Appendix D – Accounting for Partnerships

Exercise D-6 (35 minutes)

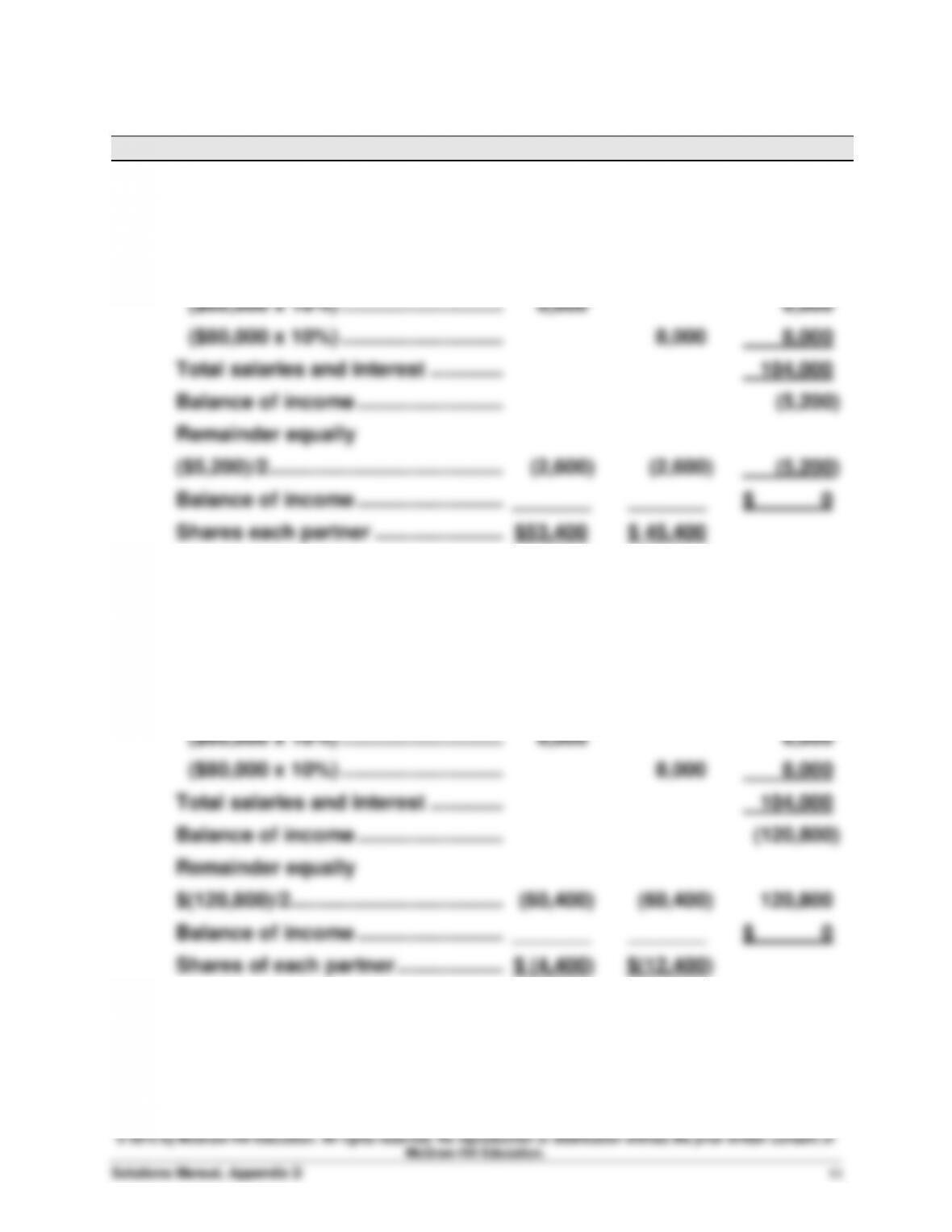

Kramer

Knox

Total

1.

Net income …………………………………………….

$ 98,800

Salary allowances …………………………..

$50,000

$ 40,000

90,000

Interest allowances

($60,000 x 10%) ………………………..…

6,000

6,000

($80,000 x 10%) ………………………..…

8,000

8,000

Total salaries and interest ………….………….

104,000

Balance of income ……………………..……

(5,200)

Remainder equally

($5,200)/2 …………………………..……….………….

(2,600)

(2,600)

(5,200)

Balance of income ……………………..……

_______

_______

$ 0

Shares each partner …………………..………

$53,400

$ 45,400

2.

Net income …………………………………………….

$ (16,800)

Salary allowances …………………………..

$50,000

$ 40,000

90,000

Interest allowances

($60,000 x 10%) ………………………..…

6,000

6,000

($80,000 x 10%) ………………………..…

8,000

8,000

Total salaries and interest ………….………….

104,000

Balance of income ……………………..……

(120,800)

Remainder equally

$(120,800)/2 ………………………………..………….

(60,400)

(60,400)

120,800

Balance of income ……………………..……

_______

_______

$ 0

Shares of each partner ……………….………….

$ (4,400)

$(12,400)

Exercise D-7 (25 minutes)

1.

Nov. 1

Cash ……………………………………………………………..….

90,000

Madison, Capital ………………………………………….

90,000

To record admission of Madison

[($510,000 + $90,000) x 15%].

2.

Nov. 1

Cash ………………………………………………………………..

120,000

Madison, Capital …………………………..……………..

94,500

Main, Capital …………………………………………..…..

20,400

Frist, Capital …………………………………………..…..

5,100

To record admission of Madison.

Supporting computations

$510,000 + $120,000 = $630,000

$630,000 x 15% = $94,500

$120,000 – $94,500 = $25,500

$25,500 x 80% = $20,400

$25,500 x 20% = $5,100

3.

Nov. 1

Cash ………………………………………………………………..

80,000

Main, Capital ………………………………………………..…..

6,800

Frist, Capital ………………………………………………..…..

1,700

Madison, Capital …………………………..……………..

88,500

To record admission of Madison.

Supporting computations

$510,000 + $80,000 = $590,000

$590,000 x 15% = $88,500

$80,000 – $88,500 = $(8,500)

$(8,500) x 80% = $(6,800)

$(8,500) x 20% = $(1,700)

Exercise D-10 (30 minutes)

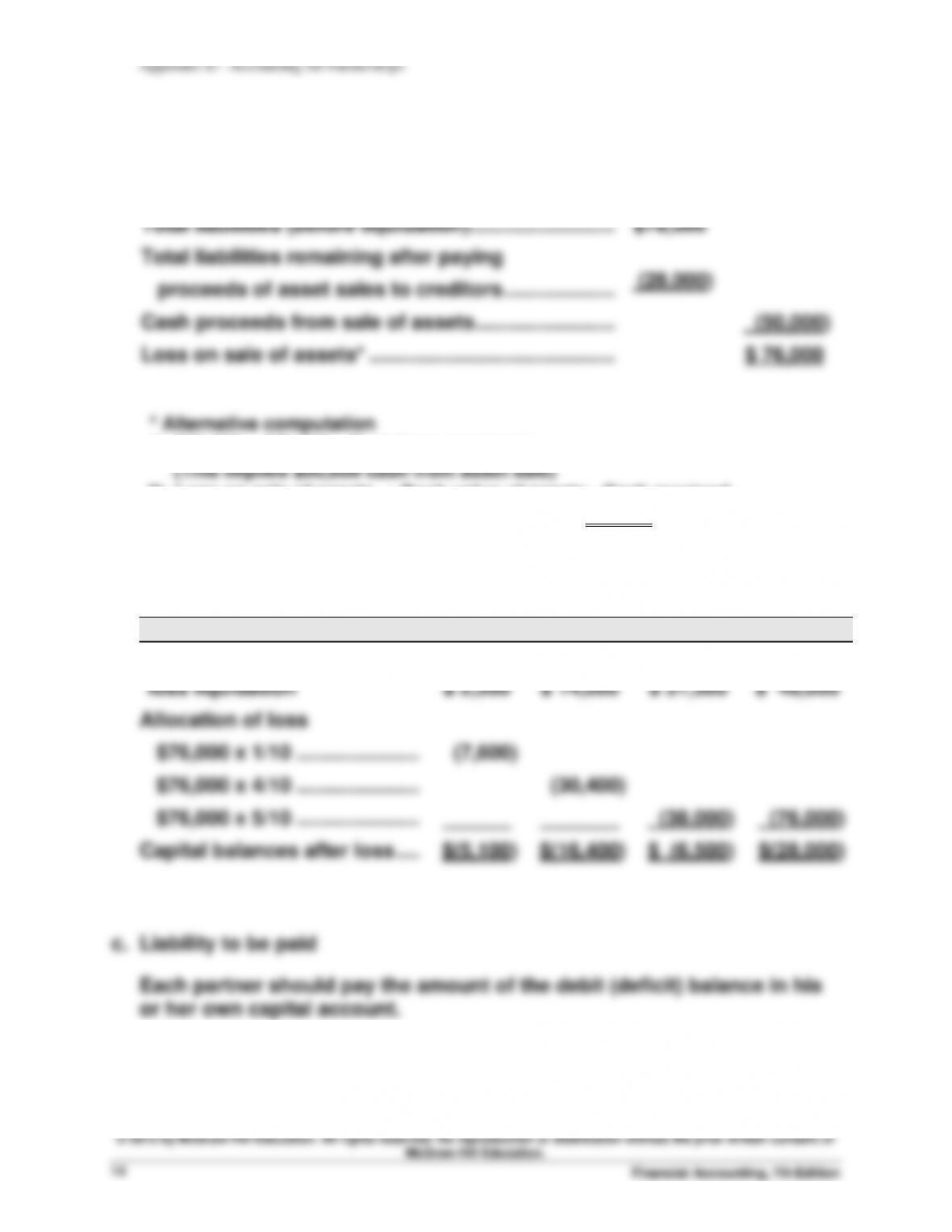

a. Loss from selling assets

Total book value of assets ………………………………………

$126,000

Total liabilities (before liquidation)……………………..……

$78,000

Total liabilities remaining after paying

proceeds of asset sales to creditors ………………..……

(28,000)

Cash proceeds from sale of assets …………………….……

(50,000)

Loss on sale of assets* ……………………………………..……

$ 76,000

* Alternative computation

1) $28,000 = $78,000 – Cash from asset sale

(This implies $50,000 cash from asset sale)

2) Loss on sale of assets = Book value of assets – Cash received

= $126,000 – $50,000 = $76,000

b. Loss allocation

Turner

Roth

Lowe

Total

Capital balances before

loss liquidation

$ 2,500

$ 14,000

$ 31,500

$ 48,000

Allocation of loss

$76,000 x 1/10 …………………..

(7,600)

$76,000 x 4/10 …………………..

(30,400)

$76,000 x 5/10 …………………..

______

_______

(38,000)

(76,000)

Capital balances after loss …..

$(5,100)

$(16,400)

$ (6,500)

$(28,000)

c. Liability to be paid

Each partner should pay the amount of the debit (deficit) balance in his

or her own capital account.

© 2015 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Financial Accounting, 7th Edition

16

Problem D-1A (50 minutes)

1.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

83,000

Tammy Bax, Capital ……………………………………

83,000

Joe Thomas, Capital ……………………………………

83,000

To close Income Summary.

2.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

62,250

Tammy Bax, Capital ……………………………………

87,150

Joe Thomas, Capital ……………………………………

99,600

To close Income Summary*.

*Supporting computations

($80,000/$320,000) x $249,000 = $62,250

($112,000/$320,000) x $249,000 = $87,150

($128,000/$320,000) x $249,000 = $99,600

3.

Dec. 31

Income Summary …………………………………………..…

249,000

Kara Ries, Capital …………………………………….…

79,000

Tammy Bax, Capital ……………………………………

72,200

Joe Thomas, Capital ……………………………………

97,800

To close Income Summary*.

*Supporting calculations

Ries

Bax

Thomas

Total

Net income ……………………………….………..

$249,000

Salary allowances

Ries ……………………………………….………..

$66,000

Bax………………………………………..………..

$56,000

Thomas …………………………………………..

$80,000

Total salaries ……………………………………..

202,000

Balance after salary allowances …………..

47,000

Interest allowances

Ries (10% on $80,000) …………….………..

8,000

Bax (10% on $112,000) ……………………..

11,200

Thomas (10% on $128,000) ……..………..

12,800

Total interest …………………………….………..

32,000

Bal. after interest and salaries ……………..

15,000

Balance allocated equally ………….………..

5,000

5,000

5,000

Total allocated equally ………………………..

15,000

Balance of income …………………….…….

______

______

______

$ 0

Shares of the partners……………….………..

$79,000

$72,200

$97,800

Problem D-2A (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $90,000 income …………………………..

$36,000

60% x $90,000 income …………………………..

$54,000

(b)

33 1/3% x $90,000 income …………………….…….

$30,000

66 2/3% x $90,000 income …………………….…….

$60,000

(c)

Salary allowance ………………………………….…………..

$72,000

40% x ($90,000 income – $72,000 salary) ….…………..

$ 7,200

60% x ($90,000 income – $72,000 salary) ….…………..

_______

10,800

Totals …………………………………………………..…..

$ 7,200

$82,800

(d)

Salary allowance ………………………………….…………..

$72,000

Interest allowances …………………………………………..

$ 4,200

6,300

50% x ($90,000 income – $72,000

salary – $10,500 interest) …………………………..

3,750

3,750

Totals …………………………………………………..…..

$ 7,950

$82,050

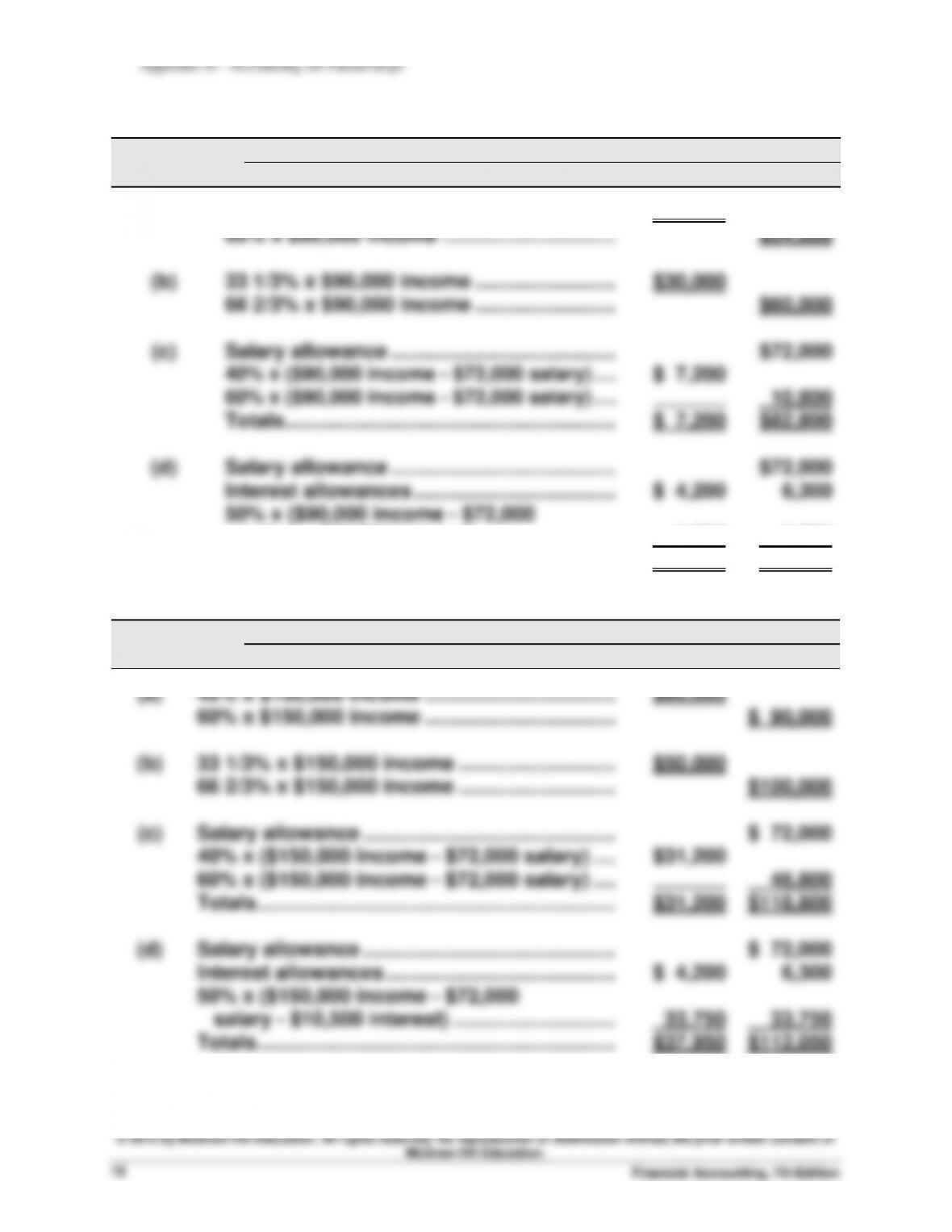

Income (Loss)

Year 3

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $150,000 income …………………………….………

$60,000

60% x $150,000 income …………………………….………

$ 90,000

(b)

33 1/3% x $150,000 income ……………………….….

$50,000

66 2/3% x $150,000 income ……………………….….

$100,000

(c)

Salary allowance ………………………………………………

$ 72,000

40% x ($150,000 income – $72,000 salary) ….………

$31,200

60% x ($150,000 income – $72,000 salary) ….………

_______

46,800

Totals …………………………..…………………………..………

$31,200

$118,800

(d)

Salary allowance ………………………………………………

$ 72,000

Interest allowances …………………………………..………

$ 4,200

6,300

50% x ($150,000 income – $72,000

salary – $10,500 interest) ………………………..…

33,750

33,750

Totals …………………………..…………………………..………

$37,950

$112,050

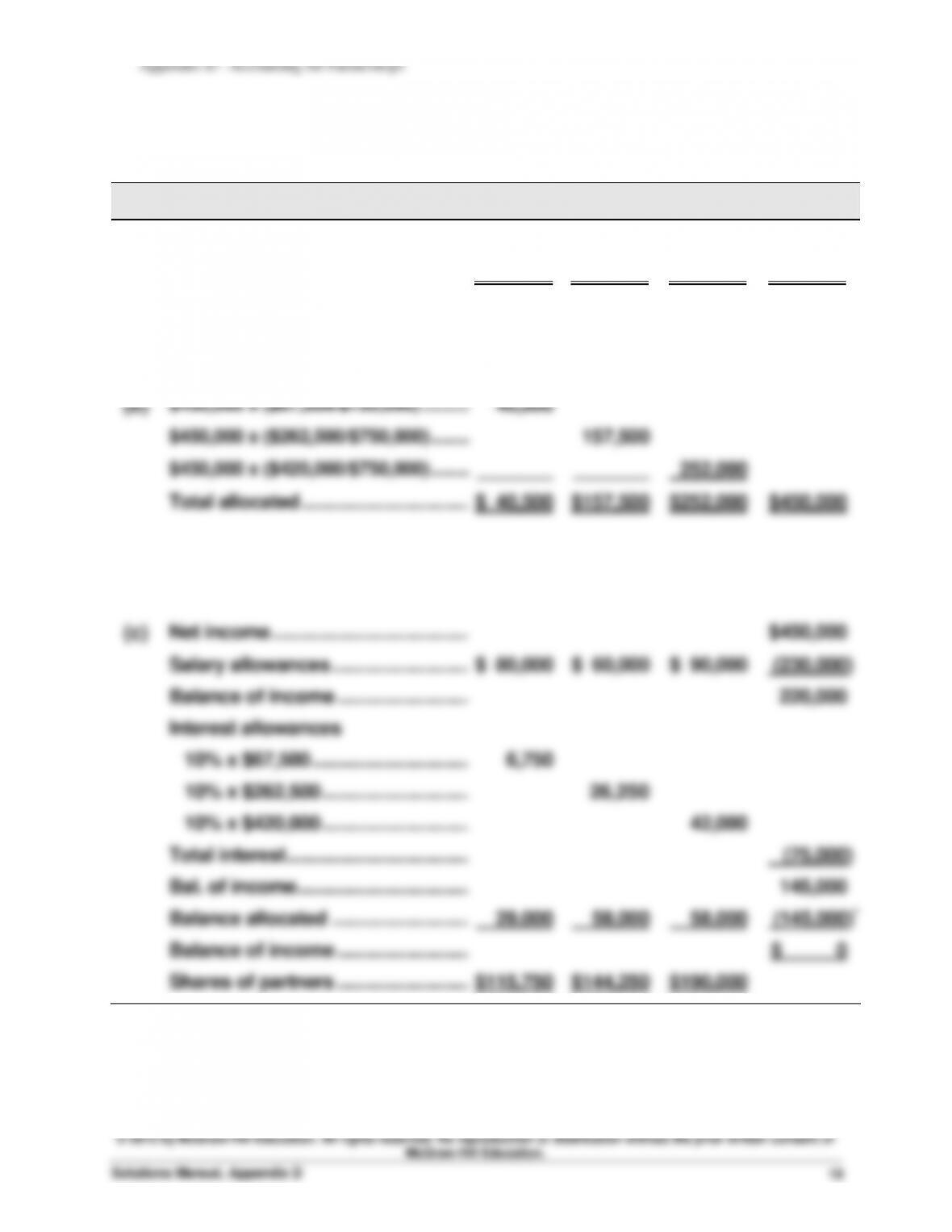

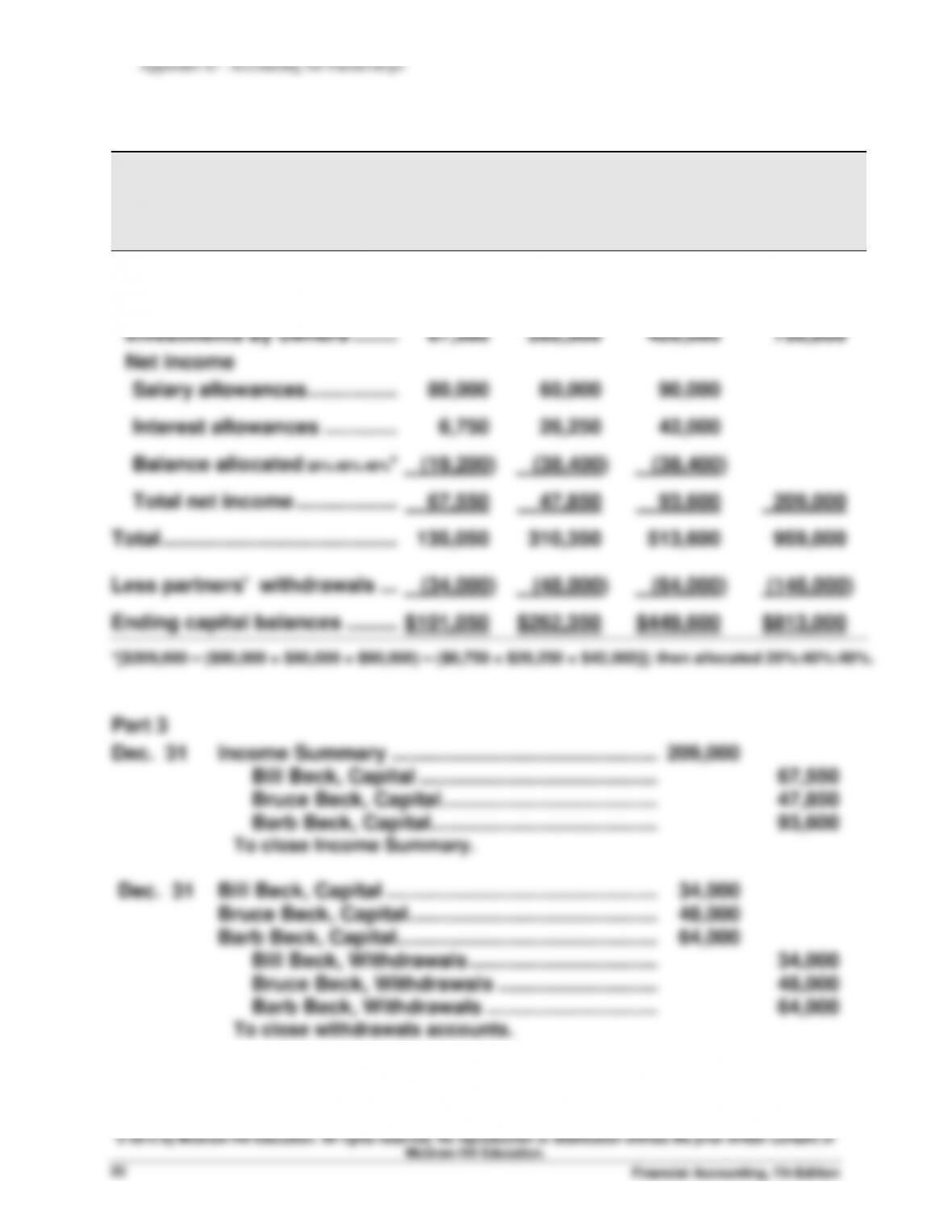

Problem D-3A (Concluded)

Part 2

BBB PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Bill

Bruce

Barb

Total

Beginning capital balances …..………

$ 0

$ 0

$ 0

$ 0

Plus

Investments by owners ………………

67,500

262,500

420,000

750,000

Net income

Salary allowances ……………..………

80,000

60,000

90,000

Interest allowances …………..………

6,750

26,250

42,000

Balance allocated 20%:40%:40%*

(19,200)

(38,400)

(38,400)

Total net income ……………….………

67,550

47,850

93,600

209,000

Total …………………………………….………

135,050

310,350

513,600

959,000

Less partners’ withdrawals ….………

(34,000)

(48,000)

(64,000)

(146,000)

Ending capital balances ……….………

$101,050

$262,350

$449,600

$813,000

*[$209,000 – ($80,000 + $60,000 + $90,000) – ($6,750 + $26,250 + $42,000)]; then allocated 20%:40%:40%.

Part 3

Dec. 31

Income Summary ……………………………………………..

209,000

Bill Beck, Capital …………………………………….…..

67,550

Bruce Beck, Capital ……………………………………..

47,850

Barb Beck, Capital …………………………………..…..

93,600

To close Income Summary.

Dec. 31

Bill Beck, Capital ………………………………………….…..

34,000

Bruce Beck, Capital …………………………………………..

48,000

Barb Beck, Capital ………………………………………..…..

64,000

Bill Beck, Withdrawals …………………………….…..

34,000

Bruce Beck, Withdrawals ………………………..…

48,000

Barb Beck, Withdrawals …………………………..

64,000

To close withdrawals accounts.