Supplemental Enrichment Activities

Note: These activities would be suitable for individual or group activities.

1. Handout 1–1

Use this handout for an in-class activity designed to review the classification of various accounts,

elements, or transactions on the financial statements. The solution follows the handout master.

2. Handout 1–2

Use this handout for an in-class activity designed to review the classification of various account

names on the balance sheet. The solution follows the handout master.

3. Handout 1–3

Use this handout for an in-class activity designed to review the classification of various transactions

on the statement of cash flows. The solution follows the handout master.

4. Handout 1–4

Use this handout for an in-class activity designed to review the individual financial statements and the

relationships among the financial statements. The solution follows the handout master.

5. Consider showing the first segment of the following video in class; most students will be able to

identify with the “fraudster.” Lively discussion of the manner in which the fraud was perpetrated will

follow.

The Association of Certified Fraud Examiners produced a video in 1991 called “Cooking the Books:

What Every Accountant Should Know about Fraud.” It can be ordered by calling 1-800-245-3321 or

visiting the ACFE web site at www.cfenet.com. (Consider joining as an educator to obtain a

discounted rate.)

Three frauds are overviewed: ZZZZ Best Carpet, Regina Vacuum Cleaner Company, and ESM

Group, Inc. (ESM Government Securities). ZZZZ Best Carpet might be the best one to use. Barry

Minkow, the CEO and major stockholder, is interviewed in prison. The video segment discusses

revenue overstatements, deferred costs, asset valuations, inadequate disclosures, and horizontal and

vertical analysis. It is very well done. (Note that the discussion of ratio analysis and trends would

also be appropriate for Chapter 13—Measuring and Evaluating Financial Performance.).

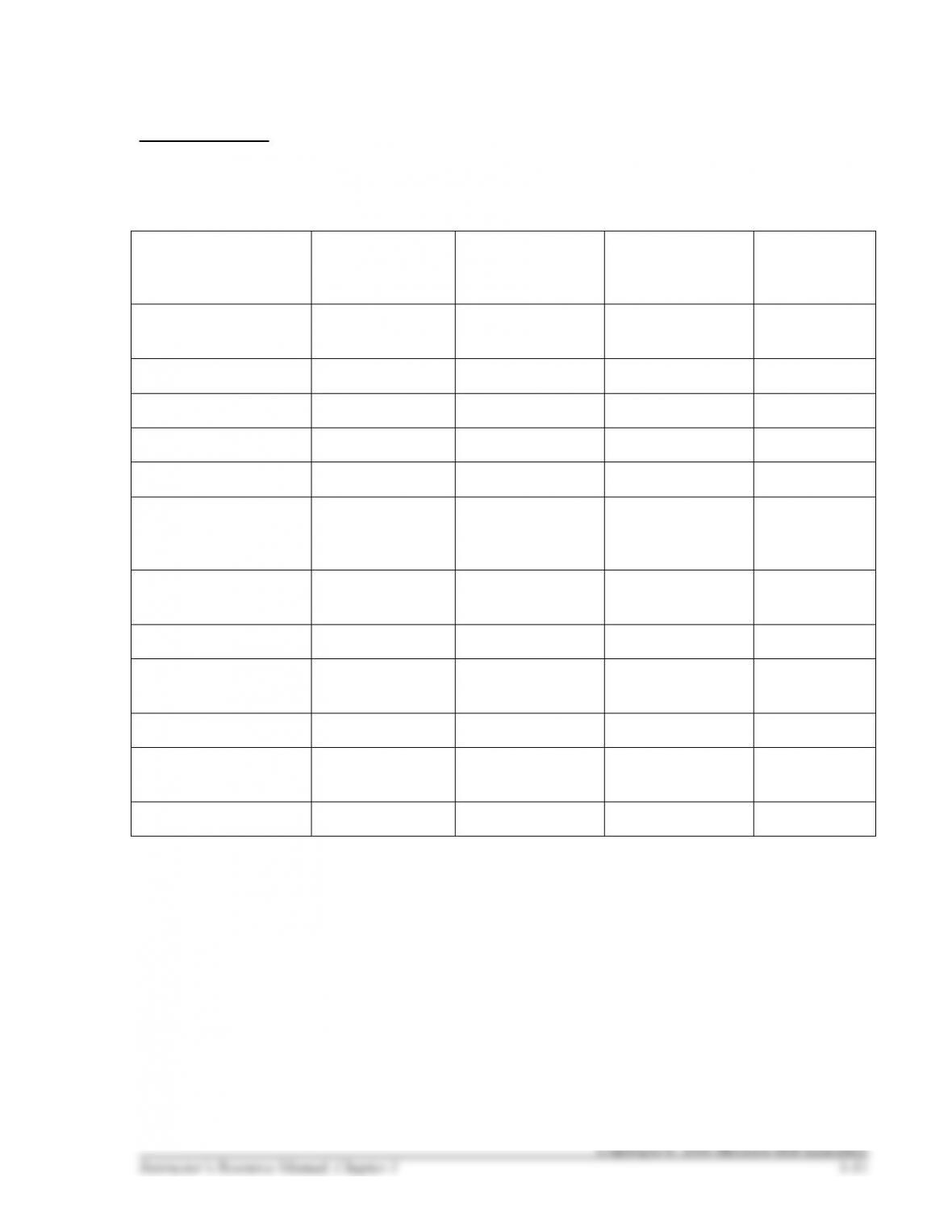

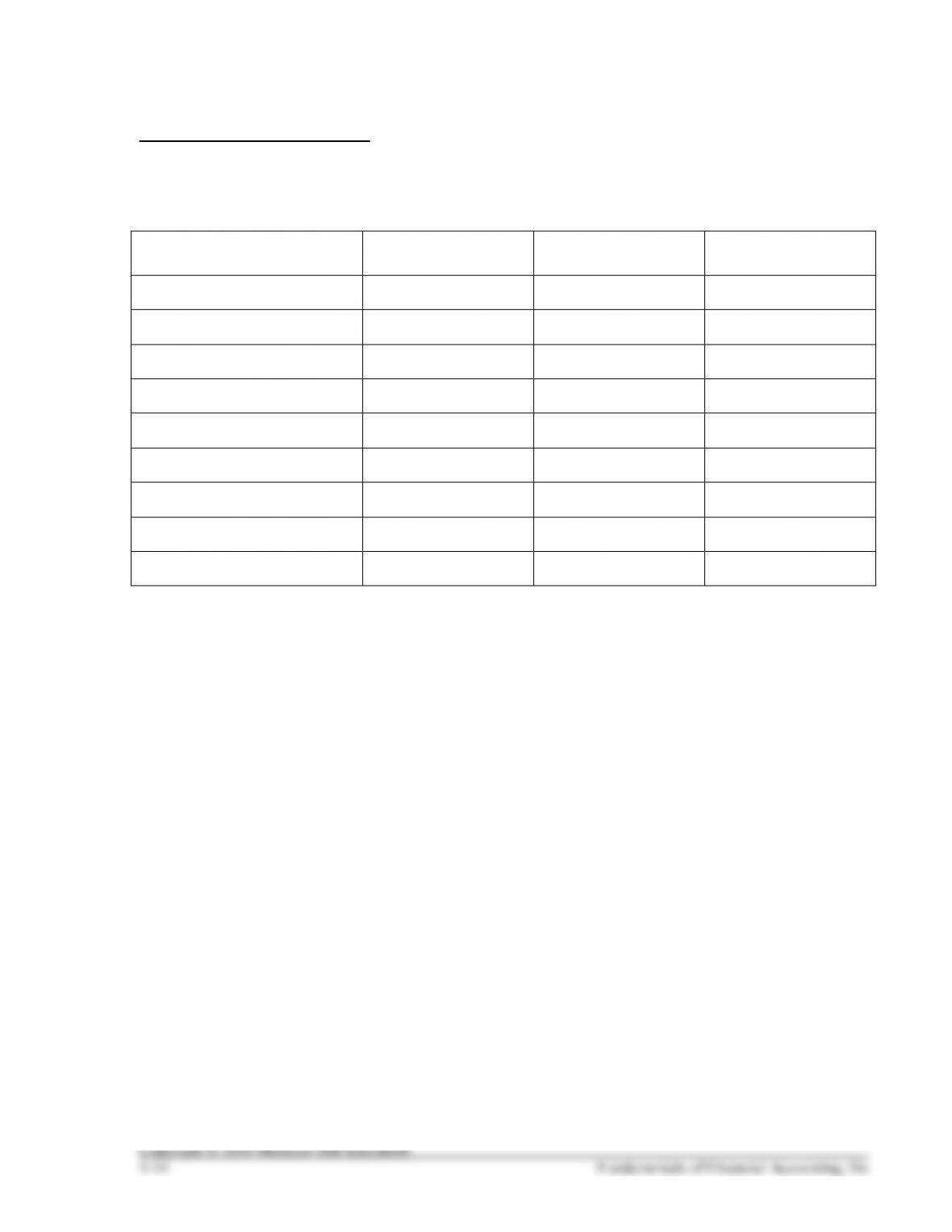

HANDOUT 1–1

COMPONENTS OF FINANCIAL STATEMENTS

Match each account, element, or transaction to the financial statement(s) on which it would be reported.

Account or Element

Income

Statement

Statement of

Retained

Earnings

Balance Sheet

Statement of

Cash Flows

a. The amount of cash

paid for equipment

b. Cash

c. Notes Payable

d. Common Stock

e. Supplies

f. The amount of cash

collected from

customers

g. Accounts

Receivable

h. Notes Payable

i. Salaries and Wages

Expense

j. Equipment

k. Dividends paid to

stockholders

l. Net Income

HANDOUT 1–1 SOLUTION

COMPONENTS OF FINANCIAL STATEMENTS

Match each account, element, or transaction to the financial statement(s) on which it would be reported.

Account or Element

Income

Statement

Statement of

Retained

Earnings

Balance Sheet

Statement of

Cash Flows

a. The amount of cash

paid for equipment

X

b. Cash

X

c. Notes Payable

X

d. Common Stock

X

e. Supplies

X

f. The amount of cash

collected from

customers

X

g. Accounts

Receivable

X

h. Notes Payable

X

i. Salaries and Wages

Expense

X

j. Equipment

X

k. Dividends paid to

stockholders

X

X

l. Net Income

X

X

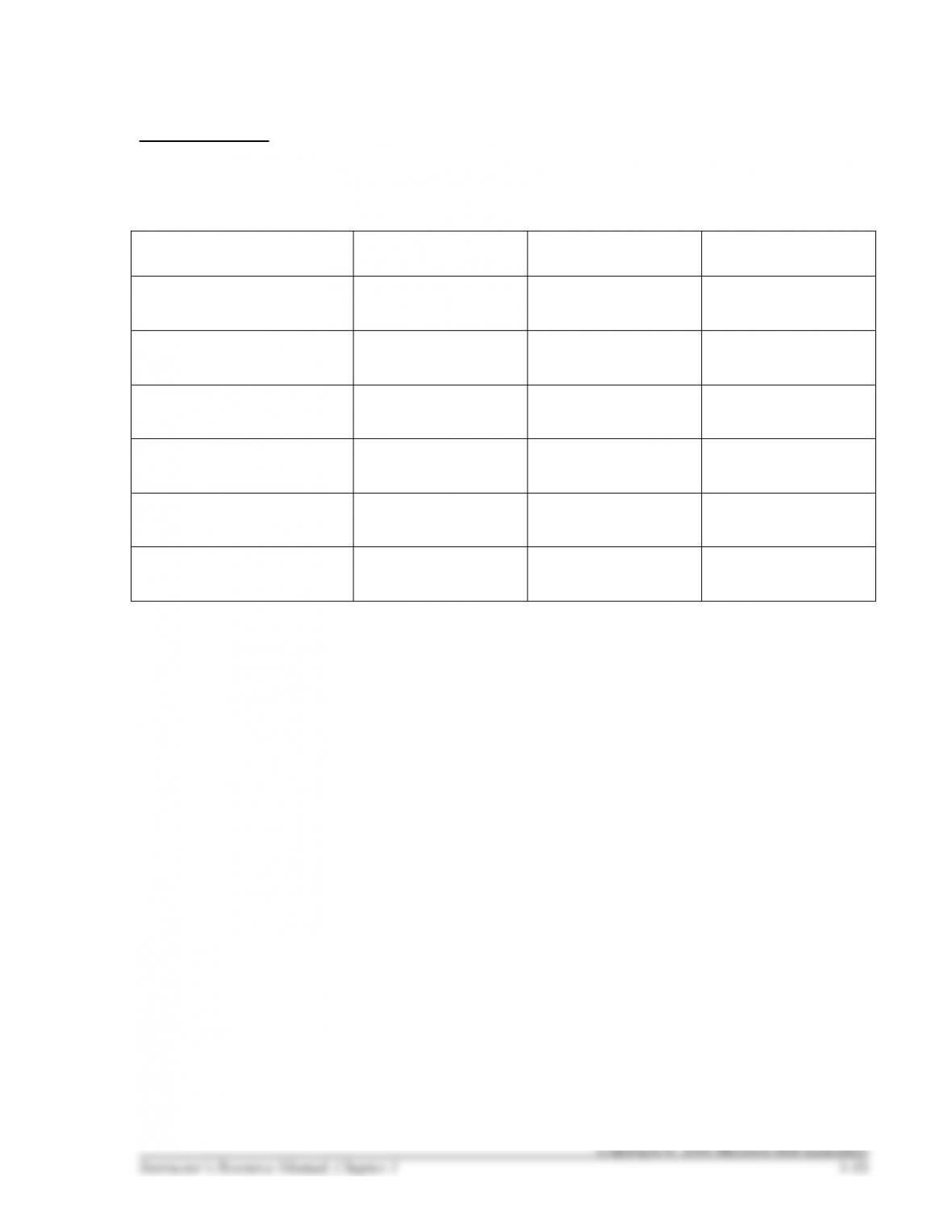

HANDOUT 1–2

BASIC BALANCE SHEET ELEMENTS

Match each account to its classification on the balance sheet.

Account

Asset

Liability

Stockholders’

Equity

a. Notes Payable

b. Cash

c. Common Stock

d. Supplies

e. Accounts Receivable

f. Accounts Payable

g. Equipment

h. Notes Payable

i. Retained Earnings

HANDOUT 1–2 SOLUTION

BASIC BALANCE SHEET ELEMENTS

Match each account to its classification on the balance sheet.

Account

Asset

Liability

Stockholders’

Equity

a. Notes Payable

X

b. Cash

X

c. Common Stock

X

d. Supplies

X

e. Accounts Receivable

X

f. Accounts Payable

X

g. Equipment

X

h. Notes Payable

X

i. Retained Earnings

X

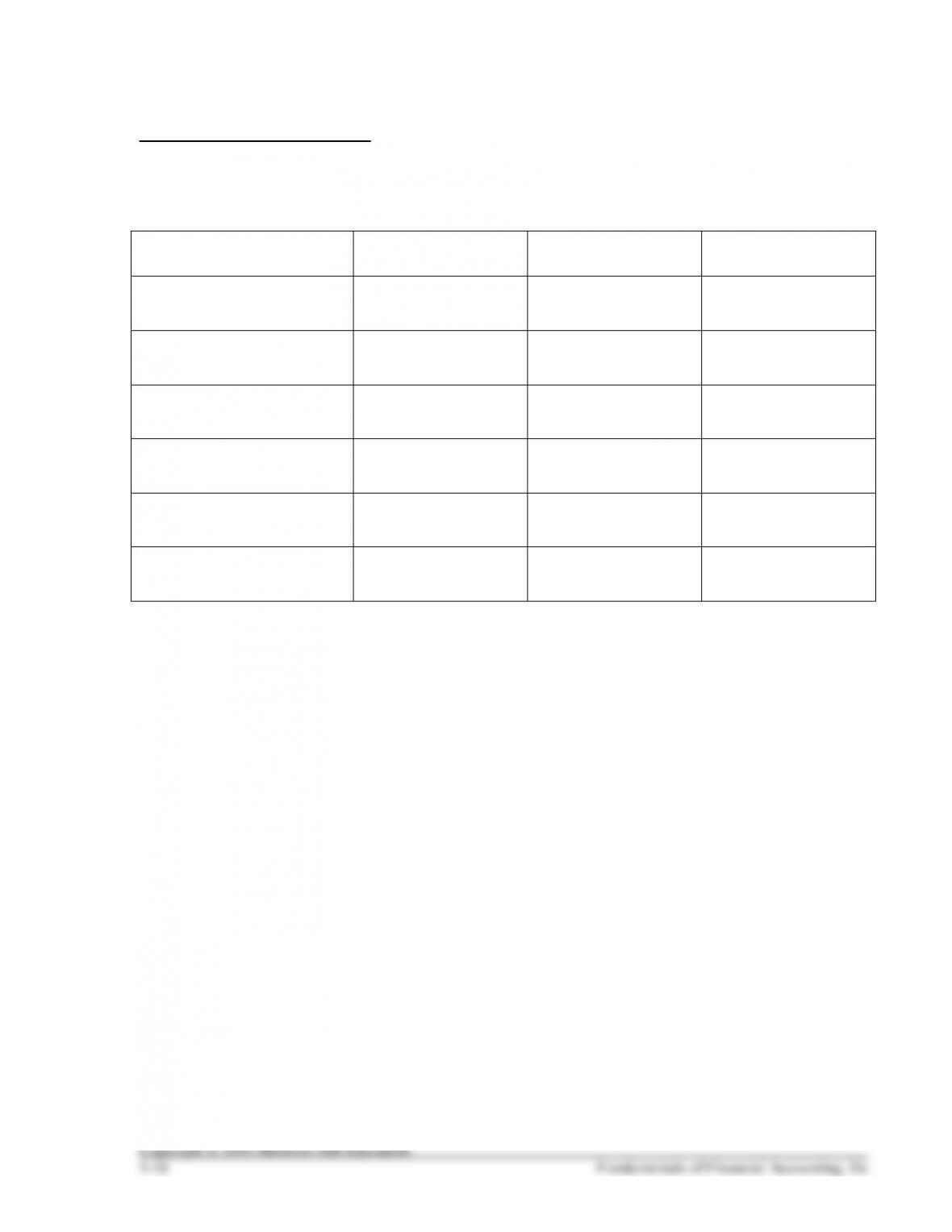

HANDOUT 1–3

STATEMENT OF CASH FLOWS

Match each activity to its classification on the statement of cash flows.

Activity

Operating

Investing

Financing

a. Cash paid to employees

and suppliers

b. Cash used to buy

equipment and software

c. Cash dividends paid to

stockholders

d. Cash received from

customers

e. Cash received from

selling equipment

f. Cash borrowed from the

bank

HANDOUT 1–3 SOLUTION

STATEMENT OF CASH FLOWS

Match each activity to its classification on the statement of cash flows.

Activity

Operating

Investing

Financing

a. Cash paid to employees

and suppliers

X

b. Cash used to buy

equipment and software

X

c. Cash dividends paid to

stockholders

X

d. Cash received from

customers

X

e. Cash received from

selling equipment

X

f. Cash borrowed from the

bank

X

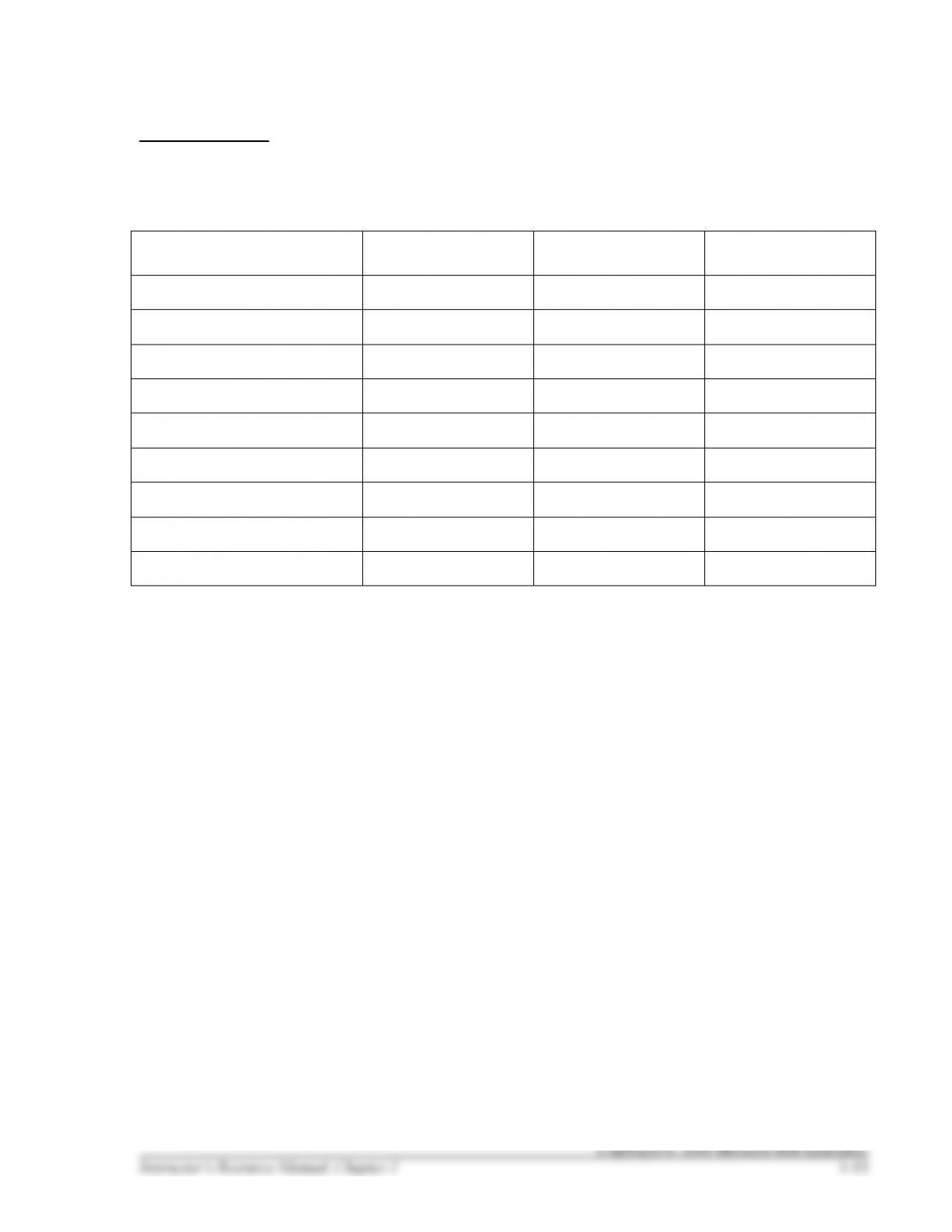

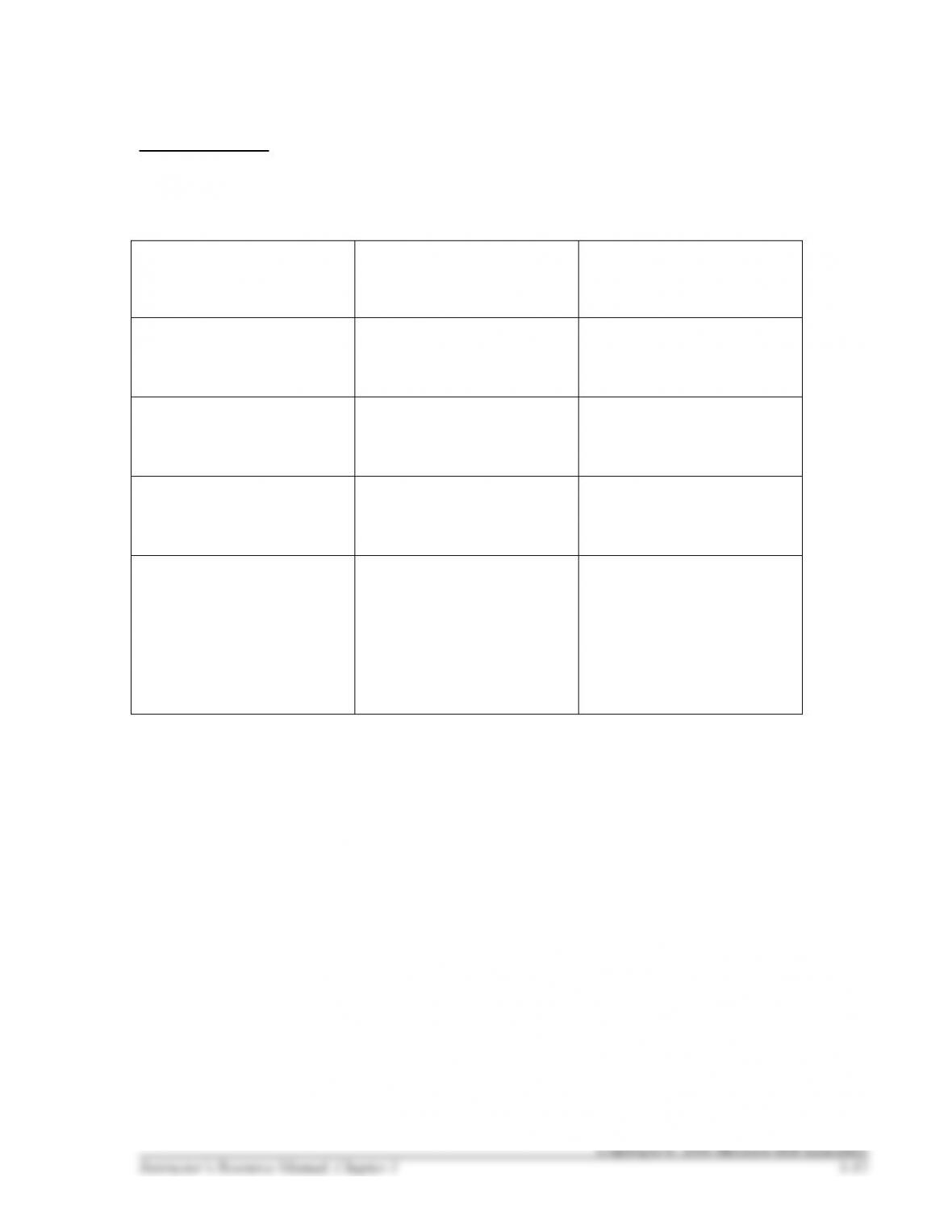

HANDOUT 1–4

TEAM PROJECT—OVERVIEW OF FINANCIAL STATMENTS

Complete the following table.

Financial Statement

Purpose

Equation

Income Statement

Statement of Retained

Earnings

Balance Sheet

Statement of Cash Flows

RELATIONSHIPS AMONG FINANCIAL STATEMENTS

Then, answer the following questions.

1. How does the income statement tie to the statement of retained earnings?

2. How does the statement of retained earnings tie to the balance sheet?

3. How does the balance sheet tie to the statement of cash flows?

HANDOUT 1–4 SOLUTION

TEAM PROJECT—OVERVIEW OF FINANCIAL STATEMENTS

Complete the following table.

Financial Statement

Purpose

Equation

Income Statement

The financial performance of

the business during the

current accounting period.

Revenues

– Expenses

= Net Income

Statement of Retained

Earnings

The accumulation of earnings

retained in the business

during the current accounting

period with that of prior

periods.

Beginning Retained Earnings

+ Net Income (this period)

– Dividends (this period)

= Ending Retained Earnings

Balance Sheet

The financial position of a

business at a point in time.

Assets = Liabilities +

Stockholders’ Equity

Statement of Cash Flows

Inflows (receipts) and

outflows (payments) of cash

during the current accounting

period.

+/– Cash Flows from

Operating Activities

+/– Cash Flows from

Investing Activities

+/– Cash Flows from

Financing Activities

= Change in Cash

+ Beginning Cash

= Ending Cash

RELATIONSHIPS AMONG FINANCIAL STATEMENTS

Then, answer the following questions.

1. How does the income statement tie to the statement of retained earnings?

Net income, from the income statement, is a component in determining ending retained earnings on

the statement of Retained Earnings.

2. How does the statement of retained earnings tie to the balance sheet?

Ending retained earnings on the statement of retained earnings is reported in the stockholders’ equity

section of the balance sheet.

3. How does the balance sheet tie to the statement of cash flows?

Cash on the balance sheet is equal to the ending Cash reported on the statement of cash flows.