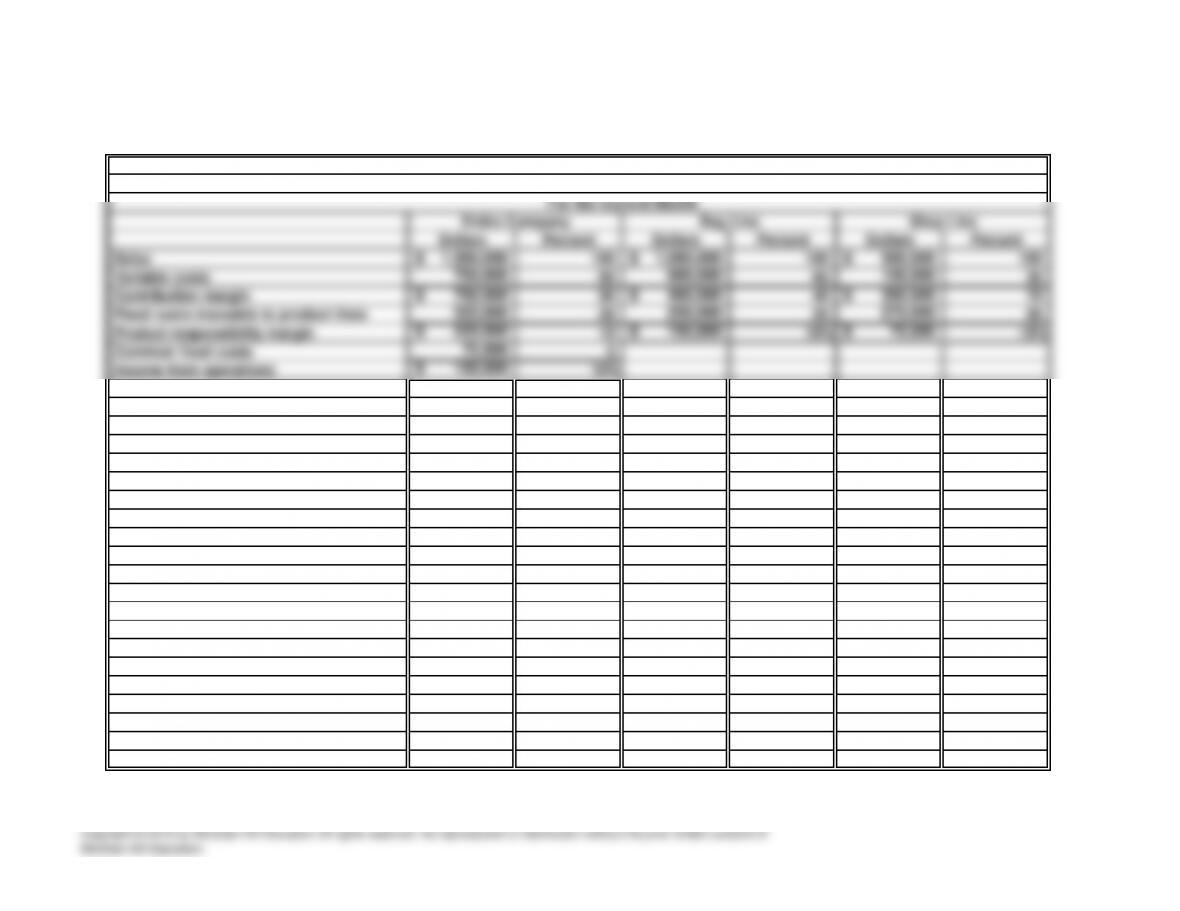

30 Minutes, Medium PROBLEM 22.2B

BROWN ENTERPRISES

a. Responsibility income statement:

BROWN ENTERPRISES

Responsibility Income Statement

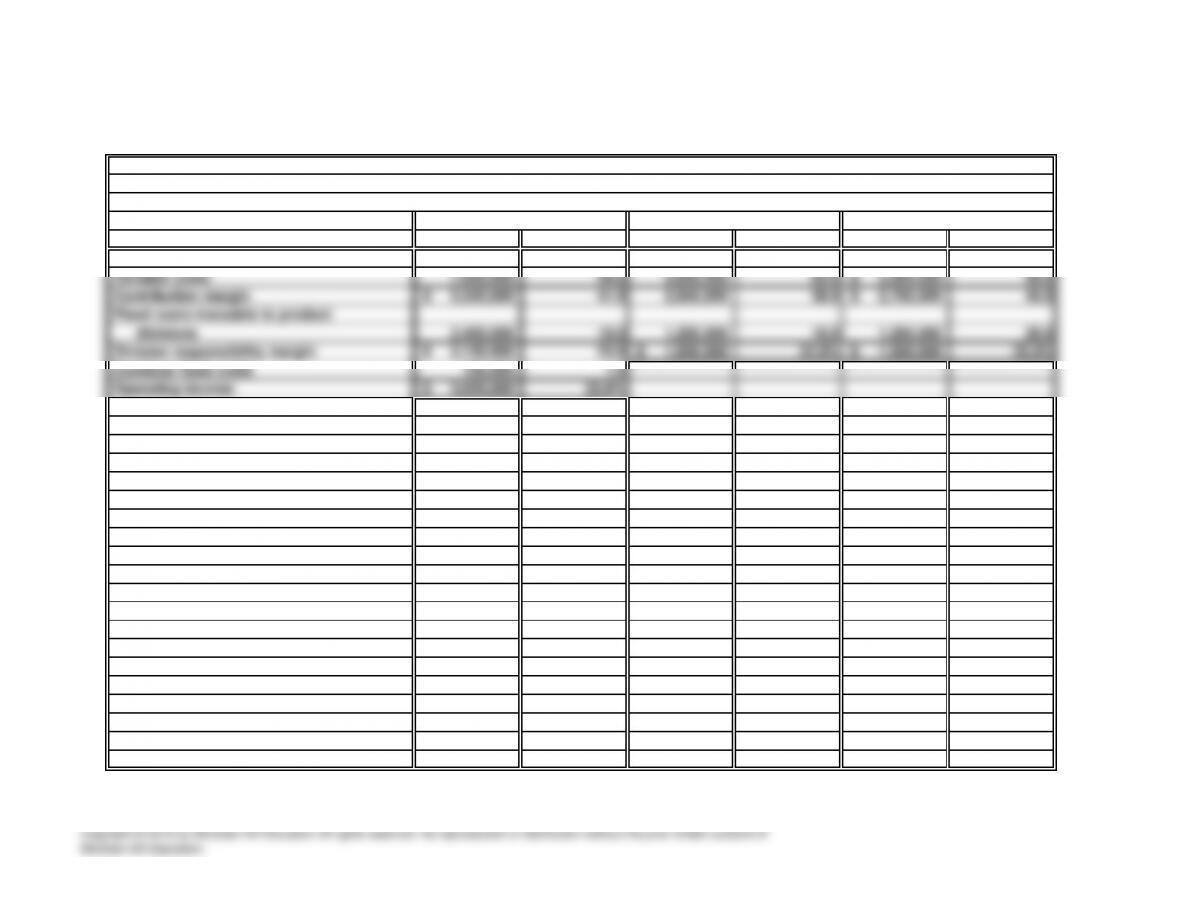

PROBLEM 22.2B

BROWN ENTERPRISES (concluded)

b.

p

g

g

(

)

p

c. Results of investment in each

p

roduct line:

Ba

g

s Shoes

Ex

p

ected increase in contribution mar

g

in:

Ba

g

s

(

$250,000 × 40%

)

100,000$

p

Because of the relatively high contribution margin ratio in the shoe segment, spending

$50,000 per month to achieve a monthly sales increase of $100,000 will increase overall

profitability. Bags, however, provides a lower contribution margin ratio. After variable

costs, a $100,000 increase in bag sales leaves only $40,000 in contribution margin, which

does not cover the cost of the proposed advertising campaign.

profitable results. The contribution margin ratio of the Bag line is considerably less than

that of the Shoe line (40% compared to 70%). Thus, an expected increase of $250,000 in

sales for the Bag line will only contribute $100,000 toward covering the expected increase in

the line’s traceable fixed costs of $150,000 ($250,000 × 60%). On the other hand, a $250,000

increase in sales of shoes will produce a contribution margin that is greater than the

Recommendations on increased advertising:.

It appears that increasing advertising expenditures on shoes will increase the profitability of

the business, but spending the proposed amount to advertise bags would reduce

profitability.

Short-run decisions that are not likely to affect fixed costs may be evaluated based upon the

expected change in contribution margin. Thus, the expected effect of the proposed

advertising campaign upon income from operations may be summarized as follows:

g

30 Minutes, Medium PROBLEM 22.3B

GLASSWARE COMPANY

a. Responsibility income statement for August:

Entire Company Etched Glass Division Clear Glass Division

Dollars Percent Dollars Percent Dollars Percent

Sales 13,500,000$ 100.0 7,500,000$ 100.0 6,000,000$ 100.0

GLASSWARE COMPANY

For August

Responsibility Income Statement

PROBLEM 22.3B

GLASSWARE COMPANY (concluded)

b.

Division Sales

÷ Contribution Margin Ratio

Sales volume required for a $1,600,000 monthly responsibility margin in the Clear Glass

Division may be computed as follows:

= [Division Fixed Costs + Responsibility Margin]

60 Minutes, Strong PROBLEM 22.4B

FREEZE, INC.

a. FREEZE, INC.

Responsibility Income Statement

Northern Territory

For January

Northern Territory Economy Efficiency

Dollars Percent Dollars Percent Dollars Percent

Common fixed costs 125,000 8.3

Operating income 235,000$ 15.7%

b. FREEZE, INC.

Responsibility Income Statement

For January

Fixed costs traceable to territories 705,000 30.7 * 415,000 27.6 290,000 36.0

Division responsibility margin 393,000$ 17.1 235,000$ 15.7% 158,000$ 20.0%

PROBLEM 22.4B

FREEZE, INC. (concluded)

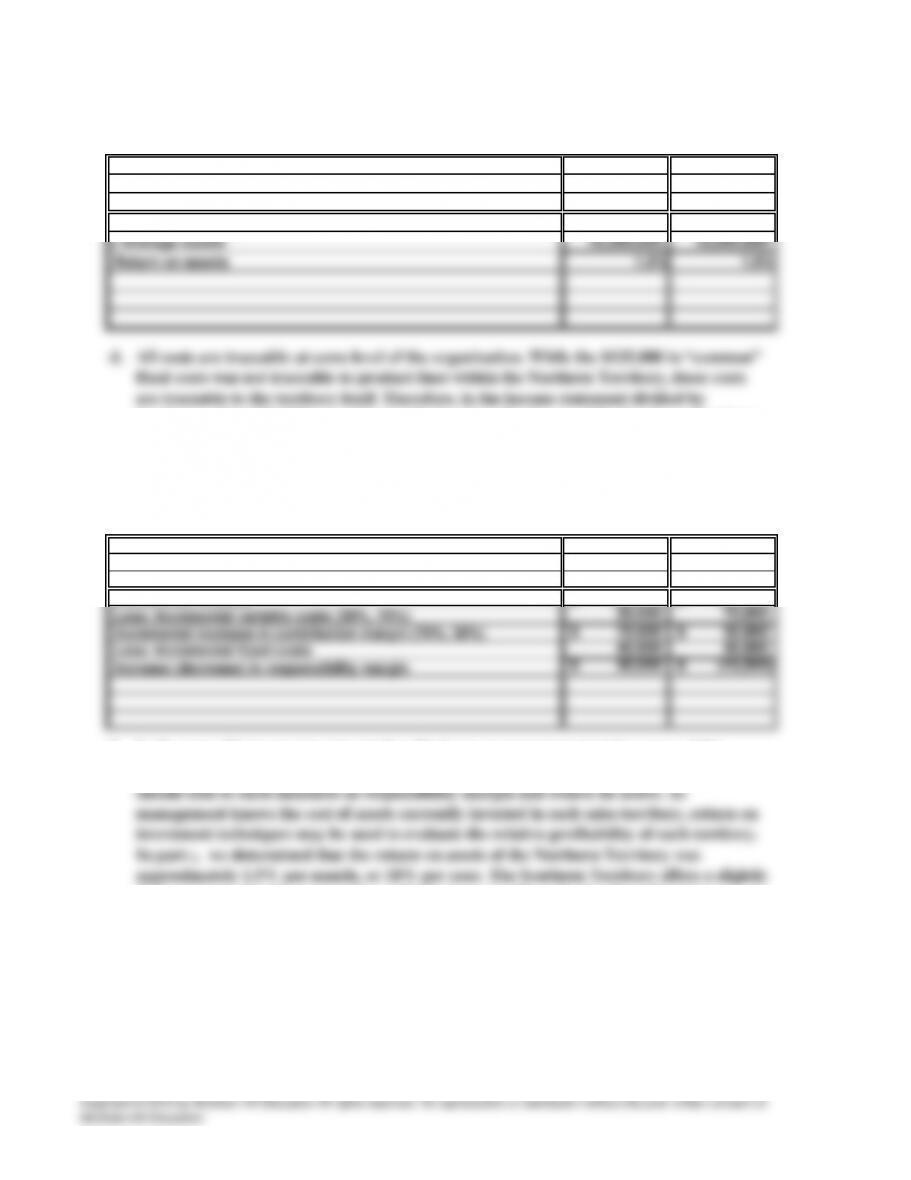

c. Each territory’s return on assets: Northern Southern

Territory Territory

Responsibility margin 235,000$ 158,000$

e.

Econom

y

Efficienc

y

Incremental revenue 100,000$ 100,000$

f.

territories, this $125,000 is combined with the other fixed costs of the Northern Territory

and is shown as “Fixed costs traceable to territories.”

The manager should focus the campaign on the product line that will generate the greatest

contribution margin in relation to the additional fixed advertising cost. Thus, the manager

should support advertising of Economy as shown below:

In the type of long-run investment described, top management must be aware of the

ability of the investment to cover fixed costs as well as variable costs. Thus, management

higher return of 1.6% per month, or 19.2% per year. Thus, the Southern Territory

appears to offer the higher potential return on investment.

45 Minutes, Strong PROBLEM 22.5B

SOTHEBY, INC.

a. Computation of expected change in responsibility margin:

(1) Product C (2) Product D

Expected increase in sales 25,000$ 25,000$

Product contribution margin ratio × 50% × 19%

b.

When an increase in revenue requires new manufacturing facilities, the revenue must be

sufficient to cover the increase in fixed costs as well as the variable costs of production. The

ability to cover fixed costs is indicated by the responsibility margin ratio. Product C has the

higher responsibility margin ratio, with 27% of total revenue currently adding directly to

PROBLEM 22.5B

SOTHEBY, INC. (concluded)

SOTHEBY, INC.

Income Statement by Divisions

PROBLEM 22.6B

FOOTWARE, INC.

a.

15 Minutes, Easy

Closure of the Sandal Division would increase the company’s operating income to $9,000 (a

$2,000 increase resulting from the elimination of the negative responsibility margin