Chapter 05 – Reporting and Analyzing Inventories

Teamwork in Action (Continued)

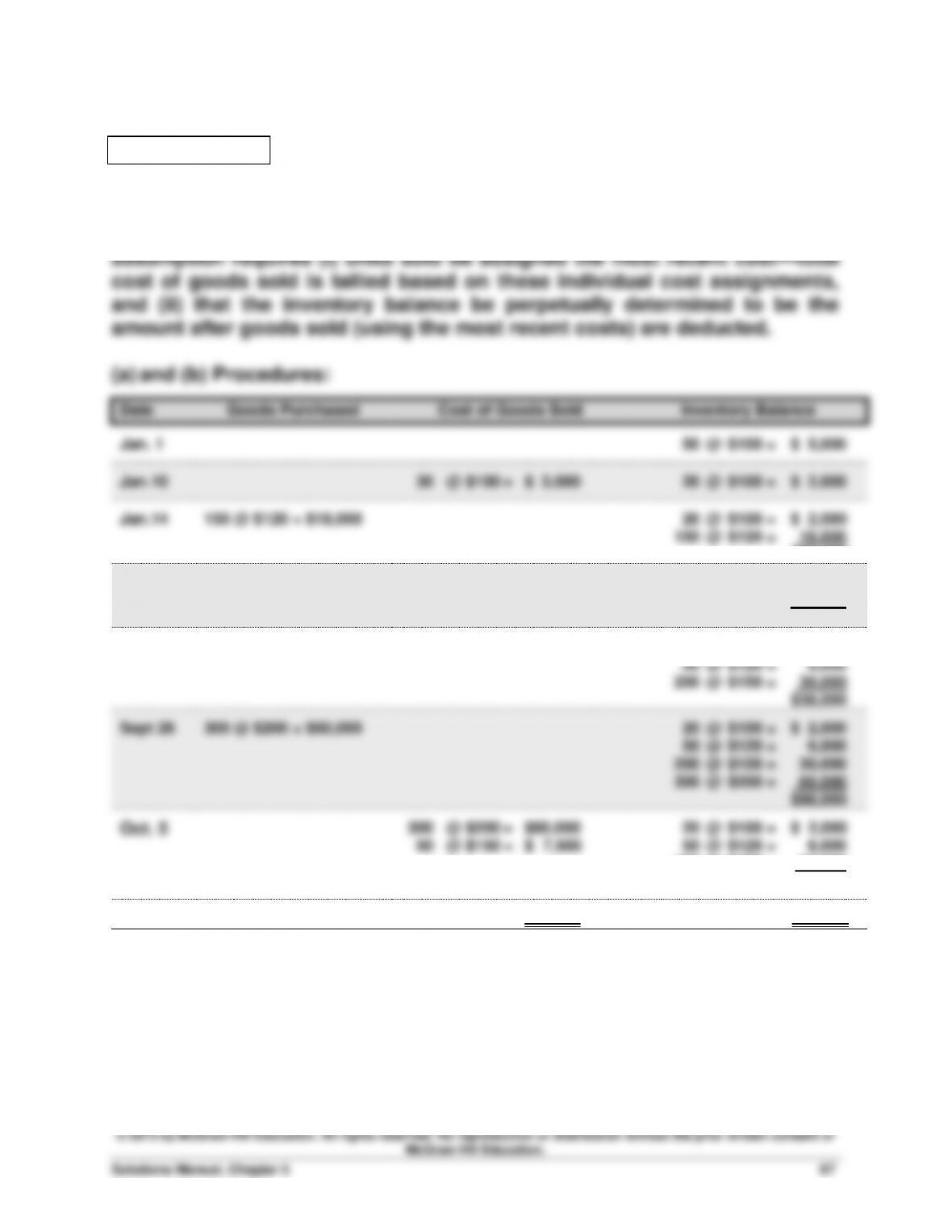

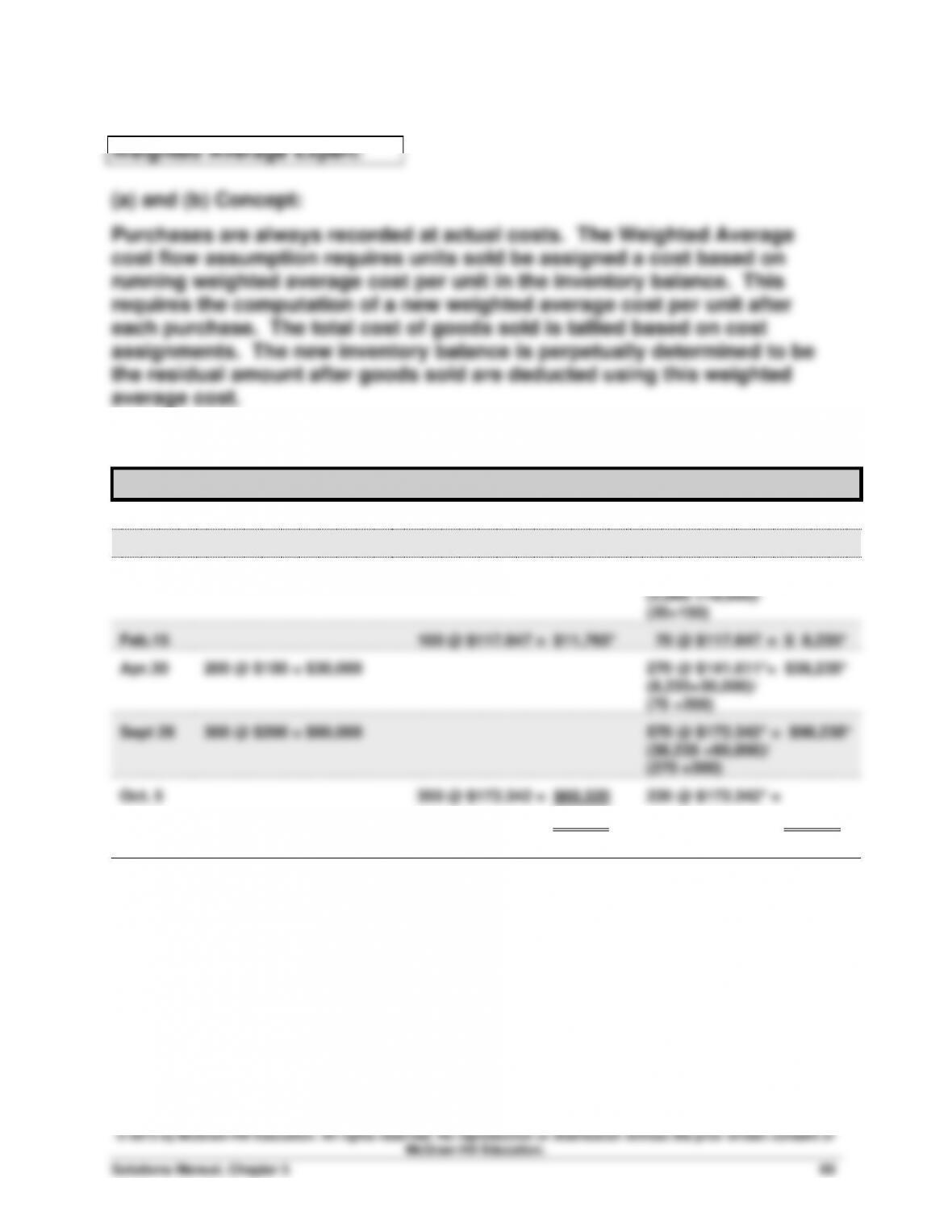

LIFO Expert:

(a) and (b) Concept:

Purchases are always recorded at actual costs. The LIFO cost flow

Chapter 05 – Reporting and Analyzing Inventories

Teamwork in Action (Continued)

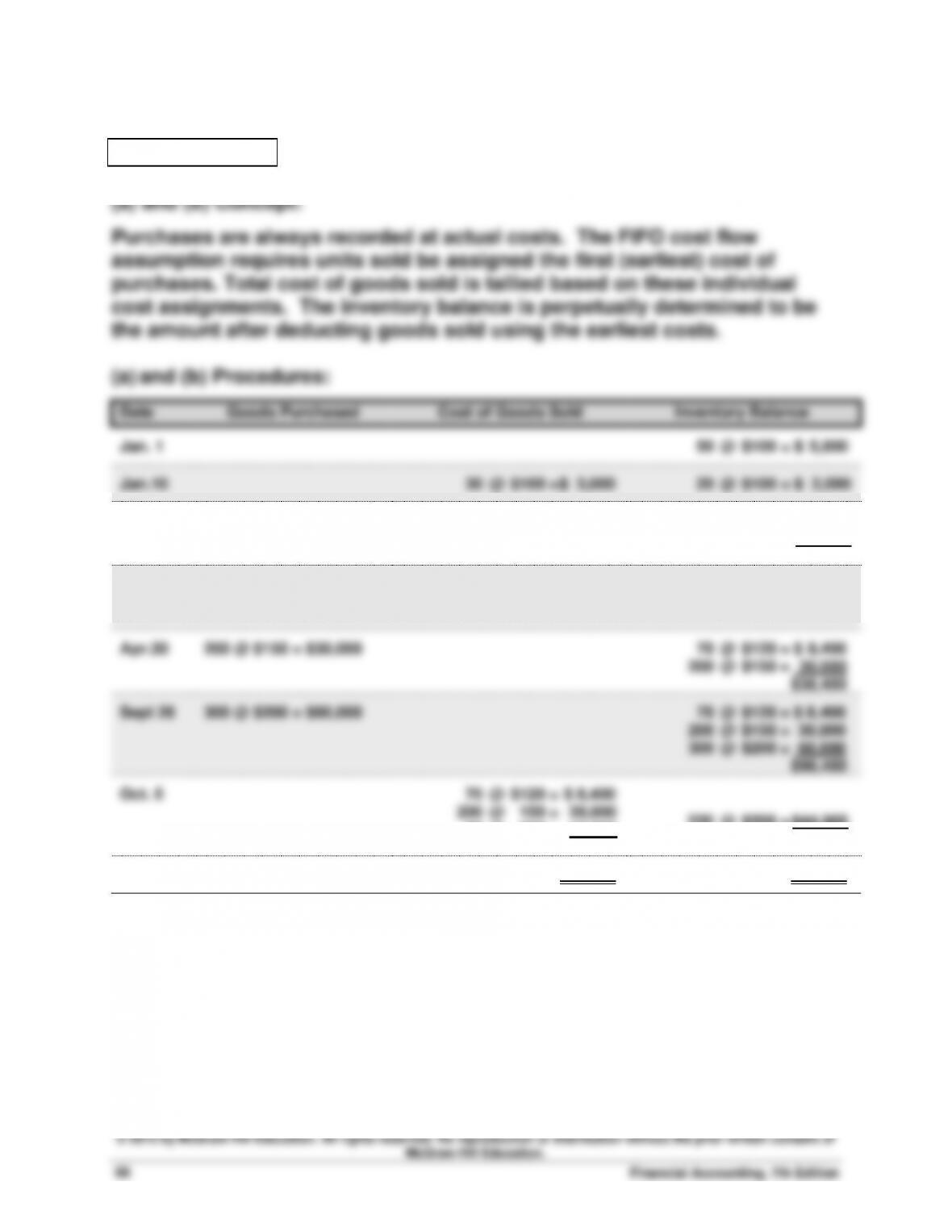

FIFO Expert:

Chapter 05 – Reporting and Analyzing Inventories

Teamwork in Action (Continued)

(a) and (b) Procedures:

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Jan. 1

50 @ $100 = $ 5,000

Jan.10

30 @ $100 = $ 3,000

20 @ $100 = $ 2,000

Jan.14

150 @ $120 = $18,000

170 @ $117.647 = $20,000

(2,000 +18,000)/

(20+150)

Feb.15

100 @ $117.647 = $11,765*

70 @ $117.647 = $ 8,235*

Apr.30

200 @ $150 = $30,000

270 @ $141.611*= $38,235*

(8,235+30,000)/

(70 +200)

Sept 26

300 @ $200 = $60,000

570 @ $172.342* = $98,235*

(38,235 +60,000)/

(270 +300)

Oct. 5

350 @ $172.342 = $60,320

220 @ $172.342* =

$75,085

$37,915**

* rounded ** adjusted for rounding

Chapter 05 – Reporting and Analyzing Inventories

Teamwork in Action (Concluded)

homogeneous goods.

FIFO—Most businesses try to move their older or earlier acquired inventory

first, particularly if they sell perishable goods. Therefore, FIFO will frequently

reflect the physical flow of goods.

LIFO—Few actually sell their most recently acquired inventory first. This

LIFO must be used for financial reporting if it is used for tax purposes.

In a period of rising prices FIFO will generally result in the lowest cost of

goods sold and therefore the highest net income and highest tax.

Weighted Average will usually result in a reported net income and tax

consequences somewhere in between LIFO and FIFO.

© 2015 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Financial Accounting, 7th Edition

72

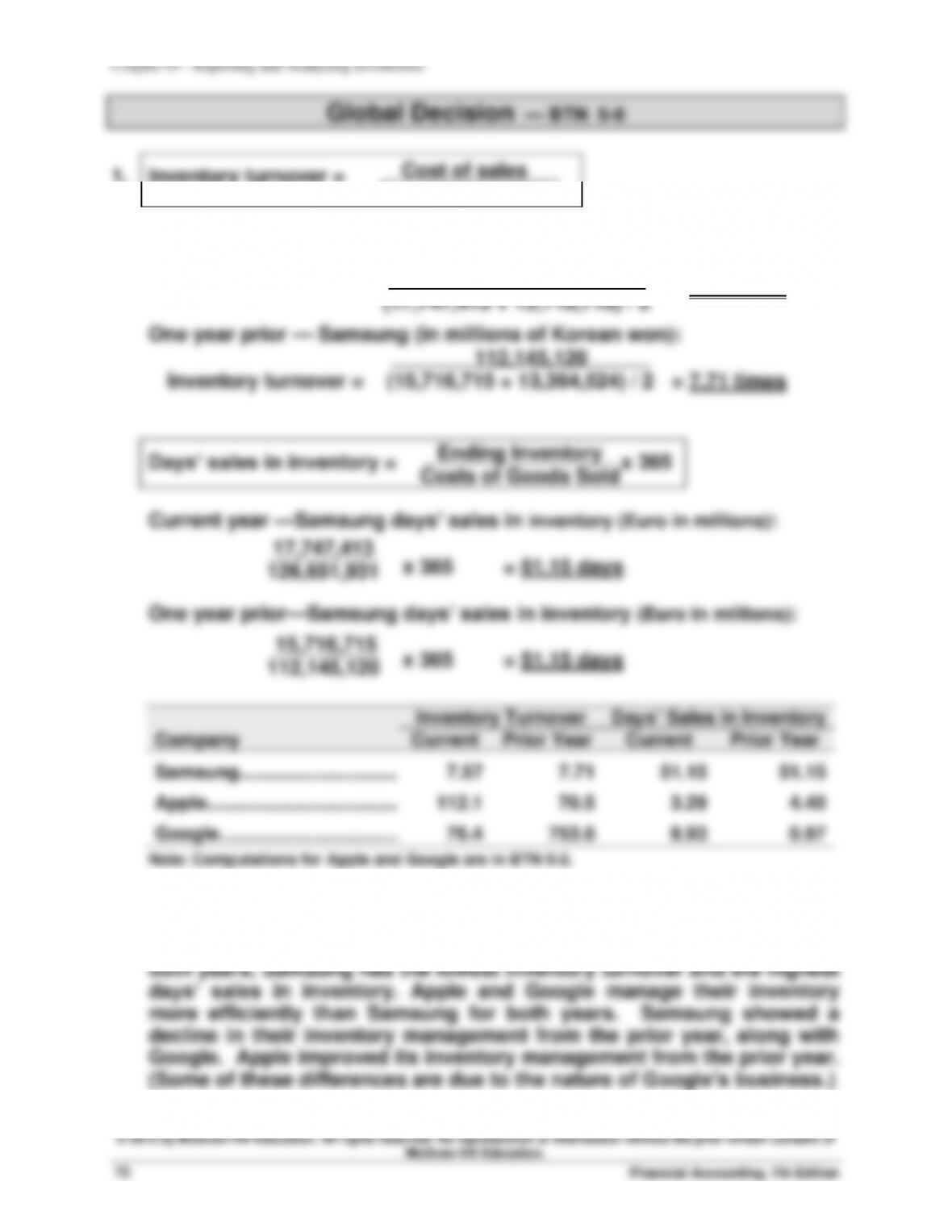

1. Inventory turnover =

Current year — Samsung (in millions of Korean won):

Inventory turnover = = 7.57 times

2. For the current year, Apple has the highest inventory turnover and the

lowest days’ sales in inventory. For the prior year, Google has the

highest inventory turnover and lowest days’ sales in inventory. For

Cost of sales

Average inventory

126,651,931

(17,747,413 + 15,716,715) / 2