Chapter 02 – Basic Financial Statements

Financial and Managerial Accounting, 17e 2-1

2 BASIC FINANCIAL STATEMENTS

Chapter Summary

Financial statements are the primary means of communicating financial information to

users. Chapter 2 covers the income statement, balance sheet, and statement of cash flows.

Chapter 1 set forth the objectives of the financial reporting process, and offered the

observation that these objectives are met in large part by a set of financial statements. In this

chapter, we take up the task of introducing the balance sheet, income statement, and the

statement of cash flows.

The presentation is organized around the accounting equation. The equation serves as the

basis for elementary transaction analysis. A continuing illustration examines the impact of a

number of simple transactions upon the balance sheet of a simple service business. Revenue and

expense transactions have been included so that we might introduce the income statement and

statement of cash flows at an elementary level. This in turn has provided the opportunity to

discuss and illustrate statement articulation.

Before closing, the chapter emphasizes the importance of adequate disclosure regarding

both financial and nonfinancial information, thereby reinforcing the Chapter 1 theme that the

financial reporting process is broader than the financial statements.

The chapter also covers accounting principles dealing with asset valuation, as well as an

introduction to forms of business organization.

Learning Objectives

1. Explain the nature and general purpose of financial statements.

2. Explain certain accounting principles that are important for an understanding of financial

statements and how professional judgment by accountants may affect the application of those

principles.

3. Demonstrate how certain business transactions affect the elements of the accounting

equation: Assets = Liabilities + Owners’ Equity.

4. Explain how the statement of financial position, often referred to as the balance sheet, is an

expansion of the basic accounting equation.

5. Explain how the income statement reports an enterprise’s financial performance for a period

of time in terms of the relationship of revenues and expenses.

6. Explain how the statement of cash flows presents the change in cash for a period of time in

terms of the company’s operating, investing, and financing activities.

7. Explain how the statement of financial position (balance sheet), income statement, and

statement of cash flows relate to each other.

Chapter 02 – Basic Financial Statements

8. Explain common forms of business organization–sole proprietorship, partnership, and

corporation–and demonstrate how they differ in terms of their statements of financial

position.

9. Discuss the importance of financial statements to a company and its investors and creditors

and why management may take steps to improve the appearance of the company in its

financial statements.

Brief topical outline

A Introduction to financial statements

B A starting point: statement of financial position

1 The concept of the business entity

2 Assets

a The cost principle

b The going-concern assumption

c The objectivity principle – see Your Turn (page 43)

d The stable-dollar assumption – see Case in Point (page 44)

3 Liabilities

4 Owners’ equity

a Increases in owners’ equity

b Decreases in owners’ equity

5 The accounting equation

6 The effects of business transactions (illustrated on pages 46-50)

7 Effects of these business transactions on the accounting equation

C Income statement (illustrated on page 53)

D Statement of cash flows (illustrated on page 54) – see Case in Point (page 54)

E Relationships among financial statements

F Financial analysis and decision making – see Your Turn (page 57)

G Forms of business organization

1 Sole proprietorships

2 Partnerships

3 Corporations

4 Reporting ownership equity in the statement of financial position

(illustrated on pages 58 & 59)

H The use of financial statements by external parties

1 The short run versus the long run

2 Evaluating short-term liquidity

3 The need for adequate disclosure

4 Management’s interest in financial statements – see Ethics, Fraud & Corporate

Governance (page 61)

I Concluding remarks

Chapter 02 – Basic Financial Statements

Financial and Managerial Accounting, 17e 2-3

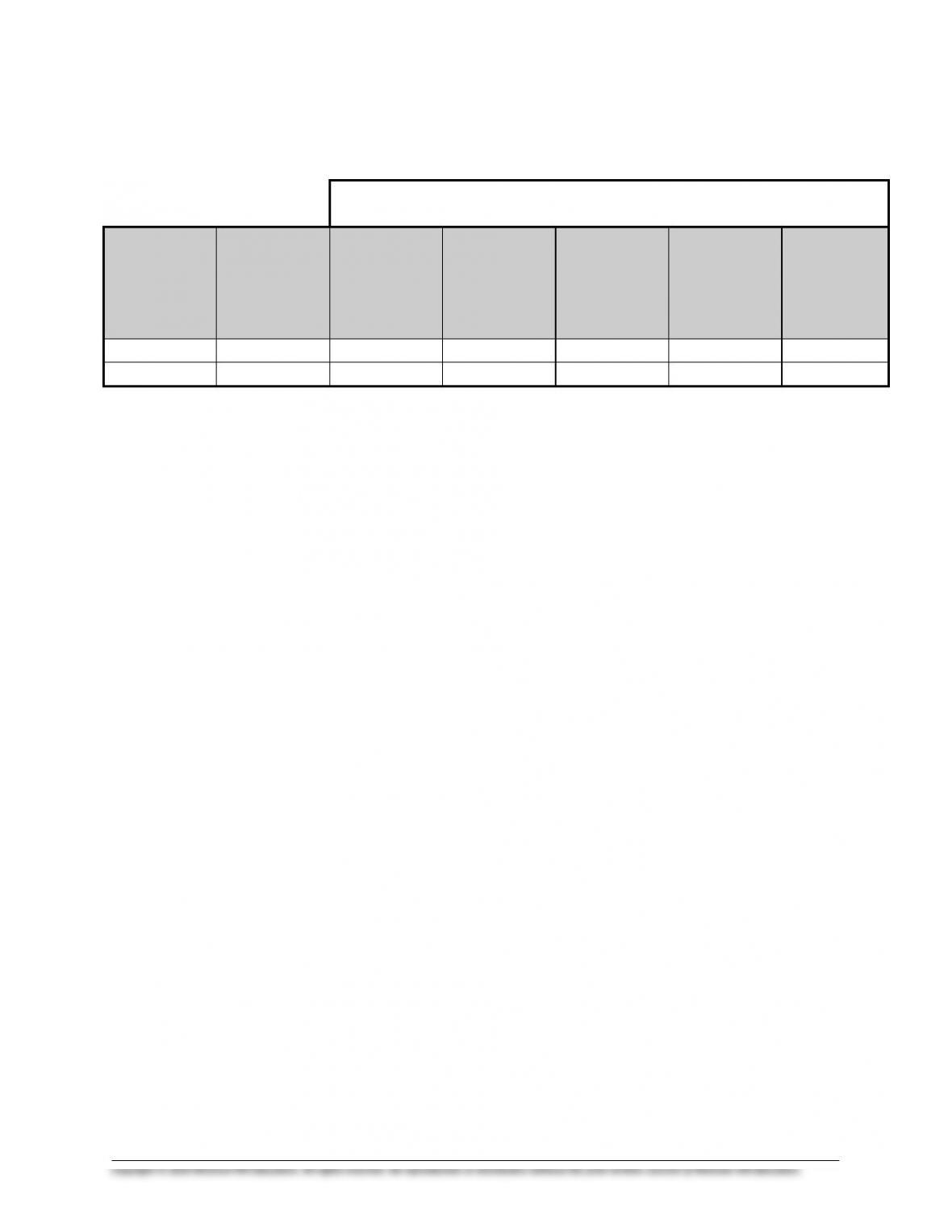

Topical coverage and suggested assignment

Homework Assignment

(To Be Completed Prior to Class)

Class

Meetings

on Chapter

Topical

Outline

Coverage

Discussion

Questions

Brief

Exercises

Exercises

Problems

Critical

Thinking

Cases

1

A – D

3, 4, 5, 8

1, 3, 4

1, 4, 6

1, 3, 6

1

2

E – I

9, 14, 15

7, 9, 10

11, 12, 13

7, 8, 9

3

Comments and observations

Teaching objectives for Chapter 2

The chapter introduces technical material, including the balance sheet, income statement,

statement of cash flows, several generally accepted accounting principles, the accounting

equation, and the effects of business transactions upon assets, liabilities, and owners’ equity.

Our objectives in presenting this chapter are:

1 Describe the nature of financial statements. Explain the role of generally accepted

accounting principles in this process.

2 Illustrate and explain a balance sheet. Define the terms assets, liabilities, and owners’

equity, and discuss the basic accounting principles relating to asset valuation. Discuss the

uses and limitations of this financial statement.

3 Introduce the accounting equation and illustrate the effects of business transactions upon

this equation and upon a balance sheet.

4 Introduce the income statement, emphasizing the nature of revenues and expenses.

5 Introduce the statement of cash flows and distinguish among operating, investing, and

financing activities.

6 Explain and illustrate the concept of financial statement articulation.

7 Define proprietorship, partnership, and the corporation as forms of business organization,

and illustrate the effect of the form of organization on the presentation of owners’ equity in

the financial statements.

8 Explain the importance of adequate disclosure.

Chapter 02 – Basic Financial Statements

General comments

Introducing the financial statements Our overriding objective in this chapter is to introduce

students to the balance sheet, income statement, and statement of cash flows. We find Problem 8

useful for this purpose. Exercise 1 defining assets and liabilities, stimulates student interest when

discussed in class. Also, it is short enough that they can be discussed without having been

assigned as homework. We also recommend Problem 9 or 10 for initiating a lively classroom

discussion of many of the concepts introduced in this chapter.

In covering Chapter 2, we like to continue the overview of the financial reporting process

begun in Chapter 1. Cases 2 and 6 provide a useful framework for this discussion, but there is

not enough time for both of them. Therefore, we rotate these cases in and out of our assignment

schedules. If Case 6 is discussed, it would be appropriate to explain, in simple terms, the

meaning and significance of debt covenants, in order to cultivate student appreciation of the

importance of the accounting issues in this case.

Have you considered using annual reports? One method of bringing the “real world” into the

classroom is through the use of annual reports. Annual report information can be obtained

through the SEC’s EDGAR database available on the Internet, or from individual company home

pages.

We encourage students to review these reports throughout the course and to note any similarities

and variations between their reports and the textbook treatment of various topics. These

comparisons increase students’ interest in the course, prompt interesting questions, and

demonstrate the diversity, which exists in practice.

Any annual report works fine. In fact a diversity of reports sparks comparisons and discussions

among students, and prevents one company from being asked to supply an unreasonable number

of reports. The reports need not be current to be useful. Once obtained, they may be passed on

to future students for at least several semesters.

An aside In discussing the valuation of assets in the balance sheet of a business, the text stresses

the cost principle. Therefore, the statement is made that the balance sheet of a business does not

show “how much the company is worth.” A different standard prevails, however, in the

preparation of personal financial statements for an individual. In an individual’s personal balance

sheet, generally accepted accounting principles require assets to be valued at estimated market

values. In addition, the estimated income tax liability, which would result from selling the assets

at these values also, is included in an individual’s balance sheet. Thus, the owners’ equity section

of a personal balance sheet shows the individual’s net worth.

Why have we not discussed personal financial statements in the text? The answer is that very

few individuals prepare personal financial statements in conformity with generally accepted

accounting principles. Most individual financial statements are prepared in conjunction with

loan applications. In these cases, the lender usually supplies its own preprinted forms, which

specify the lender’s standards for the valuation of assets and liabilities. These standards often

vary from generally accepted accounting principles. For example, most lenders do not ask a

borrower to estimate the income tax liability, which would result from liquidating appreciated

assets at their market values.

Chapter 02 – Basic Financial Statements

Financial and Managerial Accounting, 17e 2-5

Supplemental Exercises

Internet Exercise

Case 2-2 instructs students to perform an analysis of an annual report. Have students

download an annual report from a company web site and use this to complete the Case. Many

companies make their report available on their web site, and most of the sites are relatively easy

to locate through a search engine.

This chapter briefly introduces the stable dollar assumption. Students can become

familiar with the impact of inflation on monetary valuations at www.westegg.com/inflation/.

This site provides a calculator that allows a monetary amount in one year to be converted into an

equivalent amount in a second year.

Chapter 02 – Basic Financial Statements

CHAPTER 2 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

1 The financial statements of a business entity:

a Include the balance sheet, income statement, and income tax return.

b Provide information about the profitability and financial position of the

company.

c Are the first step in the accounting process.

d Are prepared for a fee by the Financial Accounting Standards Board.

2 A balance sheet is designed to show the financial position of an entity:

a At a single point in time.

b Over a period of time such as a year or quarter.

c At December 31 of the current year.

d At January 1 of the coming year.

3 Accounts payable and notes payable are:

a Always less than the amount of cash a business owns.

b Creditors.

c Written promises to pay a certain amount, plus interest, at a definite future date.

d Liabilities.

4 The balance sheet of Dotty Designs includes the following items:

Accounts Receivable

Cash

Capital Stock

Accounts Payable

Equipment

Supplies

Notes Payable

Notes Receivable

This list includes:

a Four assets and three liabilities.

b Five assets and three liabilities.

c Five assets and two liabilities.

d Six assets and two liabilities.

5 An accounting entity may best be described as:

a An individual.

b A particular economic unit.

c A publicly owned corporation.

d Any corporation, regardless of size.