Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

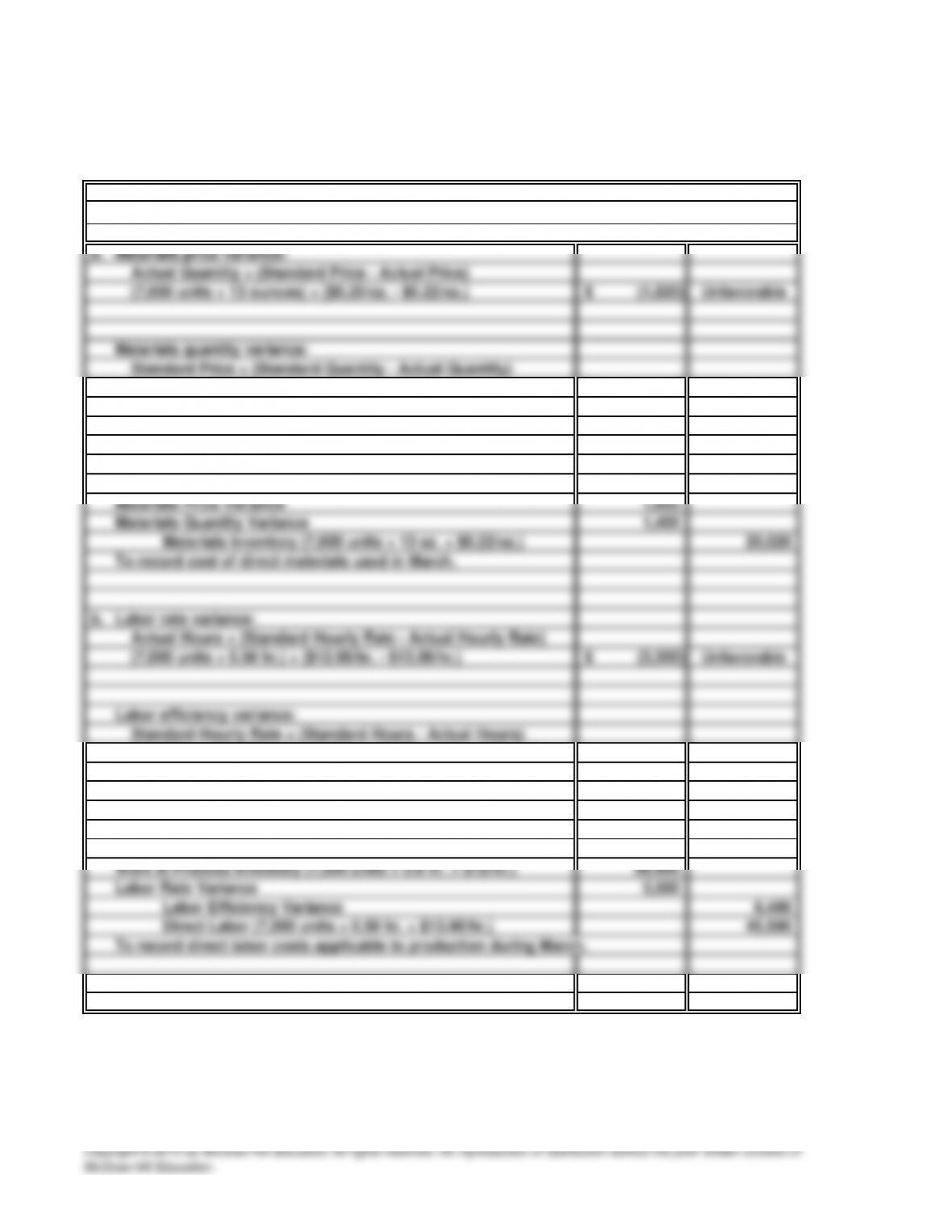

40 Minutes, Strong PROBLEM 24.6B

MONOGLUT, INC.

$0.20/oz. × (84,000 ounces - 91,000 ounces) (1,400)$ Unfavorable

Journal entry to record direct materials used in March:

Work in Process Inventory (7,000 units × 12 oz. × $0.20/oz.) 16,800

$12.00/hr. × [(7,000 units × 0.6 hr.) - (7,000 units × 0.50 hr.)]

$12.00/hr. × 700 hrs. 8,400$ Favorable

Journal entry to record direct labor cost for March:

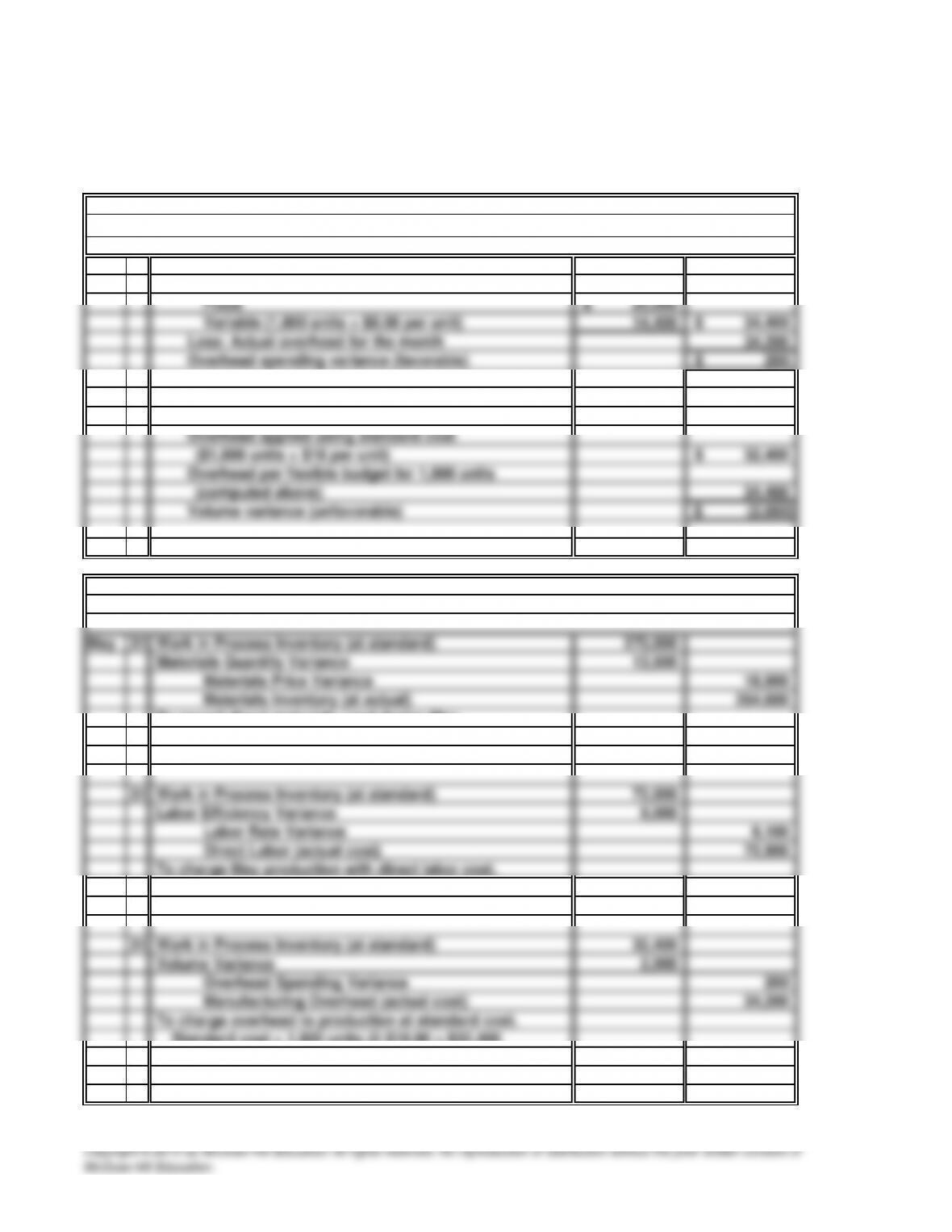

c. Overhead spending variance:

Overhead per flexible budget—7,000 units:

PROBLEM 24.6B

MONOGLUT, INC. (concluded)

PROBLEM 24.7B

COLONIAL FURNITURE CO.

a. (1)

MPV =

(3)

=

Computation of labor rate variance (LRV)

Overhead variances are computed on the following page.

-$9,000 (or $9,000 Unfavorable)

40 Minutes, Strong

Actual Quantity Used × (Standard Price - Actual Price)

Computation of materials price variance (MPV):

(5) Computation of overhead spending variance:

Overhead per flexible budget for 800 units:

(6) Computation of volume variance:

b. General Journal

To record direct materials used during May.

Standard cost = 1,800 units @ $150 = $270,000

Actual cost = 1,800 units @ $147 = $264,600

Standard cost = 1,800 units @ $40.00 = $72,000

Actual cost = 1,800 units @ $40.50 = $72,900

Standard cost = 1,800 units @ $18.00 = $32,400

Actual cost = $34,200

PROBLEM 24.7B

COLONIAL FURNITURE CO. (continued)

PROBLEM 24.7B

COLONIAL FURNITURE CO. (concluded

)

c.

(2) the labor rate variance. The favorable price variance may indicate that the purchasing

department is doing an excellent job of securing materials at advantageous prices. The

favorable labor rate variance may indicate that the number of lower paid inexperienced

workers used during the period was higher than normal. If so, their inexperience may help to

explain the unfavorable labor efficiency variance.

Comments on cost variances:

a.

=

=

=

=

c.

d.

=

=

Thus, the standard hours allowed = $35,000 ÷ $10 = 3,500 hours.

Standard Hourly Rate × (Standard Hours - Actual

Hours)

$10 per hour × (Standard Hours - 4,000 hours)

-$5,000

Based on the journal entry to charge direct labor costs to work in process, the standard

direct labor hours allowed during May is determined as follows:

Thus, the actual hourly rate incurred = -$48,000 ÷ -4,000 = $12 per hour.

Labor Efficiency Variance

$9,500

$7 (Standard Quantity)

*The 1,500 pounds figure was calculated in part a above.

Thus, the standard quantity allowed = 9,500 ÷ 7 = 1,357 pounds.

Based on the journal entry to charge direct labor costs to work in process, the average per

-$1,000 $7 per pound × (Standard Quantity - 1,500 pounds*)

$7 (Standard Quantity) - $10,500

-$1,000

60 Minutes, Strong PROBLEM 24.8B

FODING CORPORATION

Based on the journal entry to charge direct materials costs to work in process, the actual

quantity of material purchased and used during May is determined as follows:

Materials Price

Actual Quantity Used × (Standard Price - Actual Price)

e.

PROBLEM 24.8B

FODING CORPORATION (concluded)

Based on the journal entry to charge overhead costs to work in process, the following

relationships exist: