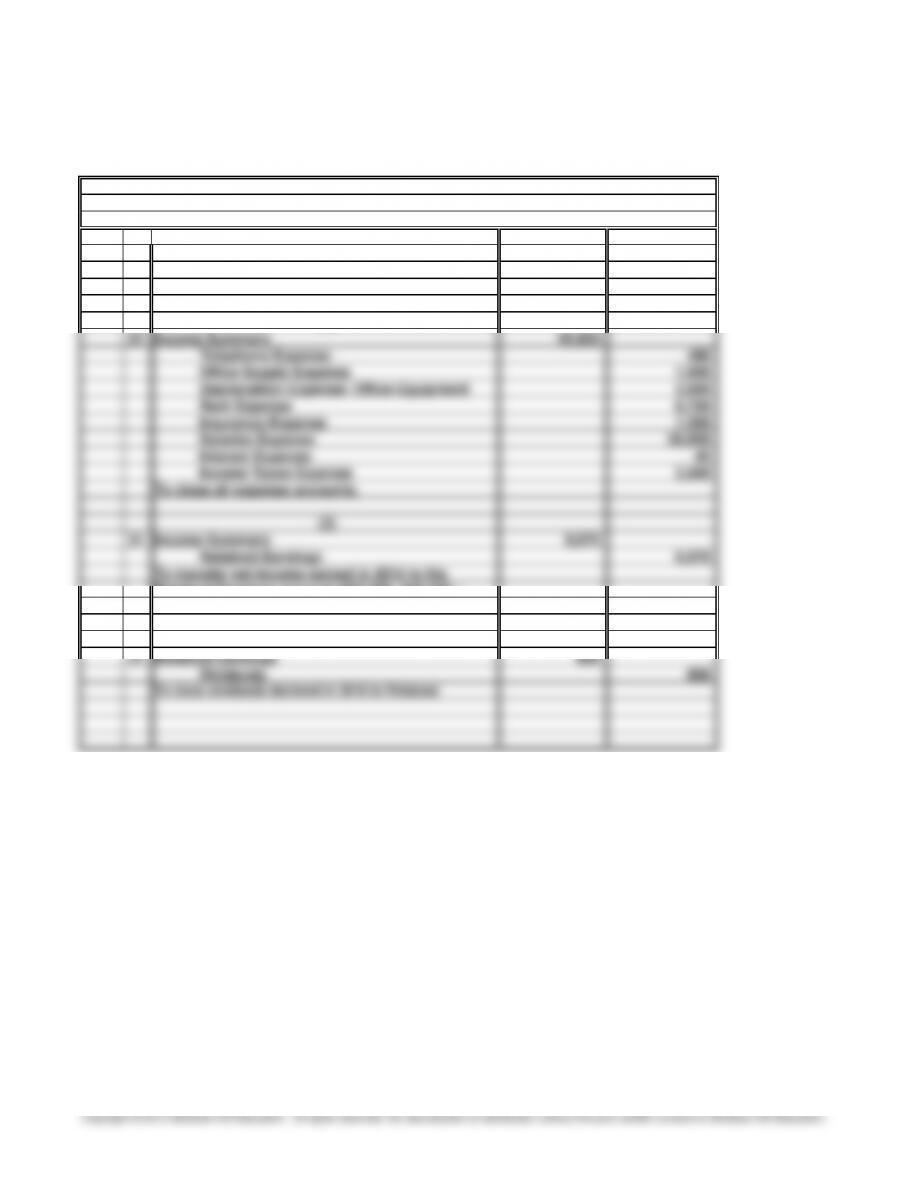

c.

Dec. 31 52

,

000

Income Summar

y

52

,

000

,

(

)

(

)

A

g

enc

y

Fees Earne

d

To close A

g

enc

y

Fees Earned.

(

2

)

PROBLEM 5.6B

TOUCHTONE TALENT AGENC

Y

December 31, 201

5

(1)

General Journal

TOUCHTONE TALENT AGENCY (continued

)

,

d.

14

,

950$ 38

,

300 600 250 530

,

,

p

,

,

,

Fees receivabl

e

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (continued

)

Unex

p

ired insurance

p

olicies

Office su

pp

lies

TOUCHTONE TALENT AGENC

Y

December 31, 201

5

After-Closing Trial Balanc

e

Cash

Pre

p

aid rent

,

50 Minutes, Strong

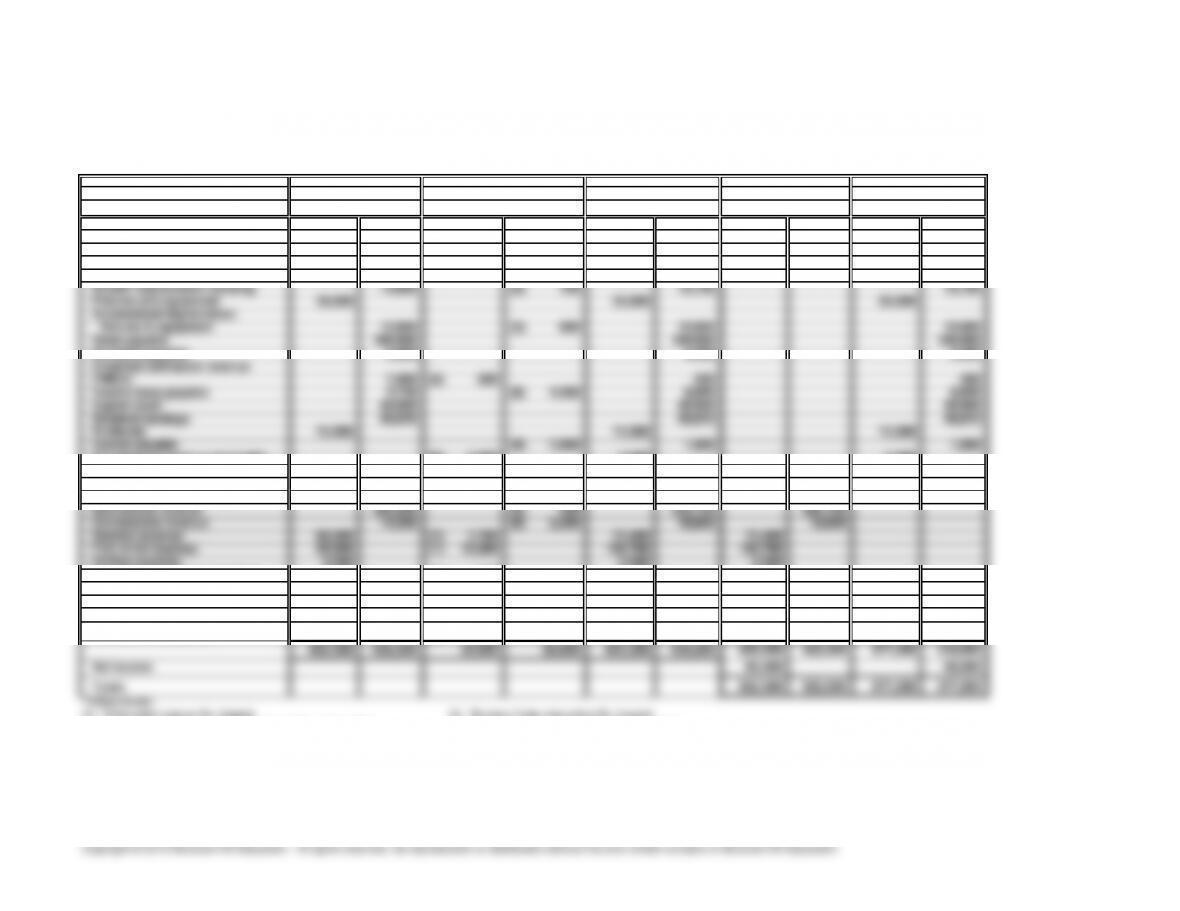

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Balance sheet accounts:

Cash

20

,

000

20

,

000

20

,

000

Prepaid film rental

31

,

200

(1)

15

,

200

16

,

000

16

,

000

Land

120

,

000

120

,

000

120

,

000

Building

168

,

000

168

,

000

168

,

000

36

000

36

000

36

000

12

000

(3)

600

12

600

12

600

180

000

180

000

180

000

Accounts payable

4

,

400

4

,

400

4

,

400

1

000

(5)

500

500

500

4

740

(8)

4

200

8

940

8

940

40

000

40

000

40

000

46

610

46

610

46

610

15

000

15

000

15

000

(4)

1

500

1

500

1

500

Concessions revenue receivable

(6)

2

,

250

2

,

250

2

,

250

Salaries payable

(7)

1

,

700

1

,

700

1

,

700

Income statement accounts:

305

200

(5)

500

305

700

305

700

14

350

(6)

2

250

16

600

16

600

68

500

(7)

1

700

70

200

70

200

94

500

(1)

15

200

109

700

109

700

9

500

9

500

9

500

Depreciation expense: building

4

,

900

(2)

700

5

,

600

5

,

600

Depreciation expense: fixtures

and equipment

4

,

200

(3)

600

4

,

800

4

,

800

Interest expense 10,500 (4) 1,500 12,000 12,000

Income taxes expense 40,000 (8) 4,200 44,200 44,200

(1) Film rental expense for August. (6) Revenue from concessions for August.

(2) Depreciation expense for August ($168,000 ÷ 240 =$700). (7) Salaries owed to employees but not yet paid.

(3) Depreciation expense for August ($36,000 ÷ 60 =$600). (8) Accrued income taxes on August income.

(4) Accrued interest on notes payable.

(5) Advance payment from YMCA earned during August ($1,500 x 1/3 = $500 per month).

CAMPUS THEATER

Income Statement Balance Shee

t

PROBLEM 5.7B

CAMPUS THEATE

R

Trial Balance

A

djustments

*

A

djusted Trial Balanc

e

WORKSHEET

For the Month Ended August 31, 201

5

14

000

(2)

700

14

700

14

700

15 Minutes, Medium

5.7%

24.1%

PROBLEM 5.8B

THE GAP, INC.

*Average Stockholders’ Equity = ($4.1 billion + $2.8 billion)/2

a. $833 million ÷ $14.5 billion =

Return on equity: Net Income/Average Stockholders’ Equity

Net income percentage: Net Income/Total Revenue

$833 million ÷ $3.45 billion*

Working capital: Current Assets – Current Liabilitiesb.

25 Minutes, Strong

a.

SOLUTIONS TO CRITICAL THINKING CASE

S

A

DEQUATE DISCLOSUR

E

CASE 5.1

Mandella Construction Co. should disclose the accounting method that it is using in the

notes accompanying its financial statements. When different accounting methods are

Group assignment:

No time estimate

CASE 5.2

We do not

p

rovide com

p

rehensive solutions for

g

rou

p

p

roblems. It is the nature of these

p

roblems

that solutions should reflect the collective experiences of the group. But the following

observations may be useful in stimulating class discussion:

WORKING FOR THE COMPETITION

ETHICS, FRAUD & CORPORATE GOVERNANCE

5 Minutes, Easy

The purpose of the personal certification process is to make CEOs and CFOs more accountable

and personally responsible for the contents in the annual reports issued by their companies.

CASE 5.3

CEOs AND CFOs

CERTIFICATIONS BY

15 Minutes, Easy

Debt and CommitmentsAccounting Policies

INTERNET

CASE 5.4

ANNUAL REPORT DISCLOSURES

Listed below are the headings of the major disclosure items presented in Ford’s most recent financial statement footnotes.

Students are to discuss the general nature and content of the various topics. The advanced nature of some of these topics goes

beyond the scope of an introductory course.