Handout D–1, continued

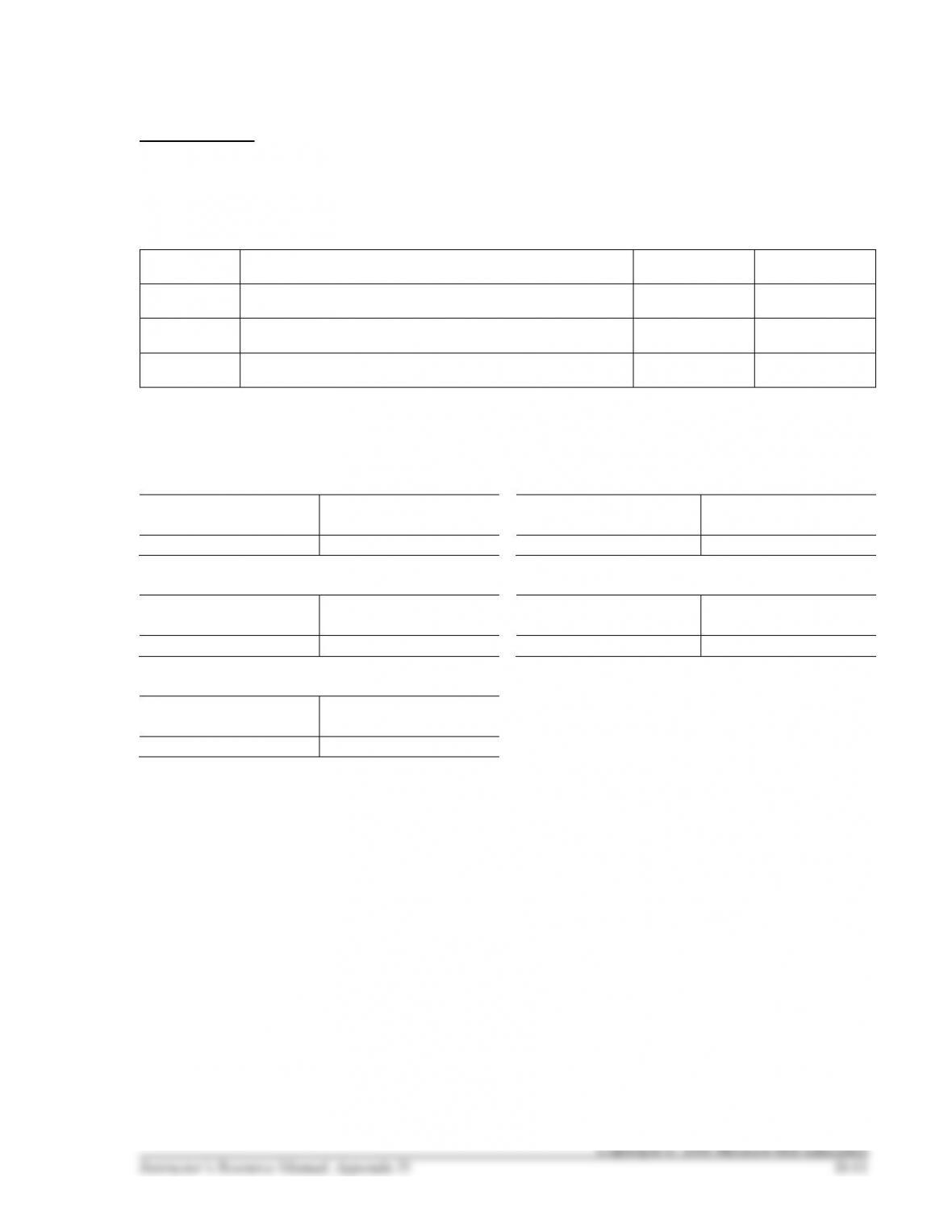

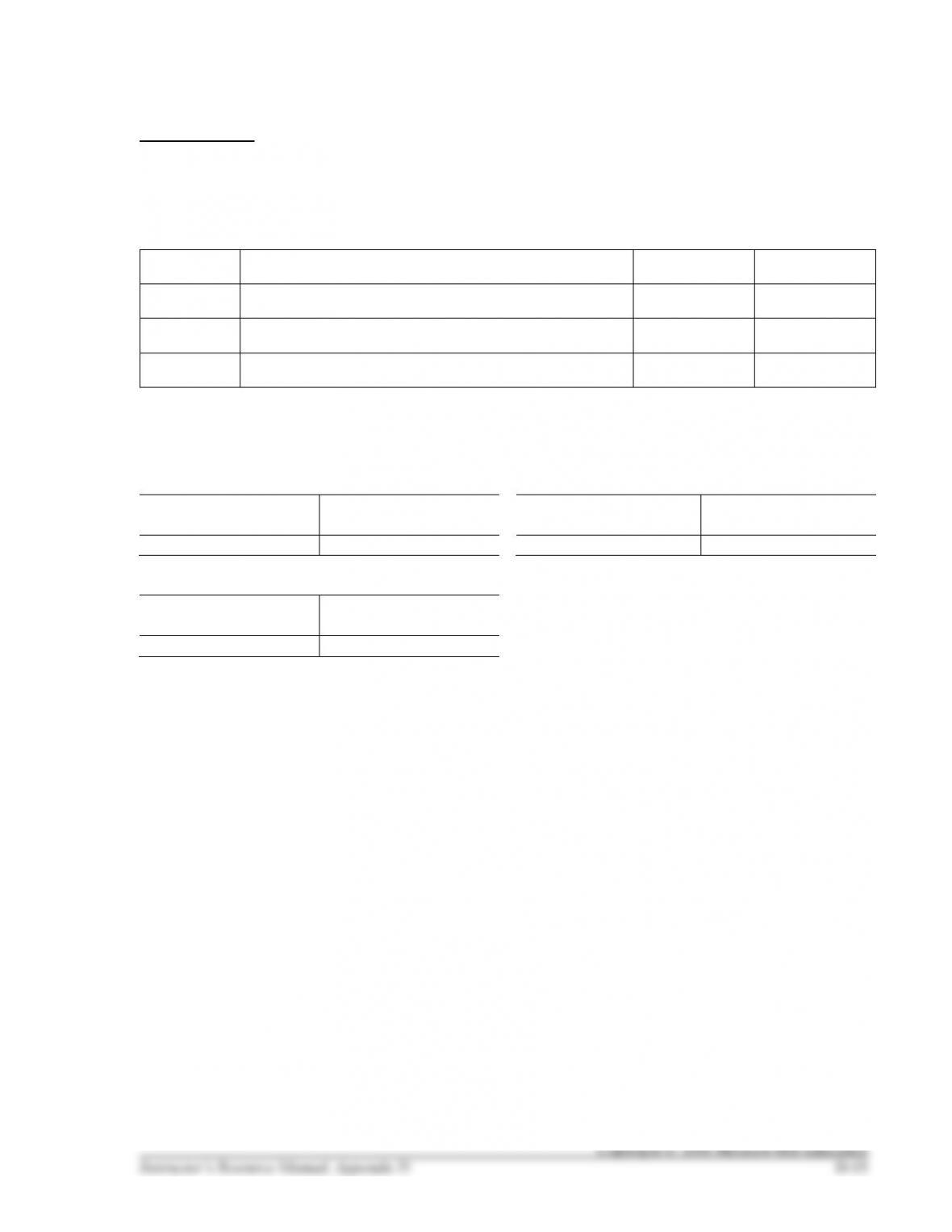

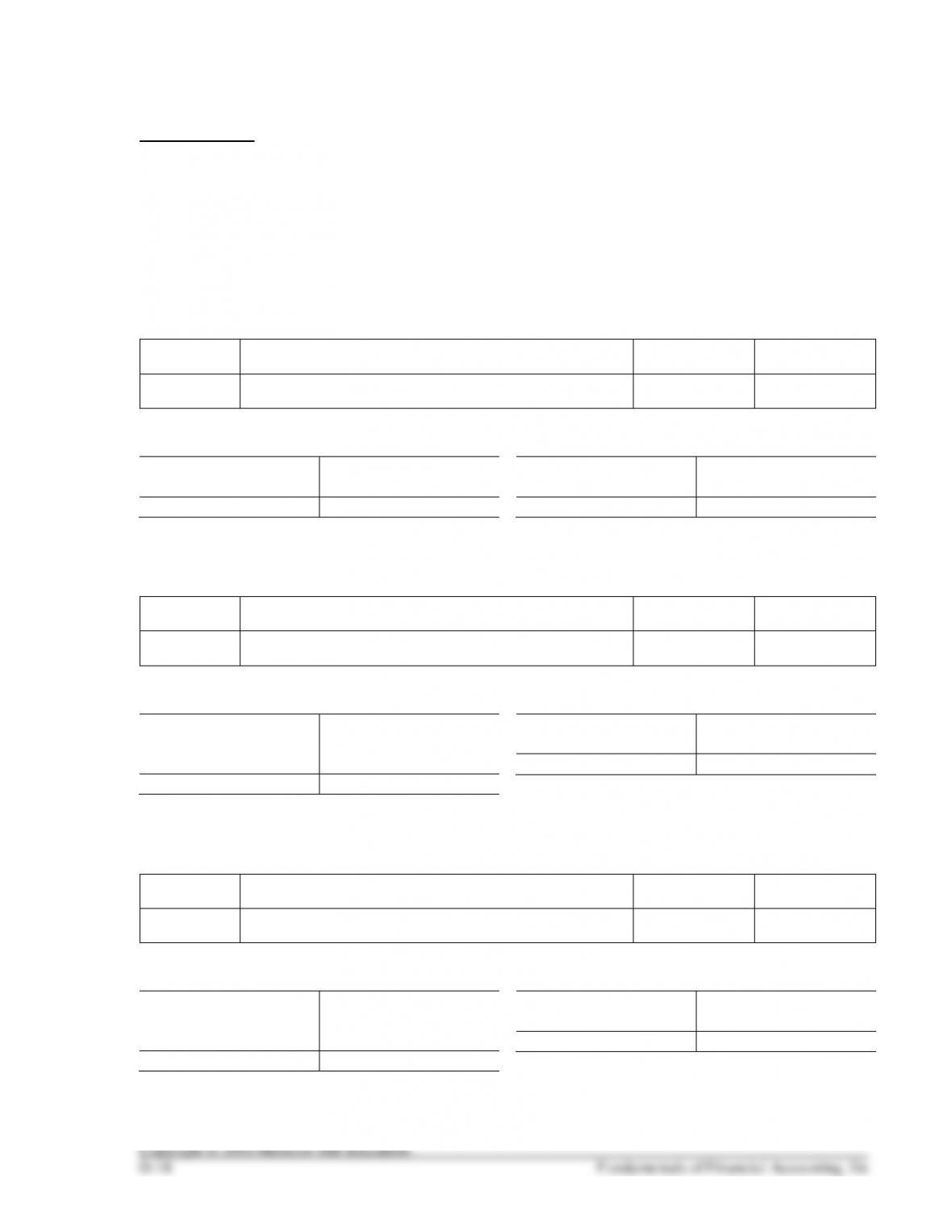

4. At February 17, 2017, Bellows sold the stock for $115 per share. Prepare the journal entry required to

record this transaction and update the appropriate T-accounts:

Feb. 17

2017

Note: Start with the beginning balances as of January 1, 2017 in the T-accounts below.

Handout D–1 Solution

BELLOWS CORP.

1. Bellows Corp. had $100,000 in its Cash account on January 1, 2016. On June 15, 2016, Bellows

Corp. acquired 100 shares of Sonny, Inc. for $75 per share. Assuming that Bellows considers the

stock as a security available for sale, prepare the journal entry required to record this transaction and

post it to the appropriate T-accounts:

June 15

Available-for-Sale Securities (+A)

7,500

Cash (–A)

7,500

+ Available-for-Sale Securities (A) –

June 15

7,500

7,500

+ Cash (A) –

Jan. 1

100,000

7,500

June 15

92,500

2. On September 15, 2016, Bellows Corp. received dividends from Sonny of $2 per share. Prepare the

journal entry required to record this transaction and update the appropriate T-accounts:

Sep. 15

Cash (+A) (100 shares @ $2)

200

Dividend Revenue (+R, +SE)

200

– Dividend Revenue +

200

Sep. 15

200

+ Cash (A) –

Jan. 1

100,000

Sep. 15

200

7,500

June 15

92,700

3. At December 31, 2016, the value of the stock was $120 per share. Prepare the journal entry required

to record this transaction and update the appropriate T-accounts:

Year

Fair Value

–

Balance in

Available-for-Sale Securities Account

=

Amount for Adjusting Entry

2016

$12,000

($120 × 100)

–

7,500

=

4,500

Dec. 31

Available-for-Sale Securities (+A)

4,500

Net Unrealized Losses/Gains (+SE)

4,500

+ Available-for-Sale Securities (A) –

June 15

7,500

Dec. 31

4,500

12,000

– Net Unrealized Losses/Gains (SE) +

4,500

Dec. 31

4,500

Handout D–1 Solution, continued

4. On February 17, 2017, Bellows sold the stock for $115 per share. Prepare the journal entry required

to record this transaction and update the appropriate T-accounts:

Feb. 17

Cash (+A) ($115 × 100)

11,500

2017

Available-for-Sale Securities (–A)

12,000

Gain on Sale of Investments (+R, +SE)

4,000

Net Unrealized Losses/Gains (–SE)

4,500

Note: Start with the beginning balances as of January 1, 2017 in the T-accounts below.

+ Cash (A) –

Jan. 1

92,700

Feb. 17

11,500

104,200

+ Available-for-Sale Securities (A) –

Jan. 1

12,000

12,000

Feb. 17

0

– Gain on Sale of Investments (SE, R) +

4,000

Feb. 17

4,000

– Net Unrealized Losses/Gains (SE) +

4,500

Jan. 1

Feb. 17

4,500

0

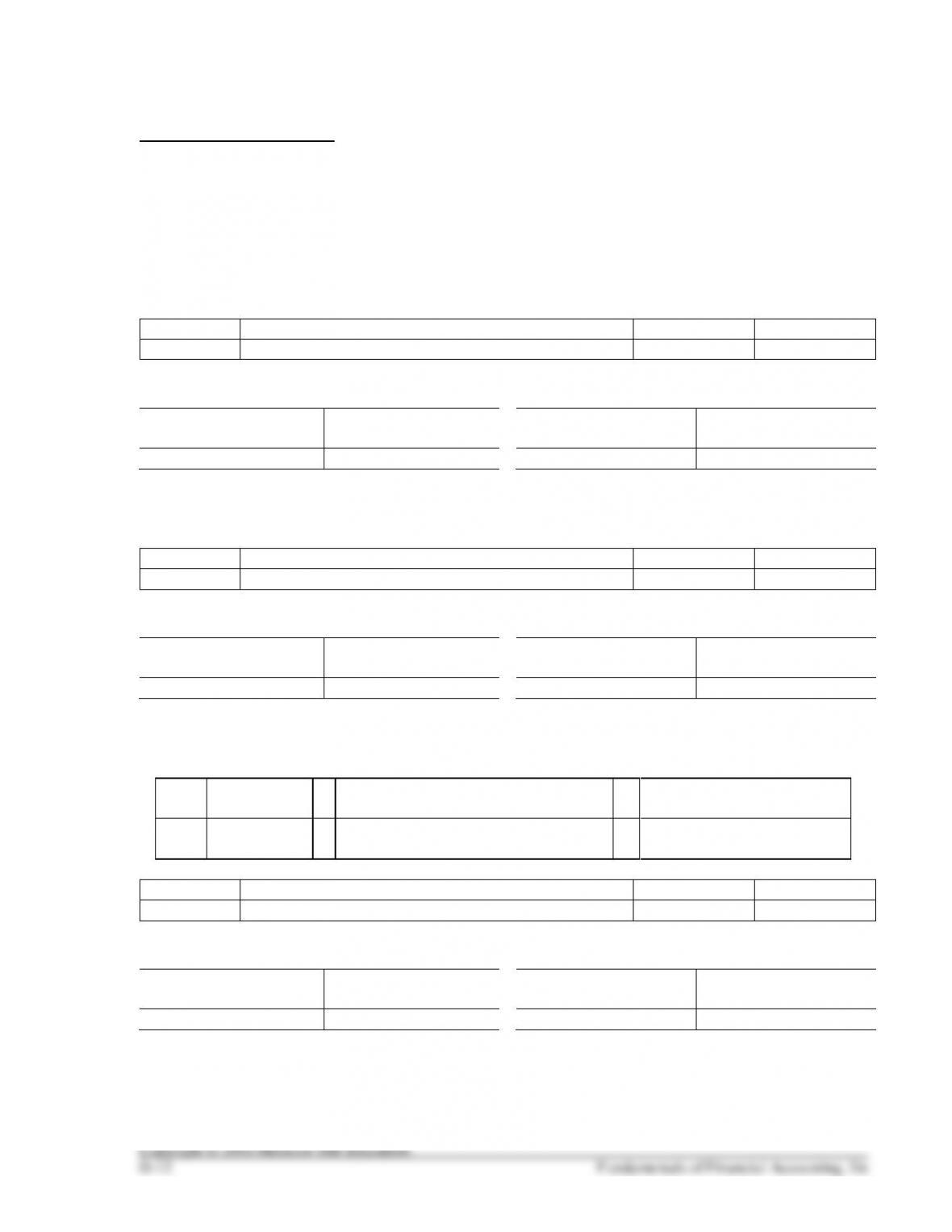

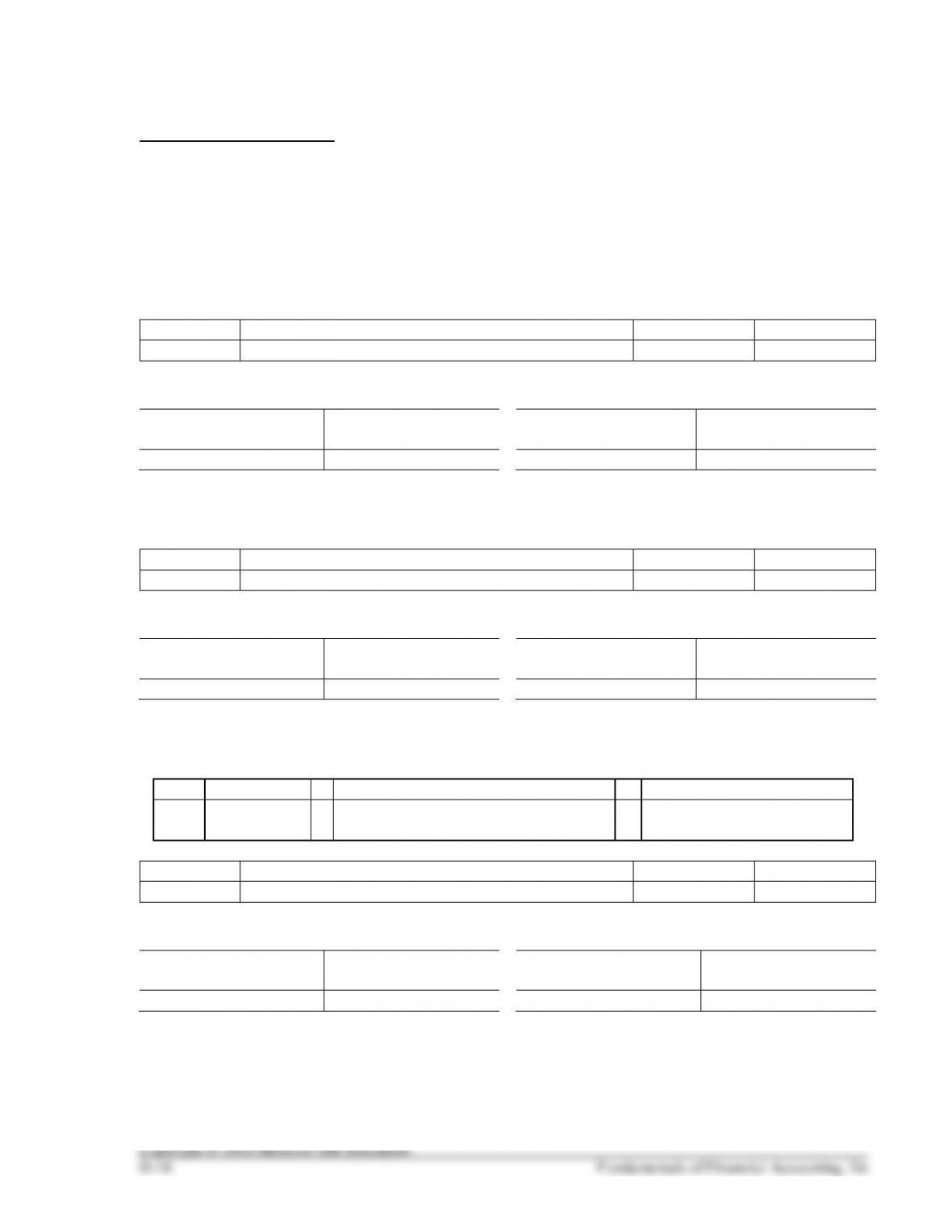

Handout D–2

BAWL CORP.

1. Bellows Corp. had $100,000 in its Cash account on January 1, 2016. On June 15, 2016, Bellows

Corp. acquired 100 shares of Sonny, Inc. for $75 per share. Assuming that Bellows considers the

stock as a trading security, prepare the journal entry required to record this transaction and post it to

the appropriate T-accounts:

June 15

2. On September 15, 2016, Bawl Corp. received dividends from Darkness of $2 per share. Prepare the

journal entry required to record this transaction and update the appropriate T-accounts:

Sept. 15

3. At December 31, 2016, the value of the stock was $120 per share. Prepare the journal entry required

to record this transaction and update the appropriate T-accounts:

Computation of amount:

Dec. 31

Handout D–2, continued

4. At February 17, 2017, Bawl sold the stock for $115 per share. Prepare the journal entry required to

record this transaction and update the appropriate T-accounts:

Feb. 17

2017

Note: Start with the beginning balances as of January 1, 2017 in the T-accounts below.

Handout D–2 Solution

BAWL CORP.

1. Bellows Corp. had $100,000 in its Cash account on January 1, 2016. On June 15, 2016, Bellows

Corp. acquired 100 shares of Sonny, Inc. for $75 per share. Assuming that Bellows considers the

stock as a trading security, prepare the journal entry required to record this transaction and post it to

the appropriate T-accounts:

June 15

Trading Securities (+A)

7,500

Cash (–A)

7,500

+ Trading Securities (A) –

June 15

7,500

7,500

+ Cash (A) –

Jan. 1

100,000

7,500

June 15

92,500

2. On September 15, Bawl Corp. received dividends from Darkness of $2 per share. Prepare the journal

entry required to record this transaction and update the appropriate T-accounts:

Sep. 15

Cash (+A) (100 shares × $2)

200

Dividend Revenue (+R, +SE)

200

– Dividend Revenue +

200

Sep. 15

200

+ Cash (A) –

Jan. 1

100,000

Sep. 15

200

7,500

June 15

92,700

3. At December 31, 2016, the value of the stock was $120 per share. Prepare the journal entry required

to record this transaction and update the appropriate T-accounts:

Year

Fair Value

–

Balance in Trading Securities Account

=

Amount for Adjusting Entry

2016

$12,000

($120 × 100)

–

7,500

=

4,500

Dec. 31

Trading Securities (+A)

4,500

Net Unrealized Losses/Gains (+R,+SE)

4,500

+ Trading Securities (A) –

June 15

7,500

Dec. 31

4,500

12,000

– Net Unrealized Losses/Gains (R, SE) +

4,500

Dec. 31

4,500

Handout D–2 Solution, continued

4. At February 17, 2017, Bawl sold the stock for $115 per share. Prepare the journal entry required to

record this transaction and update the appropriate T-accounts:

Feb. 17

Cash (+A) ($115 × 100)

11,500

2017

Loss on Sale of Investments (+R, +SE)

(11,500 – 7,500 – 4,500)

500

Trading Securities (–A)

12,000

Note: Start with the beginning balances as of January 1, 2017 in the T-accounts below.

+ Cash (A) –

Jan. 1

92,700

Feb. 17

11,500

104,200

+ Trading Securities (A) –

Jan. 1

12,000

12,000

Feb. 17

0

+ Loss on Sale of Investments (+R, +SE) –

Feb. 17

500

500

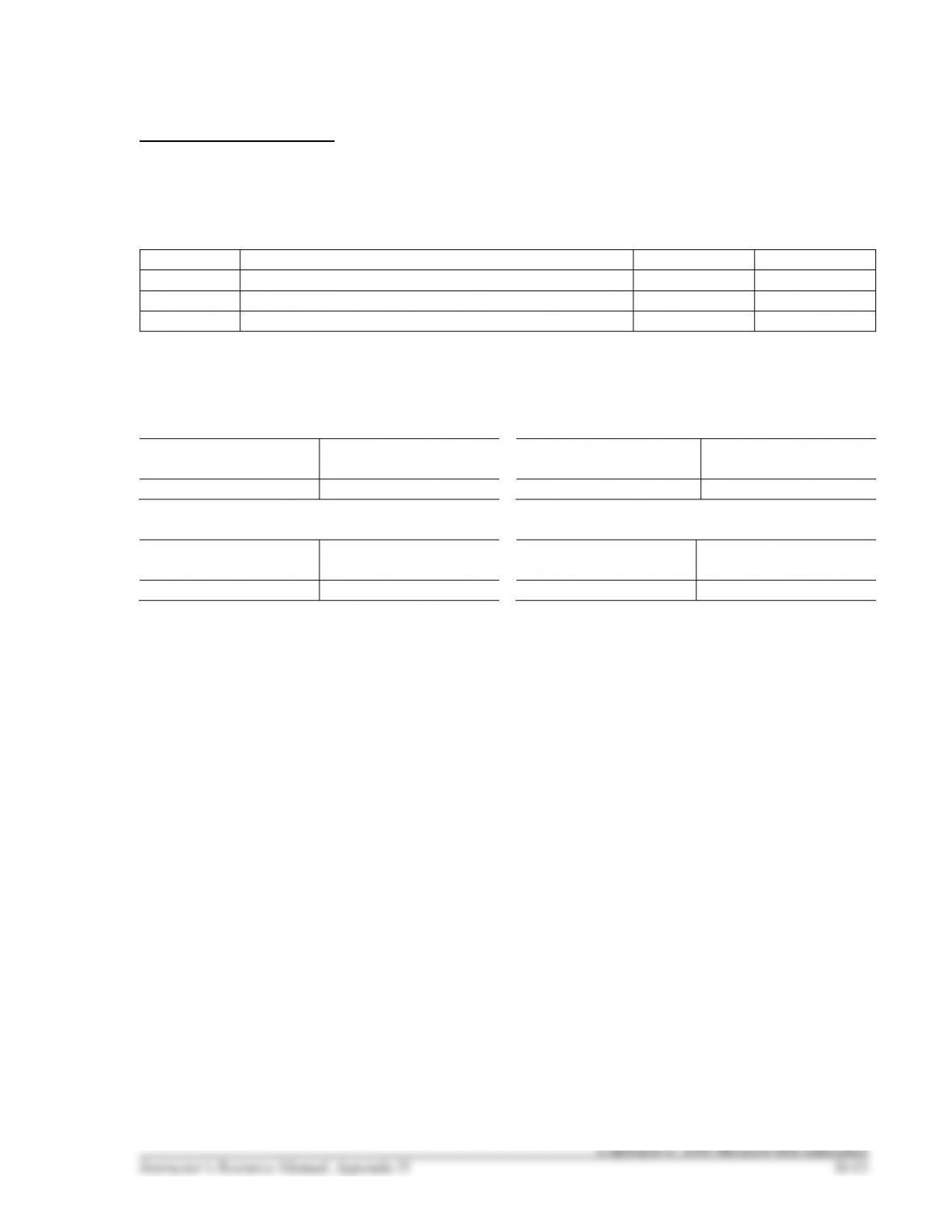

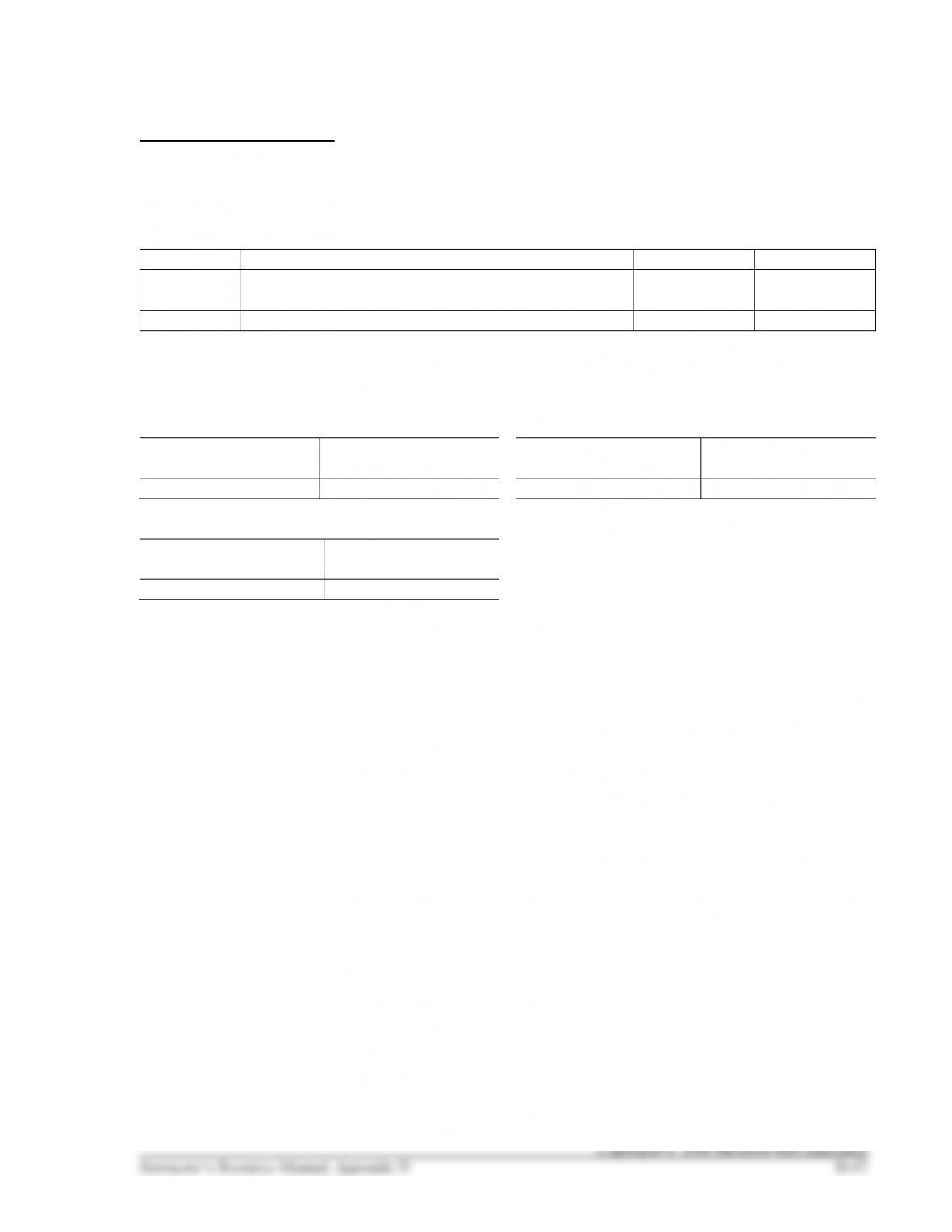

Handout D–3

PARADE CORP.

1. Parade Corp. had $10,000,000 in its Cash account on January 1, 2016. On January 2, 2016, Parade

Corp. paid $5,000,000 cash to acquire 400,000 shares of stock in Band Corp. These shares represent

40% of Band Corp.’s total outstanding stock. Parade accounted for this acquisition using the equity

method. Prepare the journal entry required to record this transaction and, after entering the beginning

Cash account balance, post it to the appropriate T-accounts:

Jan. 2

2. For the year ended December 31, 2016, Band Corp. earned $800,000 in net income. Prepare the

journal entry required to record this transaction and update the appropriate T-accounts:

Dec. 31

3. On December 31, 2016, Band Corp. declared and paid $500,000 in dividends. Prepare the journal

entry required to record this transaction and update the appropriate T-accounts:

Dec. 31

Handout D–3 Solution

PARADE CORP.

1. Parade Corp. had $10,000,000 in its Cash account on January 1, 2016. On January 2, 2016, Parade

Corp. paid $5,000,000 cash to acquire 400,000 shares of stock in Band Corp. These shares represent

40% of Band Corp.’s total outstanding stock. Parade accounted for this acquisition using the equity

method. Prepare the journal entry required to record this transaction and, after entering the beginning

Cash account balance, post it to the appropriate T-accounts:

Jan. 2

Investments in Affiliates (+A)

5,000,000

Cash (-A)

5,000,000

+ Investments in Affiliates (A) –

Jan. 1

0

Jan. 2

5,000,000

5,000,000

+ Cash (A) –

Jan. 1

10,000,000

5,000,000

Jan. 2

5,000,000

2. For the year ended December 31, 2016, Band Corp. earned $800,000 in net income. Prepare the

journal entry required to record this transaction and update the appropriate T-accounts:

Dec. 31

Investments in Affiliates (+A)

320,000

Equity in Affiliate Earnings (+R, +SE)

320,000

$800,000 × 40% = $320,000

+ Investments in Affiliates (A) –

Jan. 1

0

Jan. 2

5,000,000

Dec. 31

320,000

5,320,000

– Equity in Affiliate Earnings (R, SE) +

320,000

Dec. 31

320,000

3. On December 31, 2016, Band Corp. declared and paid $500,000 in dividends. Prepare the journal

entry required to record this transaction and update the appropriate T-accounts:

Dec. 31

Cash (+A)

200,000

Investments in Affiliates (-A)

200,000

$500,000 × 40% = $200,000

+ Investments in Affiliates (A) –

Jan. 1

0

Jan. 2

5,000,000

Dec. 31

320,000

200,000

Dec. 31

End Bal

5,120,000

+ Cash (A) –

Jan. 1

10,000,000

Dec. 31

200,000

5,000,000

Jan. 2

End Bal

5,200,000