PROBLEM 26.9

A

SONIC, INC. (concluded)

d.

There are several nonfinancial considerations worth mentioning. First, the company must

try to determine which medium the customers are most likely to use. Second, it must try to

determine future industry trends regarding software distribution. Third, it must evaluate

SOLUTIONS TO PROBLEMS SET B

30 Minutes, Strong PROBLEM 26.1B

MONSTER TOYS

a.

Estimated sales

(

100,000 units

@

$8

)

800,000$

Less estimated incremental costs:

V

ariable manufacturin

g

costs

(

100,000 units

@

$3.00

)

300,000$

Fixed manufacturin

g

costs

(

exce

p

t de

p

reciation

)

60,000

De

p

reciation ex

p

ense

[(

$400,000 – $10,000

)

÷ 3

]

130,000

Cash recei

p

ts 800,000$

Less cash outla

y

s:

V

ariable manufacturin

g

costs 300,000$

Fixed costs

(

other than de

p

reciation

)

60,000

Sellin

g

and

g

eneral ex

p

enses 40,000

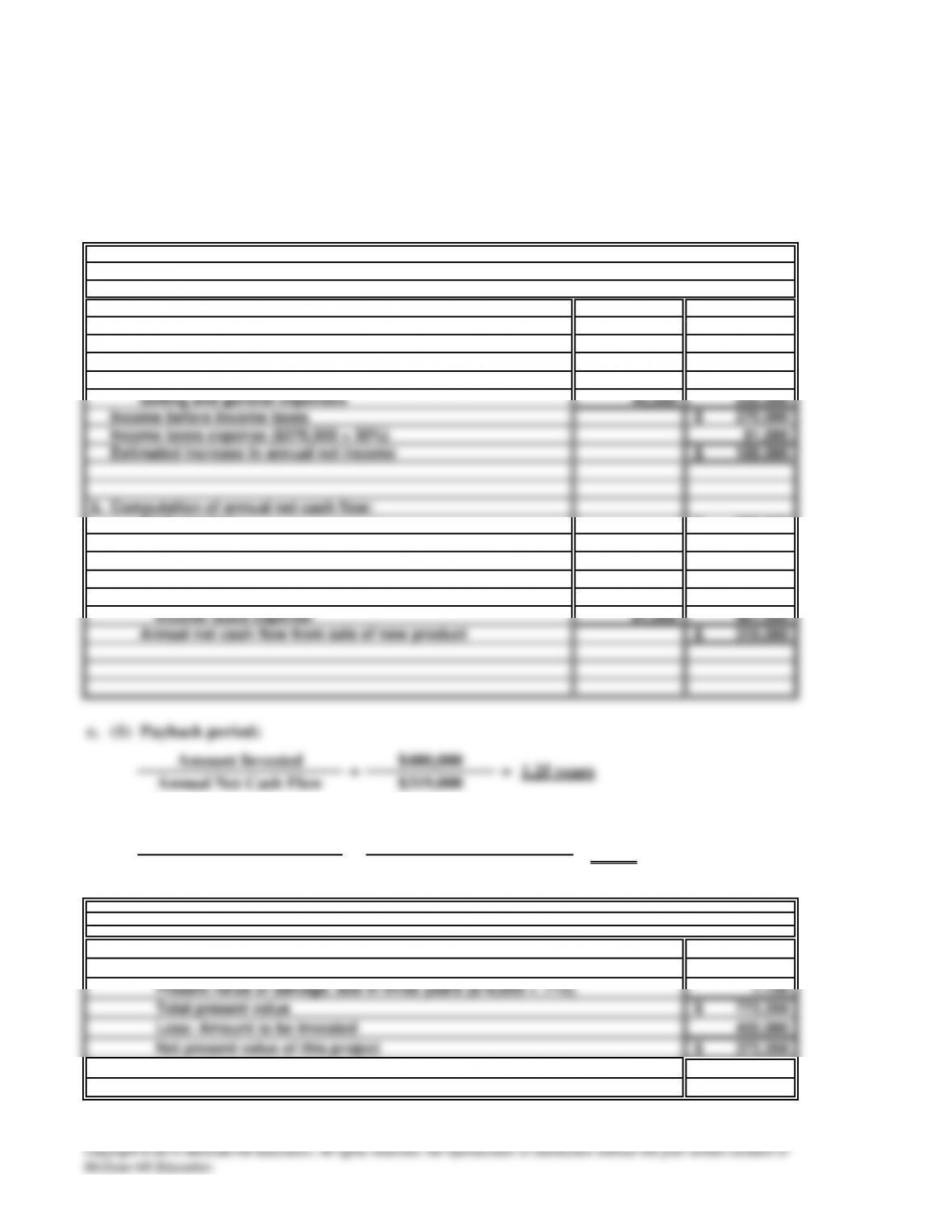

(2)

(3) Net present value of project, discounted at 12%:

Total present value of annual net cash flows ($319,000 × 2.402) 766,238$

MONSTER TOYS

Schedule of Estimated Net Income

= 92.2%

Return on average investment:

Annual Net Income

Average Investment =189,000

($400,000 + $10,000)

2

g

g

p

PROBLEM 26.2B

VIRGINIA TECHNOLOGY

a.

(1)

25 Minutes, Medium

Proposal A

Payback period:

$500,000 ÷ $100,000 = 5 years

25 Minutes, Medium PROBLEM 26.3B

JASON EQUIPMENT CO.

a.

(1)

(1)

Proposal A

Payback period:

$416,000 ÷ $131,200 = 3.2 years

$448,000 ÷ $104,000 = 4.3 years

Payback period:

25 Minutes, Medium PROBLEM 26.4B

SAMBA

a.

(1)

(2)

(

3

)

Net

p

resent value, discounted at 10%:

Total

p

resent value of 10 annual net cash flows

(

$75,000 × 6.145

)

460,875$

Present value of salva

g

e value due in 10

y

ears

(

$10,000 × .386

)

3,860

Total

p

resent value 464,735$

Less: Amount to be invested 300,000

Net

p

resent value of

p

ro

p

osal 164,735$

(1)

(3) Net present value, discounted at 10%:

Total present value of 10 annual net cash flows ($70,000 × 6.145) 430,150$

Present value of salvage value due in 10 years ($40,000 × .386) 15,440

Total present value 445,590$

Less: Amount to be invested 310,000

Net present value of proposal 135,590$

b.

Note to instructor: The net present value calculation is the best of the three capital budgeting

models because it is based on cash flows and because it considers profitability and the time

value of money. Each of the other two simpler models ignores two of these factors.

Based upon the above analysis, Proposal A is the best investment of the two proposals

under consideration. Both proposals have acceptable payback periods (less than the useful

life of fixtures). However, the lower net present value and rate of return on investment of

Proposal B suggests rejection of this proposal. The positive net present value and

acceptable rate of return on investment (higher than management’s required 10%) of

Proposal A indicates that this option is the more profitable alternative.

Proposal B

Payback period:

$310,000 ÷ $70,000 = 4.4 years

($75,000 – $29,000) ÷ [($300,000 + $10,000) ÷ 2]

$46,000 ÷ $155,000 = 29.7%

Proposal A

Payback period:

$300,000 ÷ $75,000 = 4 years

Return on average investment:

25 Minutes, Medium PROBLEM 26.5B

I.C. CREAM

a.

(1)

Proposal A

Payback period:

$4,000,000 ÷ $800,000 = 5 years

30 Minutes, Strong PROBLEM 26.6B

CAFIELD APPLIANCE COMPANY

a.

Estimated sales (15,000 units @ $40) 600,000$

Less estimated incremental costs:

Variable manufacturing costs (15,000 units @ $18) 270,000$

Fixed manufacturing costs (except depreciation) 60,000

Depreciation expense ($300,000 ÷ 5) 60,000

Selling and general expenses 75,000 465,000

Less cash outlays:

Variable manufacturing costs 270,000$

Fixed costs (other than depreciation) 60,000

Selling and general expenses 75,000

Income taxes expense 40,500 445,500

CAFIELD APPLIANCE COMPANY

Schedule of Estimated Net Income

40 Minutes, Strong PROBLEM 26.7B

DOCTORS

a.

$1,500,000

$244,444

The supporting calculations for the above payback figure are:

b.

Payback period:

Amount to Be Invested

Estimated Annual Net Cash Flow = = 6.14 years

Return on average investment:

PROBLEM 26.7B

DOCTORS (concluded)

c. Net present value:

The discounted present value of the incremental annual cash flow o

f

the investment (see part a) discounted at 15% for 9 years is

Net present value (276,713)$

As shown above, the net present value of the MRI investment is negative. Thus

,

we may conclude that the investment’s actual rate of return is less than 15%

.

d. Some of the nonfinancial factors that the doctors should consider include (1) the pace at which MRI

technology is changing, (2) changes in legislation pertaining to government funding of medical

50 Minutes, Strong PROBLEM 26.8B

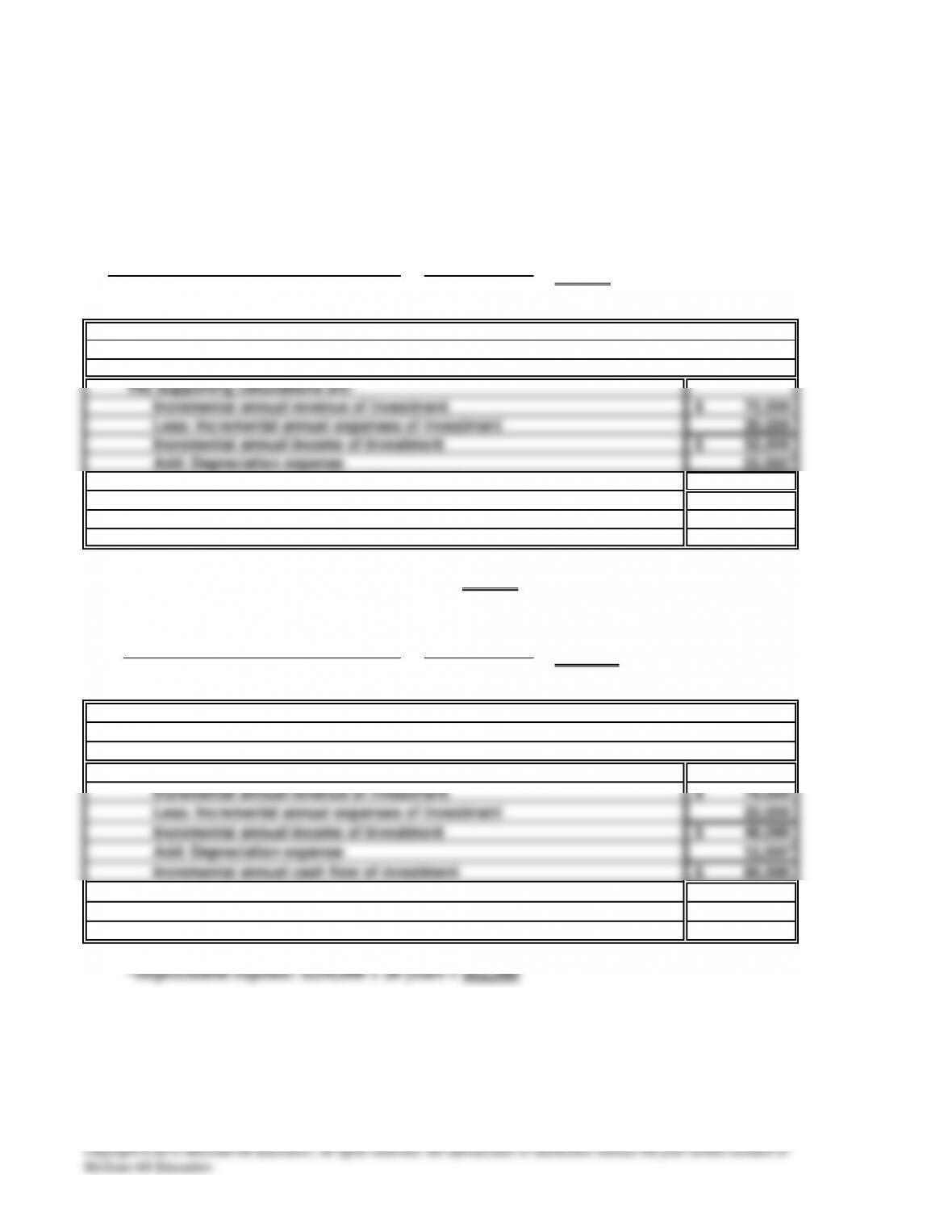

JACKSON MOUNTAIN

a.

$225,000

$75,000

Incremental annual cash flow of investmen

t

75,000$

$250,000

$48,000

The supporting calculations for the payback period figure are:

*Depreciation expense: $225,000 ÷ 10 years = $22,500

Amount to Be Invested

Estimated Annual Net Cash Flow = = 5.2 years

Chairlift

Payback period:

Snow-Making Equipment

Amount to Be Invested

Estimated Annual Net Cash Flow = 3 years

=