Chapter 10 – Reporting and Analyzing Long-Term Liabilities

Problem 10-6B (60 minutes)

Part 1

2013

Jan. 1

Cash …………………………………………………….…

198,494

Discount on Bonds Payable ………………….……….

41,506

Bonds Payable ………………………………..……………….

240,000

Sold bonds on stated issue date.

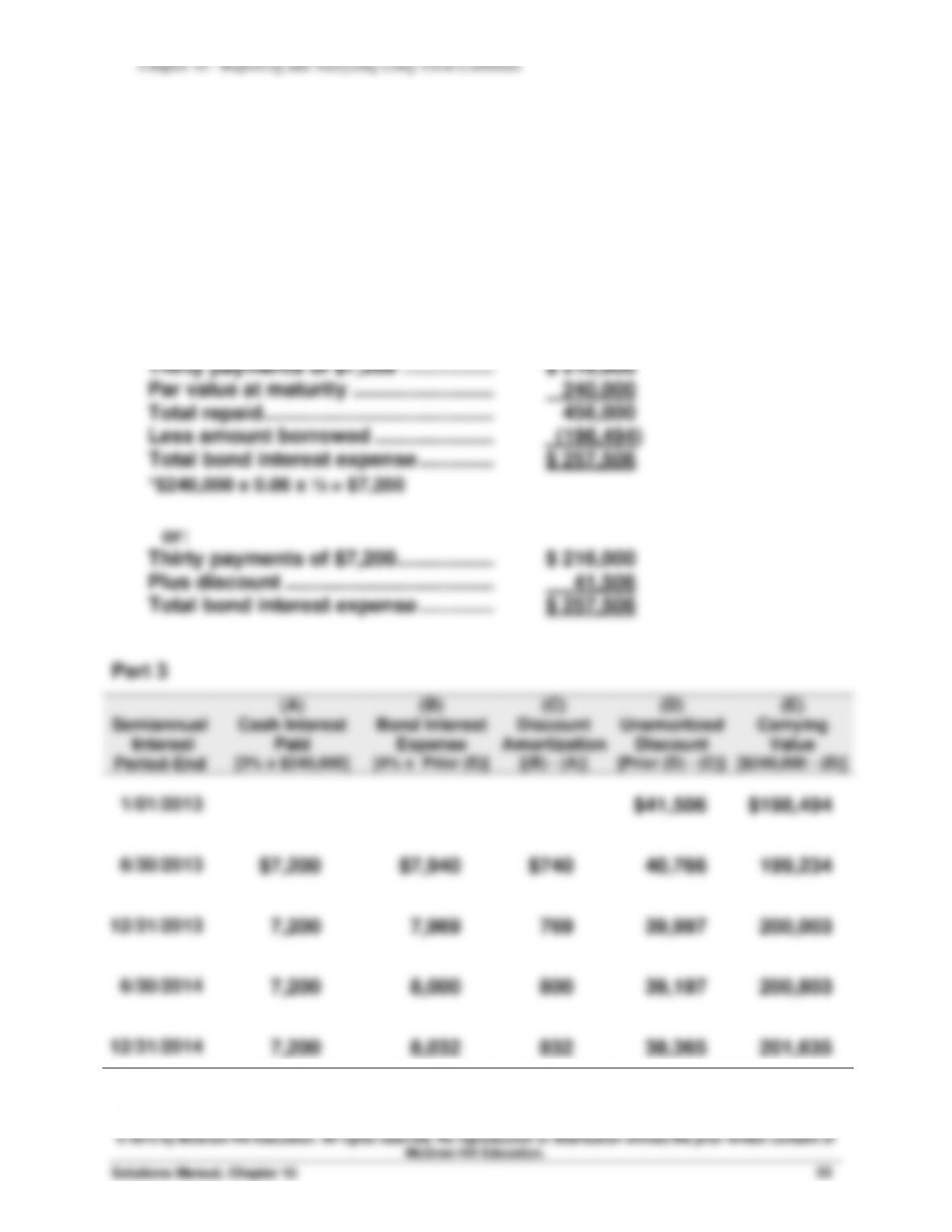

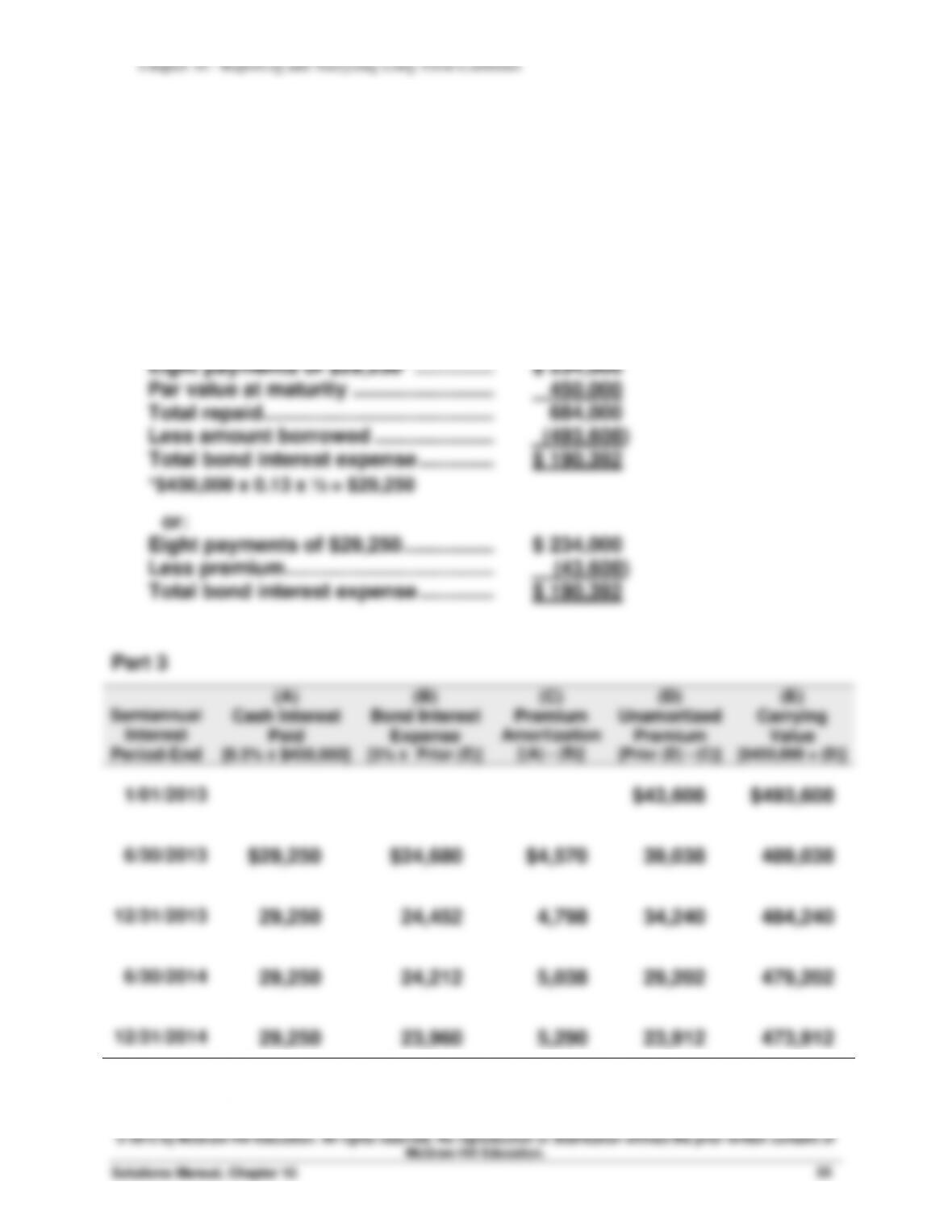

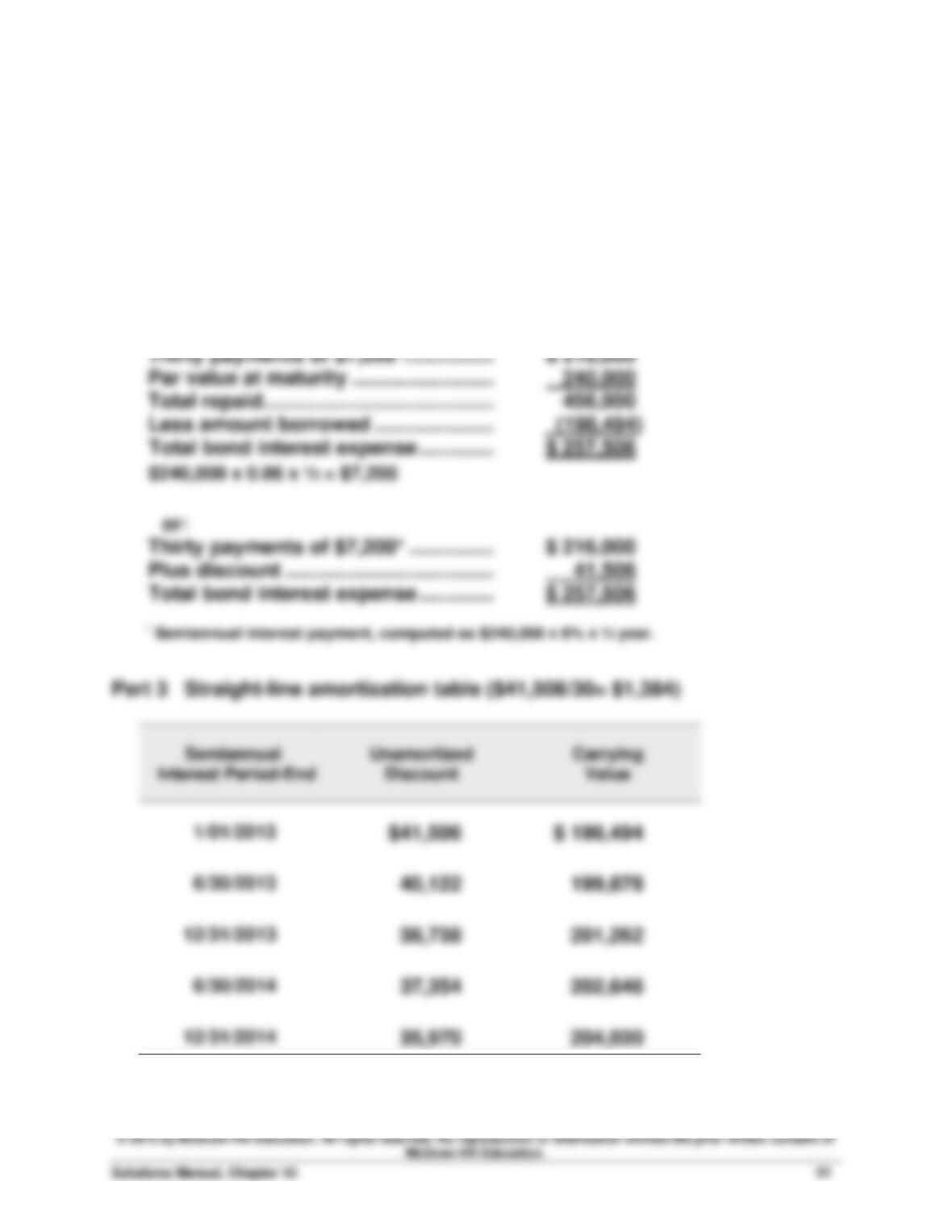

Part 2

Thirty payments of $7,200* ……………..…….

$ 216,000

Par value at maturity ……………………..……

240,000

Total repaid ………………………………………….

456,000

Less amount borrowed ………………….…….

(198,494)

Total bond interest expense …………..…….

$ 257,506

$240,000 x 0.06 x ½ = $7,200

or:

Thirty payments of $7,200* …………….…….

$ 216,000

Plus discount ………………………………..…….

41,506

Total bond interest expense …………..…….

$ 257,506

* Semiannual interest payment, computed as $240,000 x 6% x ½ year.

Part 3 Straight-line amortization table ($41,506/30= $1,384)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2013

$41,506

$ 198,494

6/30/2013

40,122

199,878

12/31/2013

38,738

201,262

6/30/2014

37,354

202,646

12/31/2014

35,970

204,030