S1-3

S1-4

Req. 1

The accounting concept that the Rigas family is accused of violating is the separate

entity assumption.

Req. 2

Based on the limited information available, it is difficult to categorize particular dealings

as appropriate or inappropriate. Dealings would clearly be inappropriate if they involved

Adelphia paying for items for the owners’ personal use or to unfairly transfer some of

S1-5

Req. 1

You should take the position that an independent annual audit of the financial

statements is an absolute must. This is the best way to ensure that the financial

statements are complete, are free from bias, and conform with GAAP. You should be

S1-6

Req. 1

A balance sheet lists items owned (assets) and owed (liabilities) at a particular point in

time, producing a “net worth” that represents the excess of assets over liabilities. Two

balance sheets are presented below, one based on historical costs (similar to GAAP)

and one based on fair values (similar to a personal financial planning approach). Notes

S1-6 (continued):

Req. 1 (continued)

Based on fair value:

Ashley

Jason

Assets

Assets

Cash

$ 1,000

Cash

$ 6,000

Artwork

1,400

PlayStation Console

180

Total Assets

2,400

Total Assets

6,180

Liabilities

Liabilities

Loan Payable

250

Tuition Payable

800

Total Liabilities

250

Loan Payable

4,800

Total Liabilities

5,600

Net Worth

$ 2,150

Net Worth

$ 580

The notes are an important part of these balance sheets.

Notes:

1) The goal in preparing these balance sheets is to estimate each individual’s net

worth, represented as the excess of assets over liabilities.

2) Use of historical cost is consistent with generally accepted accounting principles.

Note that these asset values have not been adjusted for “value” consumed

3) Some potential assets (e.g., Porsche) are not recorded because their likelihood

of occurrence is not certain.

Req. 2

Based on the calculations of net worth and underlying assumptions indicated above,

Ashley is “better off” because her net worth ($1,550 or $2,150) is greater than Jason’s

S1-6 (continued):

Req. 3

An income statement lists the amounts earned (revenues) and costs incurred

(expenses) during a particular period of time, producing “net income” that represents the

Fundamentals of Financial Accounting, 5/e 1-43

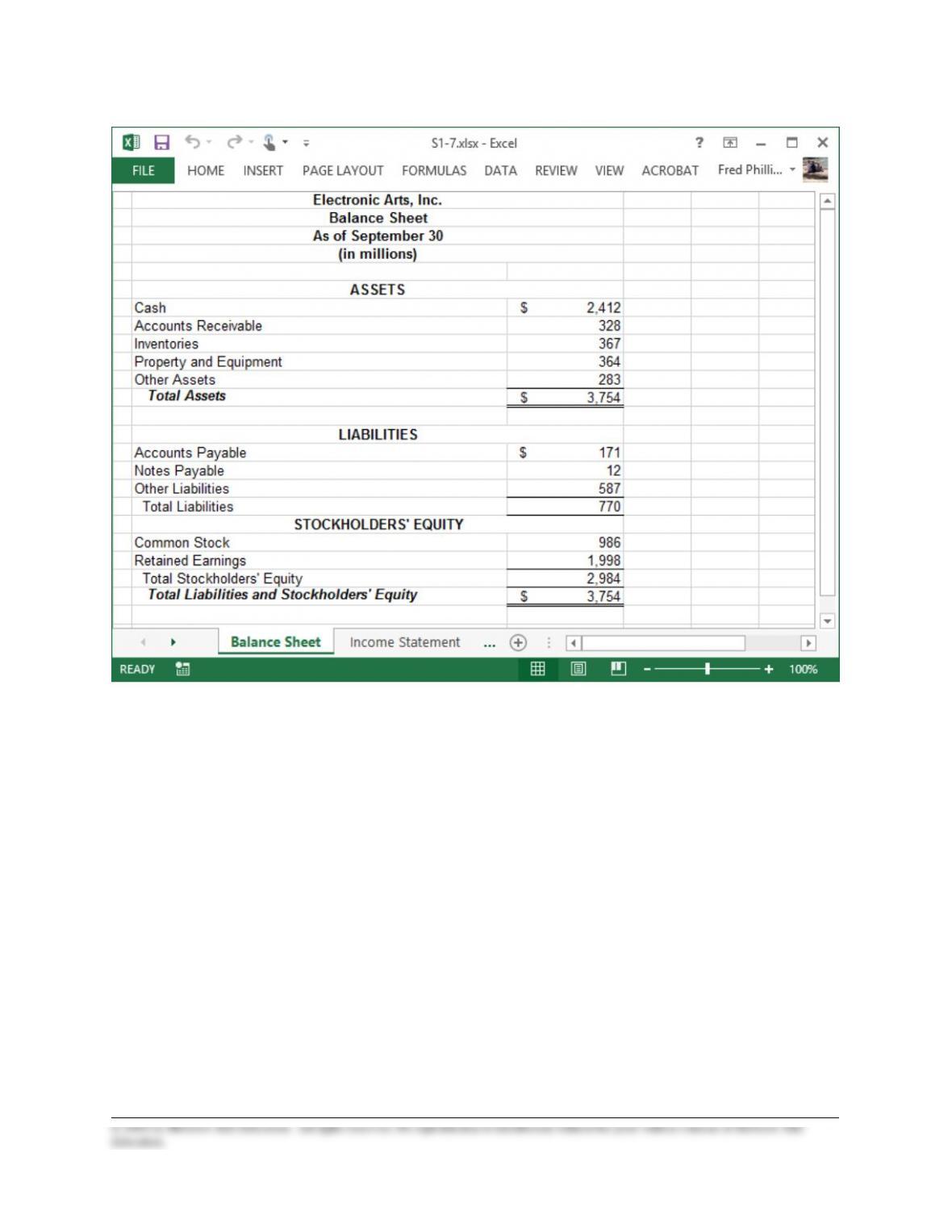

S1-7

Fundamentals of Financial Accounting, 5/e 1-44

© 2016 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw–Hill

Education.

S1-7 (continued)

ANSWERS TO CONTINUING CASE

CC1-1

Req. 1

NICOLE’S GETAWAY SPA

Income Statement (forecasted)

For the Year Ended December 31, 2015

Revenues:

Sales Revenue

$ 40,000

Expenses:

Salaries and Wages Expense

24,000

Supplies Expense

7,000

Office Expenses

5,000

Income Tax Expense

1,600

Total Expenses

37,600

Net Income

$ 2,400

CC1-1 (continued)

Req. 2

NICOLE’S GETAWAY SPA

Statement of Retained Earnings (forecasted)

For the Year Ended December 31, 2015

Retained Earnings, January 1, 2015

$ 0

Add: Net Income

Subtract: Dividends

2,400

(2,000)

Retained Earnings, December 31, 2015

$ 400

Req. 3

NICOLE’S GETAWAY SPA

Balance Sheet (forecasted)

At December 31, 2015

Assets:

Cash

Accounts Receivable

Building and Equipment

Total Assets

$ 2,150

1,780

70,000

$73,930

Liabilities:

Accounts Payable

Notes Payable

Total Liabilities

$ 4,660

38,870

43,530

30,000

400

30,400

Stockholders’ Equity:

Common Stock

Retained Earnings

Total Stockholders’ Equity

Total Liabilities and Stockholders’ Equity

$73,930

Req. 4

As of December 31, 2015, more financing is expected to come from creditors ($43,530)

than from stockholders ($30,400).