PROBLEM 22.3A

GIANT CHEF EQUIPMENT COMPANY (concluded)

b.

Sales volume required for a $500,000 monthly responsibility margin in the Home

Products Division may be computed as follows:

60 Minutes, Strong PROBLEM 22.4A

MUSCLE BOUND CO.

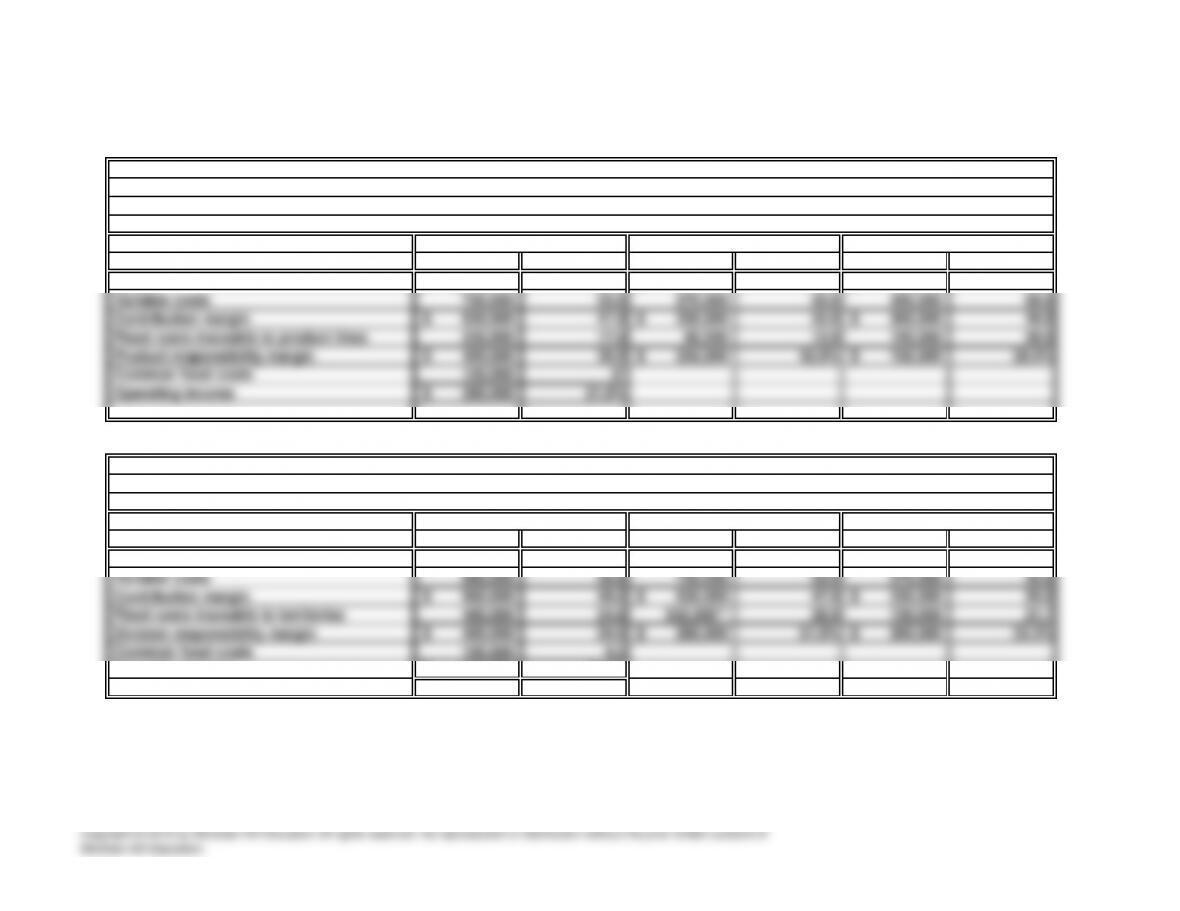

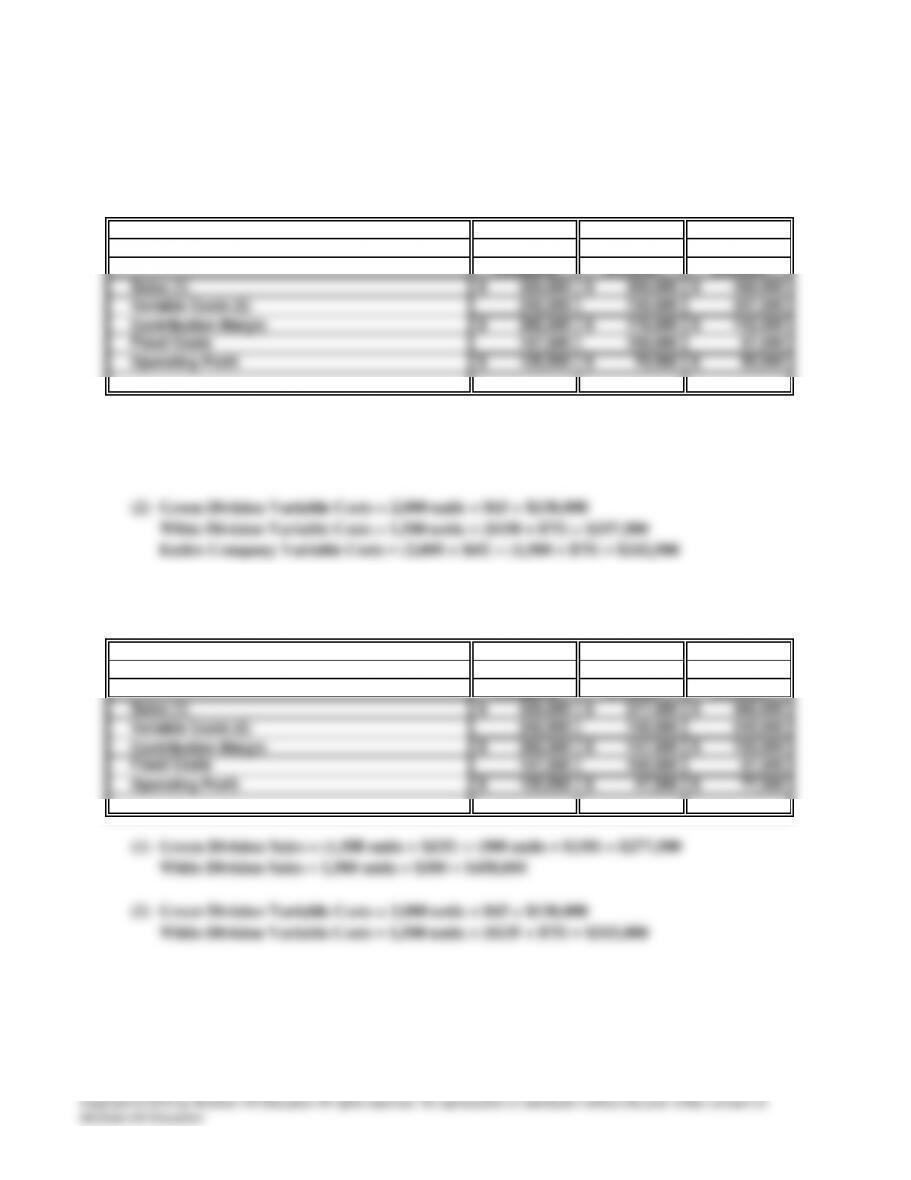

a. Responsibility income statement of MUSCLE BOUND COMPANY

the Eastern Territory: Responsibility Income Statement

Eastern Territory

For January

Eastern Territory FasTrak RowMaster

Dollars Percent Dollars Percent Dollars Percent

Sales 1,350,000$ 100.0 600,000$ 100.0 750,000$ 100.0

b. Responsibility income statement of MUSCLE BOUND COMPANY

the entire company: Responsibility Income Statement

For January

Entire Company Eastern Territory Western Territory

Dollars Percent Dollars Percent Dollars Percent

Sales 1,950,000$ 100.0 1,350,000$ 100.0 600,000$ 100.0

Operating income 300,000$ 15.4%

* Minor rounding difference

** $350,000 = $120,000 common fixed costs of Eastern Territory + $230,000 traceable fixed costs.

PROBLEM 22.4A

MUSCLE BOUND CO. (concluded)

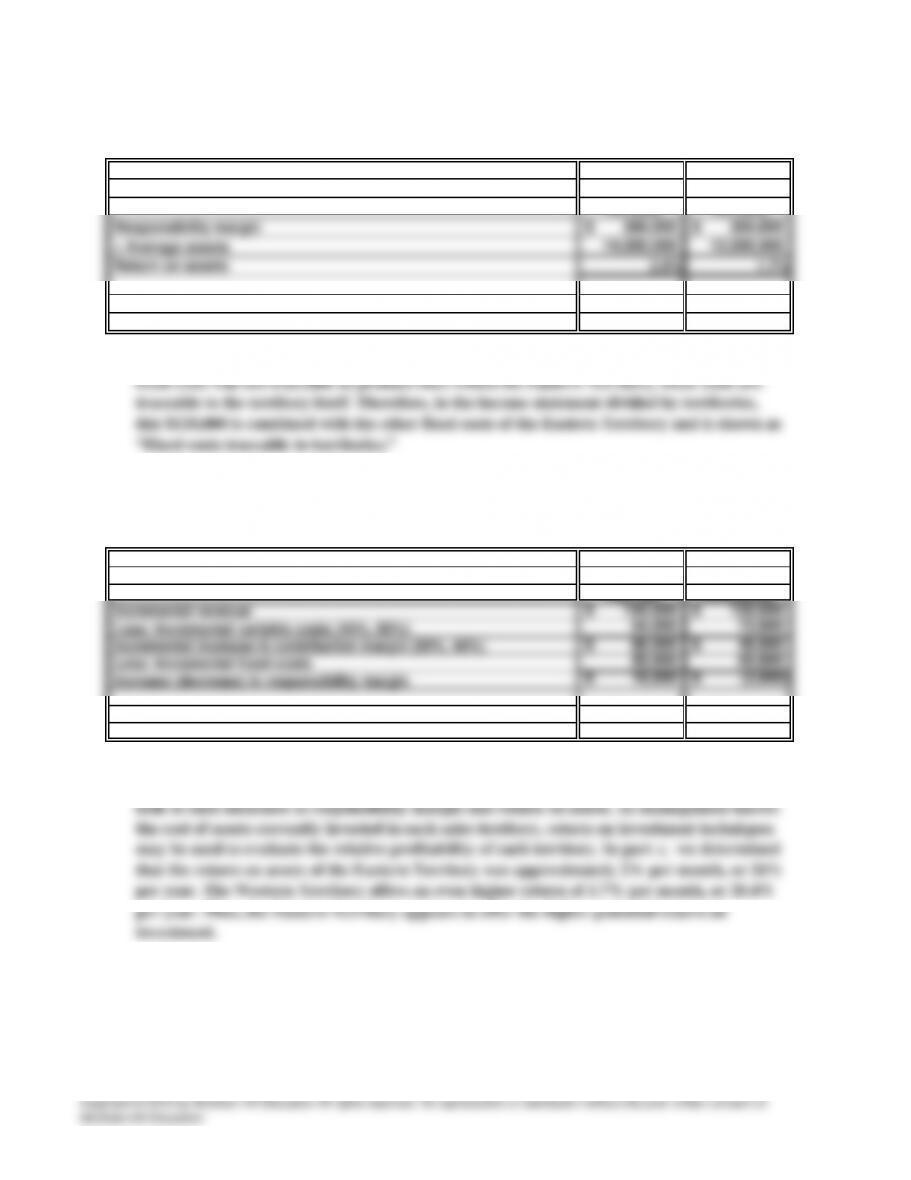

c. Each territory’s return on assets: Eastern Western

Territory Territory

d.

e.

FasTrak RowMaster

f.

All costs are traceable at some level of the organization. While the $120,000 in “common”

The manager should focus the campaign on the product line that will generate the greatest

contribution margin in relation to the additional fixed advertising cost. Thus, the manager

should support advertising of FasTrak, as shown below:

In the type of long-run investment described, top management must be aware of the ability

of the investment to cover fixed costs as well as variable costs. Thus, management should

PROBLEM 22.5A

BUTTERFIELD, INC.

a. Com

p

utation of ex

p

ected chan

g

e in res

p

onsibilit

y

mar

g

in:

(

1

)

Product

A

(

2

)

Product B

Ex

p

ected increase in sales 30,000$ 30,000$

p

p

b.

c.

45 Minutes, Strong

When an increase in revenue requires new manufacturing facilities, the revenue must be

In the Division 1 responsibility income statement, this $21,000 in costs was classified as

p

PROBLEM 22.5A

BUTTERFIELD, INC. (concluded)

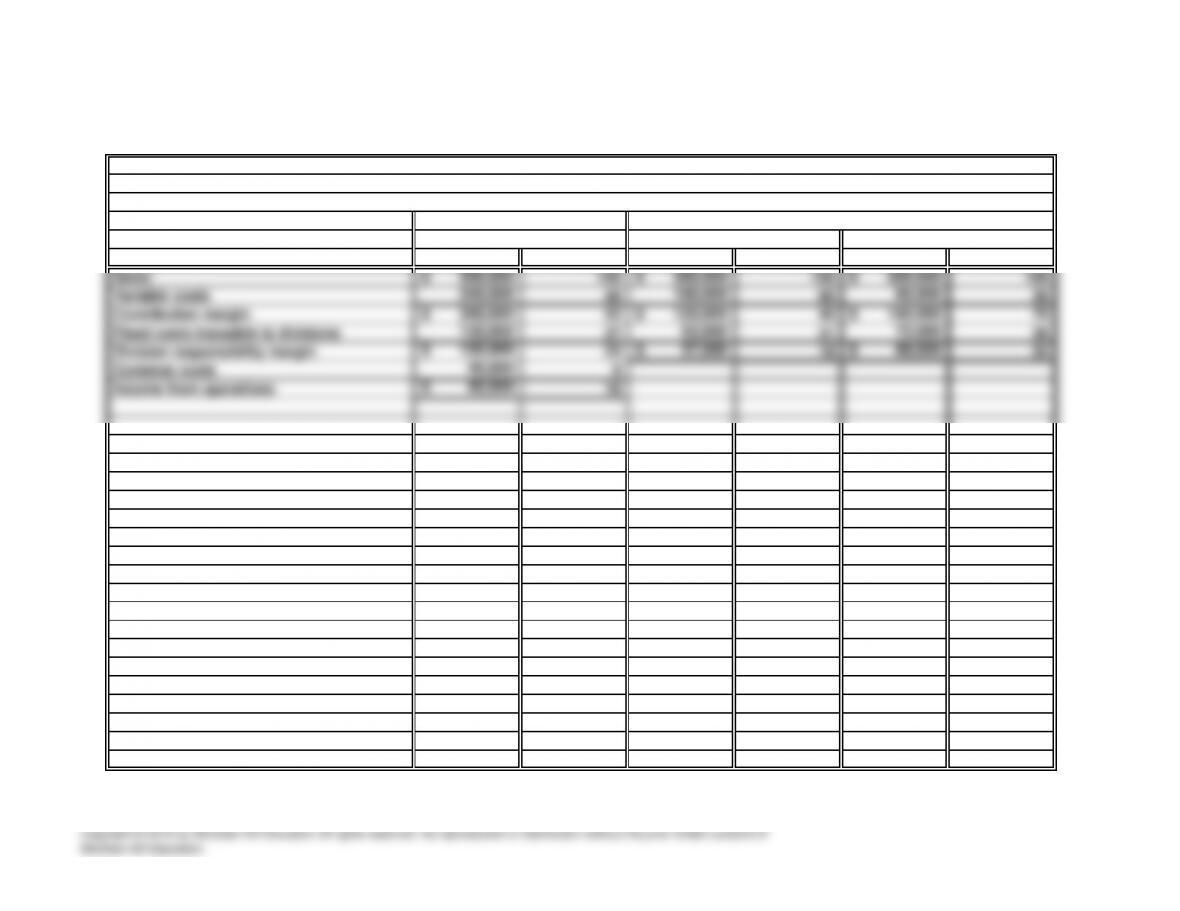

e. BUTTERFIELD, INC.

Income Statement by Divisions

For the Month Ended April 30 Divisions

Butterfield, Inc. Division 1 Division 2

Dollars Percent Dollars Percent Dollars Percent

PROBLEM 22.6

A

FLYWIZ, INC.

a.

15 Minutes, Easy

Based solely on the financial data given, closure of the Rod Division would have increased

the company’s operating income to $9,000 (a $4,000 increase resulting from the elimination

of the negative responsibility margin generated by that division).

20 Minutes, Easy PROBLEM 22.7A

TOTS-TO-GO COMPANY

a.

Entire Seat Stroller

Using the market price, the contribution margins for each division and for the company as a

whole:

PROBLEM 22.8A

SPARTA AND ASSOCIATES

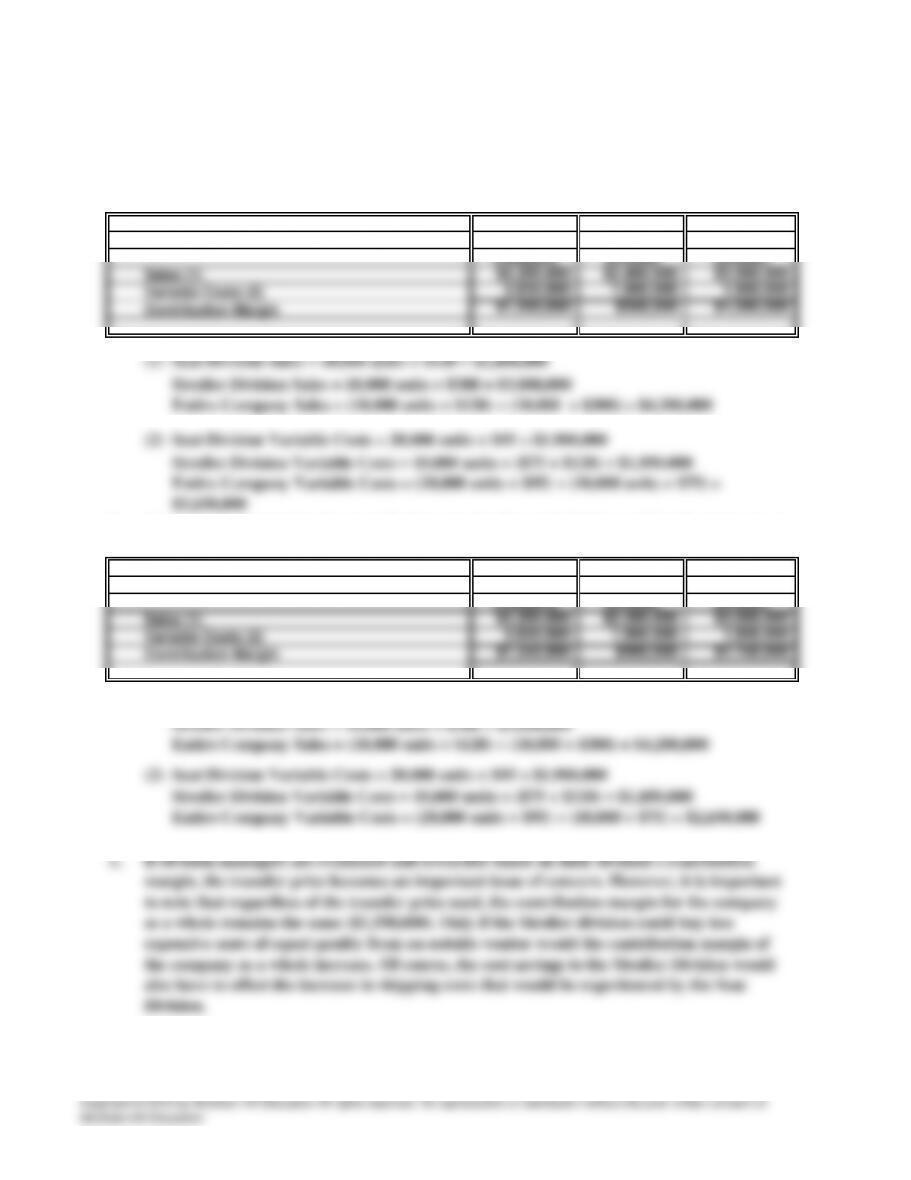

a.

Entire Green White

Company Division Division

(1)

b.

Entire Green White

Company Division Division

Using the discount price, the pre-tax operating profit for each division and for the company

as a whole:

Green Division Sales = 2,000 units × $150 = $300,000

White Division Sales = 1,500 units × $300 = $450,000

Entire Company Sales = (2,000 – 1,500) × $150 + (1,500 × $300) = $525,000

40 Minutes, Medium

Using the market price, the pre-tax operating profit for each division and for the company as

a whole:

PROBLEM 22.8A

SPARTA AND ASSOCIATES (concluded)

c.

Transfer prices generate accounting entries that show the flow of goods between

departments. One department records the transfer price as revenue, while the other

SOLUTIONS TO PROBLEMS SET B

PROBLEM 22.1B

FASTENERS INC.

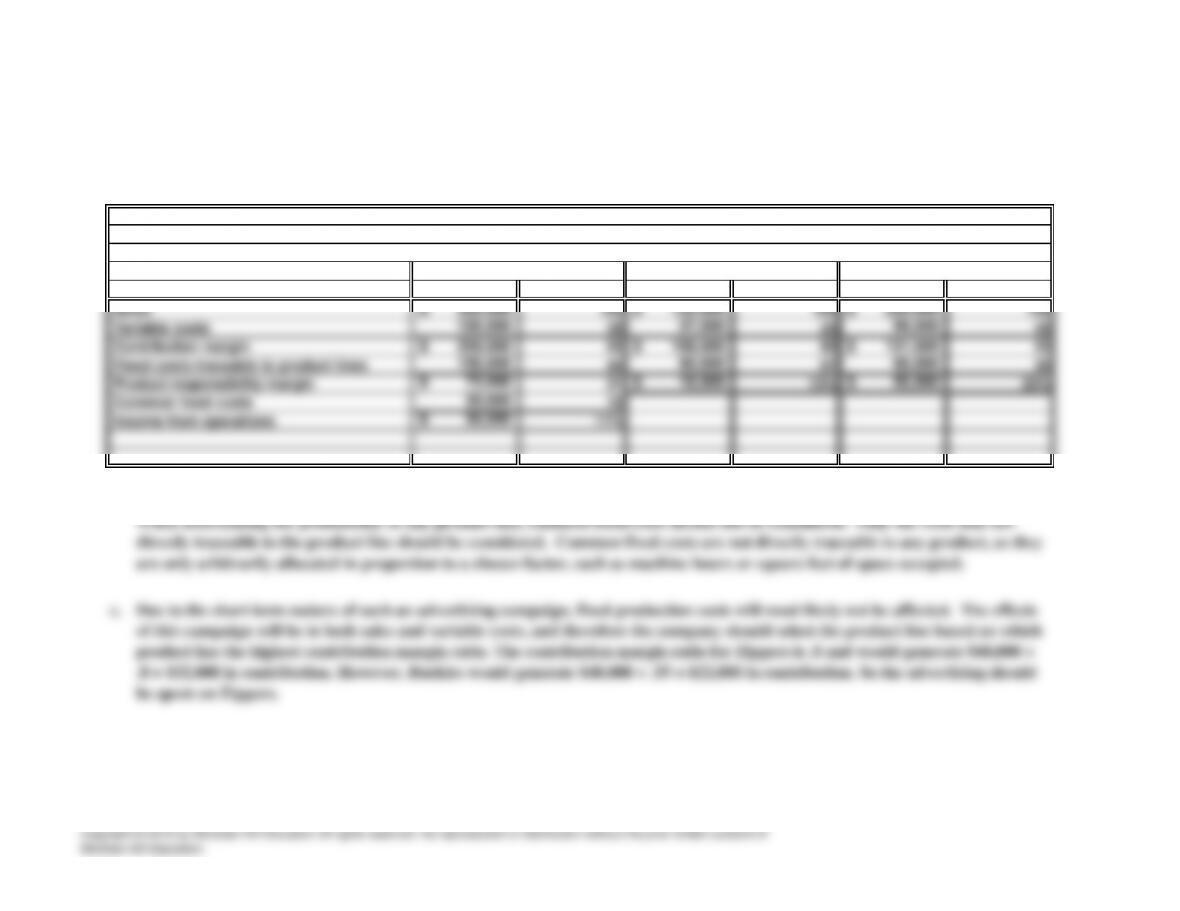

a. FASTENERS INC.

Responsibility Income Statement

For the Current Month

Entire Company Zippers Line Buckles Line

Dollars Percent Dollars Percent Dollars Percent

b.

According to the analysis in part a, the Buckles product line is more profitable.

of this campaign will be in both sales and variable costs, and therefore the company should select the product line based on which

product has the highest contribution margin ratio. The contribution margin ratio for Zippers is .8 and would generate $40,000 ×

.8 = $32,000 in contribution. However, Buckles would generate $40,000 × .55 = $22,000 in contribution. So the advertising should

be spent on Zippers.

When determining the profitability of any product line, common fixed costs should not be considered. Only the costs that are

directly traceable to the product line should be considered. Common fixed costs are not directly traceable to any product, as they

are only arbitrarily allocated in proportion to a chosen factor, such as machine hours or square feet of space occupied.

20 Minutes, Easy