Chapter 09 – Reporting and Analyzing Current Liabilities

Exercise 9-10 (15 minutes)

1. B = 0.03 ($500,000 – B)

1.03B = $15,000

2.

2013

Dec. 31 Employee Bonus Expense ………………………….. 14,563

3.

2014

Jan. 19 Bonus Payable ……………………………………………. 14,563

Exercise 9-11 (10 minutes)

1.

Vacation Benefits Expense …………………………………....

3,200

Vacation Benefits Payable ………………………………..

3,200

To record vacation benefits expense

[20 employees x 1 day x $160].

2.

Warranty Expense………………………………………………....

18,000

Estimated Warranty Liability …………………………....

18,000

To record warranty expense [12,000 units x 10% x $15].

Exercise 9-12 (15 minutes)

(a)

(b)

(c)

(d)

(e)

(f)

Numerator

Income before

interest & taxes ….

$194,000

$176,000

$182,000

$379,000

$103,000

$ 5,000

Denominator

Interest expense …...

$ 44,000

$ 16,000

$ 12,000

$ 14,000

$ 14,000

$10,000

Ratio ………………….

4.41

11.00

15.17

27.07

7.36

0.50

Analysis: Company (d) has the strongest ability to pay interest expense as it

comes due as evidenced by the company’s times interest earned (coverage)

ratio of 27.07 times.

Exercise 9-13B (25 minutes)

1.

Income Taxes Payable (target balance) ……………………………….……….

$28,300

Total accrued [($28,600 + $19,100 + $34,600) x .30] ……………………….

24,690

Adjustment (additional expense) ………………………………………………….

$ 3,610

2.

2013

(a)

Dec. 31

Income Tax Expense …………………………………………

3,610

Income Taxes Payable …………………………………

3,610

To adjust tax expense and liability.

2014

(b)

Jan. 20

Income Taxes Payable ………………………………………

28,300

Cash ……………………………………………………………

28,300

To make the final quarterly payment

of income taxes for 2013.

Exercise 9-14A (15 minutes)

Regular pay (40 hours @ $14) …………………………………....

$560.00

Overtime premium pay (8 hours @ [$14 x 150%]) ………..

168.00

Gross pay ………………………………………………………………..

728.00

FICA—Social Security tax deduction (6.2%) ………………..

$ 45.14

FICA—Medicare tax deduction (1.45%) ……………………....

10.56

Income tax deduction (from Exhibit 9A.6) …………………...

76.00

Total deductions ……………………………………………………...

131.70

Net pay ……………………………………………………………………...

$596.30

Exercise 9-16 (30 minutes)

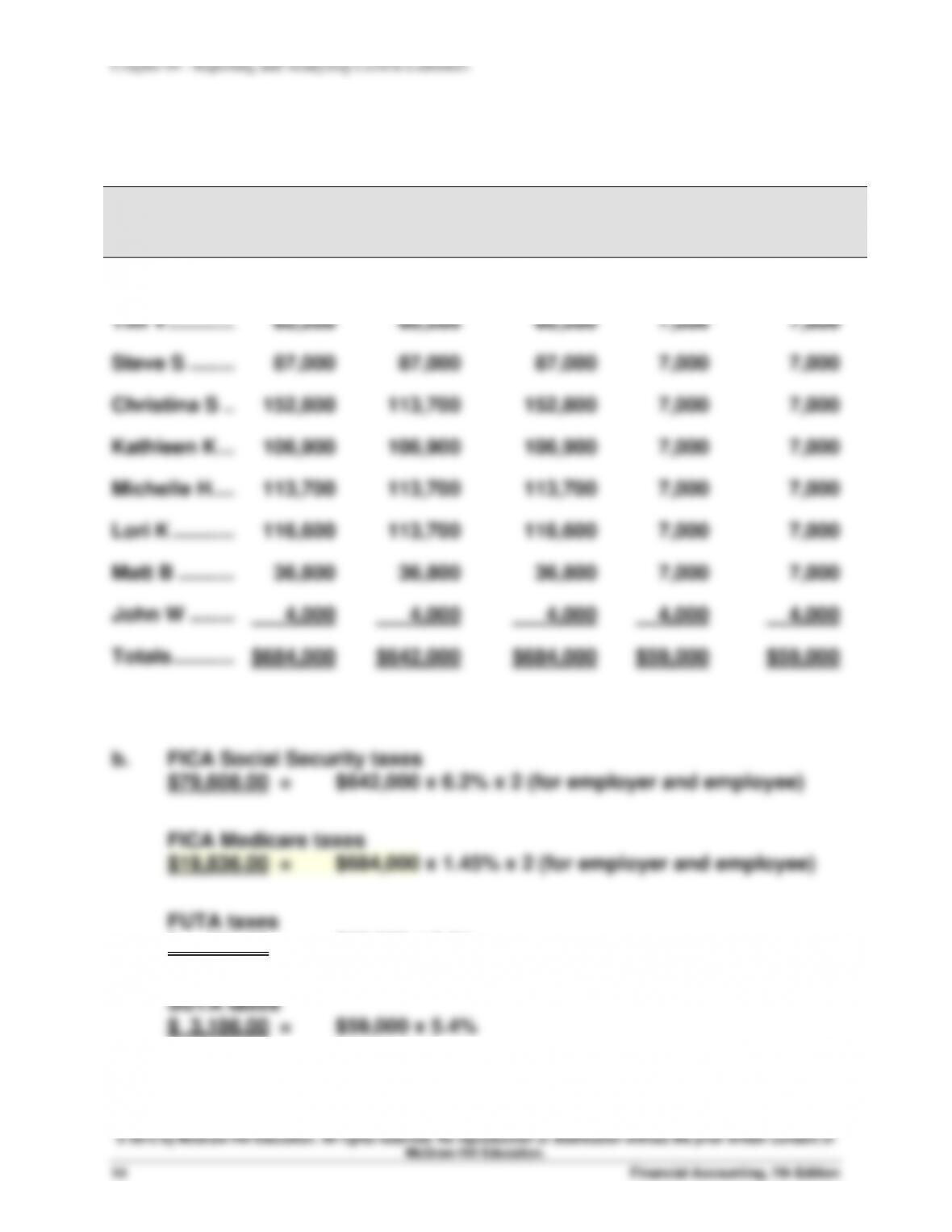

a.

Employee

Cumulative

Pay

Pay Subject to

FICA Social

Security

Pay Subject

to FICA

Medicare

Pay Subject

to FUTA

Taxes

Pay Subject

to SUTA

Taxes

Ken S ………..……..

$ 6,000

$ 6,000

$ 6,000

$ 6,000

$ 6,000

Tim V ………………..

60,200

60,200

60,200

7,000

7,000

Steve S ……..……..

87,000

87,000

87,000

7,000

7,000

Christina S ..……..

152,800

113,700

152,800

7,000

7,000

Kathleen K ………..

106,900

106,900

106,900

7,000

7,000

Michelle H ….……..

113,700

113,700

113,700

7,000

7,000

Lori K ………..……..

116,600

113,700

116,600

7,000

7,000

Matt B ……….……..

36,800

36,800

36,800

7,000

7,000

John W ……..……..

4,000

4,000

4,000

4,000

4,000

Totals ………..……..

$684,000

$642,000

$684,000

$59,000

$59,000

$ 354.00 = $59,000 x 0.6%

Exercise 9-17 (concluded)

(b)

Aug 31

Salaries (or Wages) Expense …………………………..

10,020.00

FICA—Social Sec. Taxes Payable ………….…….

298.84

FICA—Medicare Taxes Payable ……………..…….

145.29

Employee Fed. Inc. Taxes Payable ……………….

2,380.00

Employee State Inc. Taxes Payable ……….…….

388.00

Employee Benefits Plan Payable ………………….

501.00

Salaries Payable ………………………………………….

6,306.87

To record payroll for period.

6,306.87

To record payment of payroll.

Aug 31

298.84

145.29

Federal Unemployment Taxes Payable ….…….

State Unemployment Taxes Payable…………….

Aug 31

Employee Benefits Plan Payable ………………….

1,002.00

To record costs of employee benefits.

Employee Benefits Plan Payable ……………………….

Cash …………………………………………………….…

© 2015 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Financial Accounting, 7th Edition

18

Problem 9-1A (45 minutes)

Locust

Natl. Bank

Fargo

1.

Maturity dates

Date of the note …………………………

May 19

July 8

Nov. 28

Term of the note (in days) …….……

90

120

60

Maturity date ………………………..…

Aug. 17

Nov. 5

Jan. 27

2.

Interest due at maturity

Principal of the note …………….……

$35,000

$80,000

$42,000

Annual interest rate ……………..……

10%

9%

8%

Fraction of year …………………………

90/360

120/360

60/360

Interest expense…………………..……

$ 875

$ 2,400

$ 560

3.

Accrued interest on Fargo note at the end of 2012

Total interest for note …………………………………………….

$ 560

Fraction of term in 2012 …………………………………………

33/60

Accrued interest expense ………………………………………

$ 308

4.

Interest on Fargo note in 2013

Total interest for note …………………………………………….

$ 560

Fraction of term in 2013 …………………………………………

27/60

Interest expense in 2013 ………………………………………..

$ 252

Problem 9-2A (60 minutes)

1. Each employee’s FICA withholdings for Social Security

Dahlia

Trey

Kiesha

Chee

Total

Maximum base …………

$113,700

$113,700

$113,700

$113,700

Earned through 8/18 …

112,600

112,800

7,100

1,050

Amount subject to tax

$ 1,100

$ 900

$106,600

$112,650

Earned this week ………

$ 2,000

$ 900

$ 450

$ 400

Subject to tax ……………

1,100

900

450

400

Tax rate ……………………

6.20%

6.20%

6.20%

6.20%

Social Security tax ……

$ 68.20

$ 55.80

$ 27.90

$ 24.80

$176.70

2. Each employee’s FICA withholdings for Medicare (no limits)

Dahlia

Trey

Kiesha

Chee

Total

Earned this week ………

$ 2,000

$ 900

$ 450

$ 400

Tax rate ……………………

1.45%

1.45%

1.45%

1.45%

Medicare tax …………….

$ 29.00

$ 13.05

$ 6.53

$ 5.80

$ 54.38

3. Employer’s FICA taxes for Social Security

Dahlia

Trey

Kiesha

Chee

Total

Amount from part 1 …..

$ 68.20

$ 55.80

$ 27.90

$ 24.80

$176.70

4. Employer’s FICA taxes for Medicare

Dahlia

Trey

Kiesha

Chee

Total

Amount from part 2 …..

$ 29.00

$ 13.05

$ 6.53

$ 5.80

$ 54.38