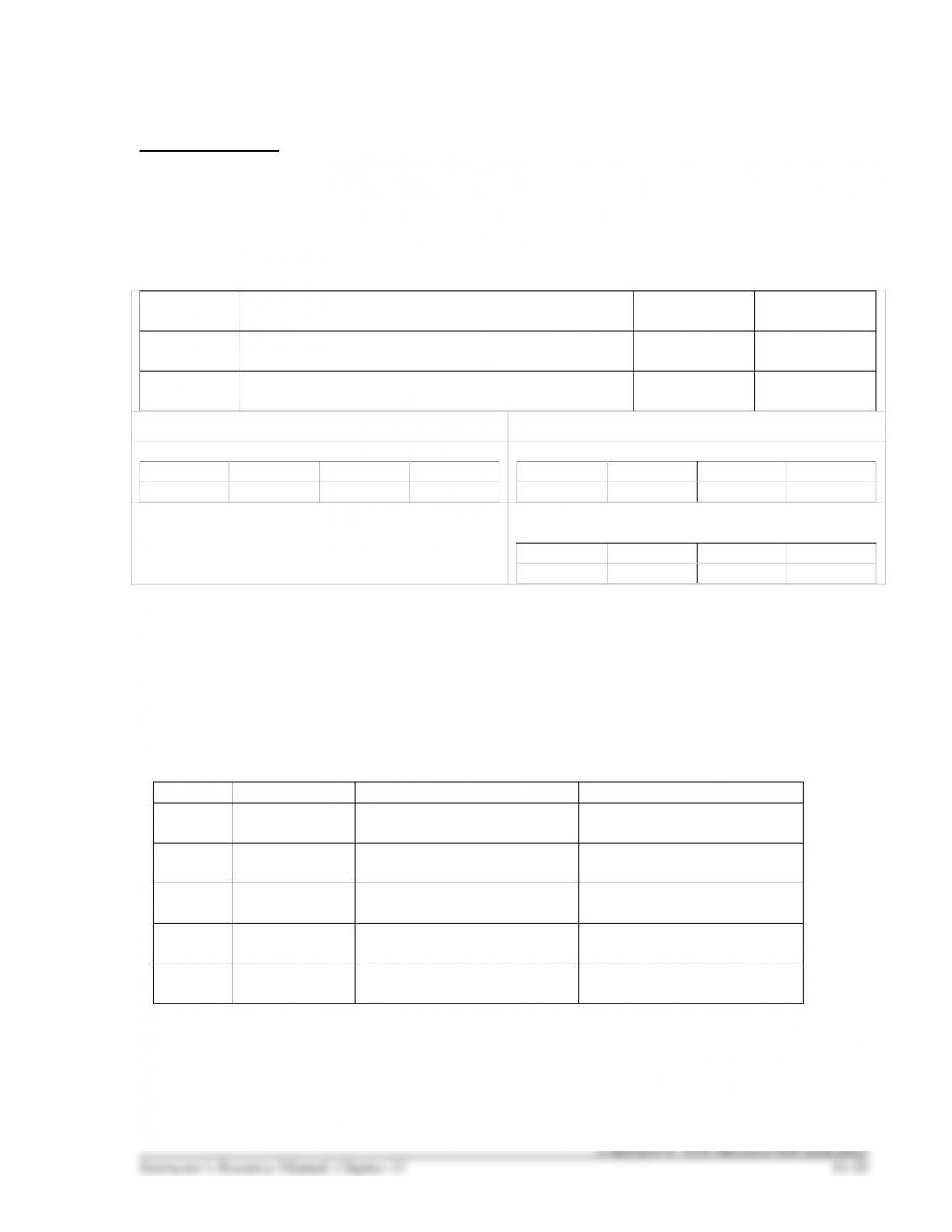

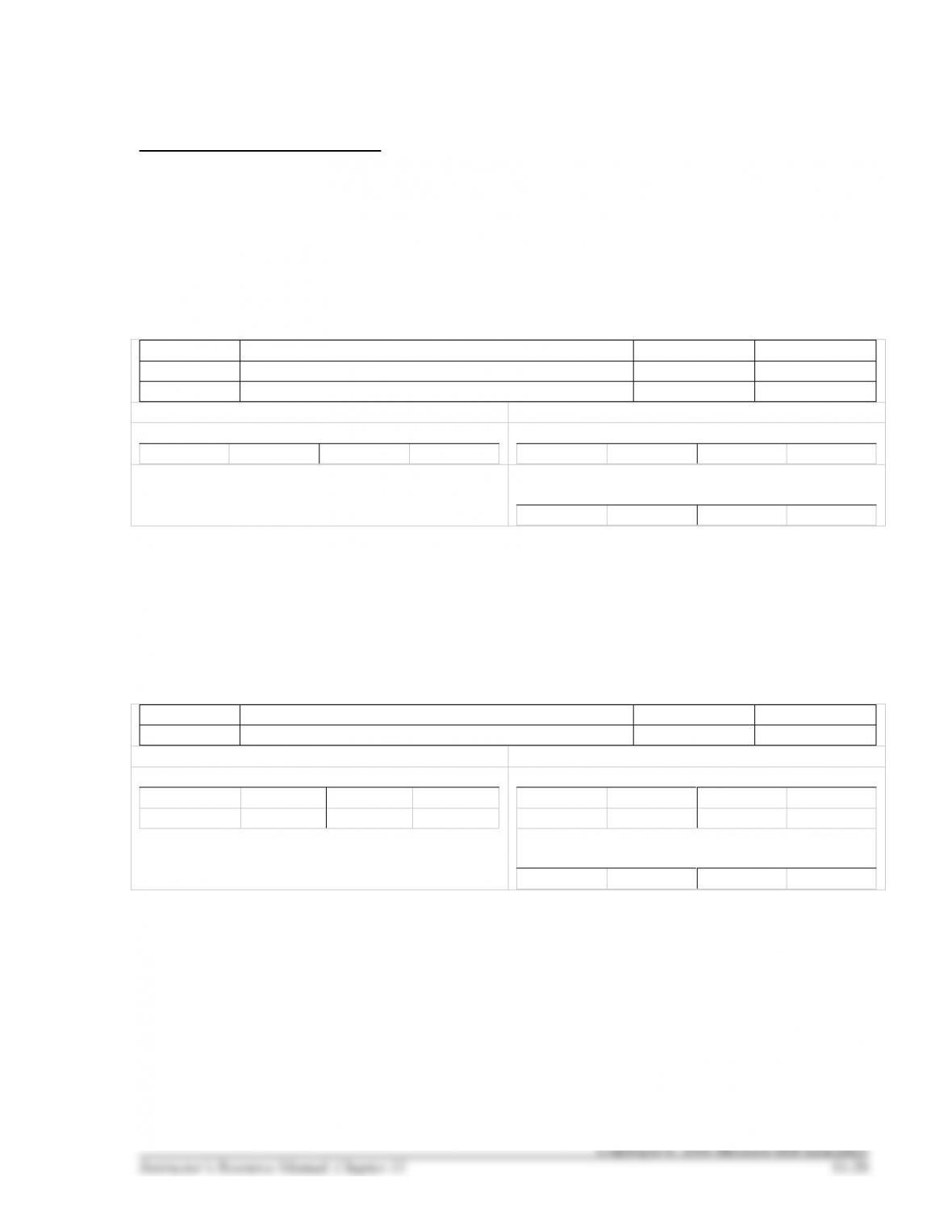

HANDOUT 11–1 SOLUTION

STOCK TRANSACTIONS

Prepare the journal entries required to record the following transactions and then post them to the related

T-accounts:

Strait Corp. sold 10,000 shares of $1 par value stock for $25 per share on May 1.

May 1

Cash (10,000 × $25)

250,000

Common Stock (10,000 × $1)

10,000

Additional Paid-in Capital ($250,000 – $10,000)

240,000

+ Cash (A) –

May 1

250,000

– Common Stock (SE) +

10,000

May 1

– Additional Paid-in Capital (SE) +

240,000

May 1

On December 1, Strait Corp. repurchased 1,000 shares of its stock on the market when it was trading for

$16 per share.

Dec. 1

Treasury Stock (1,000 × $16)

16,000

Cash (–A)

16,000

+ Cash (A) –

May 1

250,000

16,000

Dec. 1

+ Treasury Stock (xSE) –

Dec. 1

16,000

On December 15, Strait Corp. sold 500 of the treasury shares for $30 each.

Dec. 15

Cash (500 × $30)

15,000

Treasury Stock (500 × $16)

8,000

Additional Paid-in Capital (500 × [$30 – $16])

7,000

+ Cash (A) –

May 1

250,000

16,000

Dec. 1

Dec. 15

15,000

+ Treasury Stock (xSE) –

Dec. 1

16,000

8,000

Dec. 15

– Additional Paid-in Capital (SE) +

240,000

May 1

7,000

Dec. 15

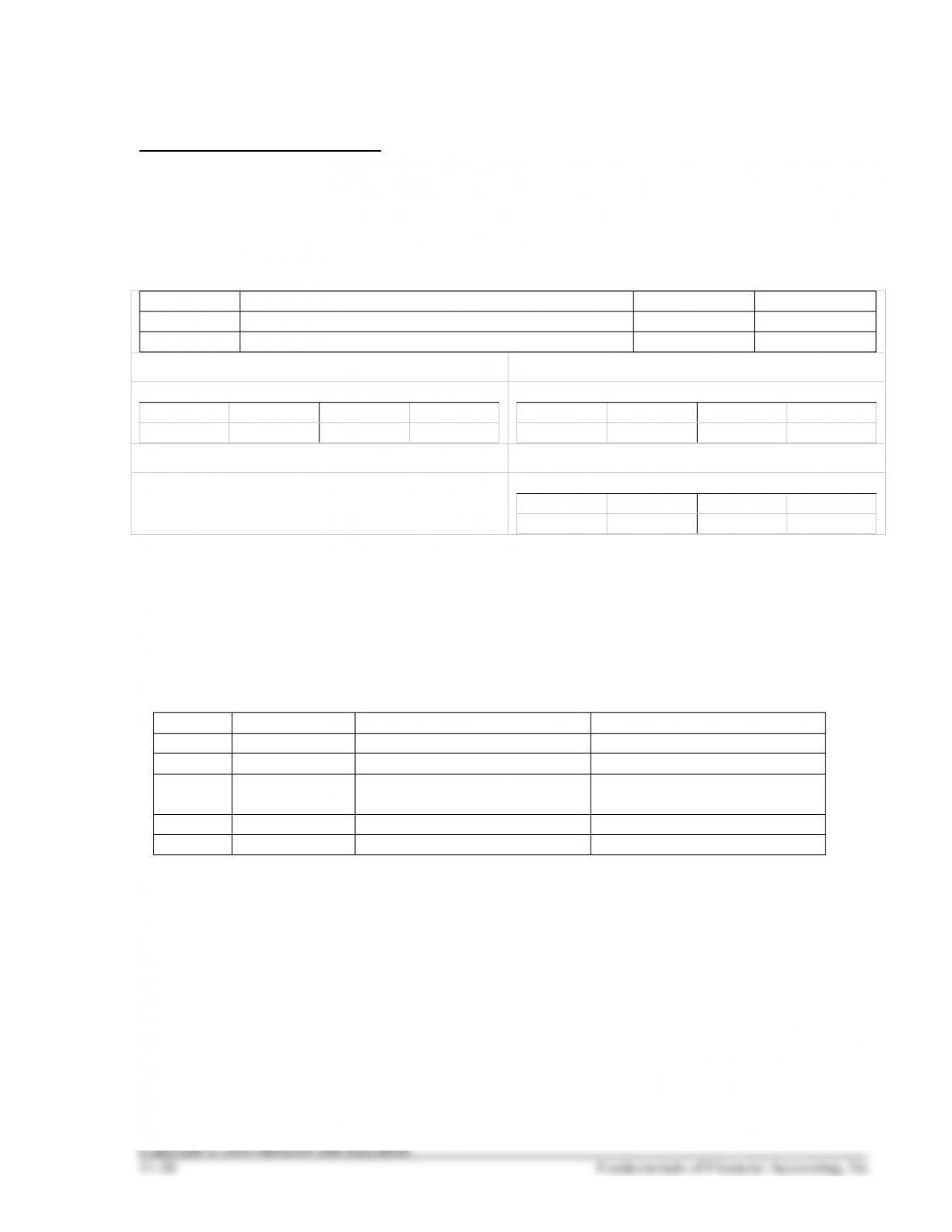

HANDOUT 11–1 SOLUTION, CONTINUED

On December 30, Strait Corp. sold 500 of the treasury shares for $15 each.

Dec. 30

Cash (500 × $15)

7,500

Additional Paid-in Capital (500 × [$16 – $15])

500

Treasury Stock (500 × $16)

8,000

+ Cash (A) –

May 1

250,000

16,000

Dec. 1

Dec. 15

15,000

+ Treasury Stock (xSE) –

Dec. 1

16,000

8,000

Dec. 15

8,000

Dec. 30

Balance

0

– Additional Paid-in Capital (SE) +

240,000

May 1

7,000

Dec. 15

Dec. 30

500

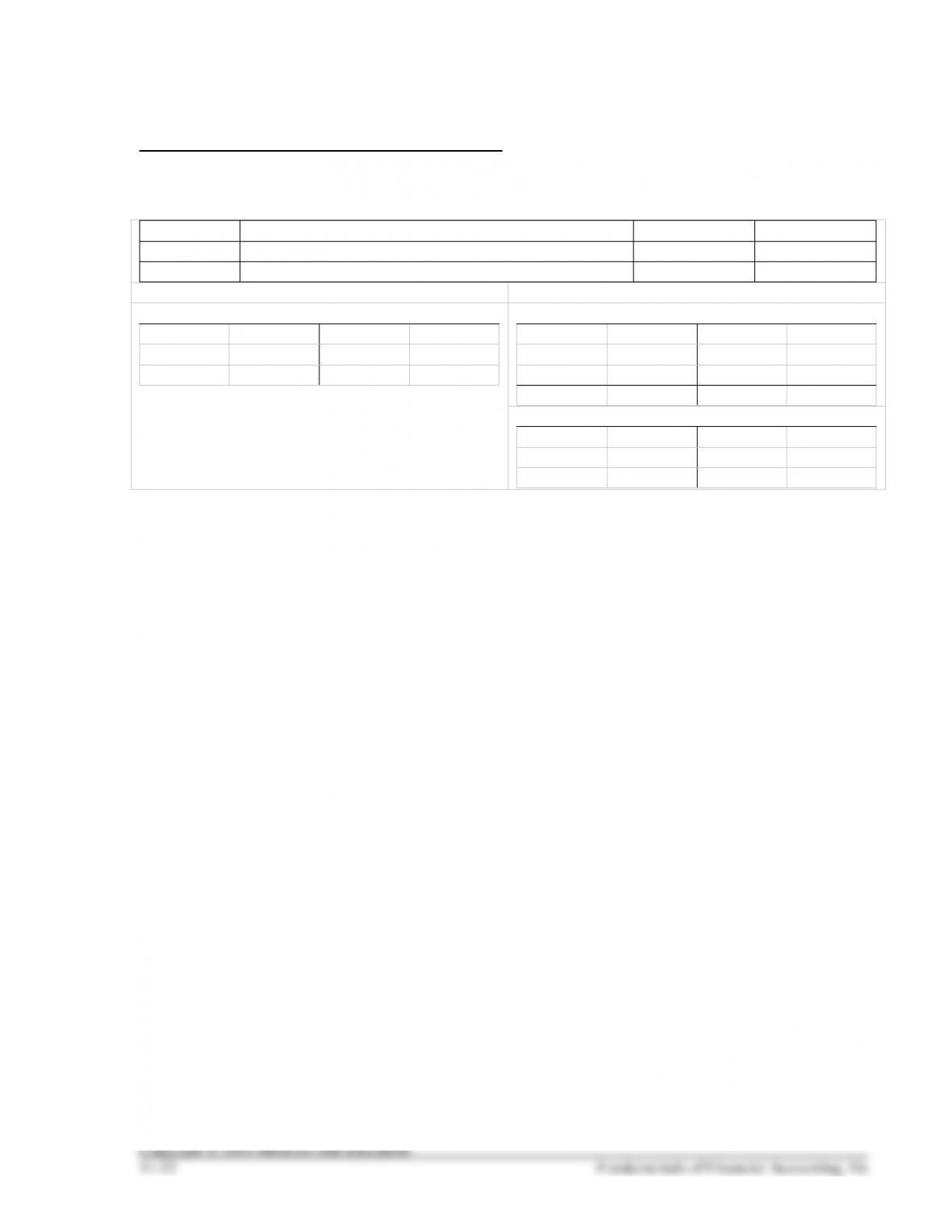

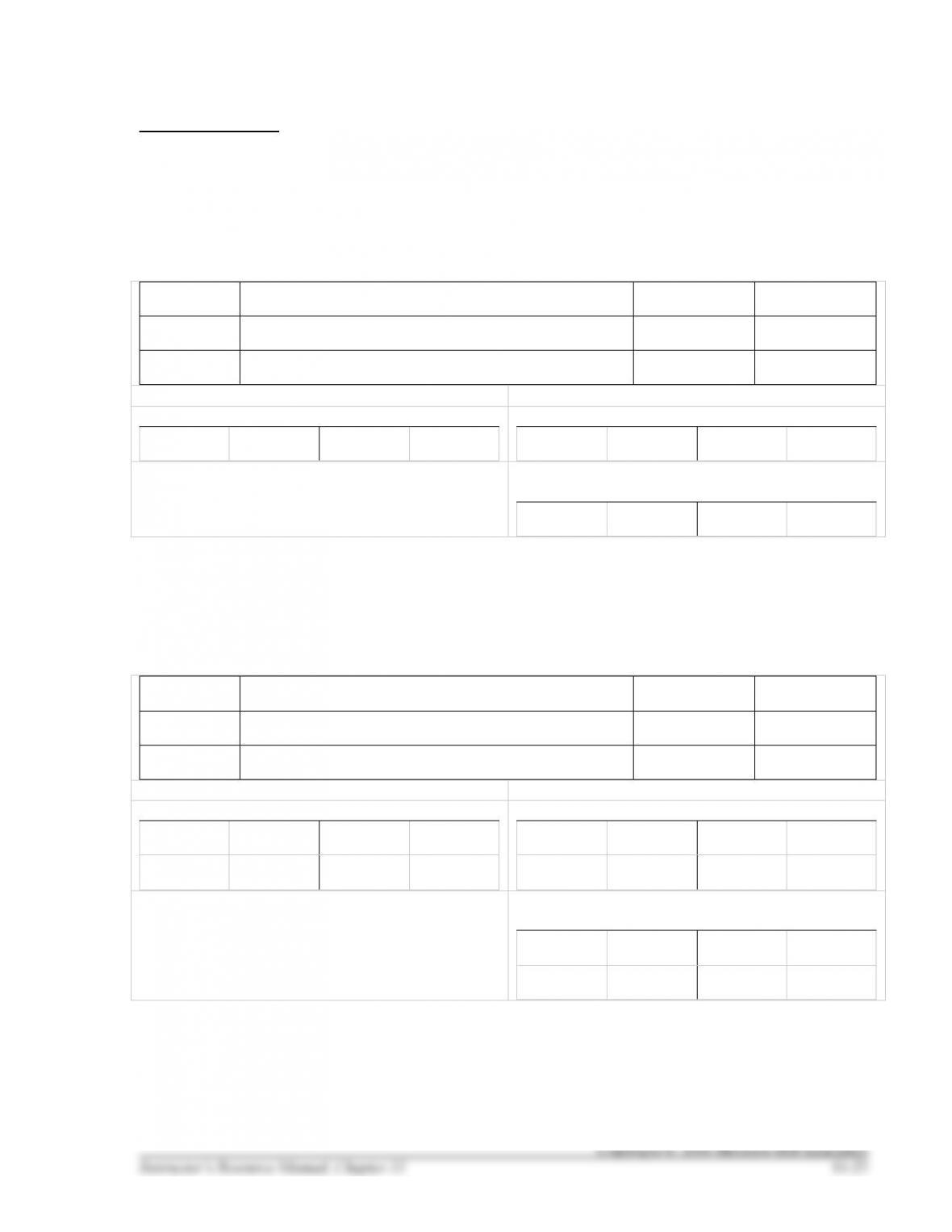

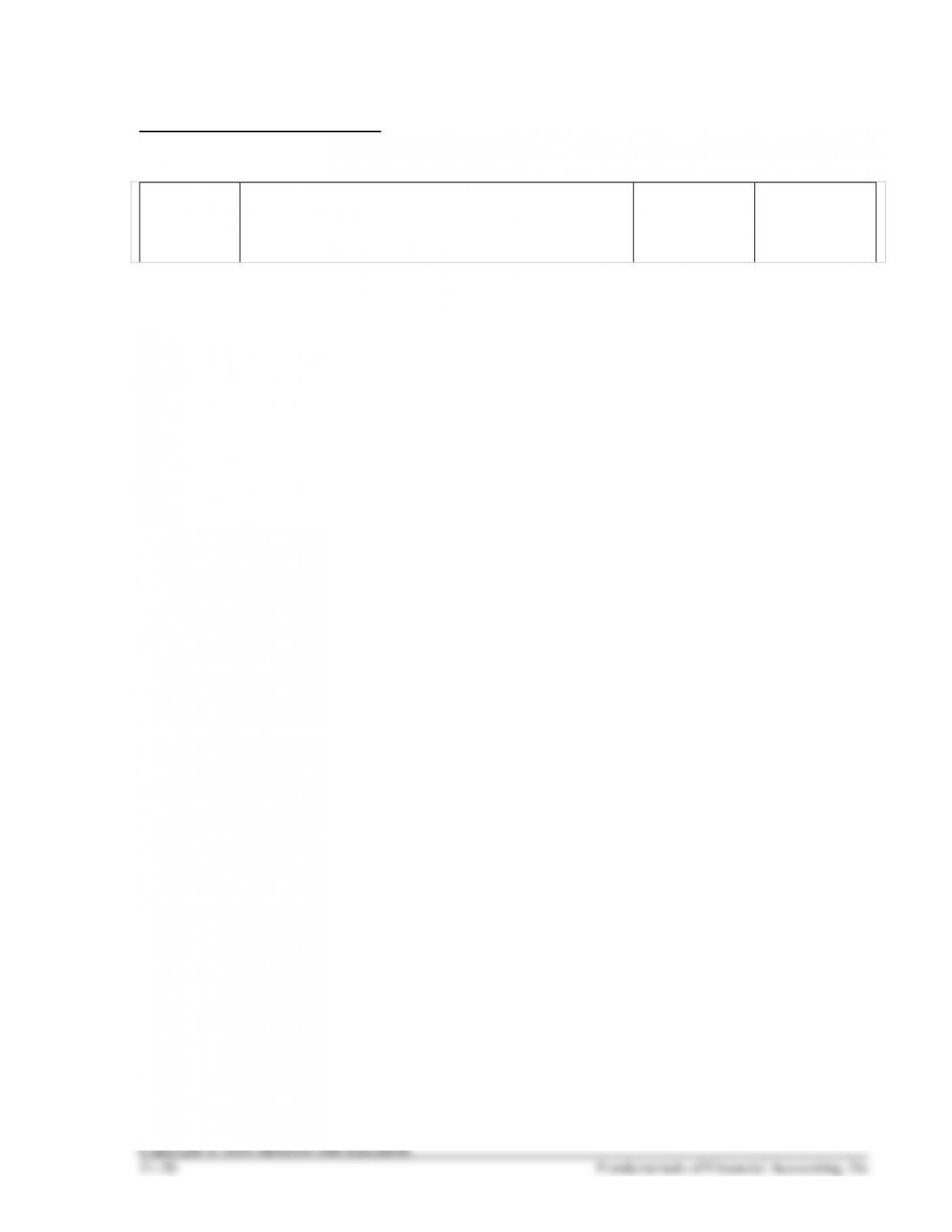

HANDOUT 11–2

CASH DIVIDENDS

Jones Corp. has 200,000 shares of stock authorized, 120,000 shares issued, and 100,000 shares

outstanding. On August 1, Jones’ Board of Directors declared a cash dividend of $0.50 per share, with a

record date of September 1. The dividend will be paid on October 1.

Prepare the journal entries required to record the transactions described above, as needed, and then post

them to the related T-accounts:

Aug. 1

Sept. 1

Oct. 1

HANDOUT 11–2 SOLUTION

CASH DIVIDENDS

Jones Corp. has 200,000 shares of stock authorized, 120,000 shares issued, and 100,000 shares

outstanding. On August 1, Jones’ Board of Directors declared a cash dividend of $0.50 per share, with a

record date of September 1. The dividend will be paid on October 1.

Prepare the journal entries required to record the transactions described above, as needed, and then post

them to the related T-accounts:

Aug. 1

Dividends (100,000 × $0.50)

50,000

Dividends Payable

50,000

+ Dividends (D) –

Aug 1

50,000

– Dividends Payable (L) +

50,000

May 1

Sept. 1

No Entry

Oct. 1

Dividends Payable

50,000

Cash

50,000

+ Cash (A) –

Oct. 1

50,000

– Dividends Payable (L) +

50,000

May 1

Oct. 1

50,000

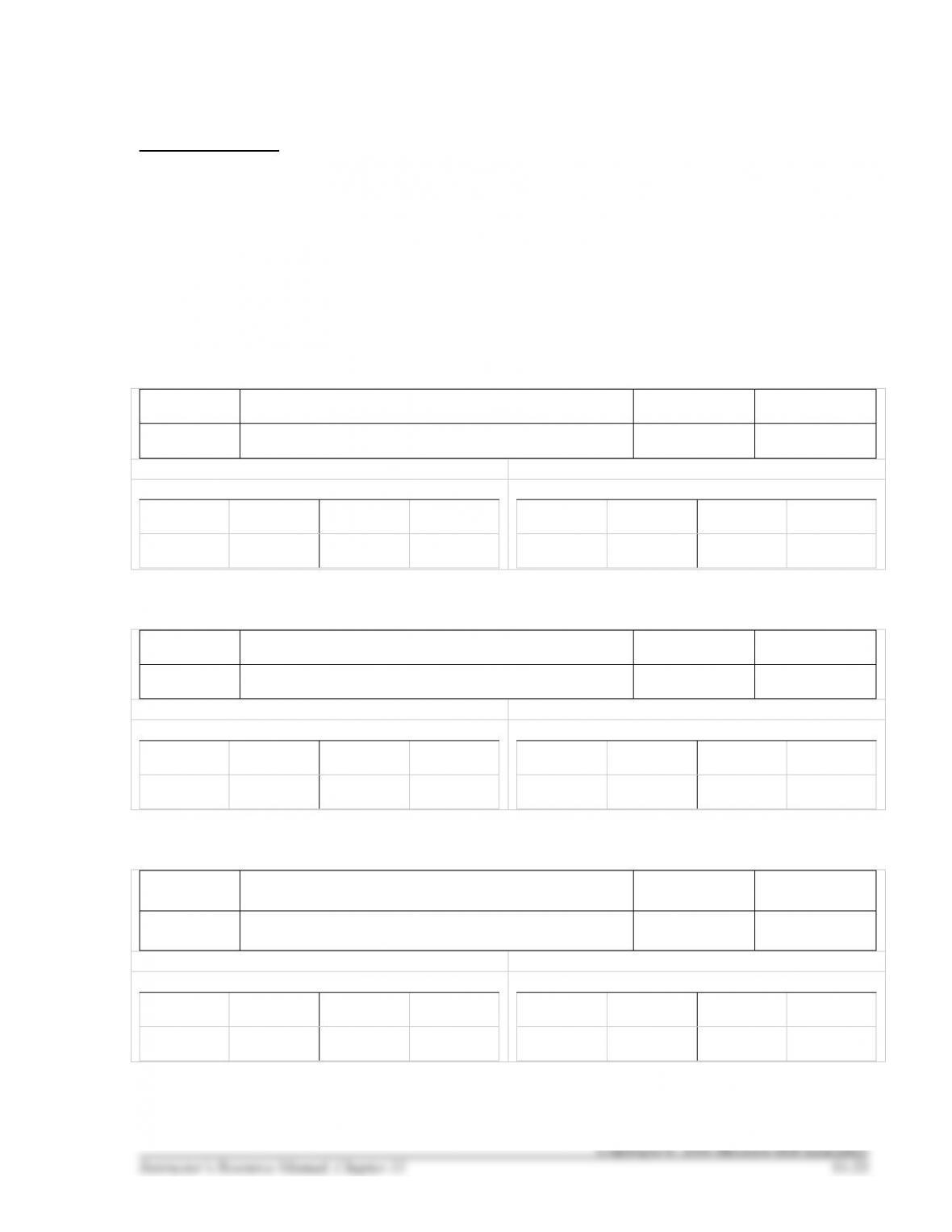

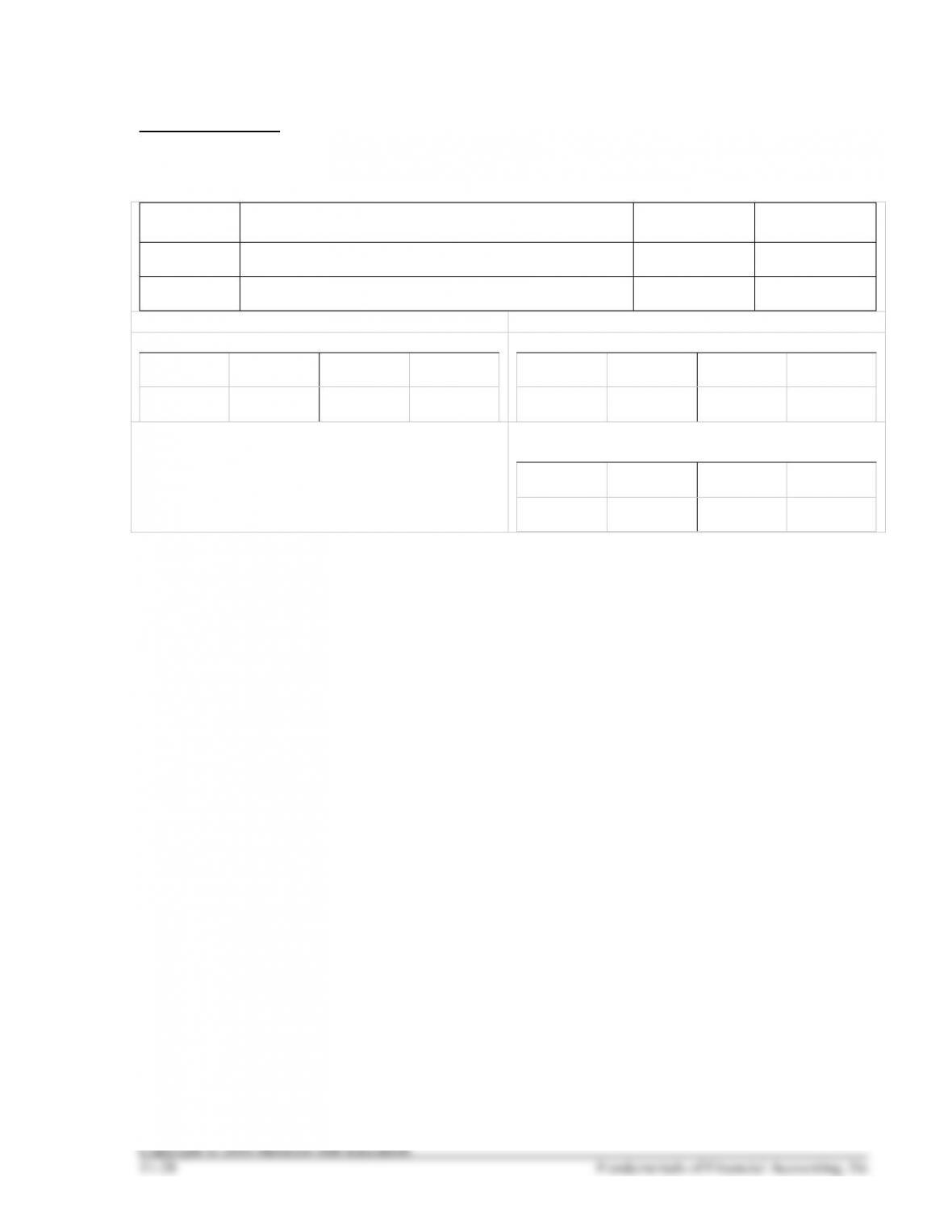

HANDOUT 11–3

PREFERRED DIVIDENDS

On January 1, Garden State issued 10,000 shares of $10 par preferred stock for $19 per share. Prepare the

journal entry required to record this transaction and post it to the appropriate T-accounts:

Jan. 1

The stock pays a cumulative annual dividend of 7% of par value. What is the total amount of the annual

dividends that would be paid, if declared, to preferred stockholders?

Complete the following table to explain how dividends would be allocated between preferred and

common stockholders:

Year

Total Dividend

To Preferred Stockholders

To Common Stockholders

Current

$100,000

Year 2

5,000

Year 3

10,000

Year 4

None

Year 5

20,000

HANDOUT 11–3 SOLUTION

PREFERRED DIVIDENDS

On January 1, Garden State issued 10,000 shares of $10 par preferred stock for $19 per share. Prepare the

journal entry required to record this transaction and post it to the appropriate T-accounts:

Jan. 1

Cash (10,000 × $20)

190,000

Preferred Stock (10,000 × $10 )

100,000

Additional Paid-in Capital

90,000

+ Cash (A) –

Jan. 1

190,000

– Preferred Stock (SE) +

100,000

Jan. 1

– Additional Paid-In Capital (SE) +

90,000

Jan. 1

The stock pays a cumulative annual dividend of 7% of par value. What is the total amount of the annual

dividends that would be paid, if declared, to preferred stockholders?

Par value of $100,000 × 7% = $7,000 to preferred

Complete the following table to explain how dividends would be allocated between preferred and

common stockholders.

Year

Total Dividend

To Preferred Stockholders

To Common Stockholders

Current

$100,000

$ 7,000

$93,000

Year 2

5,000

5,000

0

Year 3

10,000

9,000

(2,000 in arrears + 7,000)

1,000

Year 4

None

0

0

Year 5

20,000

14,000

6,000

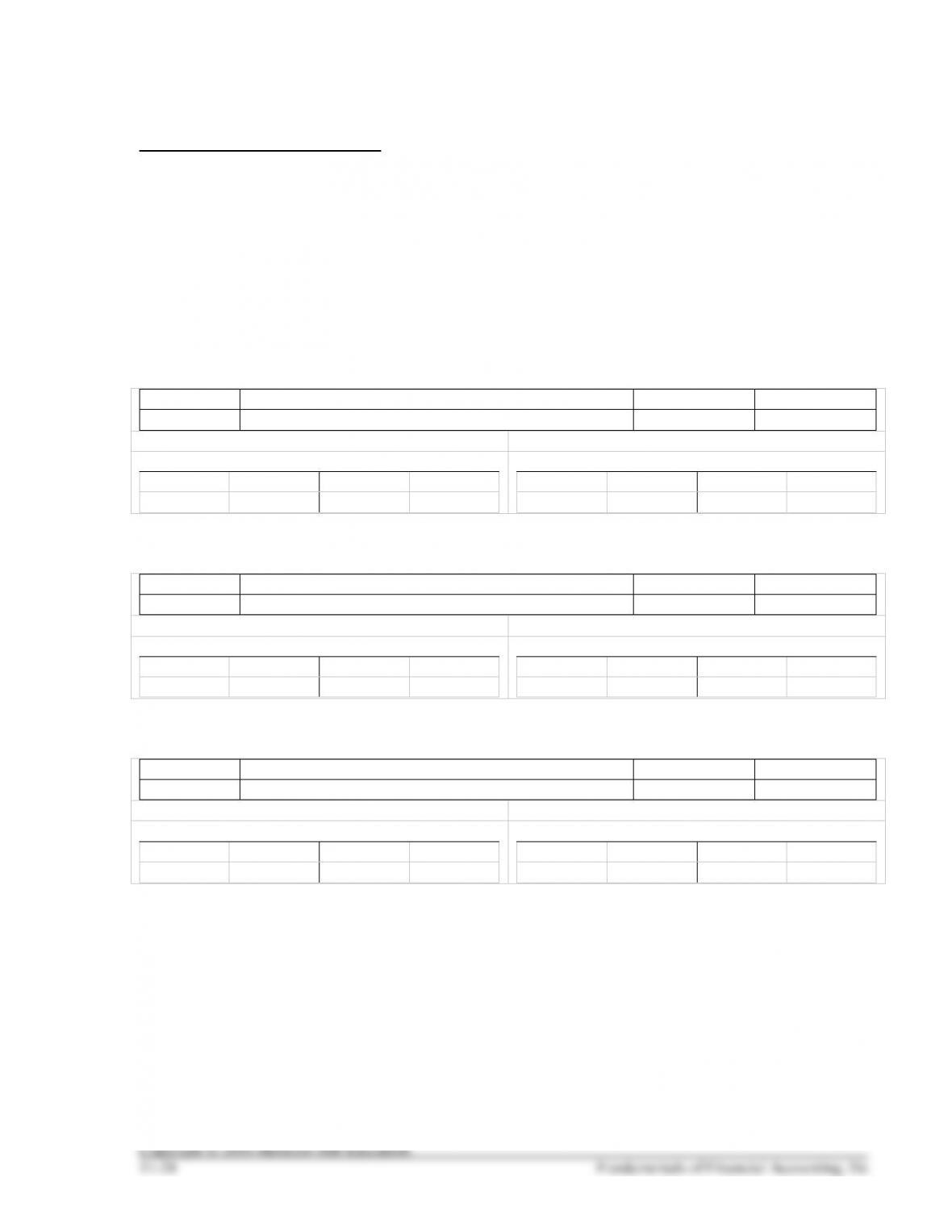

HANDOUT 11–4

STOCK DIVIDENDS AND STOCK SPLITS

Jennings Corp. has 1,000,000 shares of $1 par value stock authorized, 200,000 shares issued, and 150,000

shares outstanding. On March 31, Jones’ Board of Directors declared a 10% stock dividend at a time that

the stock carried a market value of $30. Prepare the journal entry required to record this transaction and

then post it to the related T-accounts:

March 31

Compute the number of shares outstanding after the March 31 stock dividend.

Jennings Corp. announced a 100% stock dividend on June 30. Prepare the journal entry required to record

this transaction and then post it to the related T-accounts:

June 30

Compute the number of shares outstanding after the June 30 stock dividend.

HANDOUT 11–4, continued

Jennings Corp. announced a 2 for 1 stock split on September 30. Prepare the journal entry required to

record the transaction described above and then post it to the related T-accounts:

September

30

Compute the number of shares outstanding after the September 30 stock split.

HANDOUT 11–4 SOLUTION

STOCK DIVIDENDS AND STOCK SPLITS

Jennings Corp. has 1,000,000 shares of $1 par value stock authorized, 200,000 shares issued, and 150,000

shares outstanding. On March 31, Jones’ Board of Directors declared a 10% stock dividend at a time that

the stock carried a market value of $30.

Prepare the journal entry required to record the transaction described above and then post it to the related

T-accounts:

March 31

Retained Earnings ($30 × 150,000 × 10%)

4,500,000

Common Stock ($1 × 150,000 × 10%)

15,000

Additional Paid-in Capital

4,485,000

– Retained Earnings (SE) +

March 31

4,500,000

– Common Stock (SE) +

15,000

March 31

– Additional Paid-In Capital (SE) +

4,485,000

March 31

Compute the number of shares outstanding after the March 31 stock dividend.

150,000 + (150,000 × 10%) = 165,000 shares

Jennings Corp. announced a 100% stock dividend on June 30. .

Prepare the journal entry required to record the transaction described above and then post it to the related

T-accounts:

June 30

Retained Earnings ($1 × 165,000)

165,000

Common Stock

165,000

– Retained Earnings (SE) +

March 31

4,500,000

June 30

165,000

– Common Stock (SE) +

15,000

March 31

165,000

June 30

– Additional Paid-In Capital (SE) +

4,485,000

March 31

Compute the number of shares outstanding after the June 30 stock dividend.

165,000 old shares + 165,000 new shares = 330,000 shares

HANDOUT 11–4 SOLUTION, continued

Jennings Corp. announced a 2 for 1 stock split on September 30.

September

30

Memorandum entry only: A 2-for-1 stock split caused

the number of shares outstanding to increase from

330,000 shares to 660,000 shares and the par value to

decrease from $1.00 per share to $0.50 per share.

330,000 old shares + 330,000 new shares = 660,000 shares