Ex. 5.8 a. 60,000

240,000 300,000

To close revenue accounts to income summary.

412,500

b. 450,000$

y

p

c.

Consulting Revenue – Individual Clients……………..

Income Summar

y

…………………………………………

…

Consulting Revenue – Corporate Clients……………..

Income Summar

y

…………………………………

…

No, the dollar amounts are not the same in the adjusting and closing entries. The

Insurance Ex

p

ense……………………………………

…

To close Insurance Expense (5 months) to Income

Summary.

Retained Earnings, (January 1, 2015)………………

To close dividends to retained earnings.

Ex. 5.10 a. Net Income ($12,750) ÷ Total Revenue ($51,000) 25%

d. Current Assets ($32,000) ÷ Current Liabilities ($8,000) 4-to-1

Com

p

utations:

Total revenue………………………………… 51,000$

Significance: All companies must consume resources (incur

costs) in order to generate revenue. The net income

percentage is a measure of management’s ability to control

these costs and use resources efficiently to generate revenue.

Based on the above measures, this company appears to be

profitable and potentially liquid.

Significance: Current assets often convert to cash in the near

future, whereas current liabilities often consume cash in the

near future. Thus, working capital is a measure of a

com

p

an

y

‘s short-term li

q

uidit

y

.

Significance: The current ratio is simply working capital

expressed as a proportion. Thus, it is also a measure of short-

term liquidity.

Ex. 5.11 a. Net Income ($3,040) ÷ Total Revenue ($152,000) 2%

Significance: All companies must consume resources (incur

costs) in order to generate revenue. The net income percentage

is a measure of management’s ability to control these costs and

use resources efficiently to generate revenue.

Ex. 5.12 a. (1)

Lift Ticket Revenue, $210,000 ($850,000 $640,000)

Ex. 5.14

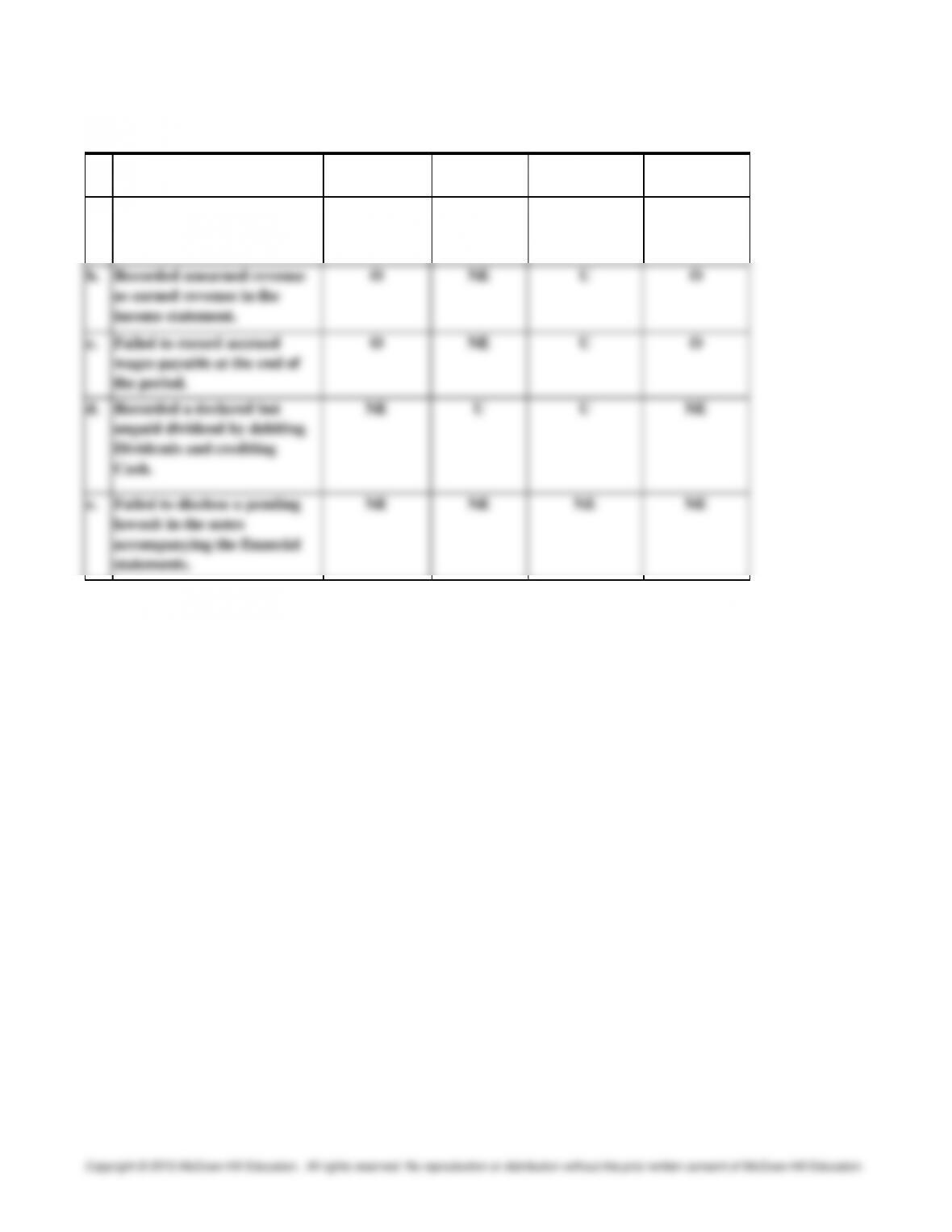

a. U NE NE NE

e. NE NE NE NEFailed to disclose a pending

lawsuit in the notes

accompanying the financial

statements.

Retained

Earnings

Error

Recorded a dividend as an

expense in the income

statement.

Net Income

Total

Assets Total

Liabilities

Ex. 5.15 a.

The company uses straight-line depreciation as discussed in the Summary of

Significant Accounting Policies section of the notes accompanying the financial

statements.

a.

130

,

000$

Part

y

revenue earne

d

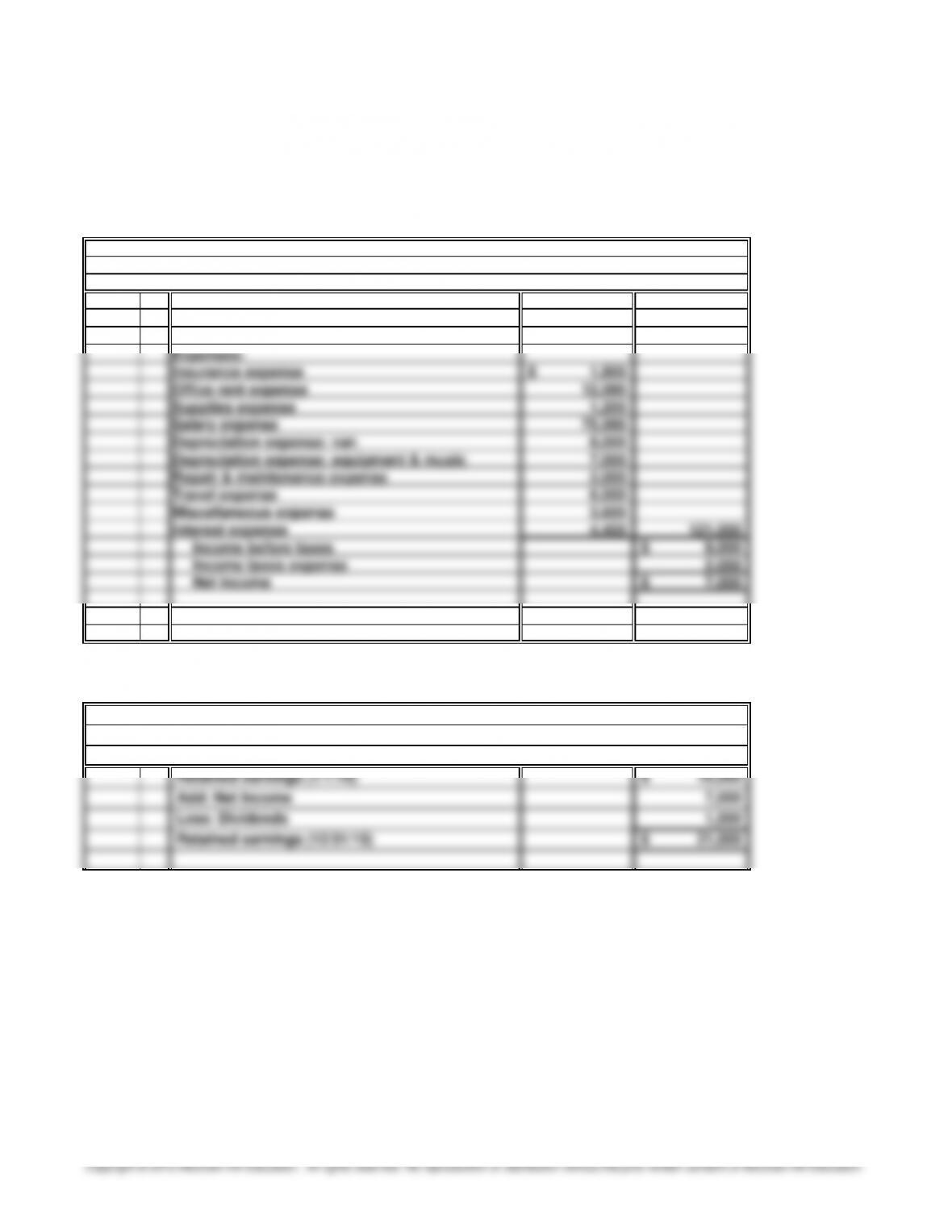

SOLUTIONS TO PROBLEMS SET

A

PARTY WAGON, INC

.

For the Year Ended December 31, 201

5

Income Statement

20 Minutes, Easy PROBLEM 5.1

A

PARTY WAGON, INC

.

Revenues:

,

Asset

s

$ 15

,

000

9

,

000

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

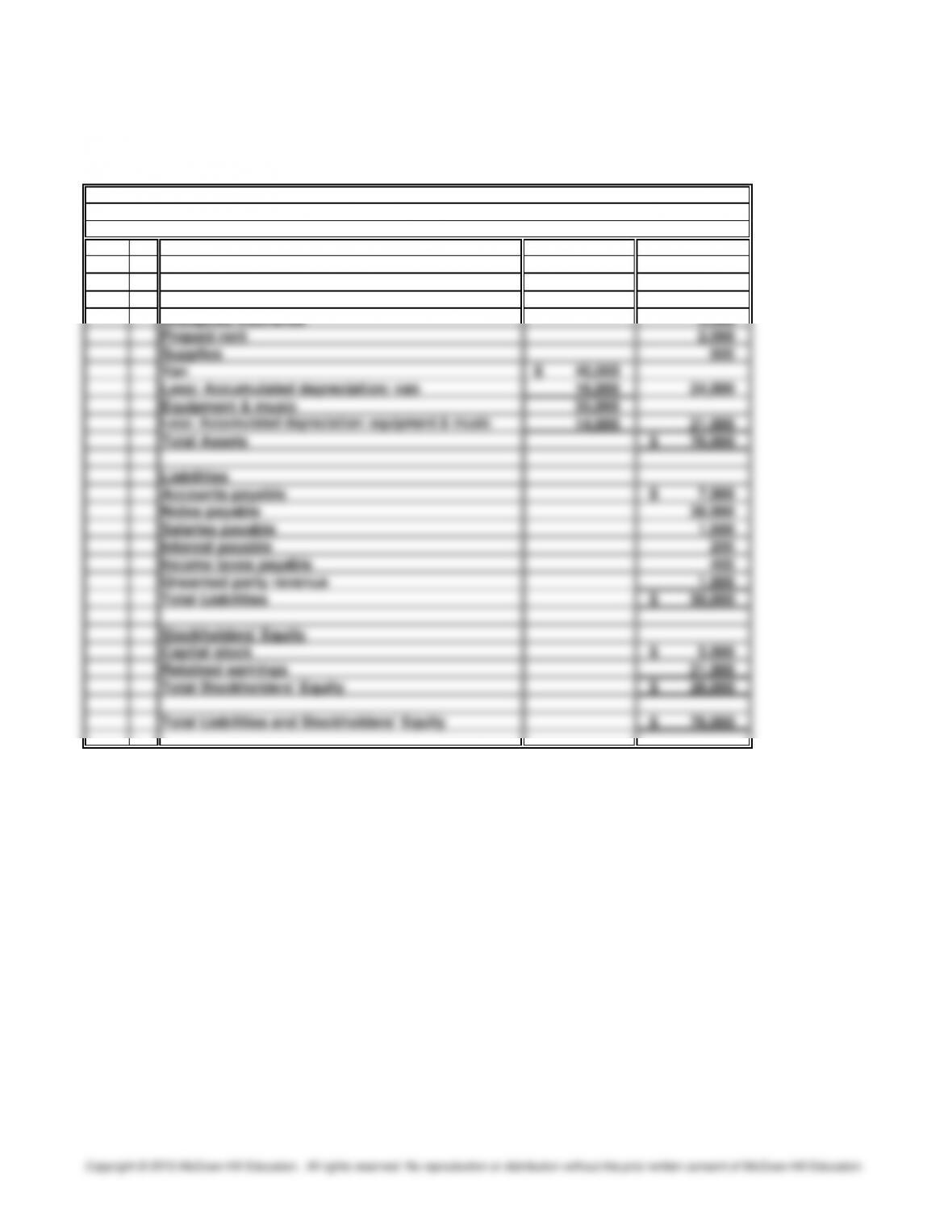

PROBLEM 5.1

A

PARTY WAGON, INC. (continued

)

Accounts receivabl

e

PARTY WAGON, INC.

December 31, 201

5

Balance Shee

t

Cash

a. (cont’d)

,

b.

Office Rent Ex

p

ense 12

,

000

,

,

,

,

,

,

,

,

,

31 7

,

000

Retained Earnin

g

s7

,

000

,

g

,

c. For the year ended December 31, 2015, the company generated net income of $7,000 on

(

3

)

To transfer net income earned in 2015 to the

g

$7,000

)

.

(

)

To close all ex

p

ense accounts.

Income Summar

y

Retained Earnin

g

s account

(

$130,000 – $123,000 =

PROBLEM

5

.

1A

PARTY WAGON, INC

.

December 31, 201

5

(1)

General Journal

PARTY WA

GO

N

(

concluded

)

,

y

(

)

a.

340

,

000$

,

For the Year Ended December 31, 2015

Statement of Retained Earnings

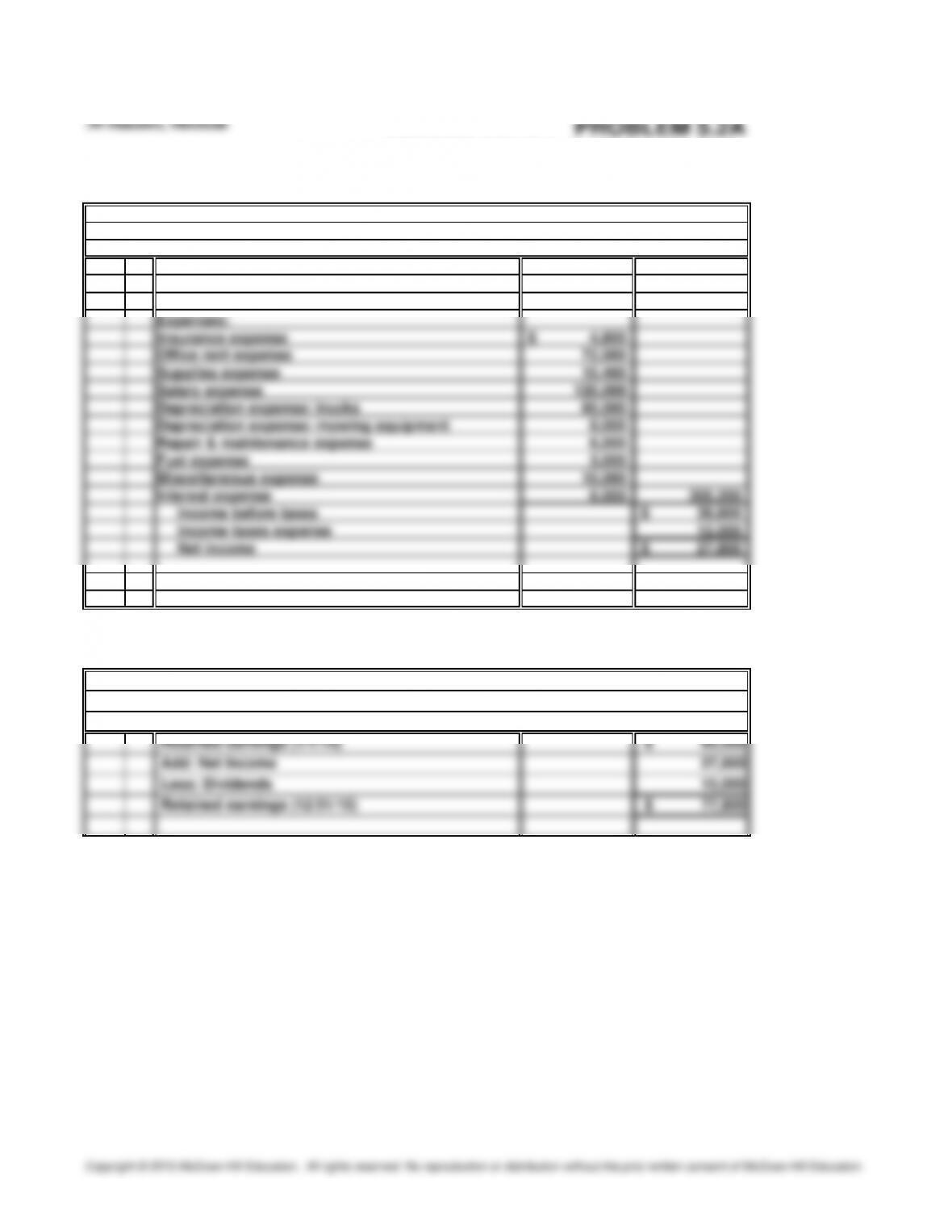

AFFORDABLE LAWN CARE, INC.

Mowin

g

revenue earned

PROBLEM 5.2

A

AFFORDABLE LAWN CARE, INC

.

Revenues:

AFFORDABLE LAWN CARE, INC

.

For the Year Ended December 31, 201

5

Income Statement

,