f.

35,250$

750

PROBLEM 4.7B

STILLMORE INVESTIGATIONS (concluded)

Add: December depreciation expense (adjusting entry 4)

Accumulated depreciation per unadjusted trial balance

20 Minutes, Strong

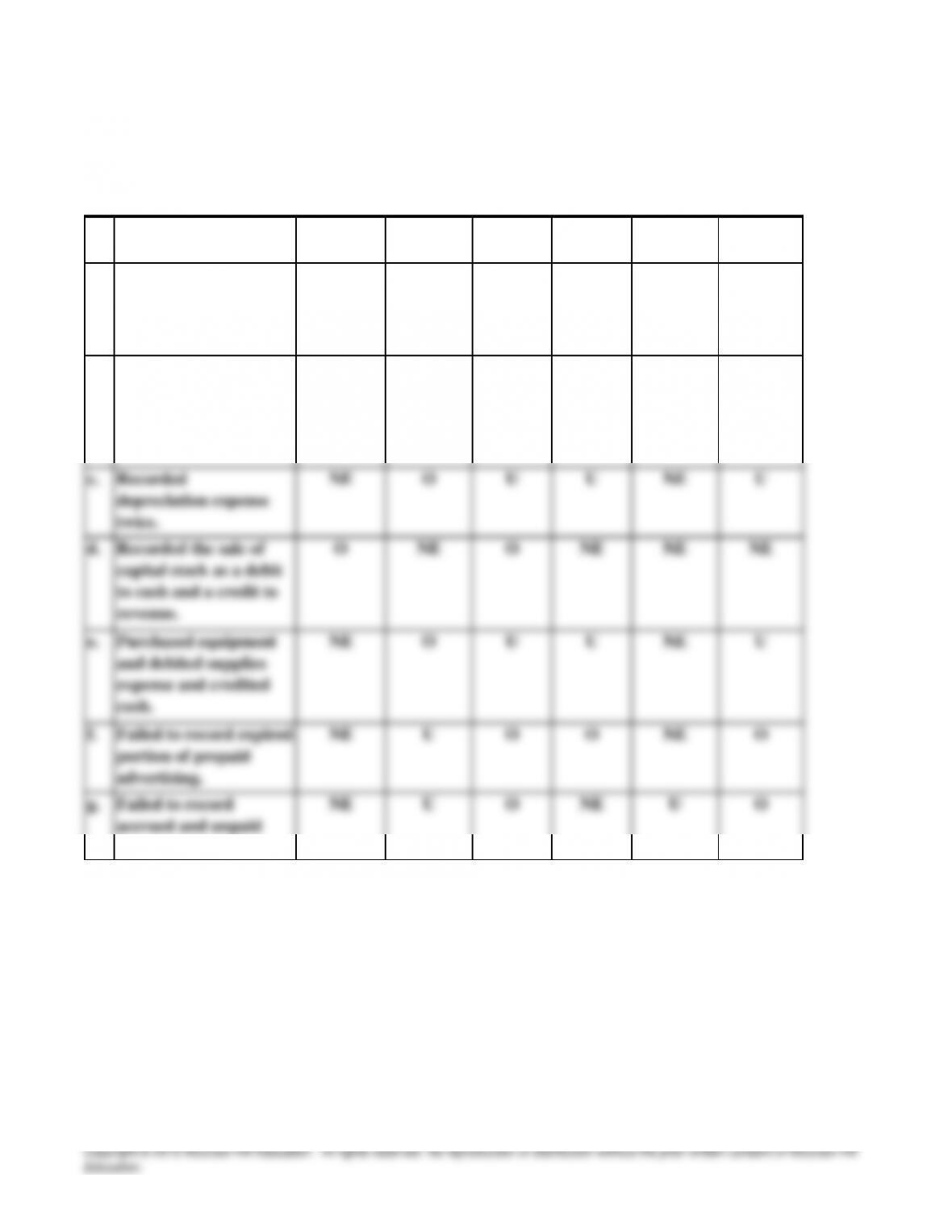

a. NE NE NE U U NE

b. O NE O O NE O

Total

Assets Total

Liabilities Owners’

Equity

PROBLEM 4.8B

STEPHEN CORPORATION

Error Total

Revenue Total

Expenses Net

Income

Recorded a declared

but unpaid dividend by

debiting dividends and

crediting Cash.

Recorded a receipt of

an account receivable

as a debit to cash and a

credit to fees earned.

30 Minutes, Medium

a.

SOLUTIONS TO CRITICAL THINKING CASES

YEAR-END ADJUSTMENTS

CASE 4.1

No adjusting entry is needed, because although the revenue was collected in advance on

September 1, it has all been earned prior to year-end. Thus, inclusion of the entire amount in

revenue of the period is correct.

25 Minutes, Medium

a. (1)

CASE 4.2

AVIS RENT-A-CAR

THE CONCEPT OF MATERIALITY:

An event or transaction is “material” when knowledge of the item reasonably may be

expected to influence the decisions of users of financial statements. One

consideration is simply the size of the dollar amounts involved: what is “material” in

relation to the operations of a small business may not be material in relation to the

operations of a large corporation. In addition, the nature of the event plays a key role in

determining whether or not knowledge of the event would influence decision

makers.

10 Minutes, Easy

a.

The decision by management to wait three years before converting the $40,000 capitalized

advertising expenditure to advertising expense clearly violates generally accepted

accounting principles. The matching principle requires that revenue earned during a

ETHICS, FRAUD & CORPORATE GOVERNANCE

CASE 4.3

EXPENSE MANIPULATION

10 Minutes, Easy

1.

2.

3.

Note to the instructor: The adjustments required for several of the accounts listed above are

discussed in subsequent chapters. Some are beyond the scope of an introductory course.

CASE 4.4

IDENTIFYING ACCOUNTS

Accounts from Hershey’s balance sheet likely to have required an adjusting entry are:

Inventories

Accounts Receivable–Trade

Deferred Income Taxes

INTERNET