20 Minutes, Medium

a.

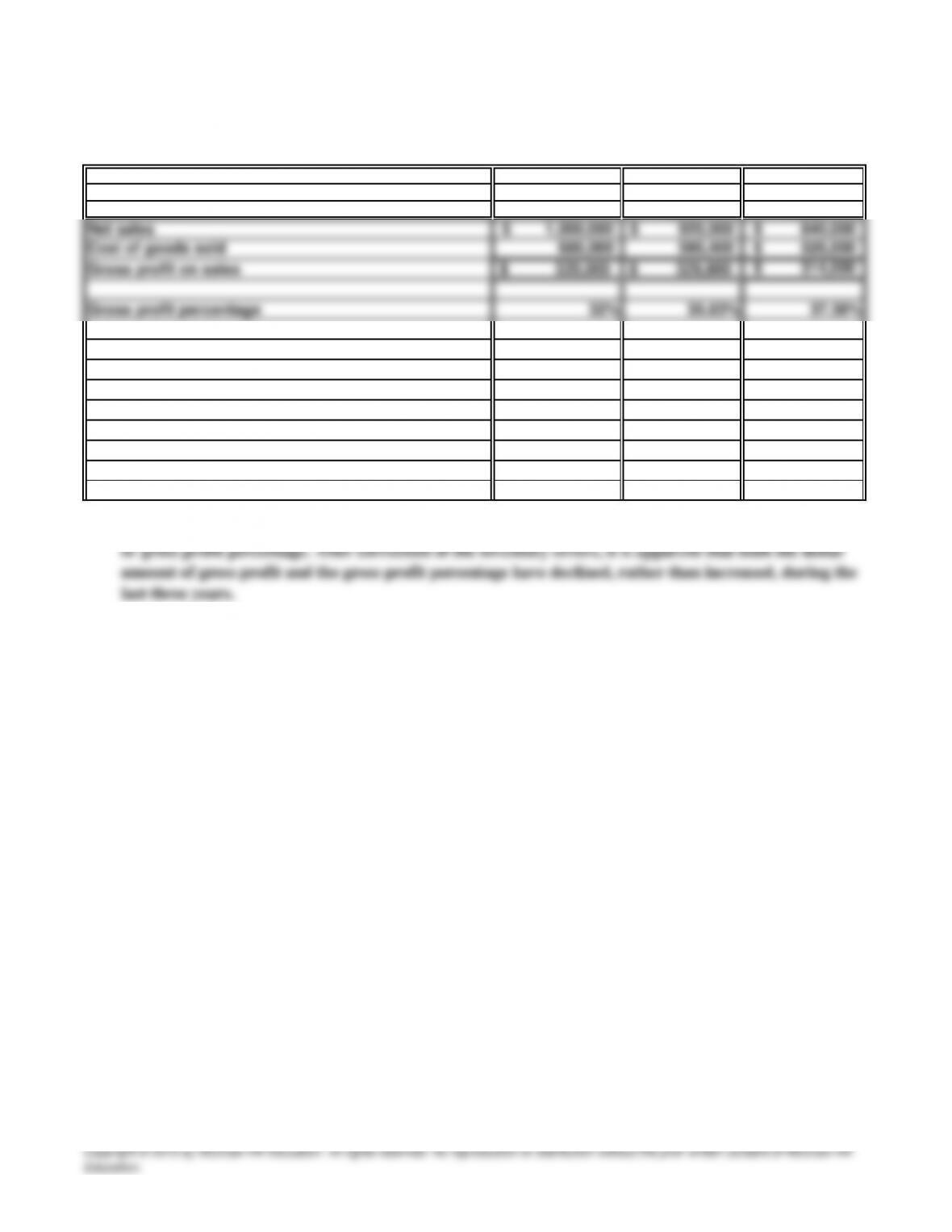

2015

2014

2013

b.

2015:

The current owners of this business have no basis for being enthusiastic about the trend of gross profit

$600,000 + $80,000 = $680,000

PROBLEM 8.6B

CITY SOFTWARE

Cost of Goods Sold:

$570,400 + $20,000 = $590,400

$546,000 – $20,000 = $526,000 2013:

2014:

25 Minutes, Medium

a.

330

,

000

$

600

,

000

55%

(

)

g

44

000

$

$

(

)

286

$

(p

(

)

g

41

,

250

2

,

750

$

,

$

,

$

g

g

41

250

288

g

G

231

$

PROBLEM 8.7B

SONG MEISTE

R

(

1

)

Estimated cost of

g

oods sold:

Cost ratio for the current

y

ear:

Cost of

g

oods available for sale

Retail

p

rices of

g

oods available for sale

Cost ratio

(

$330

,

000 ÷ $600

,

000

)

Estimated shrinka

g

e loss

,

stated at cost

at cost

(p

er

p

art b

)

(

3

)

Com

p

utation of

g

ross

p

rofit:

,

$

g

20 Minutes, Strong

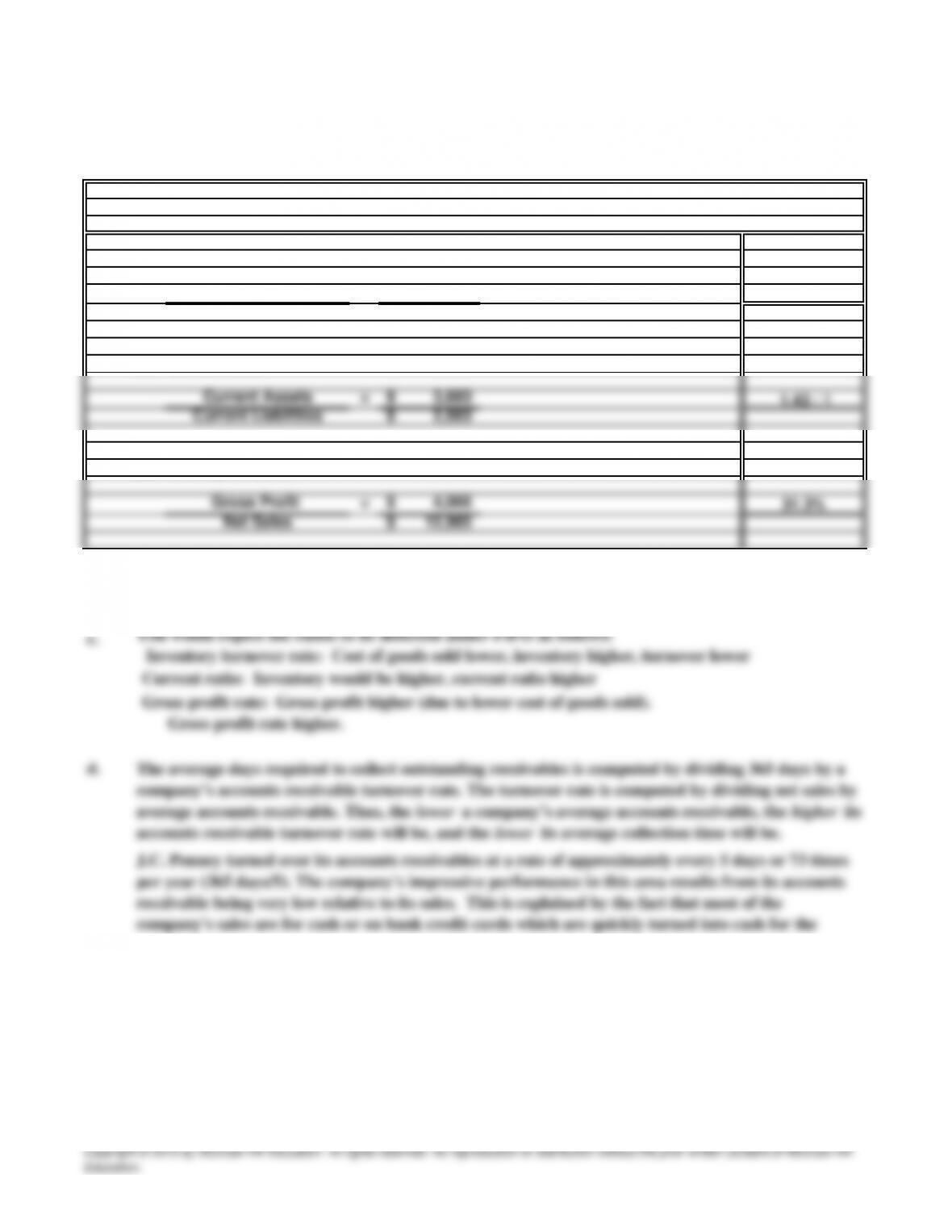

a. Computations based on LIFO valuation of inventory:

(1) Inventory turnover rate:

Cost of Goods Sold = 8,919$ 3.39 times

Average inventor

y

2,629$

(2) Current ratio:

(3) Gross profit rate:

b.

c.

d.

The company must have encountered increasing replacement costs for its merchandise during the

year.

PROBLEM 8.8B

J.C. Penne

y

30 Minutes, Strong

a.

SOLUTIONS TO CASES

OUR LITTLE SECRET

CASE 8.1

Lee confronts three related ethical issues. The first is that Our Little Secret’s past tax practices have

been both unethical and illegal. Lee should not be involved in such practices or, if she is in a position of

responsibility, allow them to continue.

2014 taxable income which would offset the understatement of taxable income in all past years. These

authors can see the practical appeal of such a “simple solution,” but we cannot support it. Our Little

Secret owes not only income taxes on its understated taxable income, but also interest and penalties for

a.

CASE 8.2

JACKSON SPECIALTIE

S

20 Minutes, Medium

While LIFO assigns old acquisition costs to inventory, it does not purport to coincide with the physical

movement of merchandise in and out of the business. Therefore, the units in inventory are not over 50

15 Minutes, Medium

a.

The inventory has been lost. It would be unethical to delay recognition of this loss in the hope that it

CASE 8.3

DEALING WITH THE BAN

K

ETHICS, FRAUD & CORPORATE GOVERNANC

E

No time limit, Strong INVENTORY TURNOVER RATES

CASE 8.

4

Turnover rates of those companies vary, depending on the year of the most recent 10-K reports used. The

INTERNET