20 Minutes, Easy PROBLEM 22.7B

EASTRISE CORPORATION

Mower Division Sales = 10,000 units × $600 = $6,000,000

PROBLEM 22.8B

WESTMINSTER, INC.

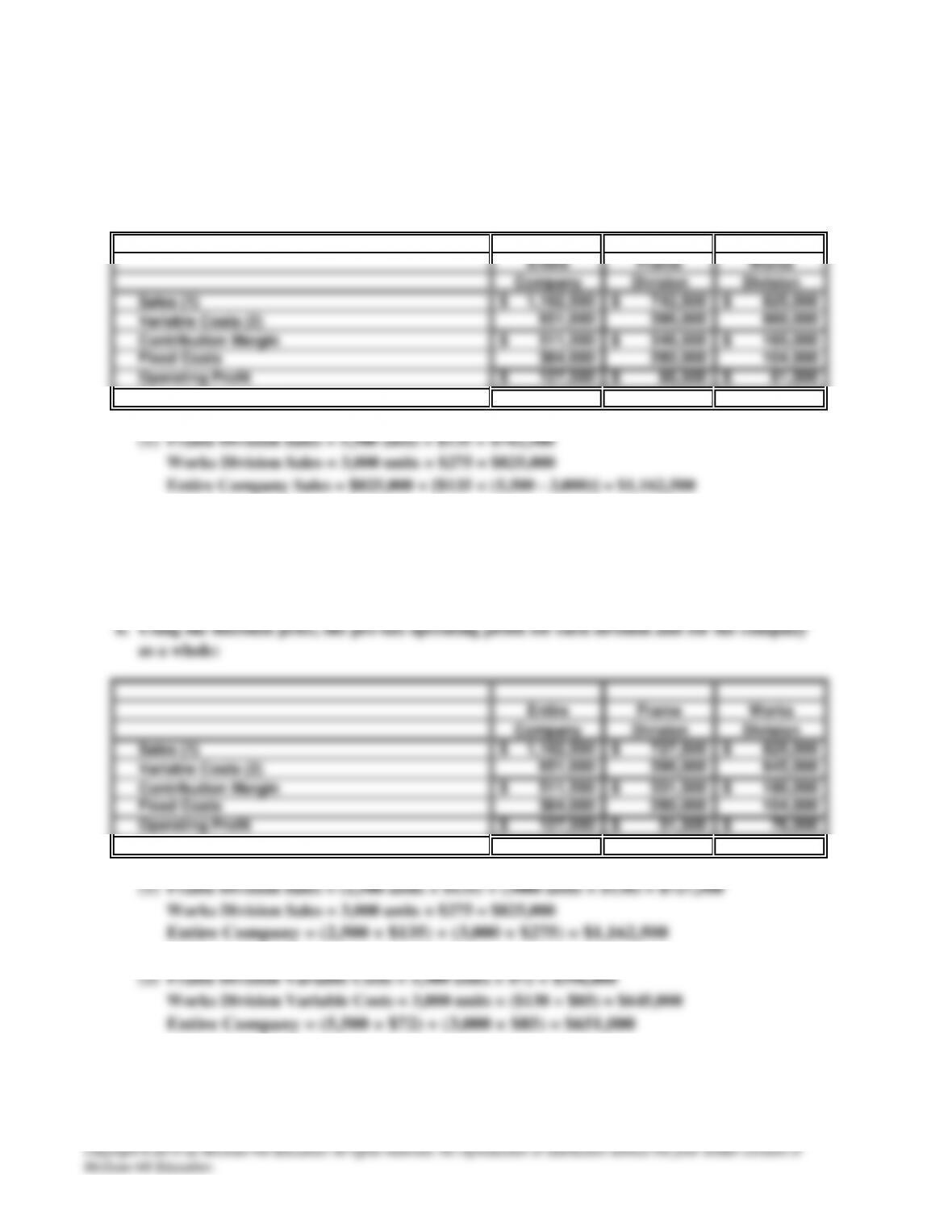

a.

(2)

40 Minutes, Medium

Frame Division Variable Costs = 5,500 units × $72 = $396,000

Works Division Variable Costs = 3,000 units × ($135 + $85) = $660,000

Entire Company Variable Costs = (5,500 units × $72) + (3,000 units × $85) = $651,000

Using the market price, the pre-tax operating profit for each division and for the company as

a whole:

Works Division Sales = 3,000 units × $275 = $825,000

Entire Company Sales = $825,000 + [$135 × (5,500 – 3,000)] = $1,162,500

PROBLEM 22.8B

WESTMINSTER, INC. (concluded)

c.

Transfer prices generate accounting entries to show the flow of goods between departments.

One department records the transfer price as revenue, while the other department records

SOLUTIONS TO CRITICAL THINKING CASE

S

CASE 22.1

LAND’S END HOTEL

a.

35 Minutes, Medium

Evaluation of Chamberlain’s comments:

A basic purpose of a responsibility accounting system is to measure the performance of

specific responsibility centers. This means that the revenue and costs upon which a center

is evaluated should be traceable directly to that center and, ideally, be under the center

performance may be obscured; the performance of strong profit centers may be

understated, and the performance of weaker centers may be overstated since these

centers are charged with less costs.

Furthermore, traceable fixed costs may be divided into the subcategories of controllable

fixed costs and committed fixed costs. This enables the responsibility income statement to

show as a subtotal (performance margin) those aspects of the center’s operations that are

readily controllable by the center manager.

We recommend that the revenue of a center should be offset only by the related variable

costs and by those fixed costs that are directly traceable to the center. Common fixed

costs—those that jointly benefit several profit centers—should not be allocated among the

centers deriving benefit. Thus, the responsibility income statement includes only those

costs directly traceable to the center’s activities.

In summary, Chamberlain’s criticisms of the existing approach to assigning costs to

profit centers are valid. His suggestion that fixed costs should instead be allocated in

by a department may be a matter of circumstances not under the center’s manager’s

direct control. Mettenburg, for example, does not have the option of “shrinking” the

Sunset Lounge.

The criticisms of the two managers point out that any allocation of common costs is

necessarily arbitrary, rewarding some profit centers, but penalizing others.

CASE 22.2

a.

OSBORN DIVERSIFIED PRODUCTS, INC.

Financially, the $40,000 error is not apt to significantly damage Osborn. However, this

does not mean that Jim should keep the money and let the error go unreported. Jim has

an ethical responsibility to make the company aware of its mistake. To do otherwise is the

CASE 22.3

a.

HOSPITAL PROFIT CENTERS

30 Minutes, Medium

Student answers will vary. However, suggested profit centers include: Emergency room,

pediatrics, intensive care, knee/hip replacement surgeries, cafeteria, dialysis center, etc.

Suggested cost centers include: housekeeping, admissions, laundry, building maintenance,

CASE 22.

4

a.

30 Minutes, Medium

Given the diverse nature of the products supplied by General Mills, there are many ways

in which to organize responsibility centers. One way would be to define responsibility

centers based on major product groups such as cereals, baked goods, snacks, dairy, and

GENERAL MILLS AND THE KIRBY COMPANY

CASE 22.5

20 Minutes, Medium

ETHICS, FRAUD & CORPORATE GOVERNANCE

Student answers will vary considerably, but one issue that can be discussed about the ethics

University Ethics