Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-8

Chapter Outline

4. Adjusting Entries From A Bank Reconciliation: A bank

reconciliation often identifies unrecorded items that need

recording. Only the items reconciling the book balance require

adjustment.

a. All reconciling additions to book balance are debits to

cash. Credit depends on reason for addition.

Notes

b. All reconciling subtractions from book balance are credits

to cash. Debit depends on reason for subtraction.

IV. Global View

A. Internal Control Purposes, Principles and Procedures – both

GAAP and IFRS aim for high quality reporting. The purposes and

principles of internal control systems are fundamentally the same

across the globe.

B. Control of Cash – Accounting definitions for cash are similar for

GAAP and IFRS and the basic techniques explained in this chapter are

part of those control procedures.

C. Banking Activities as Controls – Companies utilize banking services

as part of their effective control procedures and bank statements are

used along with bank reconciliations to control and monitor cash.

V. Decision Analysis – Days’ Sales Uncollected

A. One measure of the receivables’ nearness to cash is the days’ sales

uncollected ratio (also called days’ sales in receivables).

B. It is calculated by dividing accounts receivable by net sales and

multiplying the result by 365.

C. It is used to estimate how much time is likely to pass before the

current amount of accounts receivable is received in cash.

VI. Documentation and Verification (Appendix 6A)

A. Purchase Requisition

B. Purchase Order

C. Invoice

D. Receiving Report

E. Invoice Approval

F. Voucher

VII. Controls of Purchase Discounts (Appendix 6B)

It is very important for a company to take advantage of purchases

discounts.

A. Recording inventory purchases using net method provides more

control than the gross method, which was described in Chapter 4.

B. The gross method of recording purchases initially records the

invoice at its gross amount ignoring any cash discount.

C. The net method records the invoice at its net amount of any cash

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-9

Chapter Outline

discount. The net method gives management an advantage in

controlling and monitoring cash payments involving purchase

discounts. Any discounts not taken advantage of are recorded in a

Discounts Lost expense account. Entries to record the:

1. Purchase of inventory on credit: debit Merchandise Inventory,

credit Accounts Payable (for the amount of the invoice net of

the discount).

2. Payment of the invoice within the discount period: debit

Accounts Payable, credit Cash (for the amount of the invoice

net of the discount).

3. Payment of the invoice after the discount period has expired:

a. As of the date corresponding to the end of the discount

period: debit Discounts Lost, credit Accounts Payable (for

the amount of the discount).

b. As of the date of payment: debit Accounts Payable, credit

Cash for amount of the payment, gross invoice amount.

Notes

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-10

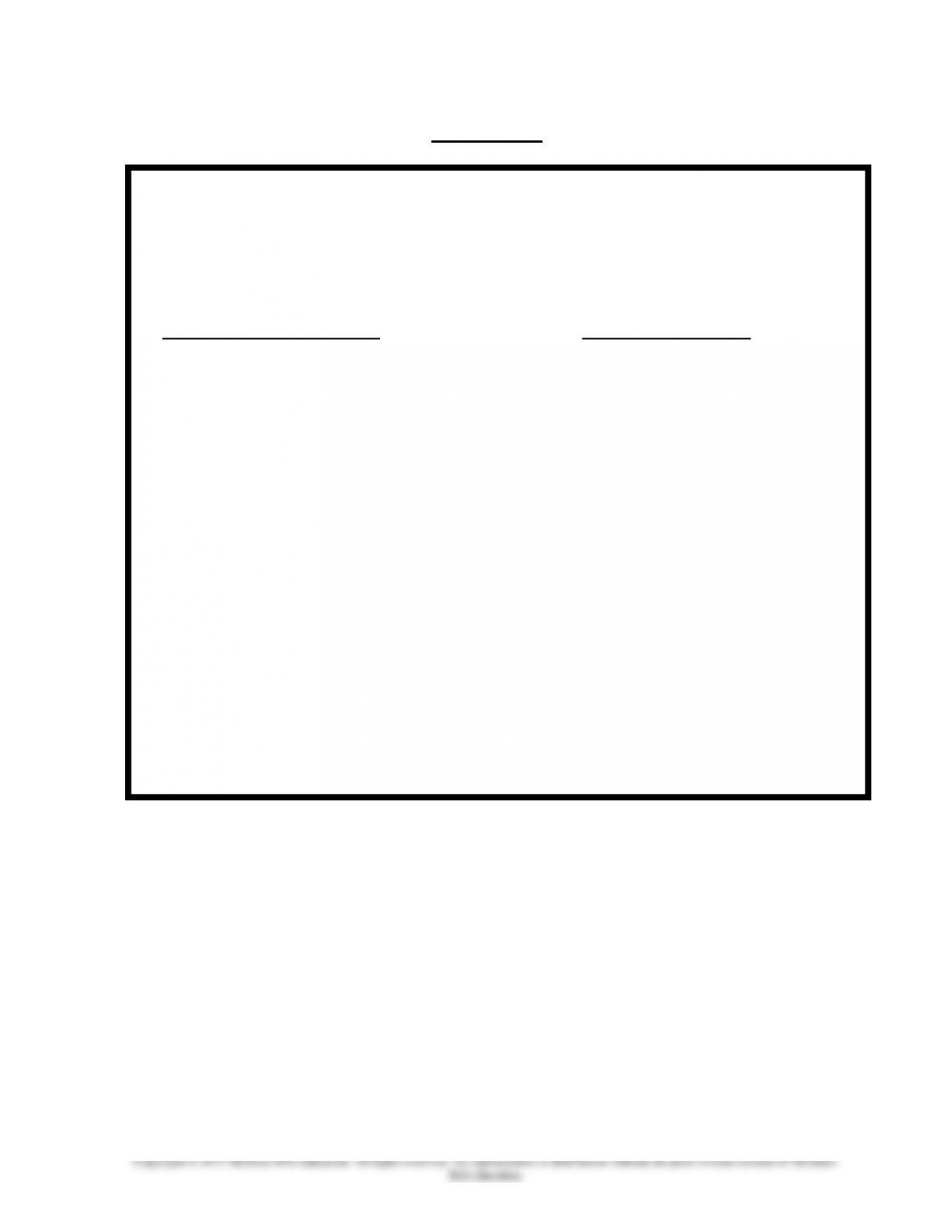

VISUAL #6-1

BANK RECONCILIATION

Reasons for differences

between bank statement

and checkbook balance: Handle as follows:

Unrecorded deposits Add to Bank Balance

Outstanding checks Deduct from Bank Balance

Bank service charges Deduct from Book Balance

Debit memos Deduct from Book Balance

Credit memos Add to Book Balance

NSF checks Deduct from Book Balance

Interest Add to Book Balance

Errors Must analyze individually

(bank errors affect bank

balance and book errors

affect book balance)

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-11

Chapter 6 – Alternate Demonstration Problem #1

The Betsy Dough Company wants to prepare a bank reconciliation for

the month of June. When the bank statement for the month of June

arrives from the bank, the following steps are performed:

1. The deposits to the bank account, as recorded on the bank statement,

are compared to the deposit slips retained by the company. It is noted

that the last deposit, of $400, occurred after banking hours on the day

of the bank statement and therefore has not been recorded by the

bank on this bank statement.

2. Checks returned with the bank statement are compared to the checks

written and listed in checkbook. This comparison shows that there

are checks outstanding amounting to $1,456.

3. The ending balances on the statement and in the company’s books

are determined. The ending bank statement balance is exactly $10,129

whereas the books show $9,000.

4. Other information contained on the bank statement, not previously

known to the company, is determined. This includes the following: (a)

a note from a customer for $200 has been collected by the bank and

credited to our account; (b) a check from Frank Ony for $120

previously deposited by us has been returned for lack of sufficient

funds; (c) the bank has charged us $25 for its services (this includes

a $10 fee for the NSF check).

5. A bank reconciliation is prepared; it does not balance! The difference

is $18, so a transposition error is looked for (whenever the difference

is a multiple of 9, there is a very good chance that there has been an

inadvertent exchange of two digits (for example, writing 29 when it

should have been 92)). An error is found. Check number 141 was

written for $235 and cleared the bank for $235, but was recorded in

the company records as $253.

Required:

Prepare a bank reconciliation for the Betsy Dough Company at June 30,

2013.

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-12

Solution: Chapter 6 – Alternate Demonstration Problem #1

BETSY DOUGH COMPANY

Bank Reconciliation

June 30, 2013

Bank Statement

Bank statement balance ………………………………………

$10,129

Add:

Deposit of June 30 ……………………………………..

400

10,529

Deduct:

Outstanding checks ……………………………………

1,456

Adjusted bank balance

$ 9,073

Depositor’s Books

Book balance ……………………………………………………..

$ 9,000

Add:

Collection of customer note ……………………….

200

Error in recording Check No. 141 ………………..

18

9,218

Deduct:

NSF check from Frank Ony …………………………

$ 120

Bank service charges …………………………………

25

145

Adjusted bank book balance

$ 9,073

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-13

Chapter 6 – Alternate Demonstration Problem #2

On January 1, Landen Company established a petty cash fund in the

amount of $200. During the month, the following petty cash transactions

occurred:

Delivery expense: $35

Supplies expense: $70

Miscellaneous expense: $10

At the end of the month, $83 was left in the petty cash fund.

Prepare the general journal entries to record:

1. Establishment of the fund

2. Reimbursement of the fund

Chapter 06 – Reporting and Analyzing Cash and Internal Controls

6-14

Solution: Chapter 6 – Alternate Demonstration Problem #2

1. Petty cash 200

Cash 200

2. Delivery expense 35

Supplies expense 70

Miscellaneous expense 10

Cash over and short 2

Cash 117