30 Minutes, Strong PROBLEM 23.5B

SYNDER’S

a. Budgeted income statement:

Budgeted sales 100,000$

Cost of goods sold (60% of sales) 60,000

Gross profit (40% of sales) 40,000$

Income taxes (25%) 5,500

Budgeted net income 16,500$

b. Cash budget:

Beginning cash, May 1 30,000$

Add: Collections on March sales (10% × $90,000) 9,000

Variable selling & administrative costs

(5% × $100,000 sales) 5,000

Fixed selling & administrative costs

($10,000 – $3,000) 7,000

Debt service payments 4,000

for production.

* Ensures the cooperation of different departments within

a company to meet the expected production levels.

For example, the HR department must provide an

adequate number of employees to produce the expected

finished good.

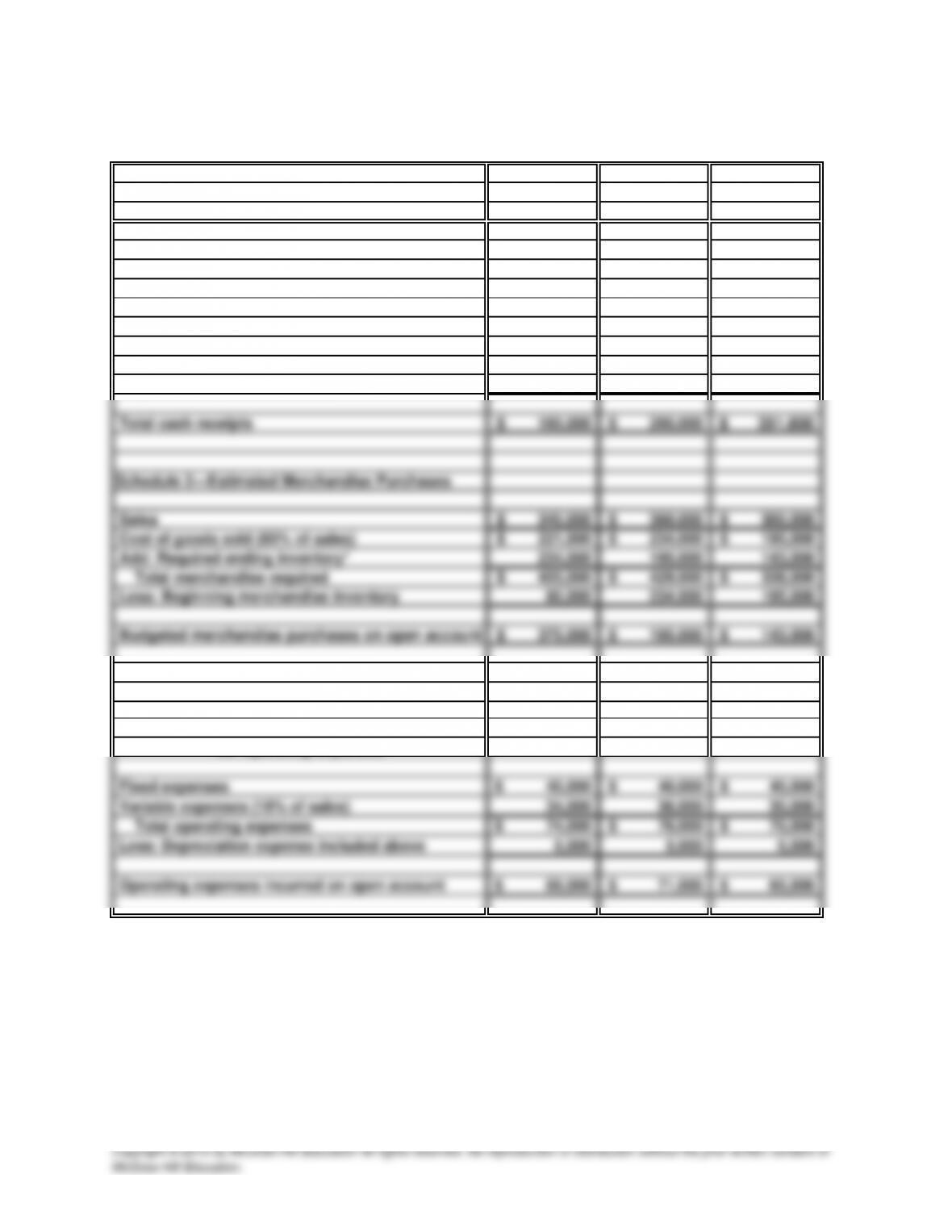

60 Minutes, Strong PROBLEM 23.6B

HOFFMAN INDUSTRIES

a.

July August September

Supporting Schedules

Schedule 1—Estimated Cash Collections

on Receivables

Receivables outstanding at June 30 160,000$ 40,000$

July sales—75% × $340,000 255,000

24% × $340,000 81,600$

August sales—75% × $360,000 270,000

*Cost of goods sold for October, 65% ×

$220,000, or $143,000.

Schedule 3—Estimated Cash Payments

for Operating Expenses

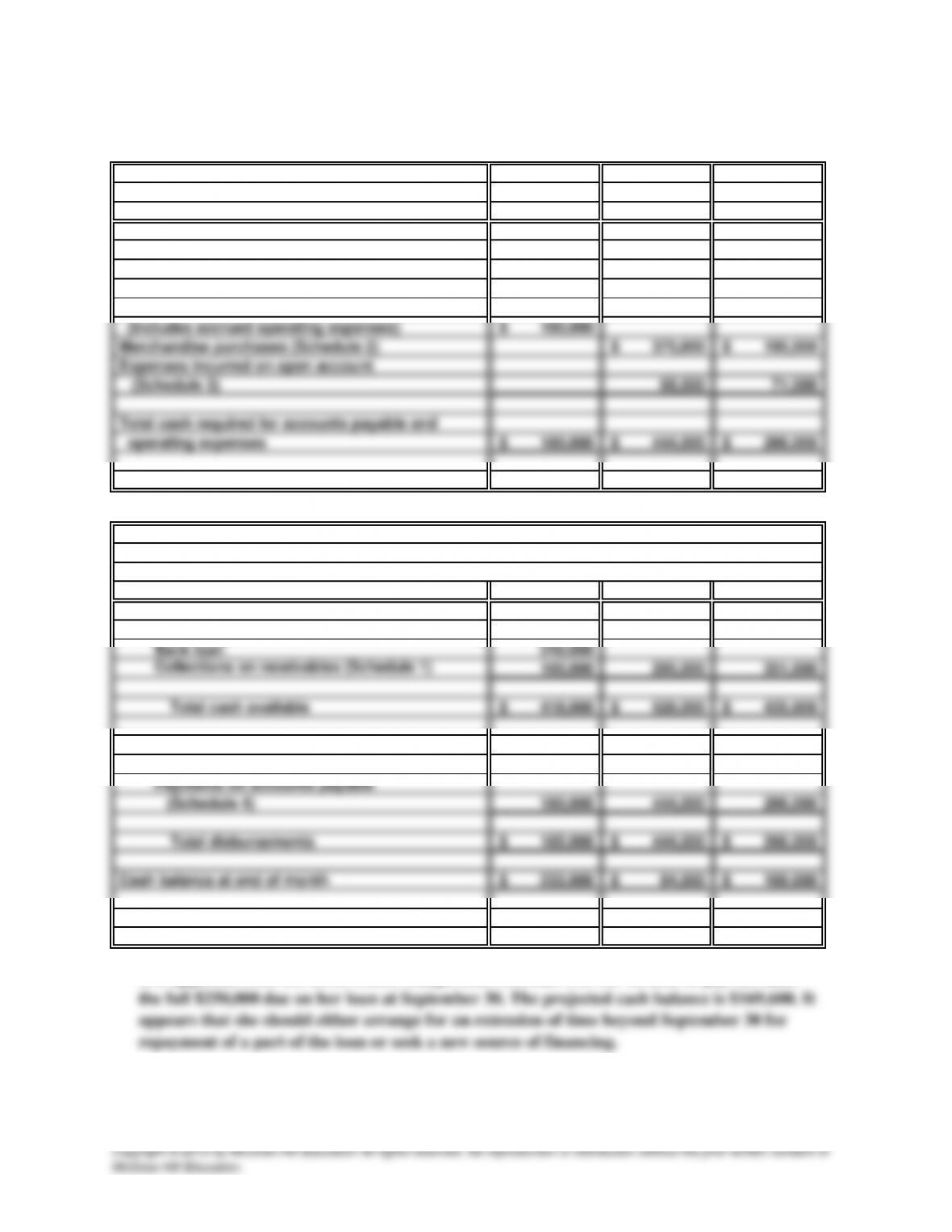

PROBLEM 23.6B

HOFFMAN INDUSTRIES (concluded)

July August September

Schedule 4—Estimated Cash Payments

on Accounts Payable (Including

Operating Expenses)

Accounts payable balance on June 30

b. HOFFMAN INDUSTRIES

Cash Budget

For Third Quarter of Current Year

July August September

Cash balance at beginning of month 18,000$ 233,000$ 84,000$

Receipts:

Disbursements:

Purchase of equipment 25,000$

It is apparent from the three-month budget that Hoffman will not be able to pay the bank

50 Minutes, Medium PROBLEM 23.7B

EIGHT FLAGS

a. EIGHT FLAGS

Comparison of Budgeted and Actual Revenue and Expenses

For the Year Ended December 31, 20__

Flexible Over (or

Budget Actual Under) Budget

Net sales 18,000,000$ 18,000,000$ 0$

Cost of goods sold 11,700,000 11,160,000 (540,000)

Gross profit on sales 6,300,000$ 6,840,000$ 540,000$

b.

Comment on performance:

Operating income was better than budgeted by $2,360,000. This result may be attributed to

two factors: (1) a better-than-budgeted merchandise purchasing performance; (2) hugely

smaller expenditures than budgeted for selling and promotion expenses, buying expenses and

administrative expenses; (3) in addition, other expenses, such as delivery and building

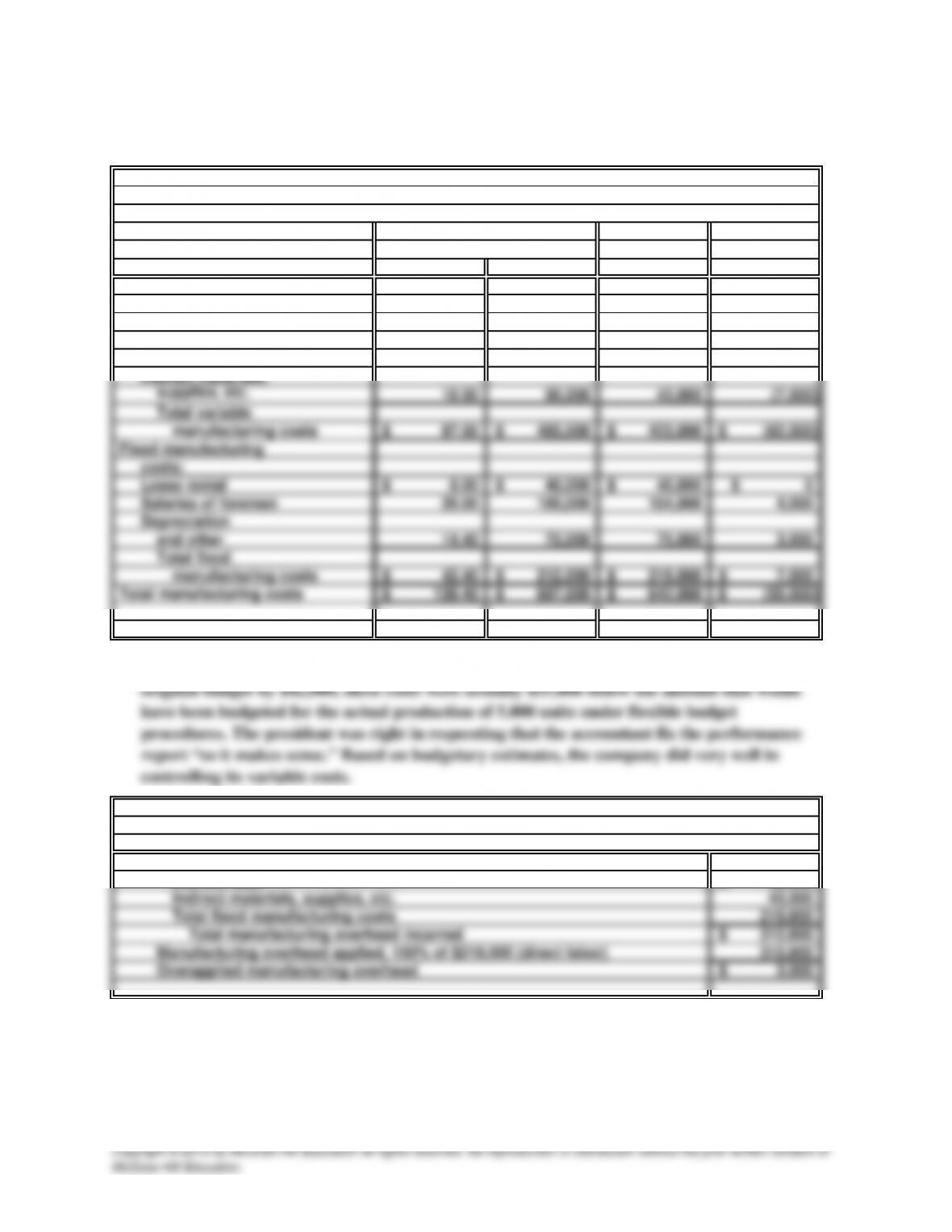

45 Minutes, Medium PROBLEM 23.8B

XL INDUSTRIES

a.

X

L INDUSTRIES

Performance Report fo

r

Widget Production Dept.

For the Year Ended December 31st

Bud

g

eted Costs

A

ctual Ove

r

for 5,000 Units Costs

(

or Under

)

Per Unit Total Incurred Bud

g

e

t

Variable manufacturin

g

costs:

Direct materials 25.00$ 125,000$ 120,000$

(

5,000

)

$

Direct labo

r

50.00 250,000 210,000

(

40,000

)

Indirect labo

r

12.00 60,000 50,000

(

10,000

)

(

)

(

)

b.

r

pp

The revised performance report above shows that although actual costs exceeded the

(

)

•

•

•

•

•

SOLUTIONS TO CRITICAL THINKING CASE

S

We discuss this case in class and call upon specific students to explain various amounts in

their budgeted balance sheets and cash budgets. The students’ assumptions should support

these budgeted amounts.

CASE 23.1

BUDGETING IN A NUTSHELL

30 Minutes, Medium

Amounts of cash sales and credit sales

Collections of accounts receivable

Purchases of inventory [This must exceed $10 (thousand) just to cover the cost of goods

sold.]

Payments on accounts payable

The value of this relatively unstructured problem lies in working it, not in the solution. We

find that it does much to refresh the students’ understanding of both accrual accounting and

cash flows.

Students should state clearly their assumptions concerning:

The amounts appearing in the budgeted statements will vary, depending upon the assumed

amounts. In all cases, however, the budgeted balance sheet should include cash of $50 and

owners’ equity of $195. The cash budget should reflect a net increase of $10 . (Amounts in

thousands)

Cash paid for expenses (There is no depreciation, so this may equal the amount shown in

the income statement).

CASE 23.2

a.

AN ETHICAL DILEMMA

20 Minutes, Medium

The primary purpose of a review (or an audit) by an independent CPA is to provide people

outside of the organization with an independent expert opinion on the fairness of the

presentation. If Gamm believes the receivable from Rembrant should be written off, he

should insist that it is—or make clear his reservations in his report. Beta’s budget of future

operating results has virtually nothing to do with the collectibility of this receivable.

CASE 23.3

a.

CASH BUDGETING

20 Minutes, Medium

Student answers will vary. However, suggestions will likely be based on discussions in the

chapter like: speed up collection of receivables, increase inventory turnover, manage debt

financing more astutely, for example match the length of the loan with the depreciation of

the assets, look for methods to reduce the taxes, review costs for telecommunications,

CASE 23.

4

a.

•

20 Minutes, Medium

The following features of the budgeting software are identified.

BUDGETING SHAREWARE

Prints Statement of Income and Expense—monthly and year to date with the percent of

budgeted amount, and actual through the selected month, budgeted, and variance, in an

annualized format.

CASE 23.5

a.

BUDGETING AND INTERNAL CONTROLS

30 Minutes, Medium

Exhibit 23-2 suggests that a material overstatement of sales will result in planned over-

production and higher budgeted selling and administrative expenses than would be

appropriate. Budgeted cost of goods manufactured and sold will be overstated. In addition,