© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB10–4

January 1, 2015—Financial statements:

Case A

Case B

Case C

At 100

At 98

At 102

a.

Bonds payable ………………………………….

$500,000

$500,000

$500,000

b.

Unamortized premium (discount) …………

(10,000

)

10,000

c.

Carrying value …………………………………..

$500,000

$ 490,000

$510,000

Note: The bonds in Case B were issued at 98, implying an issue price of $490,000 ( =

98% x $500,000). The bonds in Case C were issued at 102, implying an issue

price of $510,000 ( = 102% x $500,000). When the bond issue price is greater

(less) than the face value, the bonds have issued at a premium (discount).

PB10–5

Req. 1

Cash …………………………….. ……………..……………

53,000,000

Bonds Payable …………… ……………..……………

53,000,000

Bonds Payable ……………… ……………..……………

50,000,000

Loss on Bond Retirement … ………….

3,000,000

Cash ………………………… ……………..……………

53,000,000

PB10–6

Req. 1

Changes During the Period

Ending Bond Liability Balances

Period

Ended

(A)

Cash

Paid

(B)

Premium

Amortized

(C) (=A–B)

Interest

Expense

(D)

Bonds

Payable

(E)

Premium on

Bonds Payable

(F) (=D+E)

Carrying Value

01/01/15

–

–

–

100,000

2,070

102,070

12/31/15

5,000

690*

4,310

100,000

1,380

101,380

12/31/16

5,000

690

4,310

100,000

690

100,690

12/31/17

5,000

690

4,310

100,000

0

100,000

* Straight-line amortization of discount = $2,070 ÷ 3 periods = $690 per year.

Req. 2

January 1, 2015:

Cash ……………………………………………………….………………..

102,070

Bonds Payable ………………………………………………………

100,000

Premium on Bonds Payable …………………………………….

2,070

Req. 3

December 31, 2015:

Interest Expense ………………………………………………………..

4,310

Premium on Bonds Payable …………………………..…………….

690

Cash …………………………………………………………………….

5,000

December 31, 2016:

Interest Expense ………………………………………………………..

4,310

Premium on Bonds Payable …………………………..…………….

690

Cash …………………………………………………………………….

5,000

Interest Expense ………………………………………………………..

4,310

Bonds Payable …………………………………………………………..

100,000

Premium on Bonds Payable …………………………..…………….

690

Cash …………………………………………………………………….

105,000

Req. 5

January 1, 2017:

Bonds Payable …………………………………………………………..

100,000

Premium on Bonds Payable …………………………..…………….

690

Loss on Bond Retirement …………………………………………….

1,310

Cash ($100,000 x 102%) …………………………..……………..

102,000

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

PB10–7

Req. 1

Changes During the Period

Ending Bond Liability Balances

Period

Ended

(A)

Interest

Expense

(B)

Cash

Paid

(C) (=B–A)

Premium

Amortized

(D)

Bonds

Payable

(E)

Premium on

Bonds Payable

(F) (=D+E)

Carrying Value

01/01/15

–

–

–

100,000

2,070

102,070

12/31/15

4,338

5,000

662

100,000

1,408

101,408

12/31/16

4,310

5,000

690

100,000

718

100,718

12/31/17

4,282*

5,000

718

100,000

0

100,000

* Interest in 2017 calculates as $100,718 x .0425 = $4,281. To accommodate rounding, we

show one dollar more, which brings the Premium on Bonds Payable to zero.

Req. 2

January 1, 2015:

Cash ……………………………………………………….………………..

102,070

Bonds Payable ………………………………………………………

100,000

Premium on Bonds Payable …………………………………….

2,070

Req. 3

December 31, 2015:

Interest Expense ………………………………………………………..

4,338

Premium on Bonds Payable …………………………………………

662

Cash …………………………………………………………………….

5,000

December 31, 2016:

Interest Expense ………………………………………………………..

4,310

Premium on Bonds Payable …………………………..…………….

690

Cash …………………………………………………………………….

5,000

Interest Expense ………………………………………………………..

4,282

Bonds Payable ……………………………………………………. ……

100,000

Premium on Bonds Payable …………………………………………

718

Cash ……………………………………………………………… ……

105,000

Req. 5

January 1, 2017:

Bonds Payable ……………………………………………………. ……

100,000

Premium on Bonds Payable …………………………..…………….

718

Loss on Bond Retirement ……………………………………… ……

282

Cash ($100,000 x 101%) …………………………..………. ……

101,000

PB10–8

Req. 1

Beginning of

Year

Changes During the Period

End of Year

Period

(A)

Bonds

Payable, Net

(B)

Interest

Expense

(C)

Cash

Paid

(D) (=C–B)

Reduction in Bonds

Payable, Net

(E) (=A–D)

Bonds Payable,

Net

01/01/15-12/31/15

102,070

4,338

5,000

662

101,408

01/01/16-12/31/16

101,408

4,310

5,000

690

100,718

01/01/17-12/31/17

100,718

4,282*

5,000

718

100,000

* Interest in 2017 calculates as $100,718 x .0425 = $4,281. To accommodate rounding, we

show one dollar more, which brings the Premium on Bonds Payable to zero.

Req. 2

January 1, 2015:

Cash ……………………………………………………….………………..

102,070

Bonds Payable, Net ………………………………………………..

102,070

Req. 3

December 31, 2015:

Interest Expense ………………………………………………………..

4,338

Bonds Payable, Net …………………………..……………………….

662

Cash …………………………………………………………………….

5,000

December 31, 2016:

Interest Expense ………………………………………………………..

4,310

Bonds Payable, Net …………………………..……………………….

690

Cash …………………………………………………………………….

5,000

Interest Expense ………………………………………………………..

4,282

Bonds Payable, Net …………………………..……………………….

100,718

Cash ……………………………………………………………… ……

105,000

Req. 5

January 1, 2017:

Bonds Payable, Net …………………………..………………… ……

100,718

Loss on Bond Retirement ……………………………………… ……

282

Cash ($100,000 x 101%) …………………………………… ……

101,000

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

C10–1

Req. 1

Interest Expense = Principal x Interest Rate x Time

= $1,800,000 x 6% x 12/12

= $108,000

Req. 2

Total cost of vehicles = $2,000,000 purchase price + ($2,000,000 x 11% sales tax)

= $2,220,000

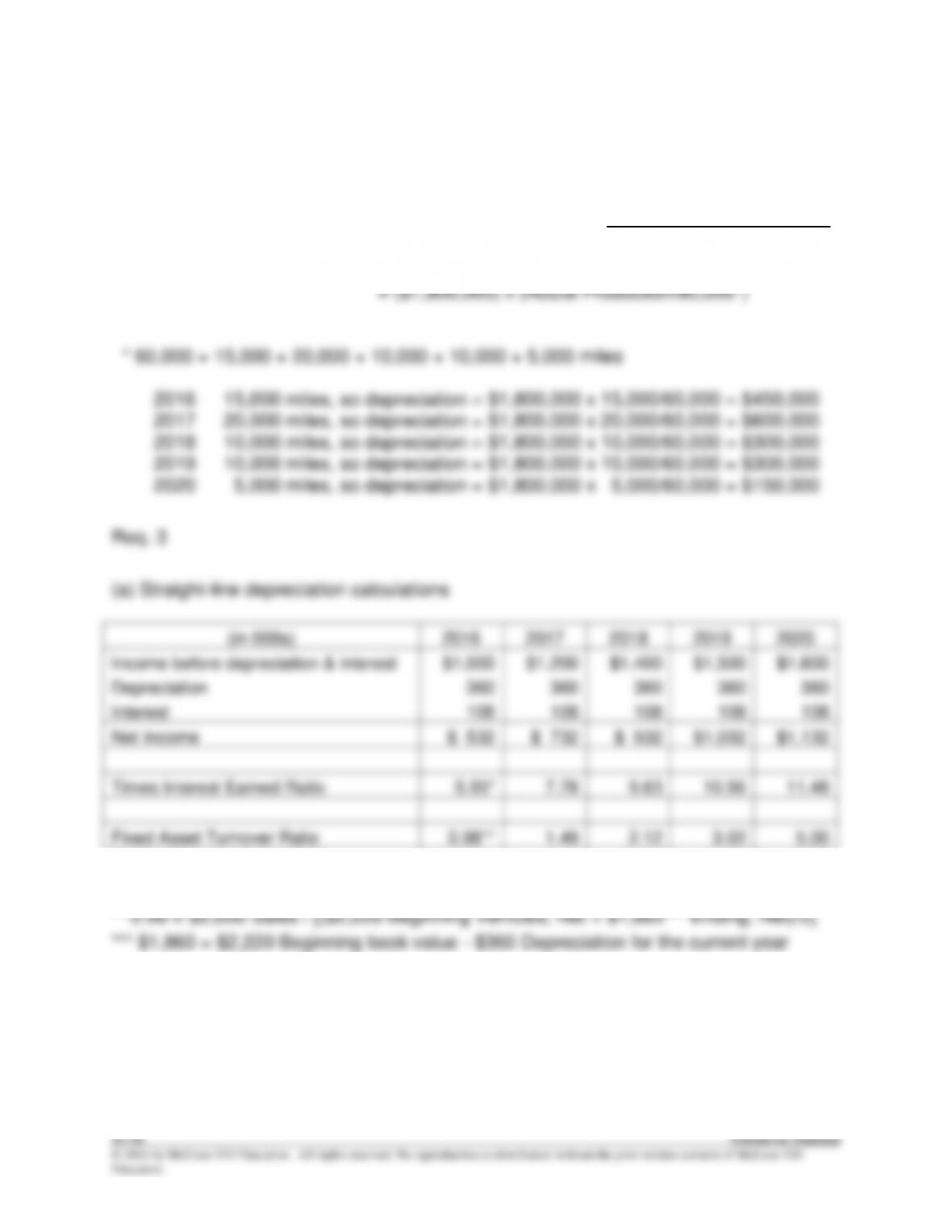

C10–1 (continued)

Req. 2 (continued)

c) Units-of-production = (Cost – Residual Value) x Actual Production

Estimated Total Production

= ($2,220,000 – 420,000) x (Actual Production/60,000*)

* 5.93 = ($532 Net Income + $108 Interest + $0 Income Tax) / $108 Interest

(in 000s)

2016

2017

2018

2019

2020

Income before depreciation & interest

$1,000

$1,200

$1,400

$1,500

$1,600

Depreciation

360

360

360

360

360

Interest

108

108

108

108

108

Net Income

$ 532

$ 732

$ 932

$1,032

$1,132

Times Interest Earned Ratio

5.93*

7.78

9.63

10.56

11.48

Fixed Asset Turnover Ratio

0.98**

1.49

2.12

3.02

5.00

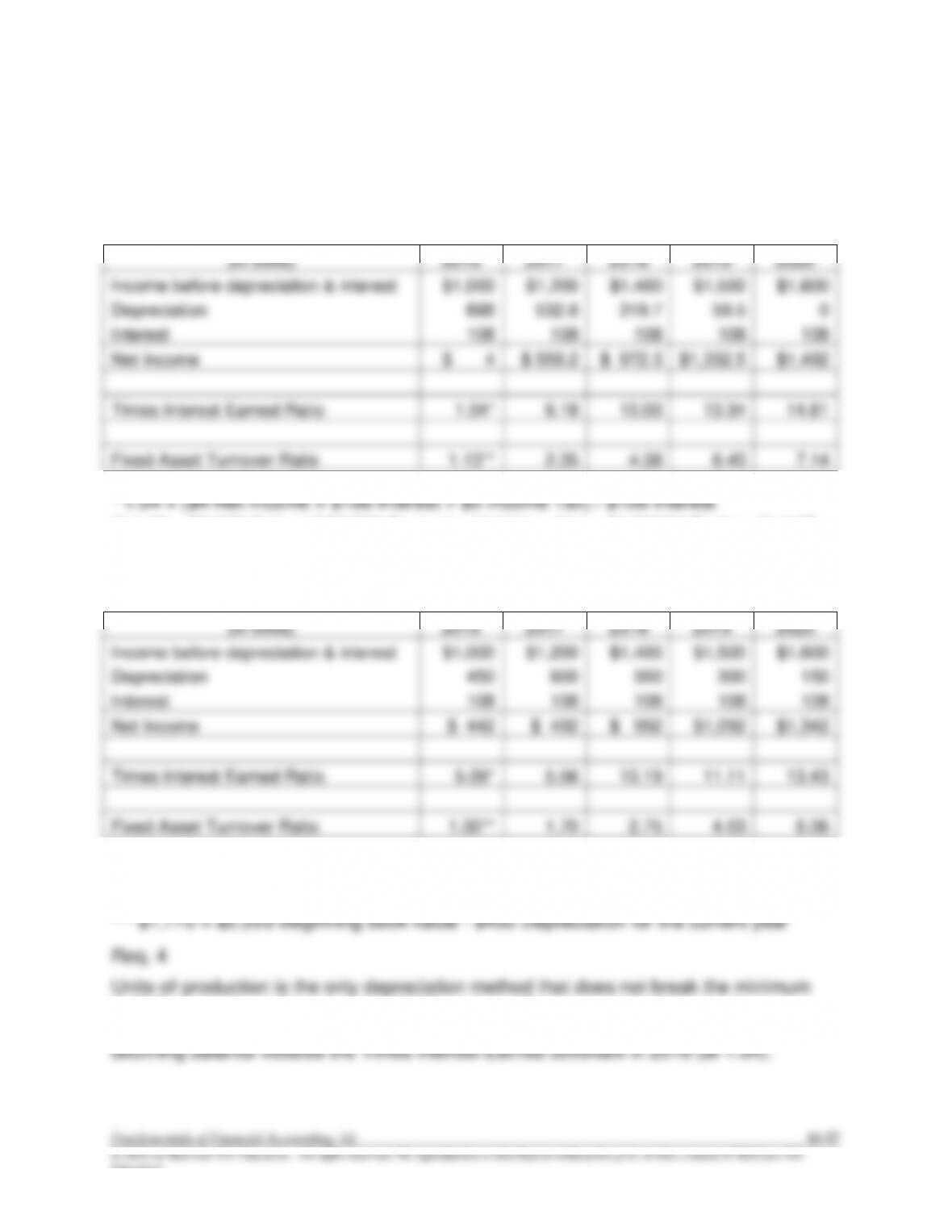

C10–1 (continued)

Req. 3 (continued)

(b) Double-declining depreciation calculations

** 1.13 = $2,000 Sales / [($2,220 Beginning Vehicles, Net + $1,332*** Ending, Net)/2]

*** $1,332 = $2,220 Beginning book value – $888 Depreciation for the current year

(c) Units-of–production depreciation calculations

* 5.09 = ($442 Net Income + $108 Interest + $0 Income Tax) / $108 Interest

** 1.00 = $2,000 Sales / [($2,220 Beginning Vehicles, Net + $1,770*** Ending, Net)/2]

3.00 Times Interest Earned and 1.00 Fixed Asset Turnover ratios. Straight-line

depreciation violates the Fixed Asset Turnover covenant in 2016 (at 0.98) and double-

(in 000s)

2016

2017

2018

2019

2020

Income before depreciation & interest

$1,000

$1,200

$1,400

$1,500

$1,600

Depreciation

888

532.8

319.7

59.5

0

Interest

108

108

108

108

108

Net Income

$ 4

$ 559.2

$ 972.3

$1,332.5

$1,492

Times Interest Earned Ratio

1.04*

6.18

10.00

13.34

14.81

Fixed Asset Turnover Ratio

1.13**

2.35

4.38

6.45

7.14

(in 000s)

2016

2017

2018

2019

2020

Income before depreciation & interest

$1,000

$1,200

$1,400

$1,500

$1,600

Depreciation

450

600

300

300

150

Interest

108

108

108

108

108

Net Income

$ 442

$ 492

$ 992

$1,092

$1,342

Times Interest Earned Ratio

5.09*

5.56

10.19

11.11

13.43

Fixed Asset Turnover Ratio

1.00**

1.70

2.75

4.03

6.06

10-58 Solutions Manual

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO SKILLS DEVELOPMENT CASES

S10–1

1. A

2. C

Calculations:

Req. 1

Debt-to–Assets

=

Total Liabilities

Total Assets

February 2,

2014

=

$27,996

=

0.691 or 69.1%

$40,518

February 3,

=

$23,307

=

0.567 or 56.7%

2013

$41,084

Req. 2

Times Interest Earned

Ratio

=

Net Income + Interest Expense + Income Tax Expense

Interest Expense

= $5,385 + $711 + $3,082

$711

= 12.91