Ex. 24.6

(continued) c.

Ex. 24.7 a.

b.

c.

Extended hours worked during the period may have resulted in an

increased average wage rate due to overtime wage premiums. This may

Standard price, $6.80 per pound

$6.80/lb.

Standard price, $6.80 per pound

The materials quantity variance is found by multiplying the standard

materials price by the difference between the standard quantity of

materials and the actual quantity used. The standard price of materials,

$6.80/lb., was determined in part a, above.

Actual quantity of materials used, 4,000 pounds

In computing the materials quantity variance, the actual quantity of

Ex. 24.8

(continued) b.

Ex. 24.9

$ 360,000

75,000

One explanation of the variances is that higher skilled workers were hired at

wages greater than the budgeted rate. The higher skilled workers may have

Overhead spending variance:

Fixed ………………………………………………

…

Variable ($3 per unit × 25,000 units) ……………

…

Overhead budgeted for actual production (25,000 units):

Ex. 24.11

(continued)

Ex. 24.12

Overhead rate per unit = $10 per labor hr. × 2 labor hours per unit = $20 per unit

Overhead applied = 4,500 actual production units × $20 per unit = $90,000

Volume variance = $90,000 $94,000 (from part a) = $4,000 Unfavorable

unfavorable volume variance, reflecting that actual production was less than

budgeted production. The overhead spending variance was favorable, due to fixed

costs that were $2,000 lower than expected ($40,000 $38,000) and variable costs

that were $1,000 higher than allowed at the actual production level ($54,000

$55,000). Zeta’s manager may want to investigate why the variable overhead costs

per unit were higher than expected and determine if it is linked to the lower fixed

costs. As long as Zeta is meeting its sales demand, the unfavorable volume variance

may not require any corrective action.

The entry to close McGill’s unfavorable overhead spending variance required that the

variance account be credited for $600. Given that the Cost of Goods Sold account was

Ex. 24.14 a. A favorable materials price variance results from the purchasing department being

able to acquire direct materials at a price below standard cost. This may result from

finding a lower price supplier or from obtaining discounts for quantity purchases.

The manager of the purchasing department (purchasing agent) is responsible for

use of materials and is responsible for the materials quantity variance. If, however,

Ex. 24.15

Several items from the Store Sales and Other Data section of Home Depot’s 5-Year

Summary could be used to create direct labor standards. For example, weighted average

sales per store per employee, number of customer transactions per employee, and

average ticket price per employee are three that seem obvious. Below are suggestions or

25 Minutes, Strong PROBLEM 24.1A

a. MPV =

=

=

= 20 (Standard Quantity) – 16,000

= 20 (Standard Quantity)

= (Standard Quantity) = 760 pounds for 760 units.

780 units × 1.00 pound per unit = 780 pounds, standard quality of materials allowed for

Thus, we may solve for the Standard Quantity as follows:

15,200 ÷ 20

-800

760 pounds divided by 760 units = 1.00 pound per unit.

$1,600 (or $1,600 Unfavorable)

15,200

SOLUTIONS TO PROBLEMS SET A

Actual Quantity × (Standard Price – Actual Price)

800 pounds × ($20/lb – $22/lb)

BRADLE

Y

PROBLEM 24.2

A

A

GRICHEM INDUSTRIES

a.

MPV =

30 Minutes, Medium

Computation of materials price variance (MPV):

Actual Quantity Used × (Standard Price – Actual Price)

PROBLEM 24.2A

AGRICHEM INDUSTRIES (concluded)

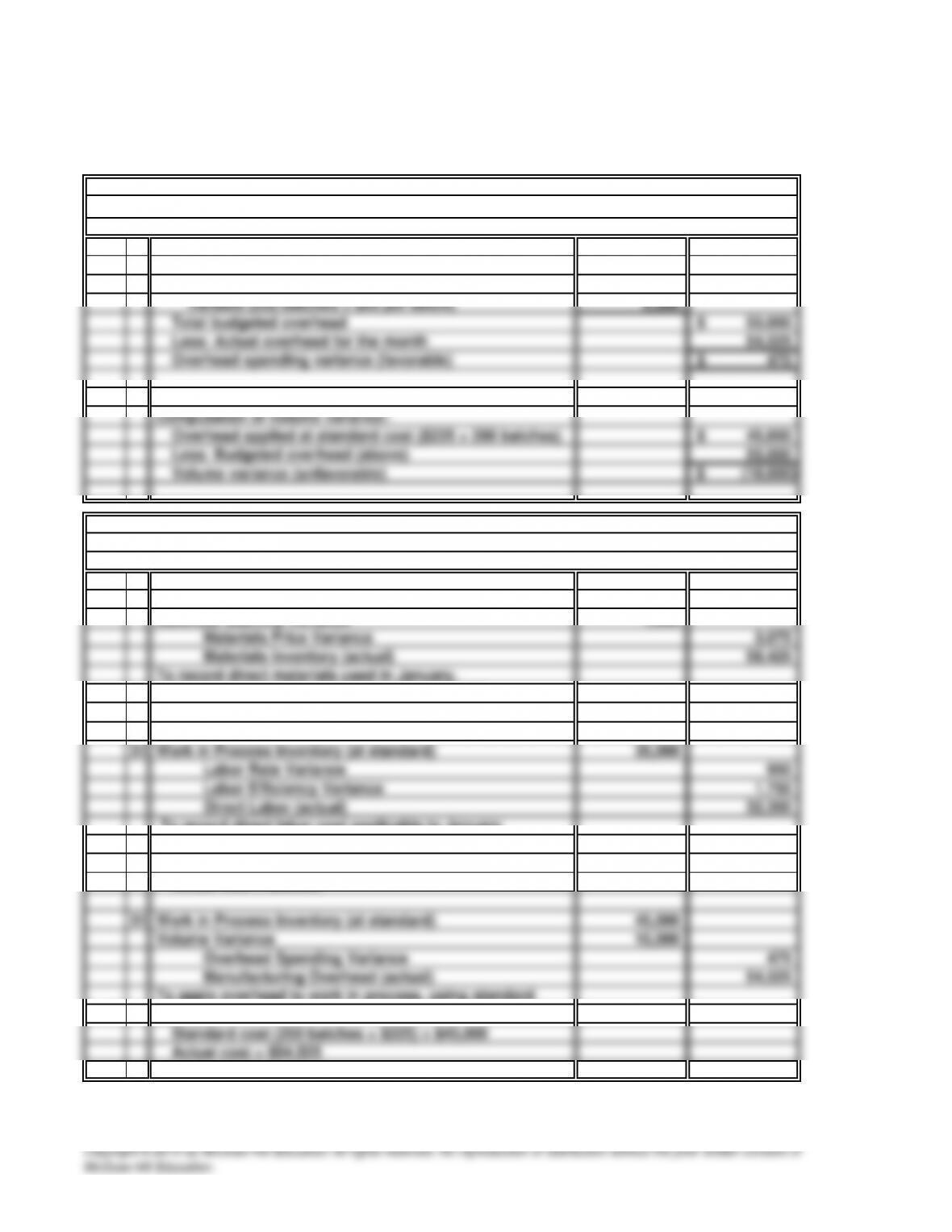

Computation of overhead spending variance:

Overhead budgeted for 200 batches:

Fixed 50,000$

V

ariable (200 batches × $25 per batch) 5,000

Total budgeted overhead 55,000$

Less: Actual overhead for the month 54,525

Overhead spending variance (favorable

)

475$

Computation of volume variance:

Overhead applied at standard cost ($225 × 200 batches) 45,000$

Less: Budgeted overhead (above) 55,000

V

olume variance (unfavorable) (10,000)$

b. General Journal

Jan. 31 Work in Process Inventory (at standard) 60,000

Materials Quantity Variance 1,500

Standard cost (200 batches × $300) = $60,000

Actual cost = $58,42

5

To record direct labor cost applicable to Januar

y

production:

Standard cost (200 batches × $175) = $35,000

Actual cost = $32,300

To apply overhead to work in process, using standard

unit cost:

5

25 Minutes, Medium PROBLEM 24.3A

AMERICAN HARDWOOD PRODUCTS

General Journal

a. (1) Work in Process (standard cost) 90,000

Materials Quantity Variance 8,400

(2) Work in Process (standard cost) 84,000

Labor Efficiency Variance 1,500

(3) Work in Process (standard cost) 115,500

Overhead Spending Variance 3,240

Overhead Volume Variance 4,500

(2) Cost of Goods Sold (at standard cost) 264,000

Finished Goods Inventory (at standard cost) 264,000

a. =

=

=

=

=

=

b. =

=

=

$29,690 Favorable

*Actual Price per Pound = $593,800/148,450 pounds = $4.00/pound

Materials Quantity Variance

$1,100 Favorable

Standard Price × (Standard Quantity – Actual

Quantity)

$4.20 per pound × (149,940 pounds* – 148,450 pounds)

$6,258 Favorable

*Standard Quantity Allowed = 147 batches × 1,020 pounds/batch = 149,940 pounds

Labor Rate Variance Actual Labor Hours × (Standard Rate – Actual Rate)

2,200 hours × ($8.50 – $8.00*)

45 Minutes, Strong

Materials Price Variance Actual Quantity Used × (Standard Price – Actual Price)

148,450 pounds × ($4.20 – $4.00*)

PROBLEM 24.4A

SVEN ENTERPRISES

c.

Overhead

Costs Applied

Costs Allowed

Actual Overhead

Costs Incurred

Problem 24.4A

SVEN ENTERPRISES (continued)

Overhead variances:

Standard Overhead