Appendix D

Investments in Other Corporations

ANSWERS TO QUESTIONS

1. The appropriate method of accounting for investments in another corporation

depends on the level of involvement the investor has over the other company.

When the investor controls the affiliate, the acquisition/consolidation method is

2. The accounting methods used for available-for-sale securities and trading

securities differ primarily in how unrealized gains or losses are recorded and

3. The primary differences between passive investments and those involving a

significant influence (i.e., equity method investments) involve the recording and

reporting of the affiliate’s net income and dividends. The investor’s share of the

affiliate’s net income is recorded as income for equity method investments because

4. Investments involving significant influence are accounted for using the equity

method whereas those involving control are accounted for using the acquisition/

5. Consolidated financial statements are financial statements prepared under the

6. Under the equity method, dividends received from the affiliated company are not

recorded as revenue because to record the dividends as revenue would involve

7. Passive investments earn a return from (1) dividends received, and (2) increases in

the stock price of the investee.

8. Unrealized gains and losses for available-for-sale securities are reported in other

comprehensive income. Unrealized gains and losses for trading securities are

reported as revenues and expenses on the income statement when calculating net

Authors’ Recommended Solution Time

(Time in minutes)

Mini-exercises

Exercises

Problems

No.

Time

No.

Time

No.

Time

1

6

1

20

CP1

40

2

6

2

15

CP2

40

3

6

3

15

PA1

40

4

6

4

15

PA2

40

5

6

5

15

6

6

6

15

7

4

7

15

D–4 Solutions Manual

© 2016 by McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

ANSWERS TO MINI-EXERCISES

MD–1

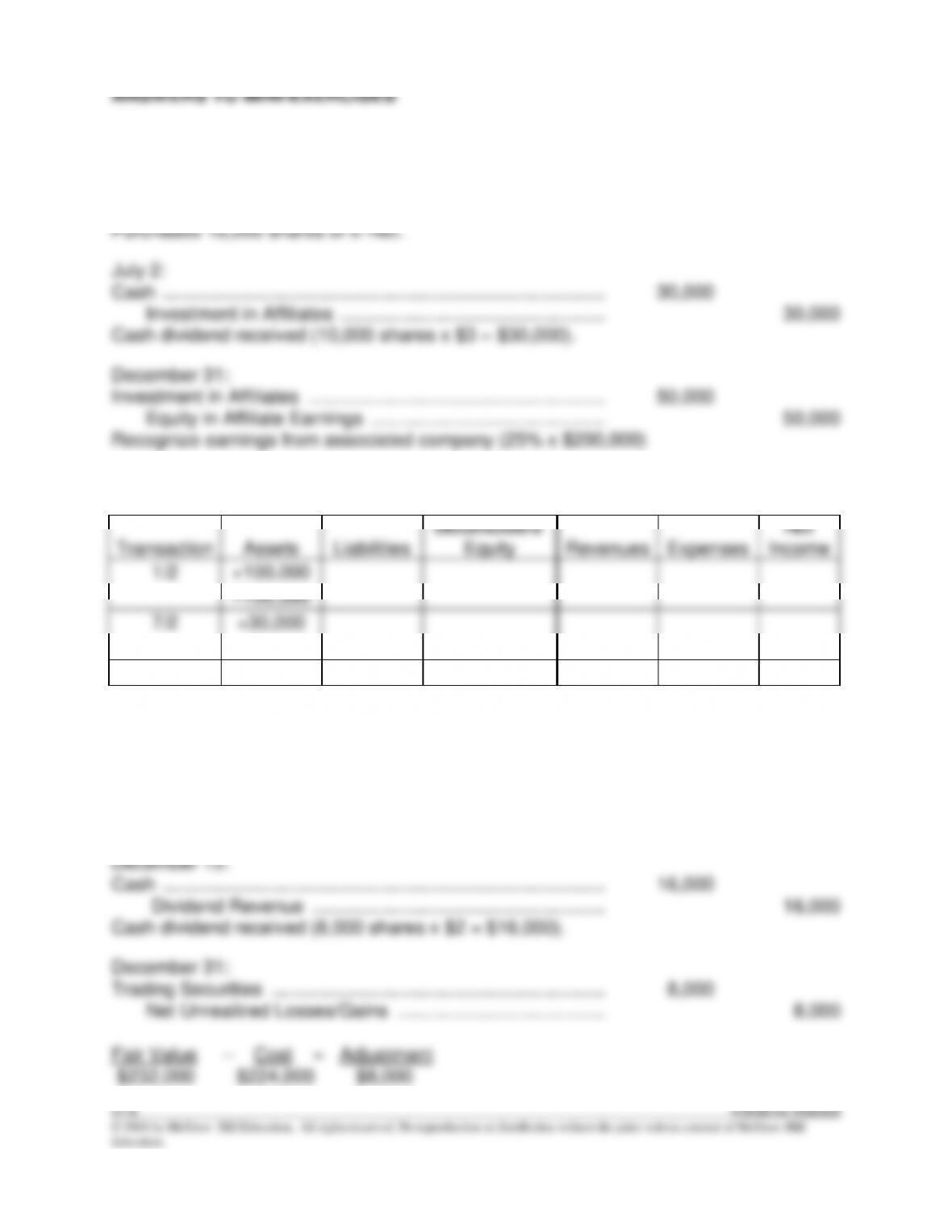

January 2:

Investment in Affiliates ………………………………………………….

100,000

Cash ……………………………………………………………………

100,000

Purchased 10,000 shares of E-Net.

Cash ………………………………………………………………………….

30,000

Investment in Affiliates ……………………………………………

30,000

Cash dividend received (10,000 shares x $3 = $30,000).

Investment in Affiliates …………………………………………………

50,000

Equity in Affiliate Earnings ………………………………………

50,000

Recognize earnings from associated company (25% x $200,000)

MD–2

Balance Sheet

Income Statement

Transaction

Assets

Liabilities

Stockholders’

Equity

Revenues

Expenses

Net

Income

1/2

+100,000

–100,000

7/2

+30,000

–30,000

12/31

+50,000

+50,000

+50,000

+50,000

MD–3

July 2:

Trading Securities ……………………………………………………….

224,000

Cash ……………………………………………………………………

224,000

Purchased 8,000 shares (16%) of Cox Corporation common stock at $28 per share.

Cash ………………………………………………………………………….

16,000

Dividend Revenue ………………………………………………..

16,000

Cash dividend received (8,000 shares x $2 = $16,000).

Trading Securities ……………………………………………………….

8,000

Net Unrealized Losses/Gains ………………………………….

8,000

Fair Value − Cost = Adjustment

$232,000 $224,000 $8,000

MD–4

Balance Sheet

Income Statement

Transaction

Assets

Liabilities

Stockholders’

Equity

Revenues

Expenses

Net

Income

7/2

+224,000

–224,000

12/15

+16,000

+16,000

+16,000

+16,000

12/31

+8,000

+8,000

+8,000

+8,000

MD–5

July 2:

Available-for-Sale Securities …………………………………………

224,000

Cash ……………………………………………………………………

224,000

Purchased 8,000 shares (16%) of Cox Corporation common stock at $28 per share.

Cash ………………………………………………………………………….

16,000

Dividend Revenue …………………………..……………………

16,000

Cash dividend received (8,000 shares x $2 = $16,000).

Balance Sheet

Income Statement

Stockholders’

Net

MD–7

March 20:

Trading Securities ……………………………………………………….

17,400

Cash ……………………………………………………………………

17,400

Purchased 600 shares of General Eccentric stock at $29 per share.

Cash ………………………………………………………………………….

19,800

Trading Securities …………………………………………………

17,400

Gain on Sale of Investments …………………………………..

2,400

Sold shares for $19,800 (600 x $33), realizing a gain of

$2,400 ($19,800 – $17,400).

ANSWERS TO EXERCISES

ED–1

Req. 1

The equity method must be used because the company owns 35% (21,000 ÷ 60,000) of

the total shares outstanding of Nueces Corporation. The equity method must be used

when there is at least 20% but not more than 50% ownership in existence. The investor

must use the equity method because it can exercise significant influence, but not

control, over the operating and financing policies of Nueces Corporation.

Req. 2

Investment in Affiliates …………………………………………………

252,000

Cash ……………………………………………………………………..

252,000

Purchased 21,000 shares (35%) of the common stock of

Nueces Corp. at $12 per share.

Investment in Affiliates …………………………………………………

31,500

Equity in Affiliate Earnings ………………………………………..

31,500

To record 35% of the net income reported by Nueces Corp.

($90,000 x 35% = $31,500)

December 31:

Cash ………………………………………………………………………….

12,600

Investment in Affiliates ……………………………………………..

12,600

To record 35% of cash dividends paid by Nueces Corp.

(21,000 shares x $.60 = $12,600)

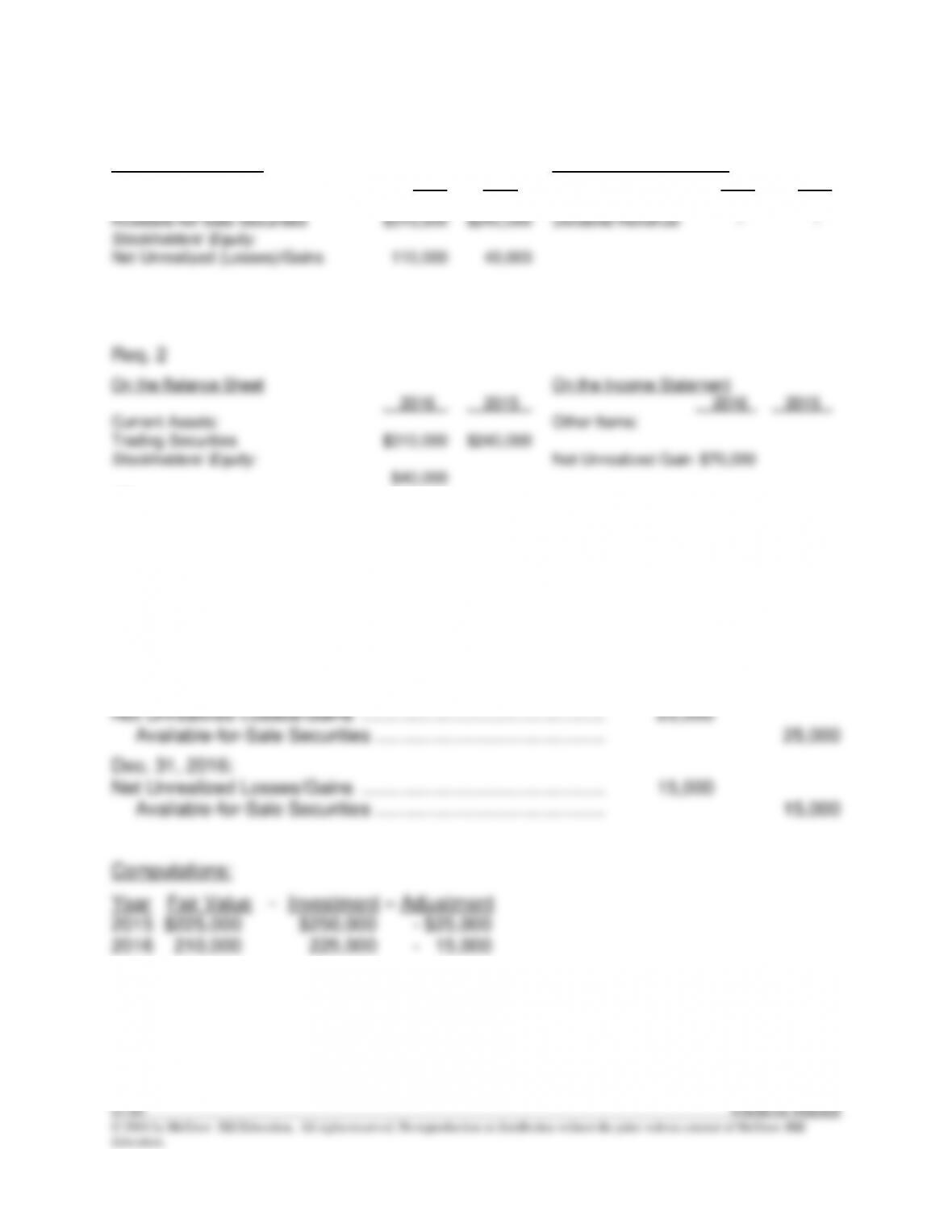

Investments in Affiliates ………………………………………………………………………

Other items:

ED–2

June 30, 2015:

Available-for-Sale Securities …………………………………………

200,000

Cash ……………………………………………………………………..

200,000

Dec. 31, 2015:

Available-for-Sale Securities …………………………………………

40,000

Net Unrealized Losses/Gains ……………………………………

40,000

Dec. 31, 2016:

Available-for-Sale Securities …………………………………………

70,000

Net Unrealized Losses/Gains ……………………………………

70,000

Computations:

Year Fair Value − Investment = Adjustment

2015 $240,000 $200,000 $40,000

2016 310,000 240,000 70,000

ED–3

June 30, 2015:

Trading Securities ……………………………………………………….

200,000

Cash ……………………………………………………………………..

200,000

Dec 31, 2015:

Trading Securities ……………………………………………………….

40,000

Net Unrealized Losses/Gains ……………………………………

40,000

Dec. 31, 2016:

Trading Securities ……………………………………………………….

70,000

Net Unrealized Losses/Gains ……………………………………

70,000

Computations:

Year Fair Value − Investment = Adjustment

2015 $240,000 $200,000 $40,000

2016 310,000 240,000 70,000

ED–4

Req. 1

On the Balance Sheet On the Income Statement

2016 2015 2016 2015

Noncurrent Assets: Other Items:

n/a

ED–5

March 10, 2015:

Available-for-Sale Securities …………………………………………

250,000

Cash ……………………………………………………………………..

250,000

Dec. 31, 2016:

Net Unrealized Losses/Gains ………………………………………..

25,000

Available-for-Sale Securities ……………………………………..

25,000

Dec. 31, 2016:

Net Unrealized Losses/Gains ………………………………………..

15,000

Available-for-Sale Securities ……………………………………..

15,000

Computations:

Year Fair Value − Investment = Adjustment

2015 $225,000 $250,000 – $25,000

2016 210,000 225,000 – 15,000