CHAPTER 2

4

STANDARD COST SYSTEM

S

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 24.1 Variances and normal capacity 24-1, 24-2, 24-

5

Analysis, judgment

B. Ex. 24.2 Standard cost applied to production 24-3 Analysis

B. Ex. 24.3 Expected volume variance 24-4 Analysis

B. Ex. 24.4 Volume and spending variances 24-4, 24-5 Analysis

B. Ex. 24.5 Normal vs. ideal standard costs 24-2, 24-5 Analysis, communication,

judgment

B. Ex. 24.6 Computing labor cost variances 24-1, 24-3, 24-

5

Analysis, judgment

B. Ex. 24.7 Journal entry for direct labor 24-3 Analysis

B. Ex. 24.8 Computing materials cost variances 24-3 Analysis

B. Ex. 24.9 Journal entry for direct materials 24-3 Analysis

B. Ex. 24.10 Overhead cost variances 24-4 Analysis, communication

Learning

Exercises Topic Objectives Skills

24.1 Accounting terminology 24-1–24-5 Analysis

24.2 Relationships among standard costs, actual

costs, and cost variances 24-3, 24-4 Analysis

24.3 Understanding materials cost variances 24-3, 24-5 Analysis, judgment

24.4 Computing materials cost variances and

volume variance 24-3–24-5 Analysis, judgment

24.5 Manufacturing overhead variances 24-4, 24-5 Analysis, judgment

24.6 Computing labor cost variances 24-1, 24-3,

24-5 Analysis, communication,

judgment

24.7 Elements of materials cost variances 24-3 Analysis

24.8 Interpreting variances 24-5 Analysis, communication,

judgment

24.9 Computing overhead cost variances 24-4 Analysis

24.10 Overhead journal entries 24-4 Analysis

24.11 Overhead cost variances 24-4, 24-5 Analysis

24.12 Understanding overhead variances 24-4 Analysis, communication,

judgment

24.13 Computing materials and labor variances 24-3 Analysis

24.14 Causes of cost variances 24-1, 24-3,

24-5 Analysis, communication,

judgment

24.15 Real World: Standards for Home Depot 24-1, 24-5 Analysis, communication,

judgment, research

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Problems Learning

Sets A, B Topic Objectives Skills

24.1 A,B Understanding materials cost variances and

volume variance 24-3–24-5 Analysis, judgment,

communication

24.2 A,B Computing and journalizing cost variances 24-3, 24-4 Analysis

24.3 A,B Computing and journalizing cost variances 24-3, 24-4 Analysis

24.4 A,B Computing and journalizing cost variances 24-3, 24-4 Analysis

24.5 A,B Computing and journalizing cost variances 24-3, 24-4 Analysis

24.6 A,B Computing and journalizing cost variances 24-3, 24-4 Analysis

24.7 A,B Computing, journalizing, and analyzing cost

variances 24-3–24-5 Analysis, communication,

judgment

24.8 A,B Understanding cost variances: solving for

missing data 24-1, 24-3,

24-4 Analysis, judgment

24.9 A,B Understanding variance calculations 24-3, 24-4 Analysis

Critical Thinking Cases

24.1 It’s not my fault 24-1, 24-3 –

24-5 Analysis, communication,

judgment

24.2 Determination and use of standard costs 24-1, 24-3 –

24-5 Analysis, communication,

judgment

24.3 Real World: Travelocity.com 24-2, 24-5 Analysis, communication,

(Internet) Standards for travel costs judgment, research,

technology

24. 4 Standard cost systems and inventory

misstatement 24-4 Analysis, communication,

judgment, research,

(Ethics, fraud and corporate governance) technology

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

24.1 A,B Bradle

y

/Undem 25 Strong

Materials variances must be computed with missing data. The problem

requires an understanding of relationships among variances, including a

volume variance.

24.2 A,B A

g

riChem Industries/D

y

elot Industries 30 Medium

Compute cost variances for direct materials, direct labor, and overhead,

and prepare journal entries to record manufacturing costs in a standard

cost system.

24.3 A,B American Hardwood Products/Latin Silk Products 25 Medium

Prepare journal entries to record cost variances and the costs incurred in

the Work in Process account. Also record cost of units completed and

cost of units sold. Compute fixed manufacturing overhead.

24.4 A,B Sven Enter

p

rises/Hans Enter

p

rises 45 Strong

A comprehensive problem requiring knowledge of all variances and

corresponding journal entries.

24.5 A,B Slick Cor

p

oration/Smooth Cor

p

oration 45 Strong

A comprehensive problem requiring knowledge of all variances and

corresponding journal entries.

24.6 A,B Pol

yg

laze, Inc./Mono

g

lut, Inc. 40 Strong

Compute cost variances and prepare journal entries to record the flow of

manufacturing costs through a standard cost accounting system.

24.7 A,B Herita

g

e Furniture Co./Colonial Furniture Co. 40 Strong

A comprehensive standard cost problem. Requires computation of cost

variances, journal entries, and an analysis of the company’s strengths and

weaknesses.

24.8 A,B Ri

p

le

y

Cor

p

oration/Fodin

g

Cor

p

oration 60 Stron

g

This is a comprehensive problem with missing data. An analytical

approach is required. This would be an excellent problem to assign to

small groups or to teams of students.

24.9 A,B Anton Com

p

an

y

/Ninna Com

p

an

y

45 Medium

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates

assume use of the partially filled-in working papers.

Problems (Sets A and B)

Given budget items and a variance report, the student is asked to solve

for various actual amounts. Also, the meaning of favorable and

unfavorable variances must be applied. A good comprehensive review

problem well suited for a group assignment.

Critical Thinking Cases

24.1 It’s Not M

y

Fault 25 Stron

g

Cabinets, Inc.

In a company using standard costs and a responsibility cost accounting

system, who should be charged with the responsibility for unfavorable

labor rate variances incurred when the production department works

overtime to fill “rush” orders?

24.2 Armstrong Chemical 50 Strong

Evaluate arguments given by the president of a company against the

revision of standard costs and the value assigned to inventory. Assuming

that standards for the year just ended should be revised, determine the

value of ending inventory using revised standard costs.

24.3 Travelocity.com 30 Medium

Internet

Students are given a budgeted amount for travel to a given destination.

Using actual ticket prices obtained from travelocity.com they calculate a

current spending variance. Factors that might affect the reasonability of

the budgeted amount are also discussed.

24.4 Standard Cost Systems and Inventory Misstatements 30 Medium

Ethics, Fraud & Corporate Governance

Jams and Jellies, Inc.

The ethical problems created by inappropriate standards are explained.

Students visit the IMA website for this research.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

2.

3.

4.

5.

1. Standard costs are predetermined estimates of what it should cost to produce a product or to

perform a particular operation under normal conditions. The use of a standard cost helps

The statement is incorrect because job order and process are the names of cost accounting

Standard costs are developed from a set of assumptions about future (budgeted) prices, wages,

production methods, and normal production levels. If unexpected changes in prices, such as the

Variances from standard cost that are generally computed are:

The production manager exercises a degree of control over the quantities of materials used in the

production process and is therefore responsible for the materials quantity variance. However, the

8.

9.

10.

11.

12.

13.

Direct materials and direct labor are variable costs that are directly traceable to the product.

Immaterial standard variance account balances are added to (for unfavorable variances-debit) or

Overtime hours are normally paid at a higher rate than regular hours. Also, overtime hours are

When a company operates at 100% capacity, there is no margin for any errors. Thus, there are

no sick workers, no equipment down time, no late shipments of supplies or materials, etc. A

The selling price of the finished product includes a consideration of the quality of the direct

materials used to create the finished product. Of course the quality of the direct materials is

A plant accountant might want to consult with the manager or supervisor of the production line

B. Ex. 24.1

B. Ex. 24.2

B. Ex. 24.3

SOLUTIONS TO BRIEF EXERCISES

The standard direct labor applied to production was $92,100 (actual direct labor of

Production = 780 units

The problem at Bramford Industries is a result of operating well above normal capacity.

The standard rates and efficiencies were based on normal operations. Because

Overhead applied to work in process

B. Ex. 24.7 The direct labor journal entry for Loring Glassware in September is:

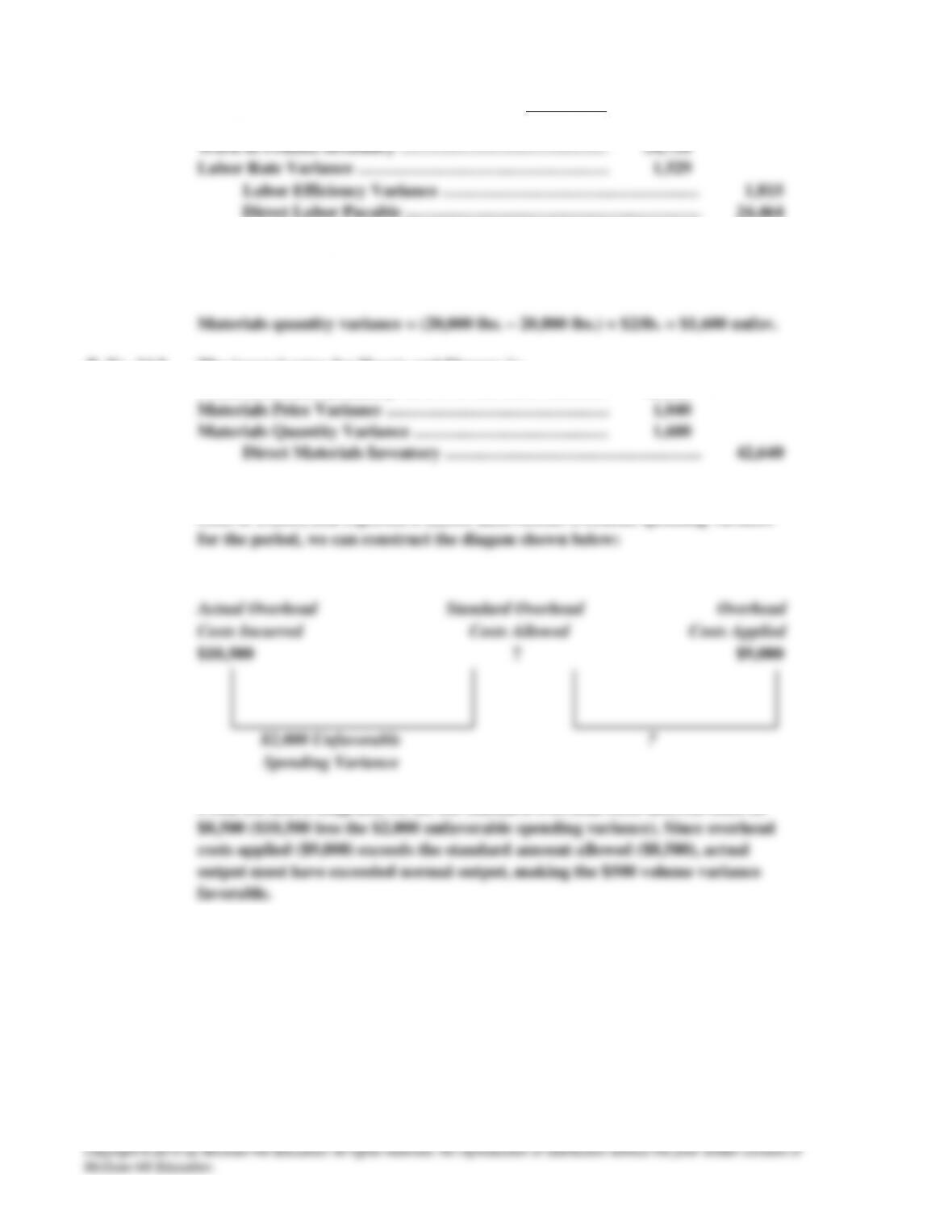

From the above diagram, we see the standard overhead costs allowed must be

Ex. 24.1 a.

b.

SOLUTIONS TO EXERCISES

Standard costs

Labor efficiency variance

Ex. 24.4 a.

Materials Price Variance =

b.

= Standard Price × (Standard Quantity

–

c.

Ex. 24.6 a.

Labor Rate Variance =

=

=

*Actual Rate per Hour

b.

= Standard Rate × (Standard Hours –

Actual Hours)

= $16 per hour × (4,500 hours* – 3,600

hours)

= $14,400 Favorable

= 9,000 units × 0.5 hours/unit = 4,500

hours

*Standard Hours Allowed

Marlo’s labor rate variance is computed as follows:

Labor Efficiency Variance

Marlo’s labor efficiency variance is computed as follows:

$64,800 ÷ 3,600 hours = $18/hour

Actual Labor Hours × (Standard Rate –

Actual Rate)

3,600 hrs. × ($16 – $18*)

-$7,200 (or $7,200 Unfavorable)

Gumchara’s overhead volume variance will be favorable because its actual

Gumchara’s materials price variance is computed as follows:

Actual Quantity Used × (Standard Price –

Gumchara’s materials quantity variance is computed as follows:

Materials Quantity Variance