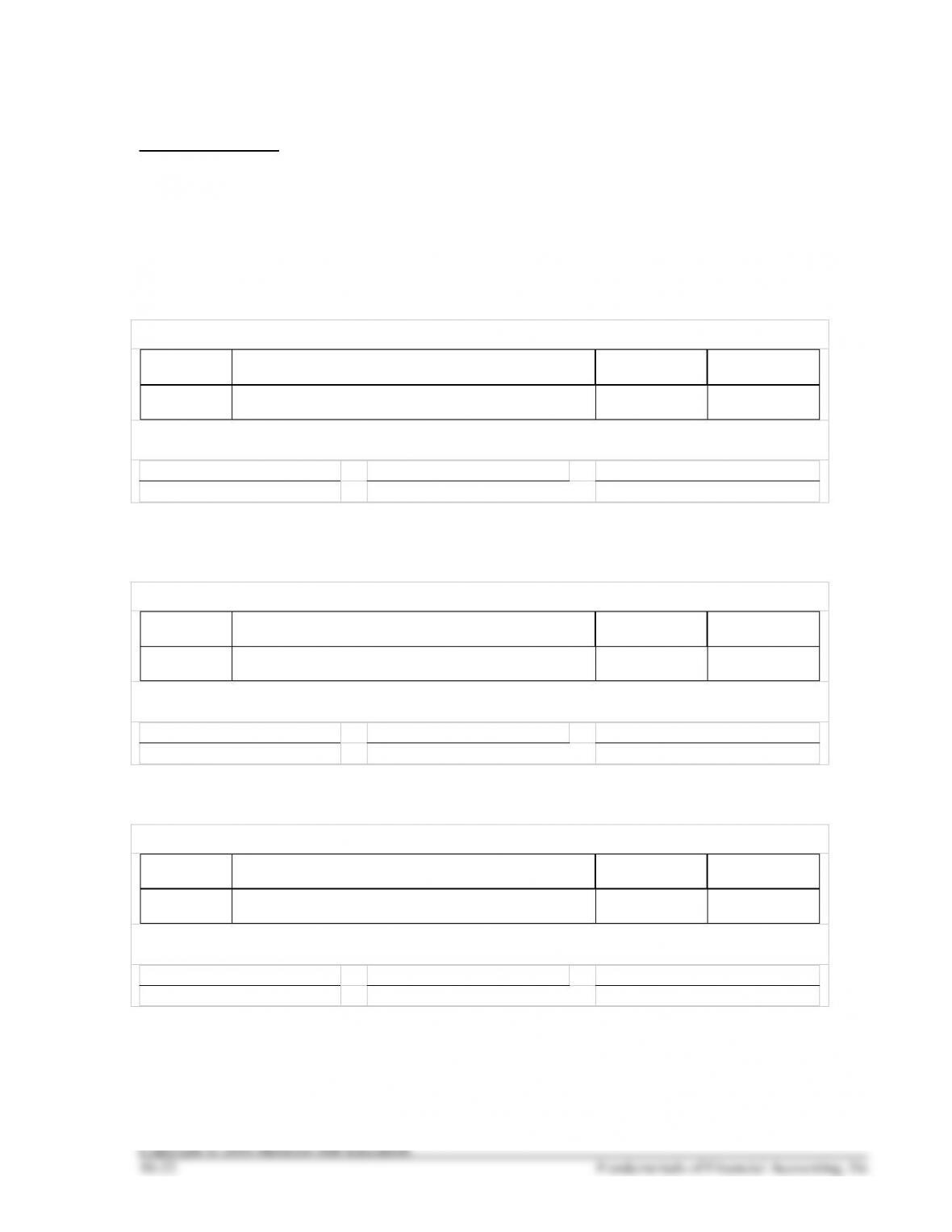

HANDOUT 10–1 SOLUTION

PAYROLL ENTRIES

J&W Buffet Co. employees earned $350,000 in the week ended December 17, 2016. Of this, $26,775 was

withheld from employees’ pay for FICA and $62,000 for income taxes. The net pay was directly

deposited into the employees’ bank accounts. The company must pay $1,200 for unemployment taxes.

Prepare the journal entry to record the employees’ portion of payroll for December 17, 2016.

Debit and credit the accounts affected

Dec. 17

Salaries and Wages Expense

350,000

2016

Withheld Income Taxes Payable

62,000

FICA Payable

26,775

Cash

261,225

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

–261,225

Withheld

Income

Taxes

Payable

+62,000

Salaries and

Wages

Expense

–350,000

FICA

Payable

+26,775

Prepare the journal entry to record the employer’s share of FICA payroll taxes for December 17, 2016.

Debit and credit the accounts affected

Dec. 17

Payroll Tax Expense

27.975

2016

FICA Payable

26,775

Unemployment Tax Payable

1,200

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

FICA

Payable

Unemployment

Tax Payable

+26,775

+1,200

Salaries and

Wages

Expense

–27,975

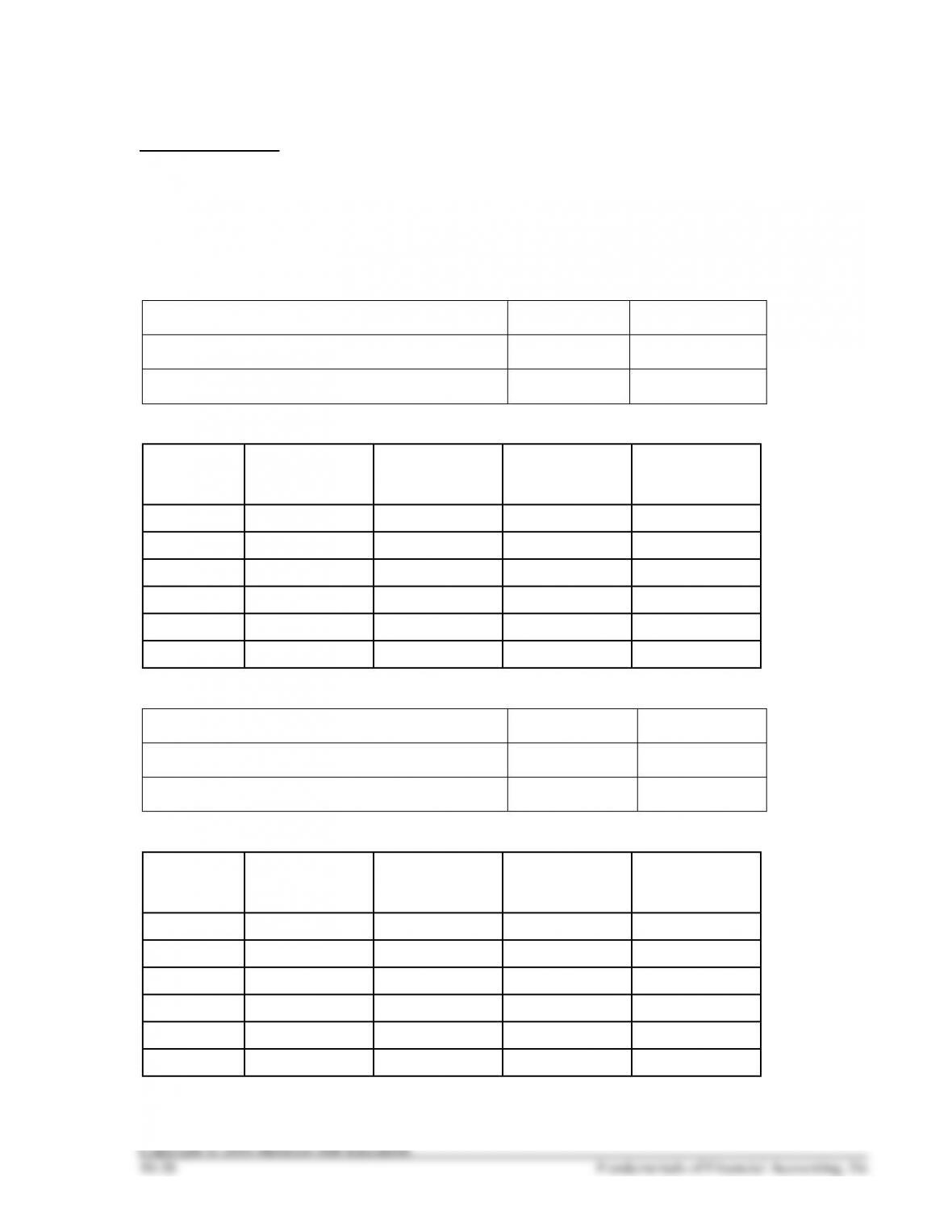

HANDOUT 10–2

NOTES PAYABLE

Mumford Co. borrowed a $100,000 note payable on June 1, 2016, with 6% interest. The note is due on

May 31, 2017.

Prepare the journal entry to record the issuance of the note and receipt of cash on June 1, 2016.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Prepare the adjusting journal entry to record the interest owed at the end of the accounting period on

December 31, 2016.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Prepare the journal entries to record the interest and principal payments to the lender on May 31, 2017.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

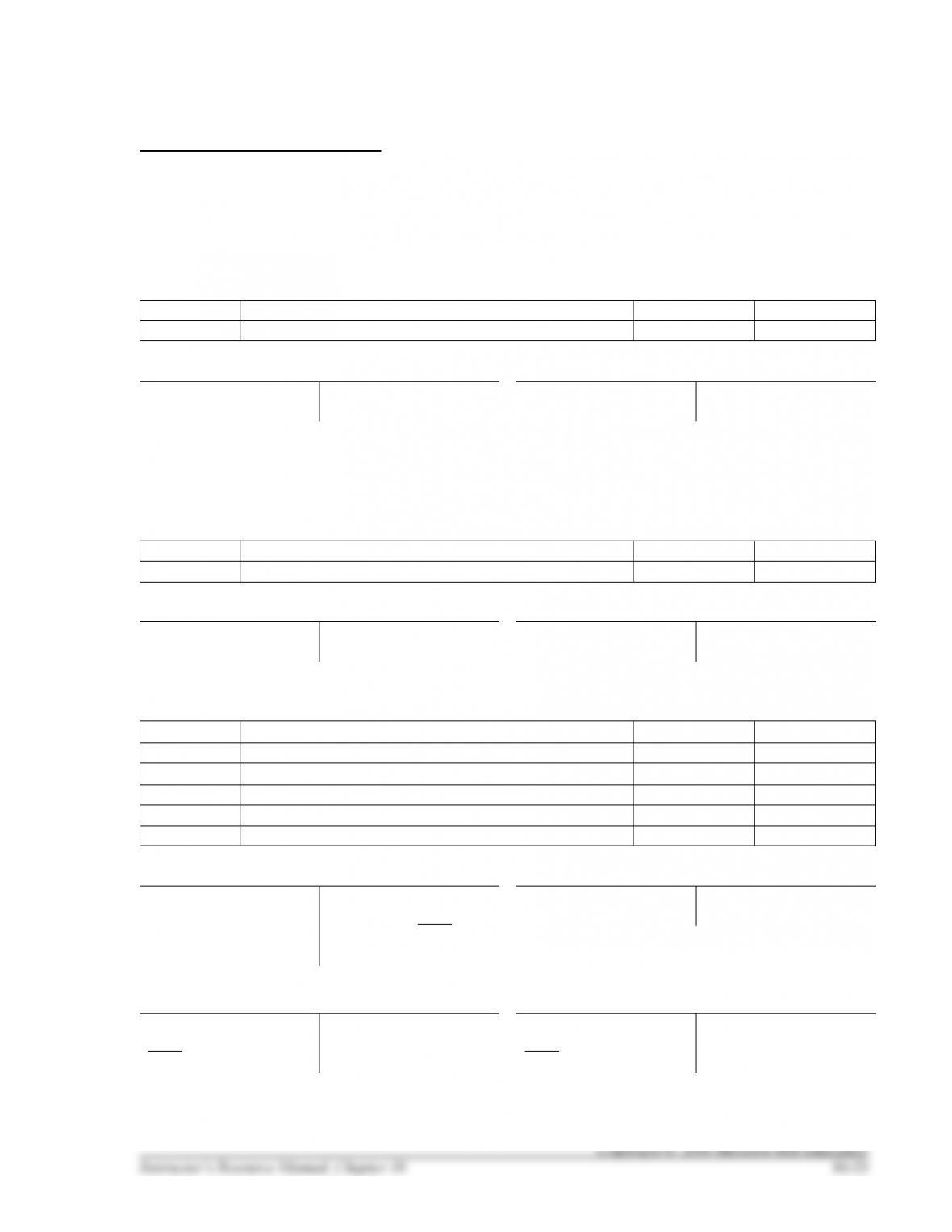

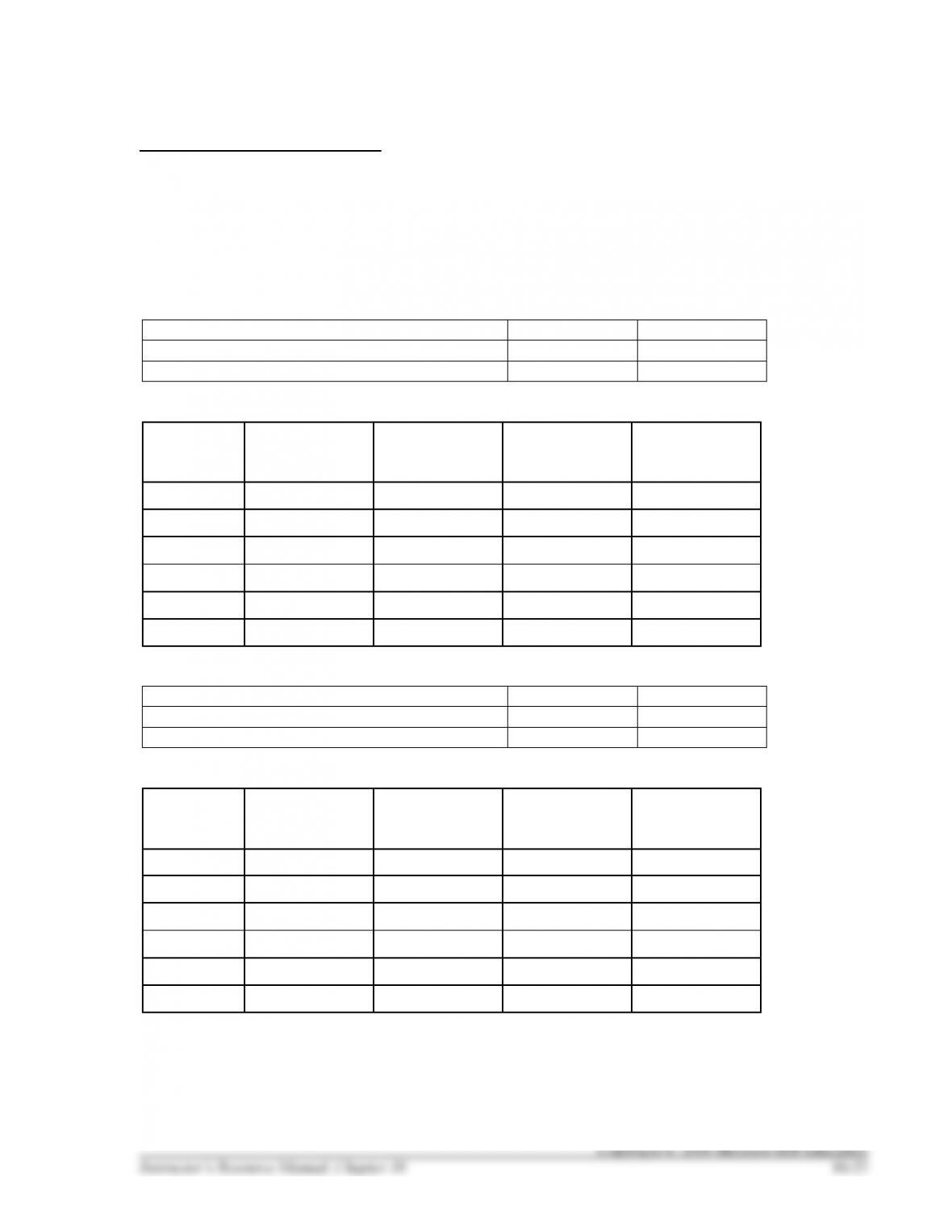

HANDOUT 10–2 SOLUTION

NOTES PAYBLE

Mumford Co. borrowed a $100,000 note payable on June 1, 2016, with 6% interest. The note is due on

May 31, 2011.

Prepare the journal entry to record the issuance of the note and receipt of cash on June 1, 2016.

June 1

Cash

100,000

2016

Note Payable

100,000

+ Cash (A) –

June 1

100,000

– Note Payable (L) +

100,000

June 1

Prepare the adjusting journal entry to record the interest owed at the end of the accounting period on

December 31, 2016.

Principal × Rate × Time Period = 100,000 × 6% × 7/12 = $3,500

Dec. 31

Interest Expense

3,500

2016

Interest Payable

3,500

– Interest Payable (L) +

3,500

Dec. 31

+ Interest Expense (E) –

Dec. 31

3,500

Prepare the journal entries to record the interest and principal payments to the lender on May 31, 2017.

May. 31

Interest Expense (100,000 × 6% × 5/12)

2,500

2017

Interest Payable

3,500

Cash (100,000 × 6% × 12/12)

6,000

May 31

Note Payable

100,000

2017

Cash

100,000

+ Cash (A) –

June 1

100,000

2011

6,000

May 31

100,000

May 31

+ Interest Expense (E) –

May 31

2,500

– Interest Payable (L) +

3,500

Dec. 31

2011

May 31

3,500

– Note Payable (L) +

100,000

June 1

2011

May 31

100,000

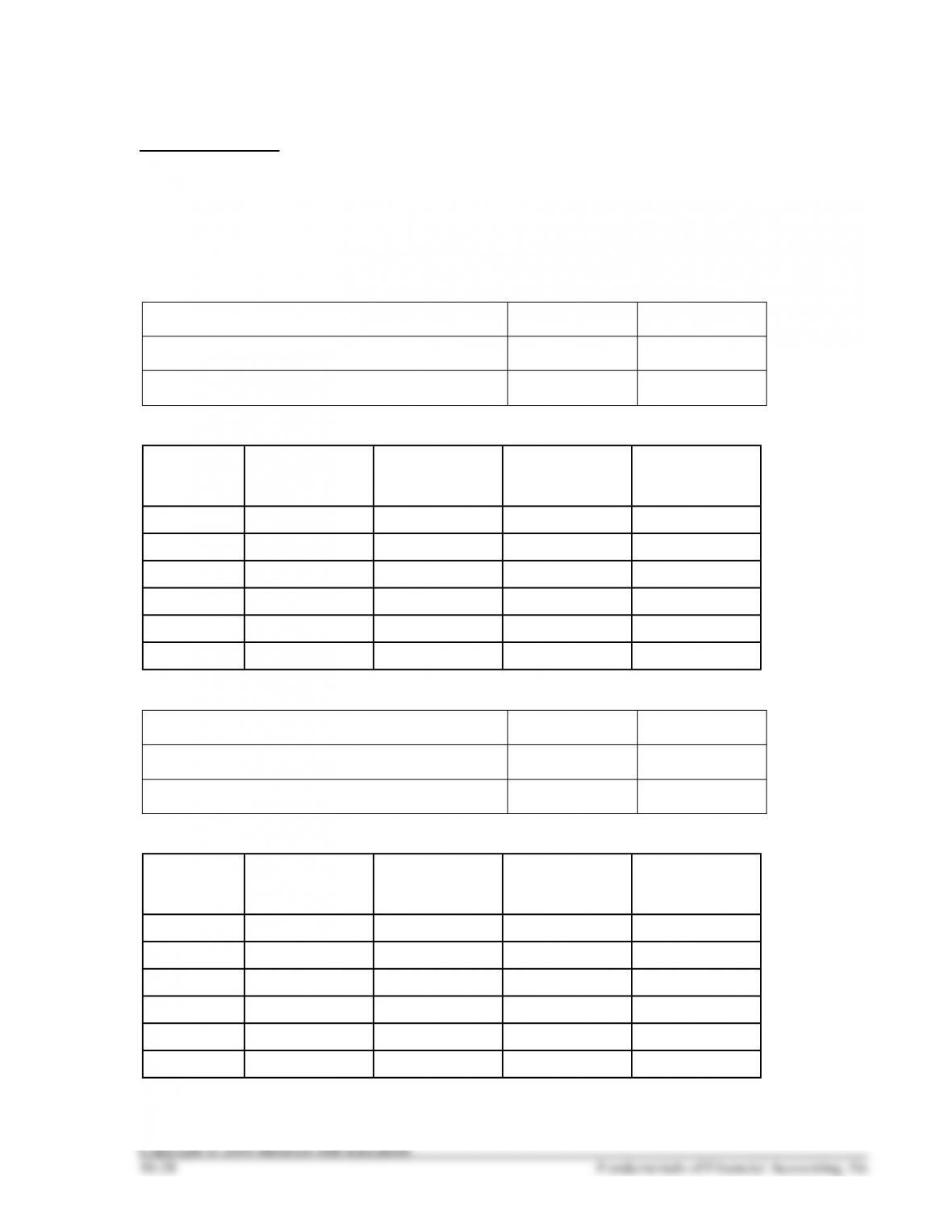

HANDOUT 10–3

UNEARNED REVENUE

On January 1, 2017, Charlie Rangel paid $2,000 for a two–year membership to the Beam Gym.

Prepare the journal entry to record the receipt of cash on January 1, 2017.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

By December 31, 2017, one half of Rangel’s membership expired. Prepare the required adjusting journal

entry on that date.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

By December 31, 2018, the remainder of Rangel’s membership expired. Prepare the required adjusting

journal entry on that date.

Debit and credit the accounts affected

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Post the entries above to the Unearned Revenue account:

– Unearned Revenue (L) +

1/1/17

12/31/17

End Bal.

12/31/18

End Bal.

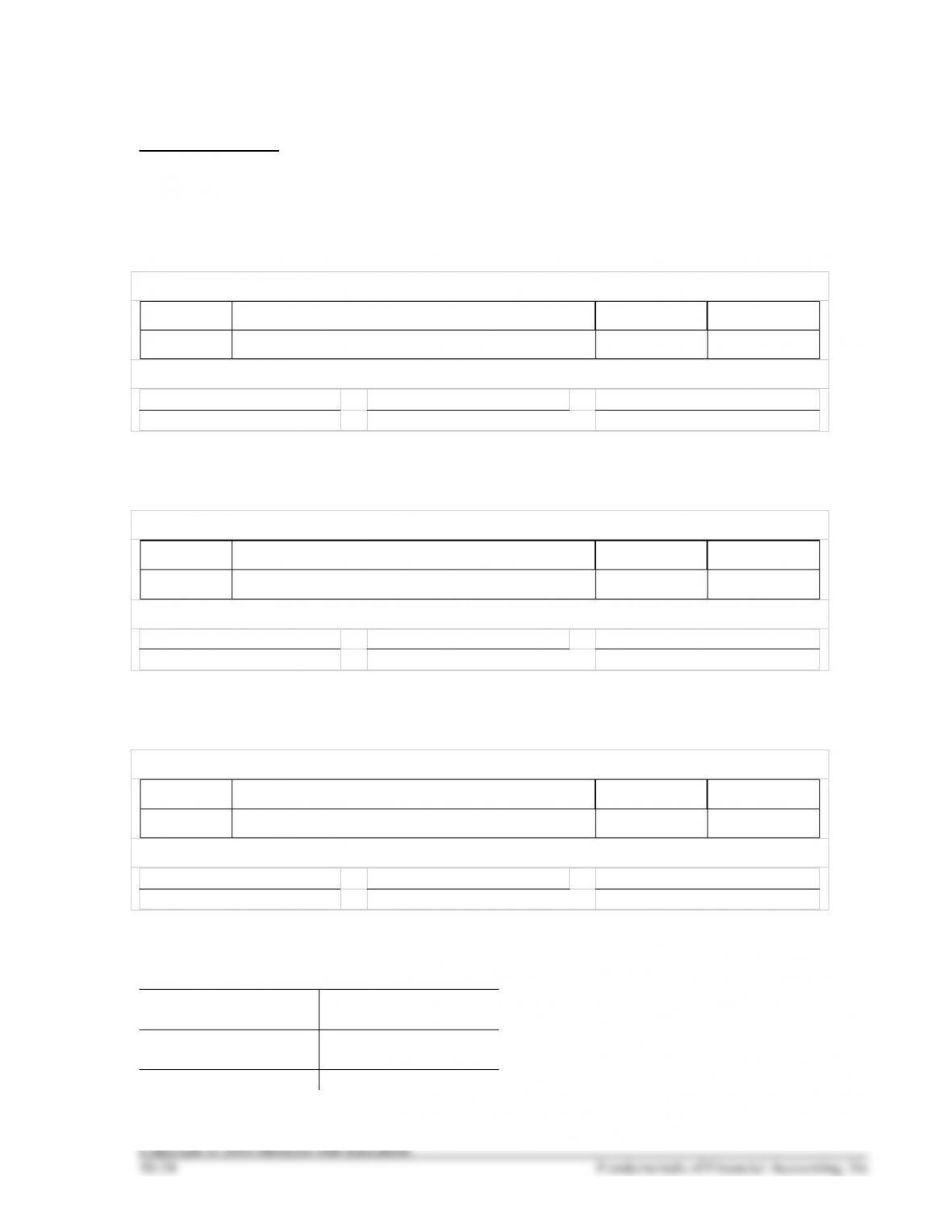

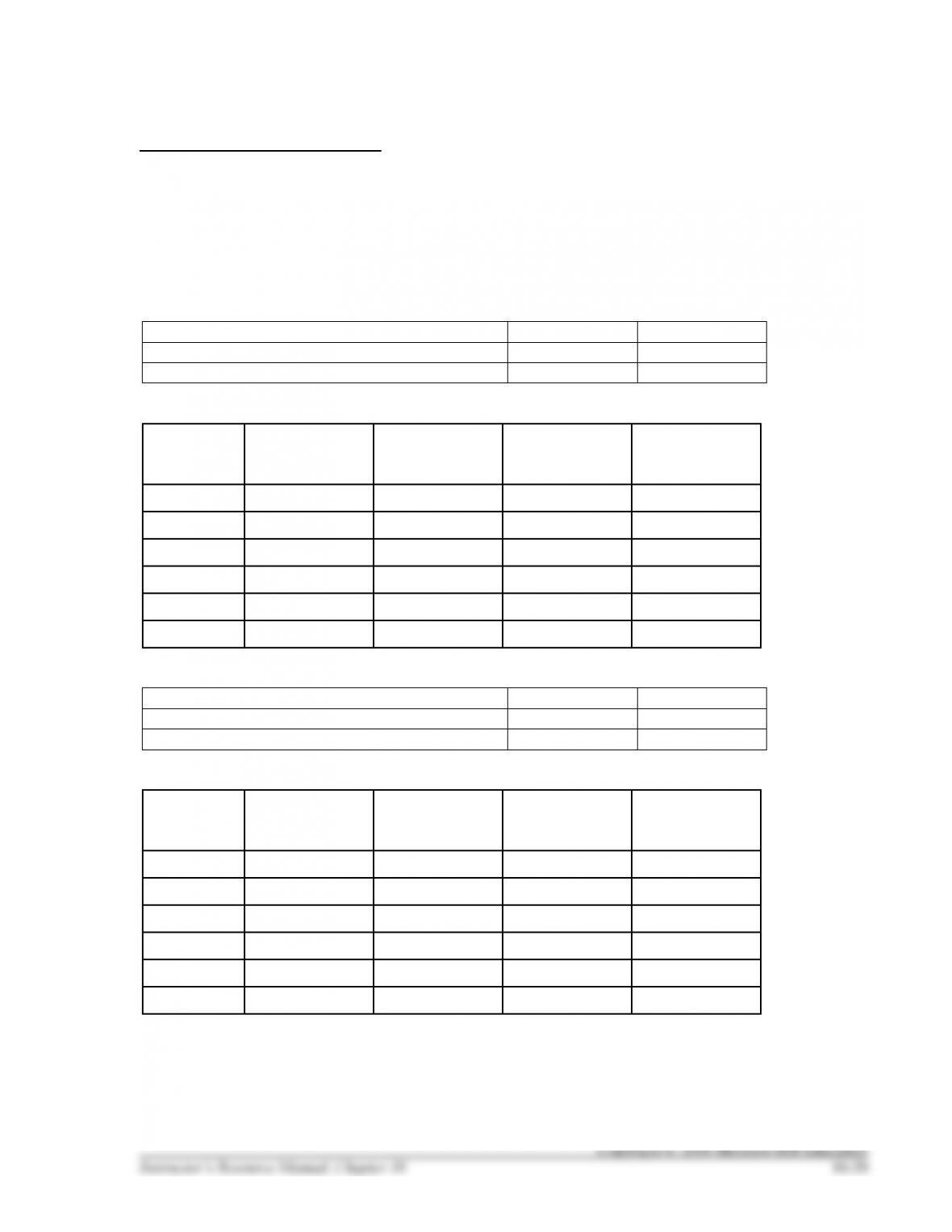

HANDOUT 10–3 SOLUTION

UNEARNED REVENUE

On January 1, 2017, Charlie Rangel paid $2,000 for a two–year membership to the Beam Gym.

Prepare the journal entry to record the receipt of cash on January 1, 2017.

Debit and credit the accounts affected

Jan. 1

Cash

2,000

2017

Unearned Revenue

2,000

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

+2,000

Unearned

Revenue

+2,000

By December 31, 2017, one half of Rangel’s membership expired. Prepare the required adjusting journal

entry on that date.

Debit and credit the accounts affected

Dec. 31

Unearned Revenue

1,000

2017

Service Revenue

1,000

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Unearned

Revenue

–1,000

Service

Revenue

+1,000

By December 31, 2018, the remainder of Rangel’s membership expired. Prepare the required adjusting

journal entry on that date.

Debit and credit the accounts affected

Dec. 31

Unearned Revenue

1,000

2018

Service Revenue

1,000

Ensure the equation still balances and debits = credits

Assets

=

Liabilities

+

Stockholders’ Equity

Unearned

Revenue

–1,000

Service

Revenue

+1,000

Post the entries above to the Unearned Revenue account:

– Unearned Revenue (L) +

2,000

1/1/17

12/31/17

1,000

1,000

End Bal

12/31/18

1,000

0

End Bal

HANDOUT 10–4

ISSUING BONDS

Consider the issuance of $800,000, 5-year, 8% payable annually (market rate 12%) for cash of $684,627

on January 1, 2016. Were these bonds issued at a discount or at a premium? Why?

Prepare the journal entry to record the issuance (sale) of the bonds:

Complete the following interest schedule (assuming straight-line amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Discount

Carrying Value

(Net Liability)

1/1/2016

None

None

None

12/31/2016

12/31/2017

12/31/2018

12/31/2019

12/31/2020

Prepare the journal entry to record the first payment of interest on December 31, 2016:

Complete the following interest schedule (assuming effective-interest amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Discount

Carrying Value

(Net Liability)

1/1/2016

None

None

None

12/31/2016

12/31/2017

12/31/2018

12/31/2019

12/31/2020

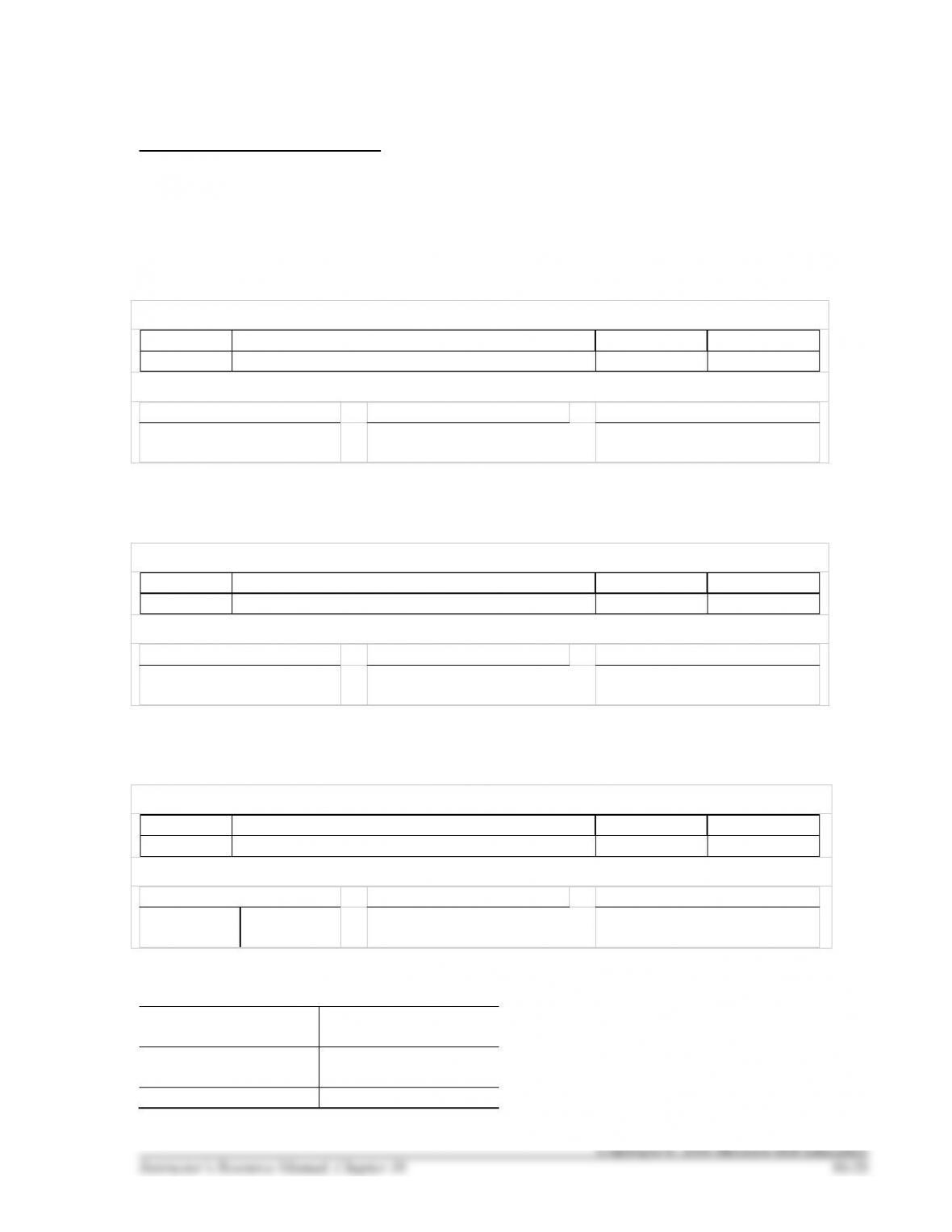

HANDOUT 10–4 SOLUTION

ISSUING BONDS

Consider the issuance of $800,000, 5-year, 8% payable annually (market rate 12%) for cash of $684,627

on January 1, 2016. Were these bonds issued at a discount or at a premium? Why?

The bonds were issued at a discount since the contract rate is less than the market rate.

Prepare the journal entry to record the issuance (sale) of the bonds:

Cash

684,627

Discount on Bonds Payable

115,373

Bonds Payable

800,000

Complete the following interest schedule (assuming straight-line amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Discount

Carrying Value

(Net Liability)

1/1/2016

None

None

None

684,627

12/31/2016

64,000

87,075

23,075

707,702

12/31/2017

64,000

87,075

23,075

730,776

12/31/2018

64,000

87,075

23,075

753,851

12/31/2019

64,000

87,075

23,075

776,925

12/31/2020

64,000

87,075

23,075

800,000

Prepare the journal entry to record the first payment of interest on December 31, 2016:

Interest Expense

87,075

Discount on Bonds Payable

23,075

Cash

64,000

Complete the following interest schedule (assuming effective-interest amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Discount

Carrying Value

(Net Liability)

1/1/2016

None

None

None

684,627

12/31/2016

64,000

82155

18155

702,782

12/31/2017

64,000

84334

20334

723,116

12/31/2018

64,000

86774

22774

745,890

12/31/2019

64,000

89507

25507

771,397

12/31/2020

64,000

92568

28568

799,965

Difference due

to rounding

HANDOUT 10–5

ISSUING BONDS

Consider the issuance of $1,200,000, 5-year, 10% payable annually (market rate 8%) for cash of

$1,295,844 on January 1, 2016. Were these bonds issued at a discount or at a premium? Why?

Prepare the journal entry to record the issuance (sale) of the bonds:

Complete the following interest schedule (assuming straight-line amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Premium

Carrying Value

(Net Liability)

1/1/2016

None

None

None

12/31/2016

12/31/2017

12/31/2018

12/31/2019

12/31/2020

Prepare the journal entry to record the first payment of interest on December 31, 2016:

Complete the following interest schedule (assuming effective-interest amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Premium

Carrying Value

(Net Liability)

1/1/2016

None

None

None

12/31/2016

12/31/2017

12/31/2018

12/31/2019

12/31/2020

HANDOUT 10–5 SOLUTION

ISSUING BONDS

Consider the issuance of $1,200,000, 5-year, 10% payable annually (market rate 8%) for cash of

$1,295,844 on January 1, 2016. Were these bonds issued at a discount or at a premium? Why?

The bonds were issued at a premium since the contract rate is more than the market rate.

Prepare the journal entry to record the issuance (sale) of the bonds:

Cash

1,295,844

Premium on Bonds Payable

95,844

Bonds Payable

1,200,000

Complete the following interest schedule (assuming straight-line amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Premium

Carrying Value

(Net Liability)

1/1/2016

None

None

None

1,295,844

12/31/2016

120,000

100,831

19,169

1,276,675

12/31/2017

120,000

100,831

19,169

1,257,506

12/31/2018

120,000

100,831

19,169

1,238,338

12/31/2019

120,000

100,831

19,169

1,219,169

12/31/2020

120,000

100,831

19,169

1,200,000

Prepare the journal entry to record the first payment of interest on December 31, 2016:

Interest Expense

100,831

Premium on Bonds Payable

19,169

Cash

120,000

Complete the following interest schedule (assuming effective-interest amortization):

Date

Cash

Payment of

Interest

Interest

Expense

Amortization of

Premium

Carrying Value

(Net Liability)

1/1/2016

None

None

None

1,295,844

12/31/2016

120,000

103,668

16,332

1,279,512

12/31/2017

120,000

102,361

17,639

1,261,872

12/31/2018

120,000

100,950

19,050

1,242,822

12/31/2019

120,000

99,426

20,574

1,222,248

12/31/2020

120,000

97,780

22,220

1,200,028

Difference due

to rounding