Chapter 04 – The Accounting Cycle: Accruals and Deferrals

Financial and Managerial Accounting, 17e 4-1

4 THE ACCOUNTING CYCLE:

ACCRUALS AND DEFERRALS

Chapter Summary

In order for revenues and expenses to be reported in which they are earned or incurred,

adjusting entries must be made at the end of the accounting period. Adjusting entries are made

so the revenue recognition and matching principles are followed. Chapter 4 completes the

treatment of the accounting cycle for service type businesses. It focuses on the year-end activities

culminating in the annual report. These include the preparation of adjusting entries, preparing

the financial statements themselves, drafting the footnotes to the statements, closing the

accounts, and preparing for the audit. These topics form the content of Chapter 4.

The chapter begins with a thorough review of various adjusting entries. The adjustments

are classified into four categories: converting assets to expenses; converting liabilities to revenue;

accruing unpaid expenses and; accruing uncollected revenues. The categories are discussed and

illustrated in this order. We briefly explain that the adjusting entries are needed to satisfy the

realization and matching principles. The concept of materiality is introduced and its relevance to

the adjusting entries is explained next.

Learning Objectives

1. Explain the purpose of adjusting entries.

2. Describe and prepare the four basic types of adjusting entries.

3. Prepare adjusting entries to convert assets to expenses.

4. Prepare adjusting entries to convert liabilities to revenue.

5. Prepare adjusting entries to accrue unpaid expenses.

6. Prepare adjusting entries to accrue uncollected revenue.

7. Explain how the principles of realization and matching relate to adjusting entries.

8. Explain the concept of materiality.

9. Prepare an adjusted trial balance and describe its purpose.

Chapter 04 – The Accounting Cycle: Accruals and Deferrals

Brief topical outline

A Adjusting entries

1 The need for adjusting entries

2 Types of adjusting entries

3 Adjusting entries and timing differences

4 Characteristics of adjusting entries

5 Year-end at Overnight Auto Service

6 Converting assets to expenses

a Prepaid expenses

b Shop supplies

c Insurance policies – see Your Turn (page 147)

d Recording prepayments directly in the expense accounts

7 The concept of depreciation

a What is deprecation?

b Depreciation is only an estimate – see Case in Point (page 149)

c Depreciation of Overnight’s building

d Depreciation of tools and equipment

e Depreciation – a noncash expense

8 Converting liabilities to revenue

a Recording advance collections directly in the revenue accounts

9 Accruing unpaid expenses

a Accrual of wages (or salaries) expense

b Accrual of interest expense

10 Accruing uncollected revenue

11 Accruing income taxes expense: the final adjusting entry – see Case in Point

(page 155)

a Income taxes in unprofitable periods

B Adjusting entries and accounting principles

1 The concept of materiality

a Materiality and adjusting entries

b Materiality is a matter of professional judgment – see Your Turn (page

158)

2 Effects of the adjusting entries – see Ethics, Fraud & Corporate Governance

(page 161)

C Concluding remarks

Chapter 04 – The Accounting Cycle: Accruals and Deferrals

Financial and Managerial Accounting, 17e 4-3

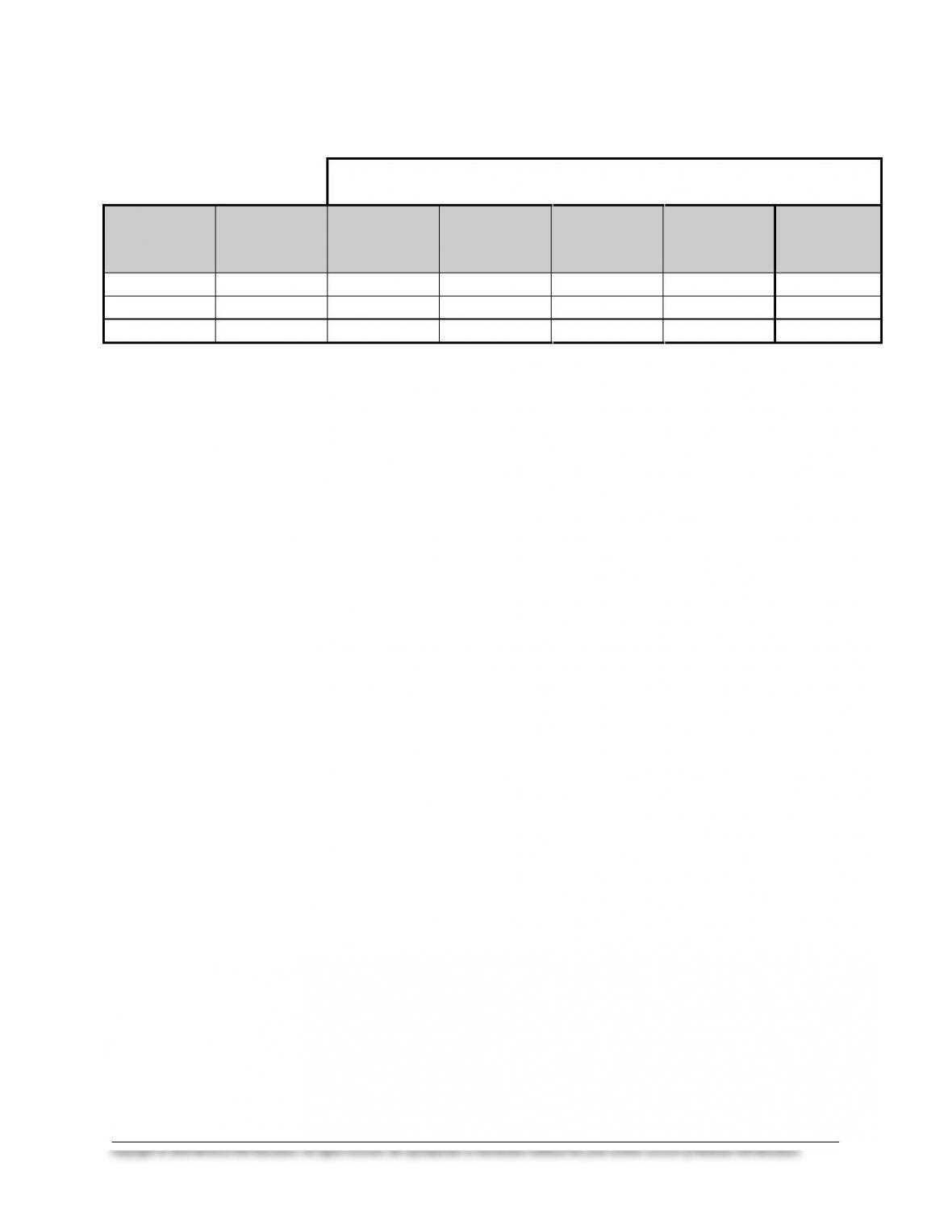

Topical coverage and suggested assignment

Homework Assignment

(To Be Completed Prior to Class)

Class

Meetings

on Chapter

Topical

Outline

Coverage

Discussion

Questions

Brief

Exercises

Exercises

Problems

Critical

Thinking

Cases

1

A

1, 2, 3

1, 2

2, 3, 6

1

2

A

8, 9

4, 5

7, 9

3, 4

1

3

B – C

10, 11

9, 10

10, 11

6

2

Comments and observations

Teaching objectives for Chapter 4

In Chapter 4 we cover the numerous accounting activities, both analytical and procedural, that

take place at the end of a fiscal year. In covering this chapter, our teaching objectives are to:

1 Explain the need for adjusting entries in accrual accounting.

2 Illustrate the four basic types of adjusting entries.

3 Review in sequence the steps in the complete accounting cycle.

4 Introduce the principle of materiality and discuss its relevance to adjusting entries.

General comments

The need for adjusting entries stems from the most basic concepts of accrual accounting,

the concepts that revenue is recognized when it is earned and that expenses are recognized when

the related goods and services are used. We find that students who do not fully understand the

nature and purpose of adjusting entries have difficulty with other accrual accounting concepts

throughout the course. We find Exercises 2, 3, 5, and 9 particularly useful. Exercise 2 illustrates

the effects of the four basic types of adjusting entries upon both the income statement and

balance sheet. Exercise 3 focuses upon those adjustments that apportion previously recorded

amounts, while Exercise 5 illustrates adjustments needed to accrue unrecorded amounts.

Exercise 9 demonstrates that the need for adjusting entries arises from transactions spanning

more than one accounting period. We also like Exercise 6, which focuses upon unearned

revenue in the accounting records of American Airlines.

We personally spend quite a bit of class time on materiality, as we consider it to be one

of the most important concepts in accounting. The chapter has several good assignments on

materiality, including Discussion Questions 10 and 11, Exercise 10, and Case 2. We always

assign at least two of these and discuss them in class.

Chapter 04 – The Accounting Cycle: Accruals and Deferrals

An aside Some students may ask why the word “debit” is abbreviated “Dr.” in the columnar

headings of the worksheet, as there is no “r” in “debit.” The word “debit” is derived from the

Latin verb debere, which means “to owe.” “Credit” stems from the Latin verb credere, meaning

“to entrust” or “to lend.” In modern usage, of course, the term debit has come to mean any entry

in the left-hand side of a ledger account, and credit has come to mean any entry in the right-hand

side.

Supplemental Exercises

Group Exercise

Have students interview accounting managers at several corporations in the local area.

Ask students to find out how often the corporation prepares adjusting entries and how important

the accounting manager thinks adjusting entries are to the fair presentation of the financial

statements to the stockholders and creditors.

Internet Exercise

Visit the homepage of Microsoft at www.microsoft.com. Access the annual report for

2009. Find the footnotes to the statements and read the disclosures in the note titled

“Contingencies.” Regarding the events described do you think Microsoft is providing adequate

disclosure to its stockholders?

Chapter 04 – The Accounting Cycle: Accruals and Deferrals

Financial and Managerial Accounting, 17e 4-5

CHAPTER 4 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

1 Joseph Jewelers purchased display shelves on March 1 for $36,000. If this asset has an

estimated useful life of five years, what is the book value of the display shelves on April

30?

a $600. b $34,800. c $33,600. d $900.

2 The adjusting entry to recognize an unrecorded expense is necessary:

a When an expense is paid in advance.

b When an expense has been neither paid nor recorded as of the end of the accounting

period.

c Whenever an expense remains unpaid at the end of an accounting period.

d Because the accountant is likely to forget to pay these unrecorded expenses.

3 Before any month-end adjustments are made, the net income of Lawrence Company is

$550,000. However, the following adjustments are necessary: office supplies used,

$35,000; services performed for clients but not yet recorded or collected, $12,300;

interest accrued on note payable to bank, $14,100. After adjusting entries are made for

the items listed above, Lawrence Company’s net income would be:

a $541,400.

b $488,600.

c $583,200.

d $513,200.

4 Of the following adjusting entries, which one results in an increase in liabilities and the

recognition of an expense at the end of an accounting period?

a The entry to accrue salaries owed to employees at the end of the period.

b The entry to record revenue earned but not yet collected or recorded.

c The entry to record earned portion of rent previously received in advance from a

tenant.

d The entry to write off a portion of unexpired insurance.

5 The CPA firm auditing Indian Company found that net income had been overstated.

Which of the following errors could be the cause?

a Failure to record depreciation expense for the period.

b No entry made to record purchase of land for cash on the last day of the year.

c Failure to record payment of an account payable on the last day of the year.

d Failure to make an adjusting entry to record revenue which had been earned but not

yet billed to customers.

Chapter 04 – The Accounting Cycle: Accruals and Deferrals

CHAPTER 4 NAME #

10-MINUTE QUIZ B SECTION

Manhattan Park adjusts its books each month and closes its books on December 31 each year.

The trial balance at January 31, 2010, before adjustments, follows:

Debit Credit

Cash …………………………………………………………………………….. $ 6,600

Supplies ……………………………………………………………………….. 5,400

Unexpired Insurance ……………………………………………………… 12,600

Equipment ……………………………………………………………………. 72,000

Accumulated Depreciation: Equipment …………………………... $ 18,000

Unearned Admission Revenue ……………………………………….. 12,000

Capital Stock ………………………………………………………………… 20,000

Retained Earnings, January 1, 2010 ………………………………… 38,200

Admissions Revenue …………………………………………………….. 27,600

Salaries Expense ……………………………………………………….….. 8,100

Utilities Expense …………………………………………………………… 5,700

Rent Expense ……………………………………………………………….. 5,400 _________

$115,800 $115,800

1 Refer to the above data. According to attendance records, $8,200 of the Unearned

Admission Revenue has been earned in January. Compute the amount of admissions

revenue to be shown in the January income statement:

a $35,800. b $19,400. c $8,200. d $3,800.

2 Refer to the above data. At January 31, the amount of supplies on hand is $2,300. What

amount is shown on the January income statement for supplies expense?

a $2,300. b $5,400. c $3,100. d $7,700.

3 Refer to the above data. The equipment has an original estimated useful life of six years.

Compute the book value of the equipment at January 31 after the proper January

adjustment is recorded:

a $1,000. b $71,000. c $53,000. d $60,000.

4 Refer to the above data. Employees are owed $1,200 for services since the last payday

in January to be paid the first week of February. No adjustment was made for this item.

As a result of this error:

a Assets at January 31 are overstated.

b January net income is overstated.

c Liabilities at January 31 are overstated.

d Owners’ equity at January 31 is understated.

5 Refer to the above data. On August 1, 2009, the park purchased a 12-month insurance

policy. The necessary adjusting entry at January 31 includes which of the following

entries? (Hint: The company has adjusted its books on a monthly basis.)

a A debit to Insurance Expense for $1,050.

b A credit to Unexpired Insurance for $11,550.

c A credit to Unexpired Insurance for $1,800.

d A debit to Unexpired Insurance for $10,800.