© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10

1. Liabilities are created when a company buys goods and services on credit, obtains

2. Liabilities are obligations that result from transactions that require future payment of

assets or the future performance of services. A liability usually has a definite

1) The initial amount of the liability. A liability is initially recorded at its cash

2) Additional amounts owed to the creditor. Liabilities are increased whenever

additional obligations arise, including interest charges that arise as time

passes.

4. An accrued liability is an expense that was incurred before the end of the current

period but has not been paid or recorded. Therefore, an accrued liability is

recognized when such a transaction is recorded. A typical example is wages

5. Unearned revenue is revenue that has been collected in advance of being earned.

6. An employer collects payroll taxes from its employees on behalf of the government.

When an employer withholds payroll taxes from its employees’ pay, the employer

7. Payroll deductions will reduce the amount paid to each employee, but they will not

reduce the total amount paid by the employer (because the employer must forward

deductions to the appropriate organization or government agency on behalf of the

8. (a) This year, the loan would be classified as a long-term liability. Only unpaid

9. A bond will issue at a discount or premium depending on whether lenders are

attracted to the bond’s features (primarily the interest rate). If the bond’s stated

10. The stated interest rate is the rate specified on the bond certificate, whereas the

11. (a) When a bond is issued at face value, the stated interest rate and the market

12. The carrying value of a bond payable is the bond liability on the issuer’s accounting

records owed at a specific date, after taking into account any unamortized bond

discount or premium. A bond issued at face value will have a carrying value equal

Interest Expense

=

Bonds Payable, Net

x

Interest Rate

x

Time

This same approach is used for bonds issued at either a discount or premium.

Education.

Authors’ Recommended Solution Time

(Time in minutes)

Mini-exercises

Exercises

Problems

Skills

Development

Cases*

Continuing Case

No.

Time

No.

Time

No.

Time

No.

Time

No.

Time

1

5

1

20

CP10-1

40

1

10

1

10

2

3

2

20

CP10-2

30

2

15

2

5

3

3

3

20

CP10-3

35

3

25

4

5

4

15

CP10-4

25

4

25

5

4

5

20

CP10-5

10

5

25

6

5

6

20

CP10-6

20

6

20

7

5

7

20

CP10-7

20

7

20

8

3

8

20

CP10-8

20

8

20

9

3

9

20

CP10-9

20

9

20

10

3

10

15

CP10–10

20

11

5

11

15

PA10-1

40

12

6

12

15

PA10-2

30

13

5

13

15

PA10-3

35

14

4

14

25

PA10-4

25

15

5

15

25

PA10-5

10

16

5

16

25

PA10-6

20

17

5

PA10-7

20

PA10-8

20

PB10-1

40

PB10-2

30

PB10-3

35

PB10-4

25

PB10-5

15

PB10-6

20

PB10-7

20

PB10-8

20

C10-1

25

* Due to the nature of cases, it is very difficult to estimate the amount of time students

will need to complete them. As with any open-ended project, it is possible for students

Case

Financial

Analysis

Research

Ethical

Reasoning

Critical

Thinking

Technology

Writing

Teamwork

1

X

2

X

3

X

x

x

x

x

4

x

x

5

x

x

6

X

x

x

7

x

8

x

9

x

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO MINI-EXERCISES

M10–1

Assets

Liabilities

Stockholders’ Equity

(a)

Cash + 375,000

Unearned Revenue + 375,000

(b)

Unearned Revenue – 37,500

Service

Revenue (+R) +37,500

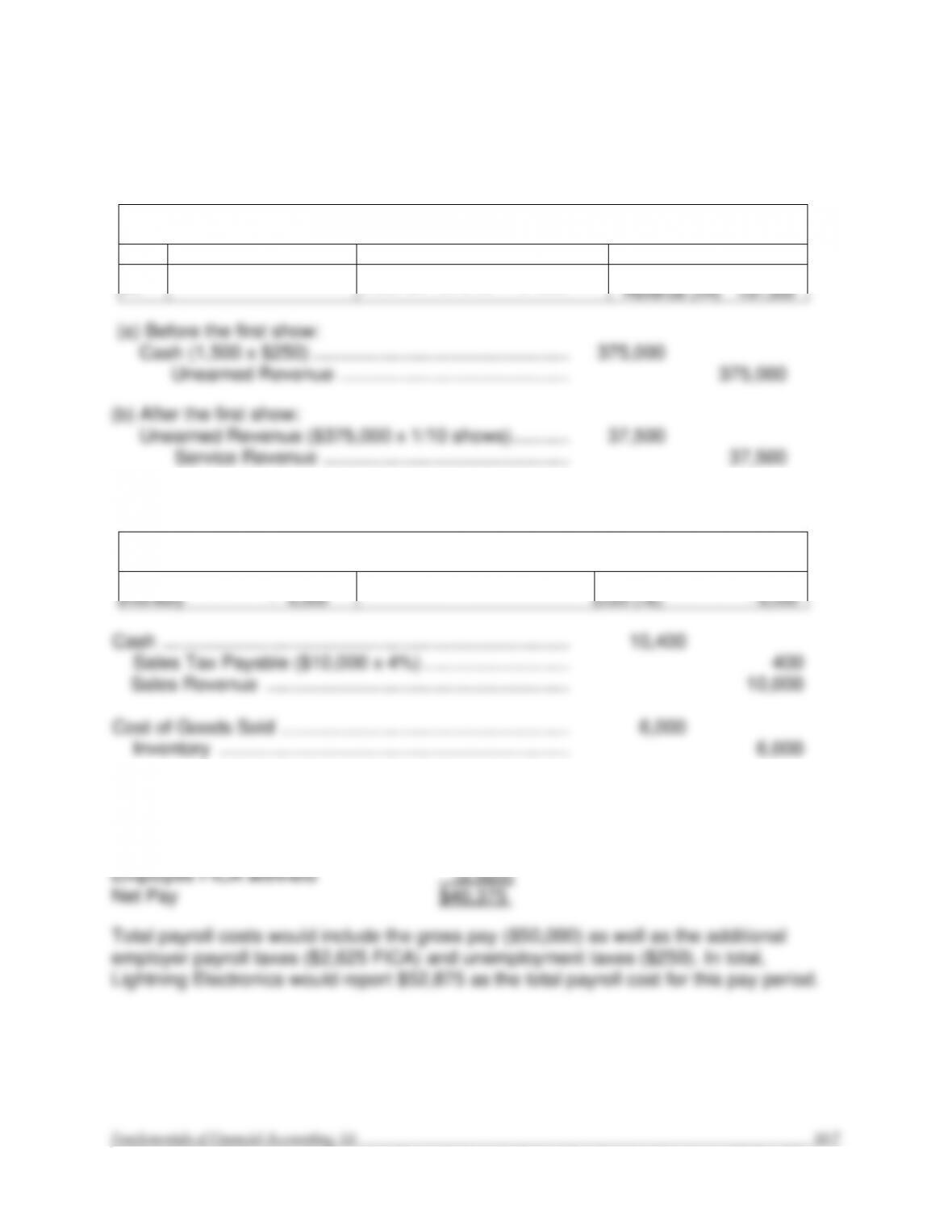

(a) Before the first show:

Cash (1,500 x $250) ………………………………………….

375,000

Unearned Revenue ……………………………………..

375,000

(b) After the first show:

Unearned Revenue ($375,000 x 1/10 shows) ………..

37,500

Service Revenue ………………………………………..

37,500

M10–2

Assets

Liabilities

Stockholders’ Equity

Cash + 10,400

Inventory – 6,000

Sales Tax Payable + 400

Sales Revenue (+R) +10,000

CGS (+E) – 6,000

Cash ……………………………………………………………………

10,400

Sales Tax Payable ($10,000 x 4%) ……………………….

400

Sales Revenue ………………………………………………….

10,000

Cost of Goods Sold ……………………………………………….

6,000

Inventory ………………………………………………………….

6,000

M10–3

Gross salaries & wages $50,000

Employee income tax withheld (7,000)

=

+

=

+

M10–4

Salaries and Wages Expense …………………………………

50,000

Withheld Income Taxes Payable ………………………….

7,000

FICA Payable ……………………………………………………

2,625

Cash ………………………………………………………………..

40,375

Payroll Tax Expense …………………………..…………………

2,875

FICA Payable ……………………………………………………

2,625

Unemployment Taxes Payable …………………………….

250

M10–5

As of December 31

2016

2015

Current Liabilities:

Current Portion of Long-term Debt

$3,000

$ 2,000

Long-term Debt

10,000

13,000

Total Liabilities

$ 13,000

$ 15,000

M10–6

Assets

Liabilities

Stockholders’ Equity

(a)

Cash + 1,000,000

Note Payable (short) + 1,000,000

(b)

Interest Payable + 15,000

Interest

Expense (+E) -15,000

(a) November 1, 2015:

Cash ……………………………………………………………………

1,000,000

Note Payable (short-term) …………………………………..

1,000,000

(b) December 31, 2015:

Interest Expense ($1,000,000 x 9% x 2/12) ……………….

15,000

Interest Payable ………………………………………………..

15,000

M10–7

December 31, 2015

Current Liabilities:

=

+

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

M10–8

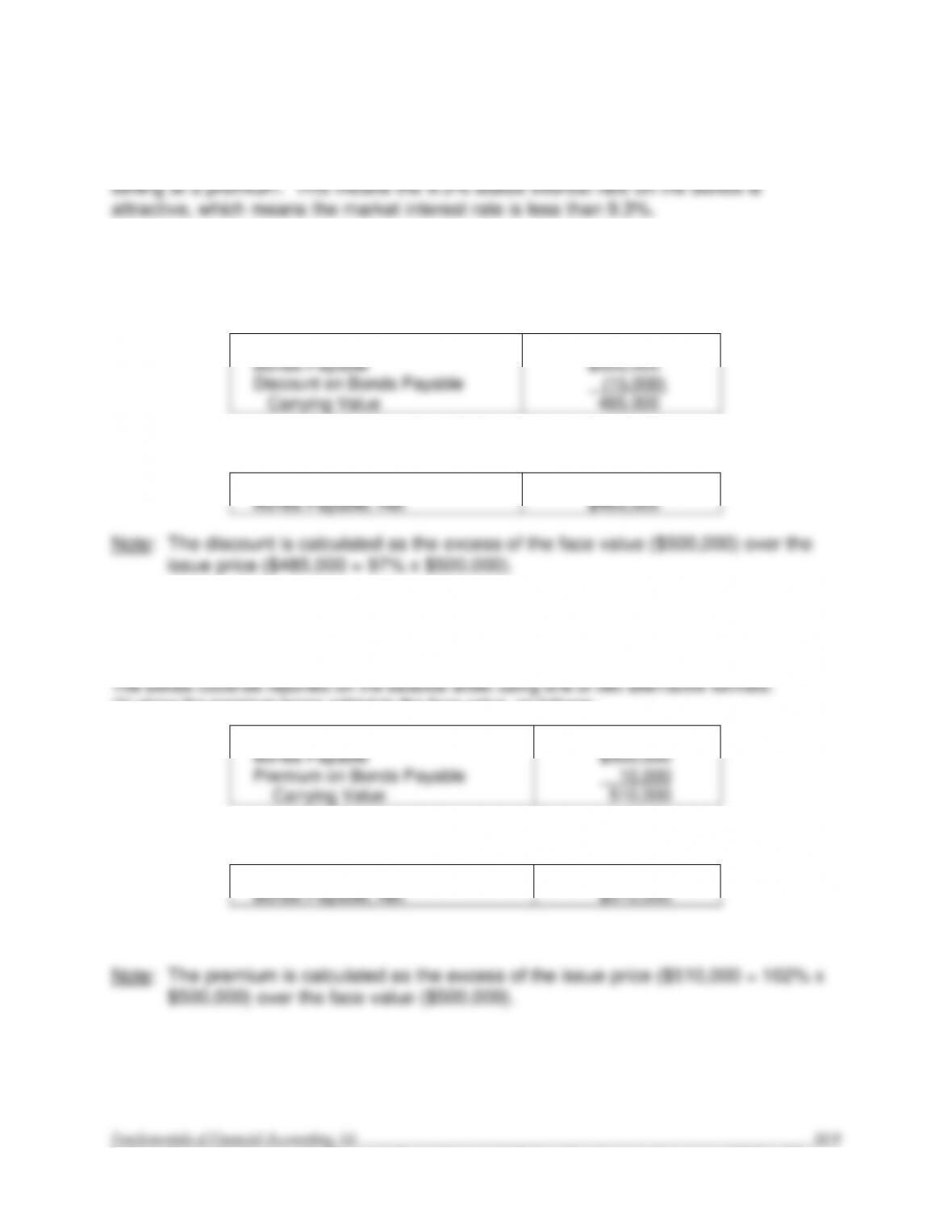

Because the bond quote price of 140.2 is greater than 100, we know the bonds are

M10–9

The bonds could be reported on the balance sheet using one of two alternative formats:

(1) show the discount being subtracted from the face value, as follows:

Long-term Liabilities

Bonds Payable

Discount on Bonds Payable

Carrying Value

$500,000

(15,000)

485,000

or (2) show only the net amount, as follows:

Long-term Liabilities

Bonds Payable, Net

$485,000

Note: The discount is calculated as the excess of the face value ($500,000) over the

issue price ($485,000 = 97% x $500,000).

M10–10

(1) show the premium being added to the face value, as follows:

Long-term Liabilities

Bonds Payable

Premium on Bonds Payable

Carrying Value

$500,000

10,000

510,000

or (2) show only the net amount, as follows:

Long-term Liabilities

Bonds Payable, Net

$510,000

Note: The premium is calculated as the excess of the issue price ($510,000 = 102% x

$500,000) over the face value ($500,000).

M10–11

Assets

Liabilities

Stockholders’ Equity

(a)

Cash + 2,500,000*

Bonds Payable + 2,500,000

(b)

Cash – 125,000

Interest

Expense (+E) -125,000

(a) January 1:

Cash ……………………………………………………………………

2,500,000*

Bonds Payable ………………………………………………….

2,500,000

(b) December 31:

Interest Expense ($2,500,000 x 5% x 12/12) ……………..

125,000

Cash ……………………………………………………….……….

125,000

* 25,000 bonds x $100 face value per bond

M10–12

2013 Buzz must disclose in a note that a potential liability exists because the

liability is possible.

2014 Buzz must disclose the liability in a note because the trial judgment makes

=

+