Chapter 01 – Introducing Financial Accounting

Exercise 1-4 (20 minutes)

a. Situations involving ethical decision making in coursework include

performing independent work on examinations and individually

completing assignments/projects. It can also extend to promptly

returning reference materials so others can enjoy them, and to

Exercise 1-5 (10 minutes)

Code

Description

Principle/Assumption

E

1.

Usually created by a pronouncement from an

authoritative body.

Specific accounting

principle

G

2.

Financial statements reflect the assumption that

the business continues operating.

Going-concern

assumption

A

3.

Derived from long-used and generally accepted

accounting practices.

General accounting

principle

C

4.

Every business is accounted for separately from

its owner or owners.

Business entity

assumption

D

5.

Revenue is recorded only when the earnings

process is complete.

Revenue recognition

principle

B

6.

Information is based on actual costs incurred in

transactions.

Cost principle

F

7.

A company records the expenses incurred to

generate the revenues reported.

Matching (expense

recognition) principle

H.

8.

A company reports details behind financial

statements that would impact users’ decisions.

Full disclosure

principle

Exercise 1-6 (10 minutes)

1.

C

4.

A

2.

F

5.

G

3.

D

Exercise 1-7 (10 minutes)

a.

Corporation

e.

Sole proprietorship

b.

Sole proprietorship

f.

Sole proprietorship

c.

Corporation

g.

Corporation

d.

Partnership

Exercise 1-9 (10 minutes)

Assets

=

Liabilities

+

Equity

(a) $ 65,000

=

$ 20,000

+

$45,000

$100,000

=

$ 34,000

+

(b) $66,000

$154,000

=

(c) $114,000

+

$40,000

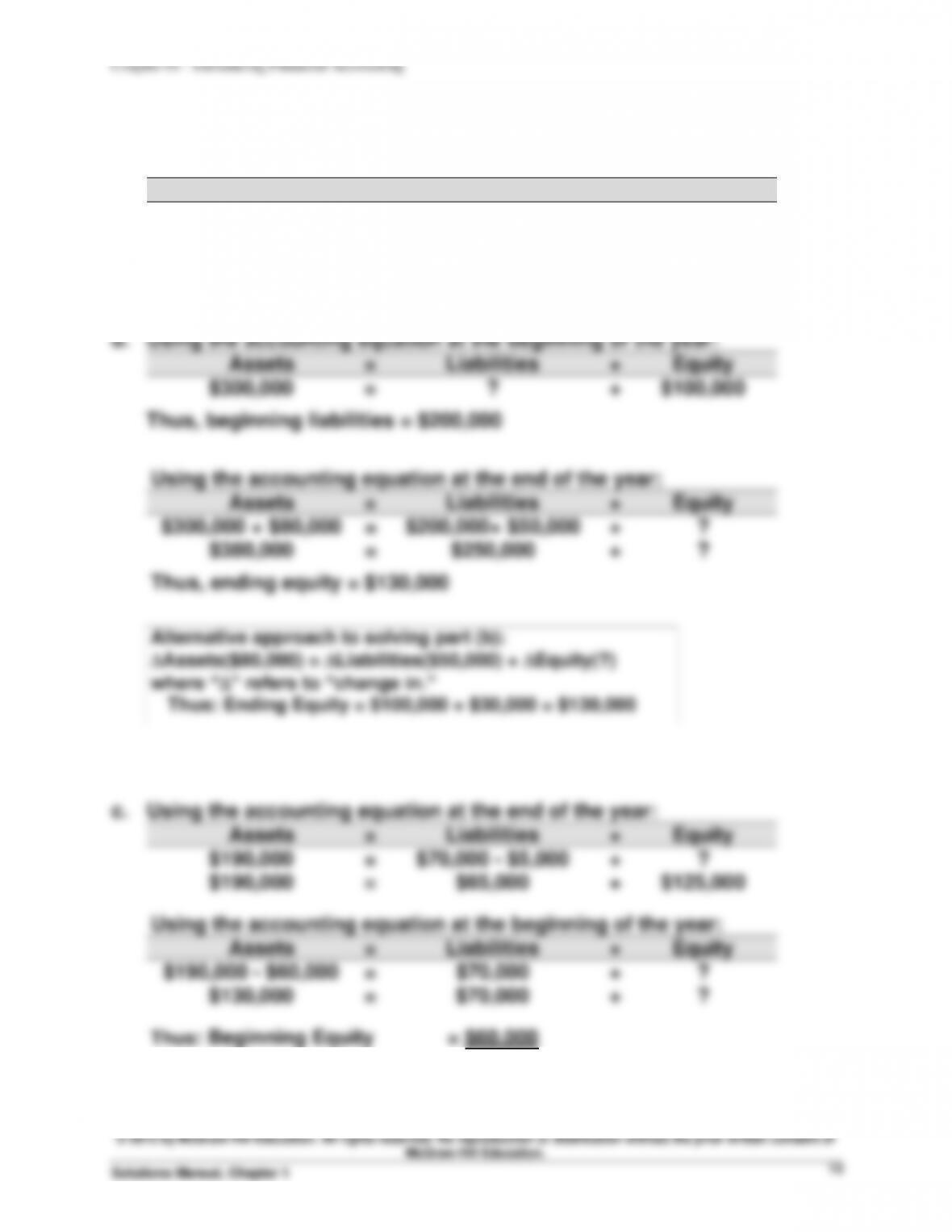

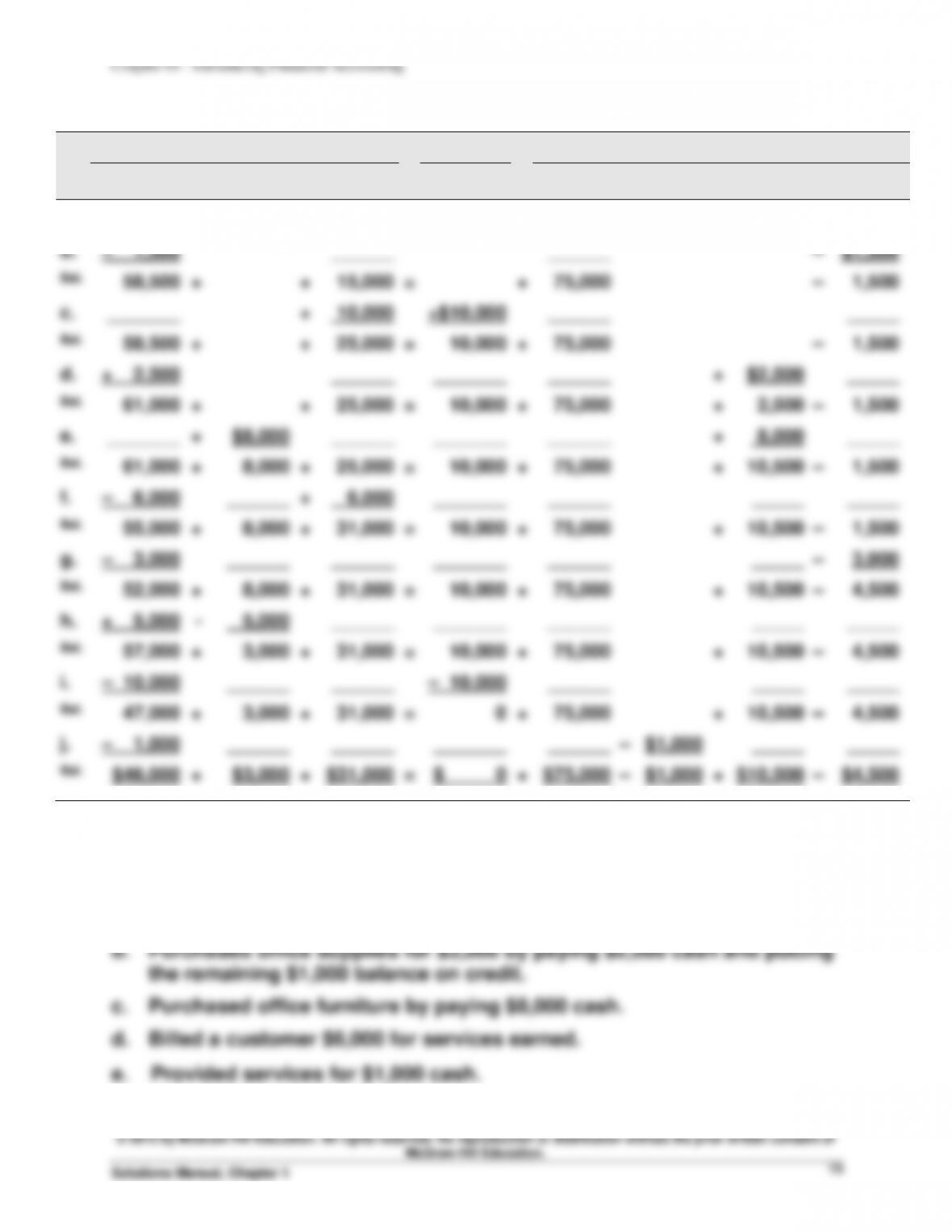

Exercise 1-10 (15 minutes)

Examples of transactions that fit each case include:

a. Cash dividends (or some other asset) paid to the stockholder(s) of the

business; OR, the business incurs an expense paid in cash.

Exercise 1-13 (20 minutes)

a. Purchased land for $4,000 cash.

Exercise 1-14 (15 minutes)

REAL ANSWERS

Income Statement

For Month Ended October 31

Revenues

Consulting fees earned …………………. $14,000

Exercise 1-15 (15 minutes)

REAL ANSWERS

Statement of Retained Earnings

For Month Ended October 31

Retained earnings, October 1 ……………………. $ 0

Exercise 1-18 (10 minutes)

Return on assets

=

Net income / Average total assets

=

$40,000 / [($200,000 + $300,000)/2]

=

16%

Interpretation: Swiss Group’s return on assets of 16% is markedly above

the 10% return of its competitors. Accordingly, its performance is

assessed as superior to its competitors.

Exercise 1-19 (10 minutes)

O 1. Cash paid for advertising O 5. Cash paid for rent

Exercise 1-20B (10 minutes)

a. Financing*

b. Investing

Chapter 01 – Introducing Financial Accounting

PROBLEM SET A

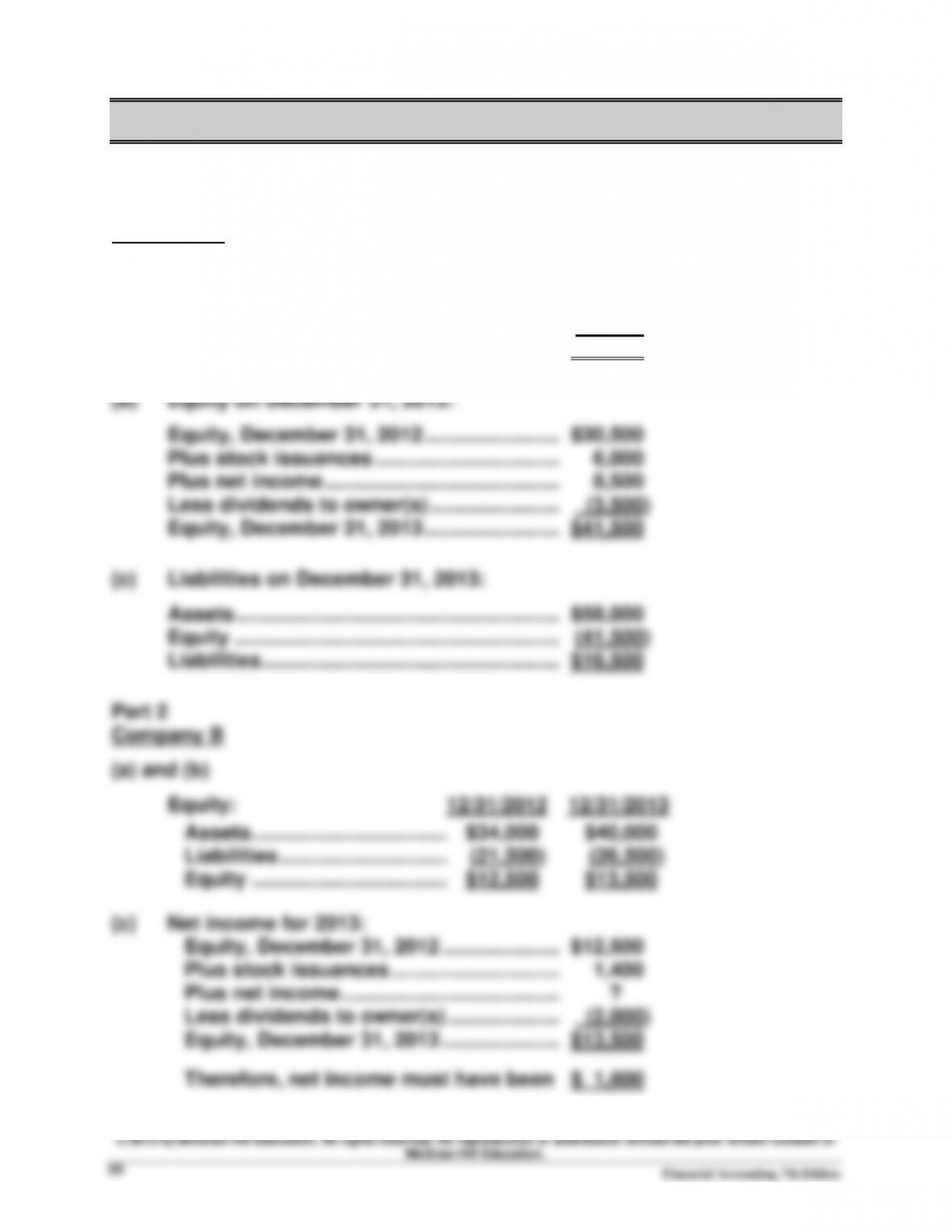

Problem 1-1A (40 minutes)

Part 1

Company A

(a) Equity on December 31, 2012:

Assets …………………………………………………. $55,000

Liabilities …………………………………………….. (24,500)

Equity …………………………………………………. $30,500