a.

b. =

c. =

PROBLEM 24.9A

ANTON COMPANY

220 stands × 3 square feet per stand = 660 square feet.

45 Minutes, Medium

Since the direct materials quantity variance is $0, the actual quantity of materials used per

stand must equal the budgeted quantity per stand. Thus, the total quantity purchased and

used is:

Standard Hourly Rate × (Standard Hours – Actual Hours)

Labor Efficiency Variance

Labor Rate Variance Actual Labor Hours × (Standard Rate – Actual Rate)

b.

=

=

Standard Price × (Standard Quantity – Actual Quantity)

The materials quantity variance (MQV) is first used to find the standard quantity of material

allowed for producing 1,520 units (MQV is half MPV):

MQV

Thus, we may solve for the Standard Quantity as follows:

SOLUTIONS TO PROBLEMS SET B

25 Minutes, Strong

-$6,400

PROBLEM 24.1B

UNDEM

$40/lb – (Standard Quantity – 3,200 pounds)

PROBLEM 24.2B

DYELOT INDUSTRIES

a.

MPV =

30 Minutes, Medium

Computation of materials price variance (MPV):

Actual Quantity Used × (Standard Price – Actual Price)

PROBLEM 24.2B

DYELOT INDUSTRIES (concluded)

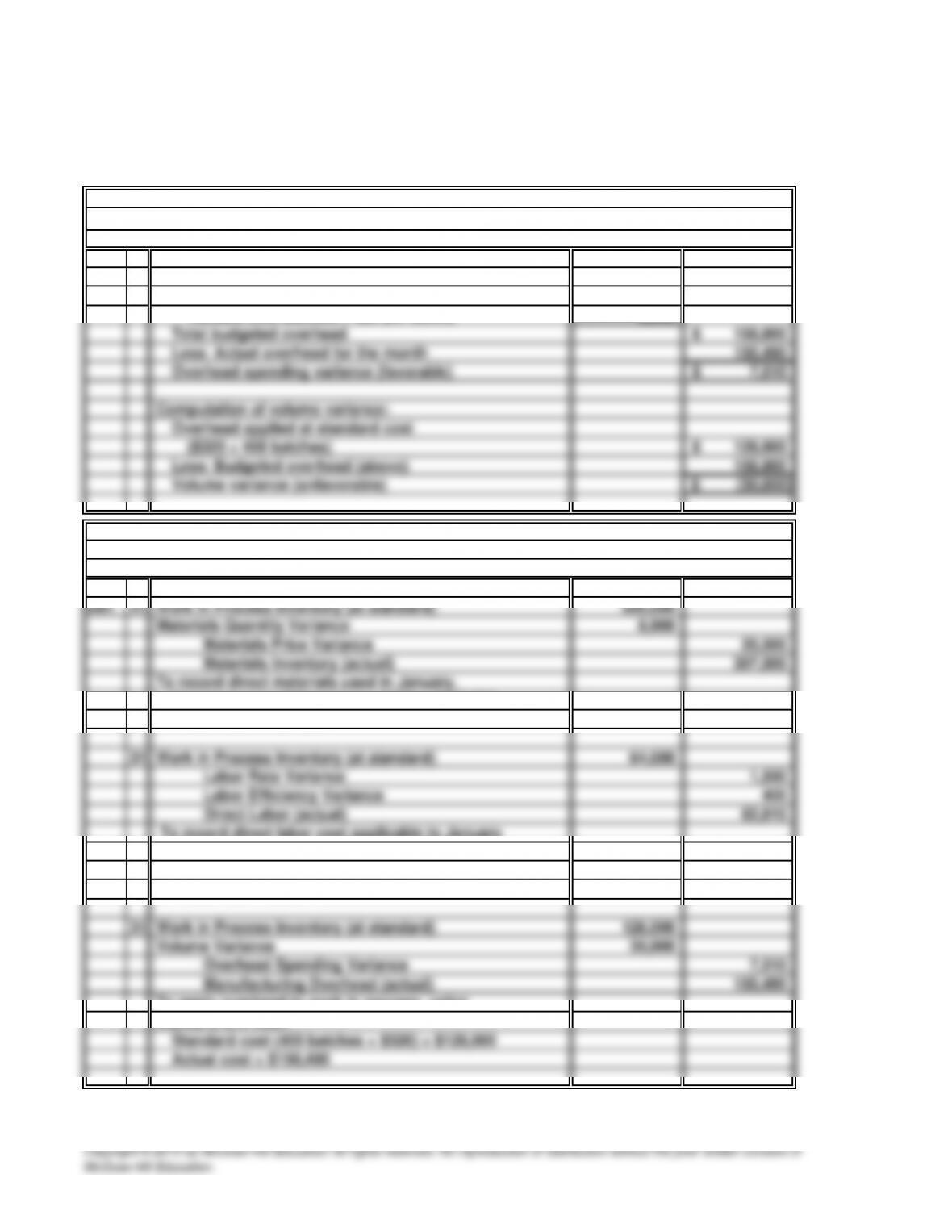

Computation of overhead spending variance:

Overhead budgeted for 400 batches:

Fixed 150,000$

V

ariable (400 batches × $20 per batch) 8,000

V

b. General Journal

Standard cost (400 batches × $800) = $320,000

Actual cost = $307,500

To record direct labor cost applicable to Januar

y

production:

Standard cost (400 batches × $160) = $64,000

Actual cost = $62,010

To apply overhead to work in process, using

standard unit cost:

25 Minutes, Medium PROBLEM 24.3B

LATIN SILK PRODUCTS

a.

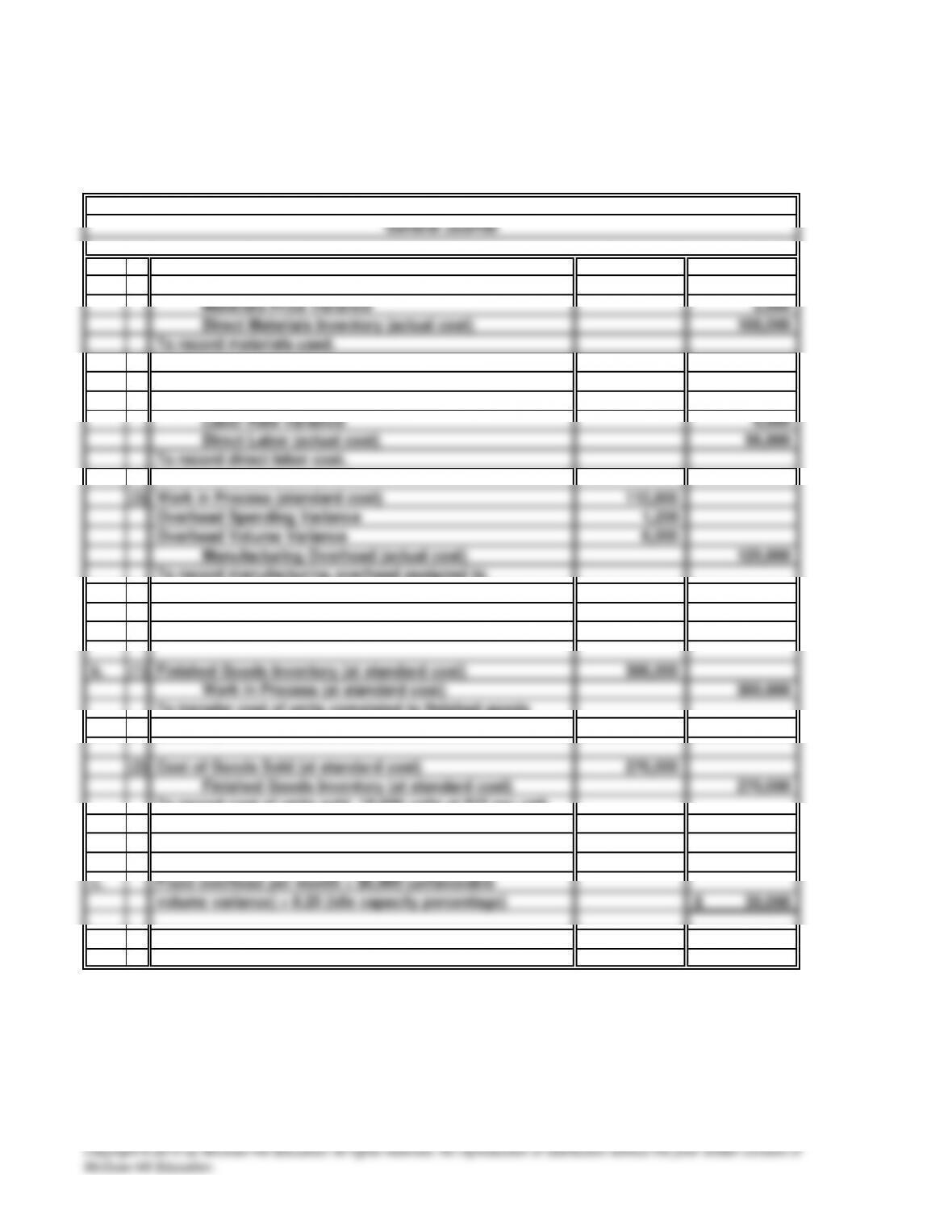

(1) Work in Process (standard cost) 100,000

Materials Quantity Variance 10,000

(2) Work in Process (standard cost) 94,000

Labor Efficiency Variance 8,000

To record manufacturing overhead assigned to

production, and to record overhead variances.

To transfer cost of units completed to finished goods

inventory, 20,000 units at $15 per unit.

To record cost of units sold, 18,000 units at $15 per unit.

a. =

=

=

=

=

b. =

=

=

=

=

=

45 Minutes, Strong

Materials Price Variance Actual Quantity Used × (Standard Price – Actual Price)

170,000 pounds × ($5.00 – $4.80*)

PROBLEM 24.4B

HANS ENTERPRISES

Labor Efficiency Variance Standard Hourly Rate × (Standard Hours – Actual

Hours)

$8.25 per hour × (2,400 hours* – 2,500 hours)

Labor Rate Variance Actual Labor Hours × (Standard Rate – Actual Rate)

2,500 hours × ($8.25 – $8.00*)

Materials Quantity Variance Standard Price × (Standard Quantity – Actual

Quantity)

*Actual Rate per Hour = $20,000/2,500 hours = $8.00/hour

-$825 Unfavorable

$625 Favorable

$30,000 Unfavorable

*Standard Quantity Allowed = 160 batches × 1,025 pounds/batch = 164,000 pounds

$5.00 per pound × (164,000 pounds* – 170,000

pounds)

c.

Overhead

Costs Applied

PROBLEM 24.4B

HANS ENTERPRISES (continued)

Overhead variances:

Actual Overhead

Costs Incurred

Costs Allowed

Standard Overhead

g

.

844,920 844,920*

PROBLEM 24.4B

HANS ENTERPRISES (concluded)

Entry to transfer the 160 batches of crow bait produced in June to finished goods:

Finished Goods Inventory (at standard cost) …………………………

a. =

=

=

=

b. =

$1.32 per gallon × (30,000 gallons* – 34,000 gallons)

Actual Labor Hours × (Standard Rate – Actual Rate)

-$5,280 (or $5,280 Unfavorable)

*Standard Quantity Allowed = 10,000 cases × 3.0 gallons/case = 30,000 gallons

Labor Rate Variance

Quantity)

45 Minutes, Strong

Actual Quantity Used × (Standard Price – Actual Price)

34,000 gallons × ($1.32 – $1.28*)

Materials Price Variance

PROBLEM 24.5B

SMOOTH CORPORATION

c.

d. (1) 39,600 *

5,280

…

(3) 21,200

52

…

…

116,200

Direct Labor (at actual cost) ………………………………………………

…

Work in Process Inventory (at standard cost) …………………

…

To record the cost of direct labor charged to production.

*10,000 actual cases × 0.80 hours allowed per case × $15 per hour = $120,000

Overhead Volume Variance (unfavorable) ……………………

…

…

8,300Labor Rate Variance (favorable) …………………………………………

…

Materials Price Variance (favorable) …………………………………

…

43,520

1,360

Direct Materials Inventory (at actual cost) ……………………………

Costs Applied

Actual Overhead

Costs Incurred Standard Overhead

Work in Process Inventory (at standard cost) ……………

…

Materials Quantity Variance (unfavorable) ………………

…

*Standard Variable Overhead Allowed = $1.60/case × 10,000 cases = $16,000

PROBLEM 24.5B

SMOOTH CORPORATION (concluded)

Overhead variances:

Overhead