50 Minutes, Strong PROBLEM 18.7B

DELRAY INDUSTRIES

a.

(1) 3,000

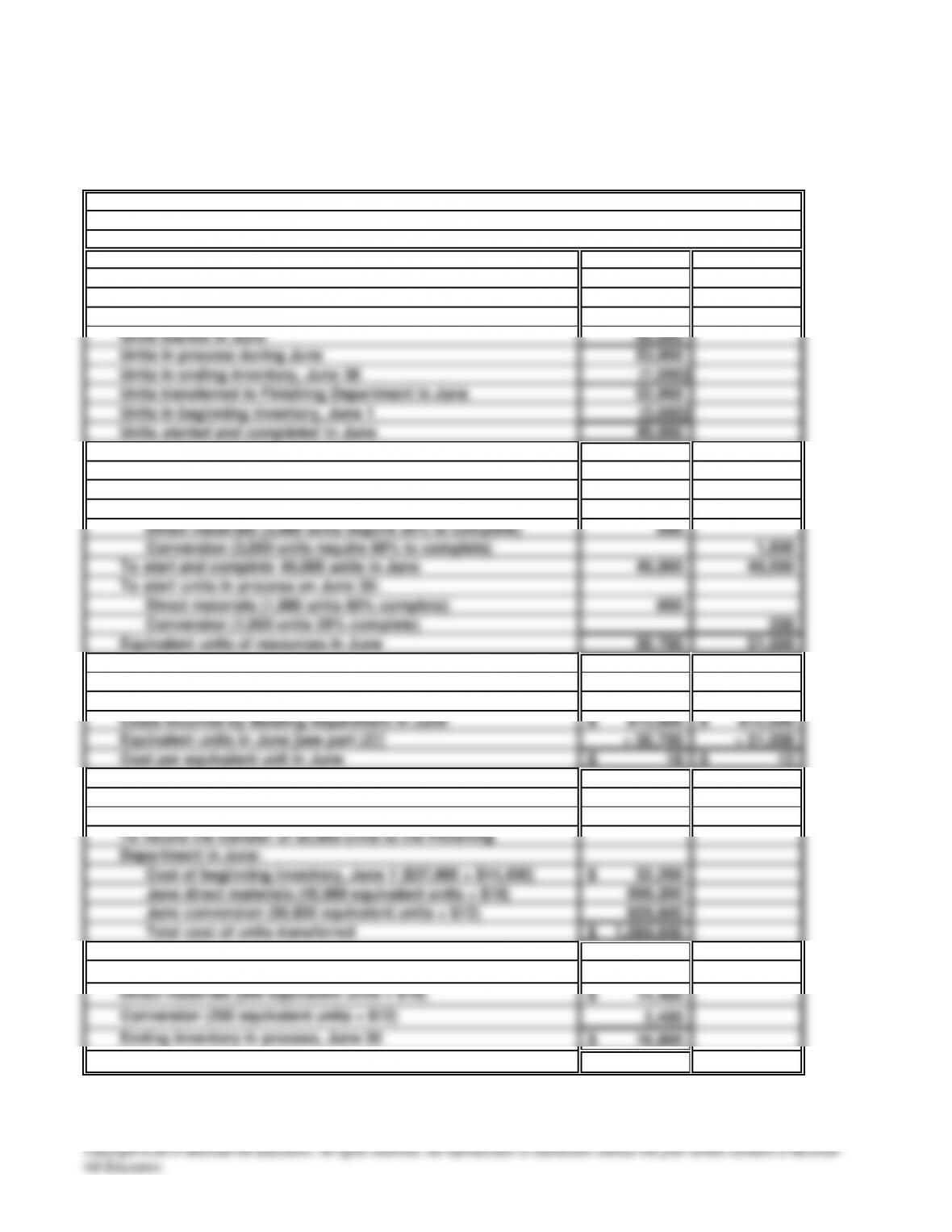

Requirements for the Molding Department in June

Flow of physical units: Molding Department

Units in beginning inventory, June 1

PROBLEM 18.7B

DELRAY INDUSTRIES (continued)

b.

(1) 5,000

Units in beginning inventory, June 1

Requirements for the Finishing Dept.

Flow of physical units: Finishing Dept.

in June

PROBLEM 18.7B

DELRAY INDUSTRIES (concluded)

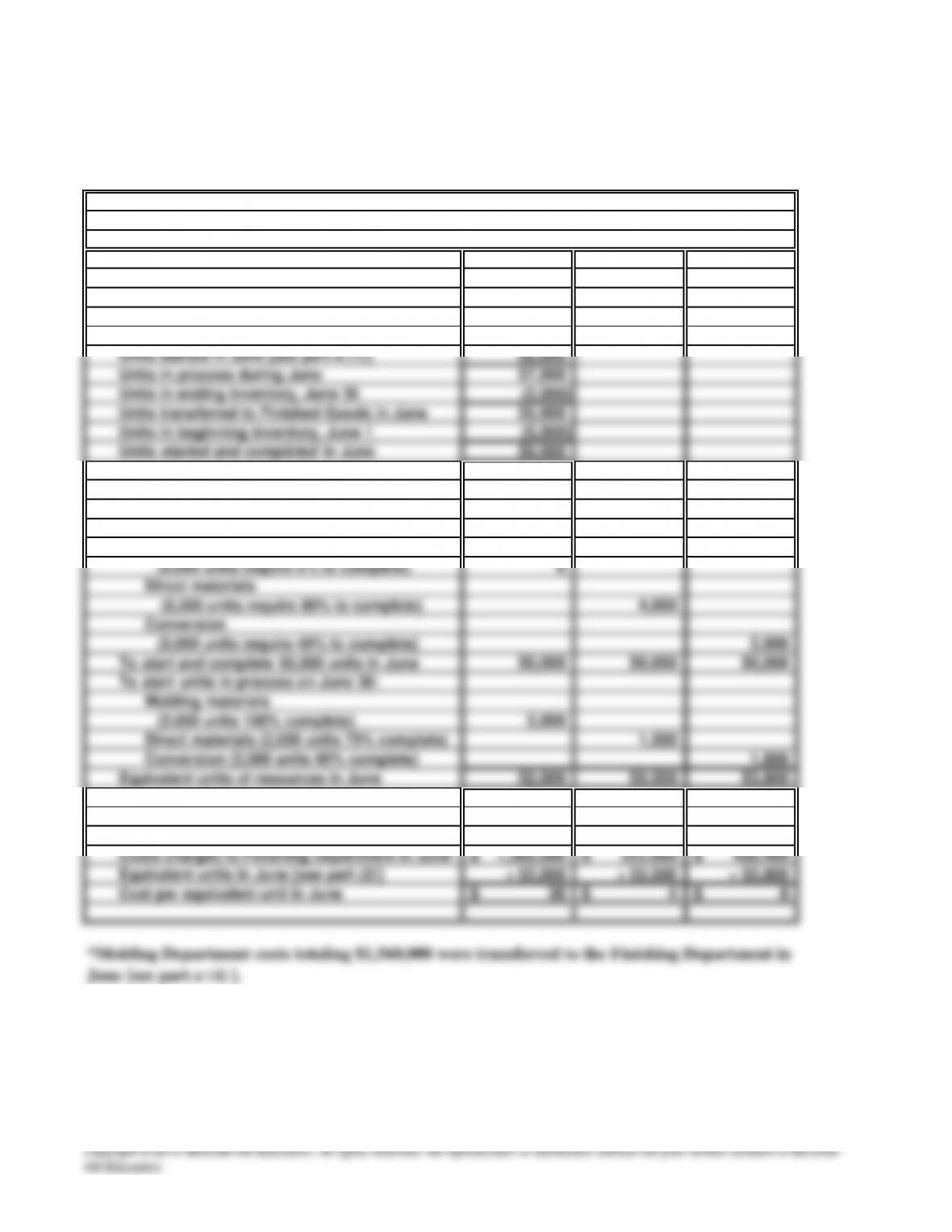

(4) 2,310,000

Work in Process: Finishing Department 2,310,000

(5)

60,000$

Finished Goods Inventory

To record the transfer of 55,000 units

Work in Process: Finishing Department,

Molding materials

to the Finished Goods Inventory in June:

June 30

(2,000 equivalent units × $30)

50 Minutes, Strong PROBLEM 18.8B

THOMPSON TOOLS

a.

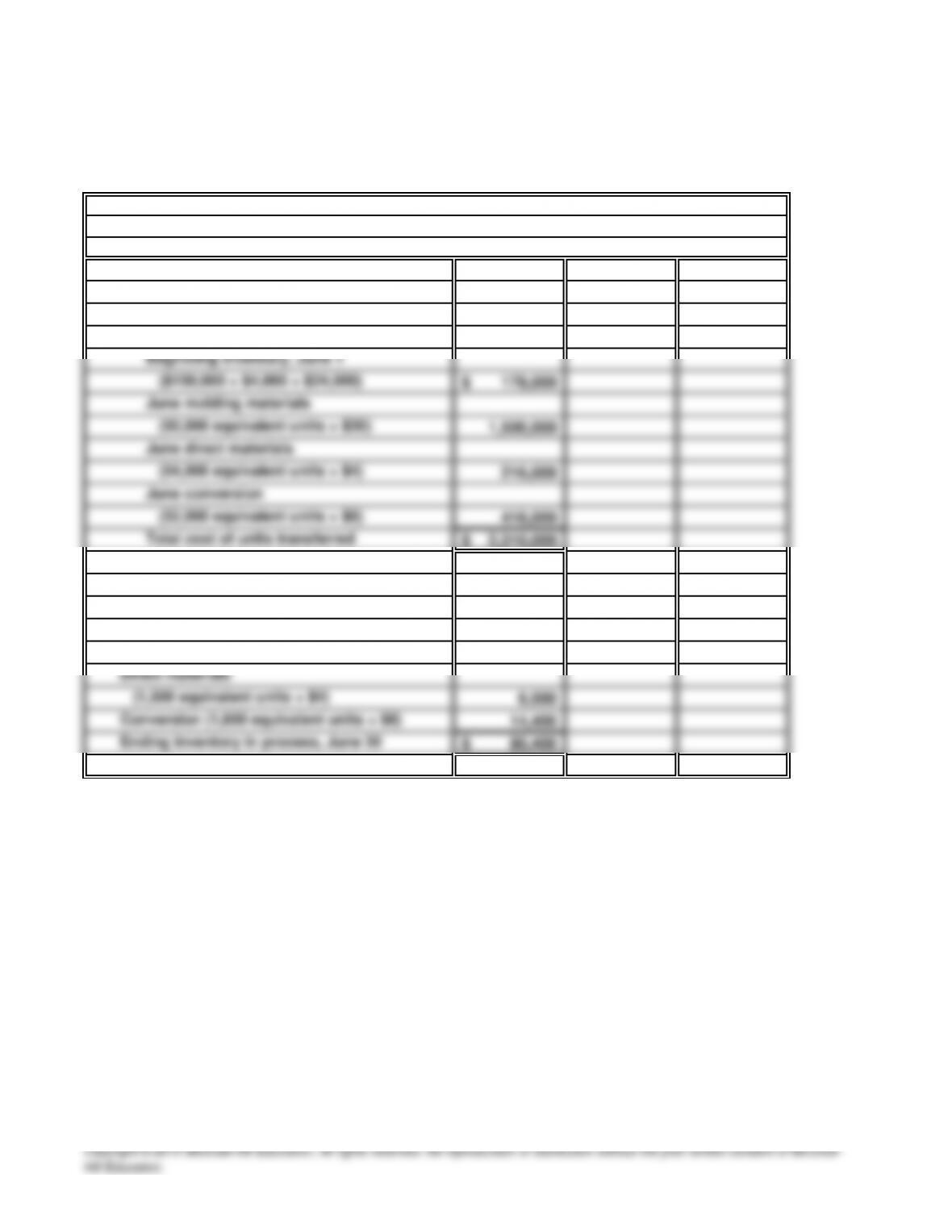

(1) 5,000

Flow of physical units: Assembly Department

Requirements for the Assembly Department in March

Units in beginning inventory, March 1

PROBLEM 18.8B

THOMPSON TOOLS (continued)

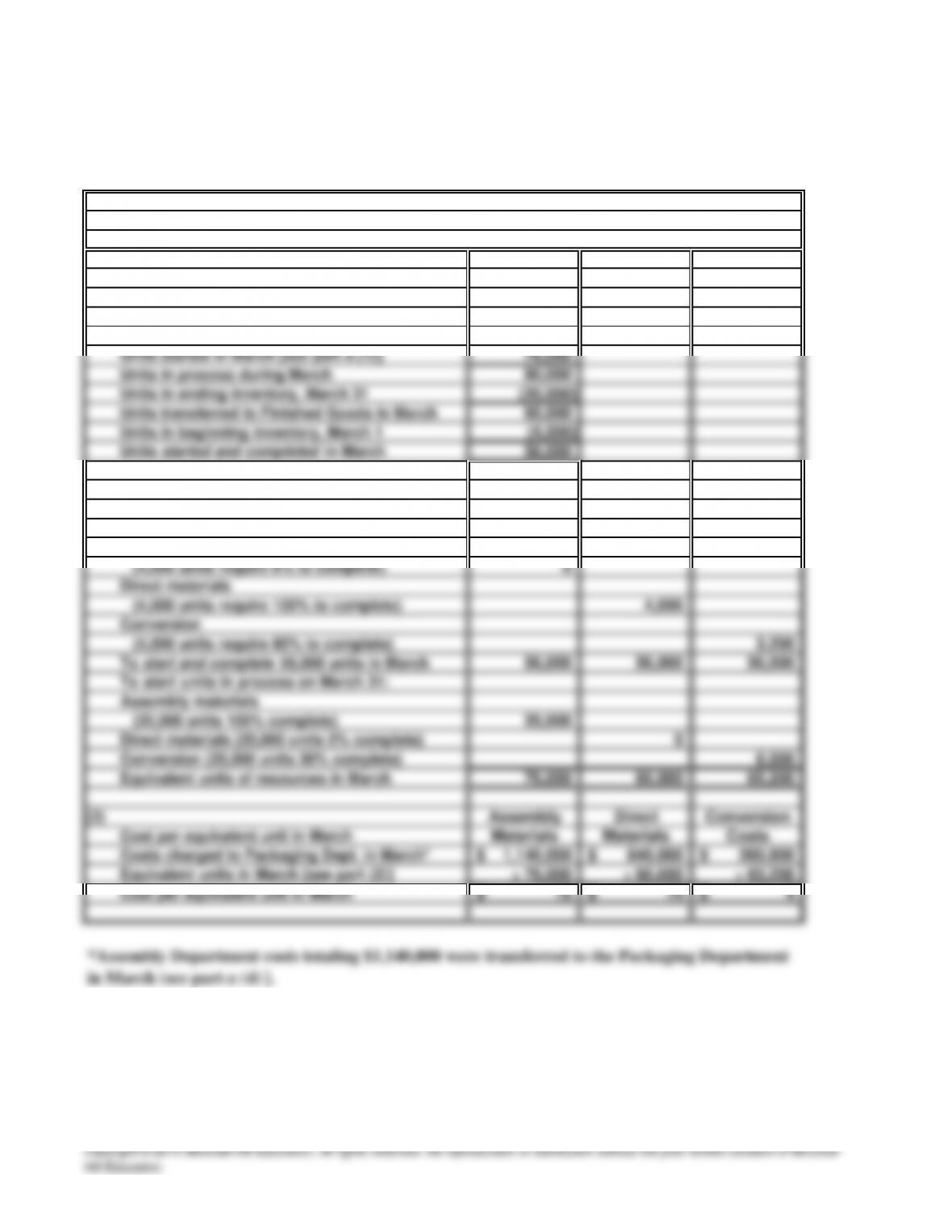

b. Requirements for the Packaging

(1) Flow of physical units: Packaging Dept.

Units in beginning inventory, March 1 4,000

(2) Assembly Direct

Input resources Materials Materials Conversion

To finish units in process on March 1:

Assembly material 0

Department in March

PROBLEM 18.8B

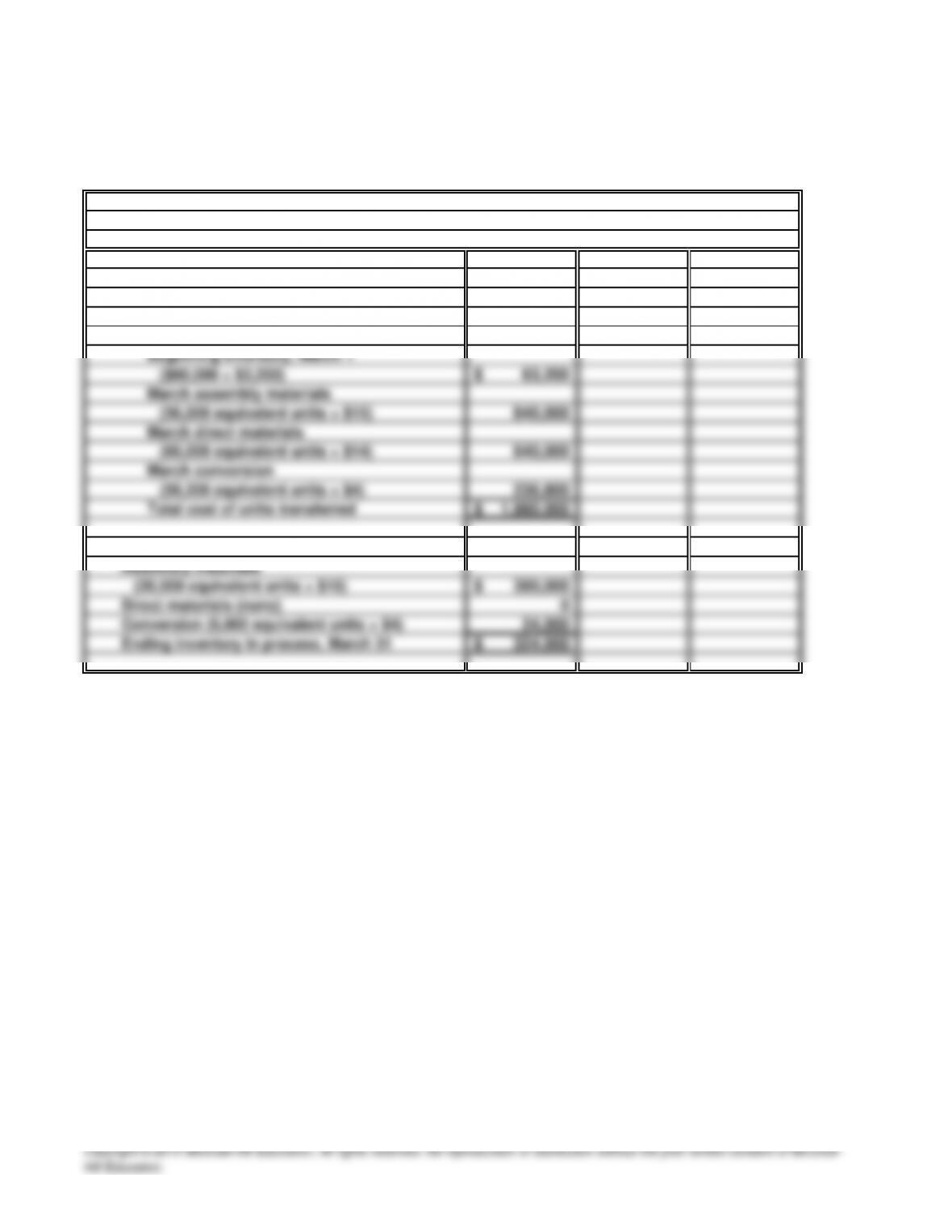

THOMPSON TOOLS (concluded)

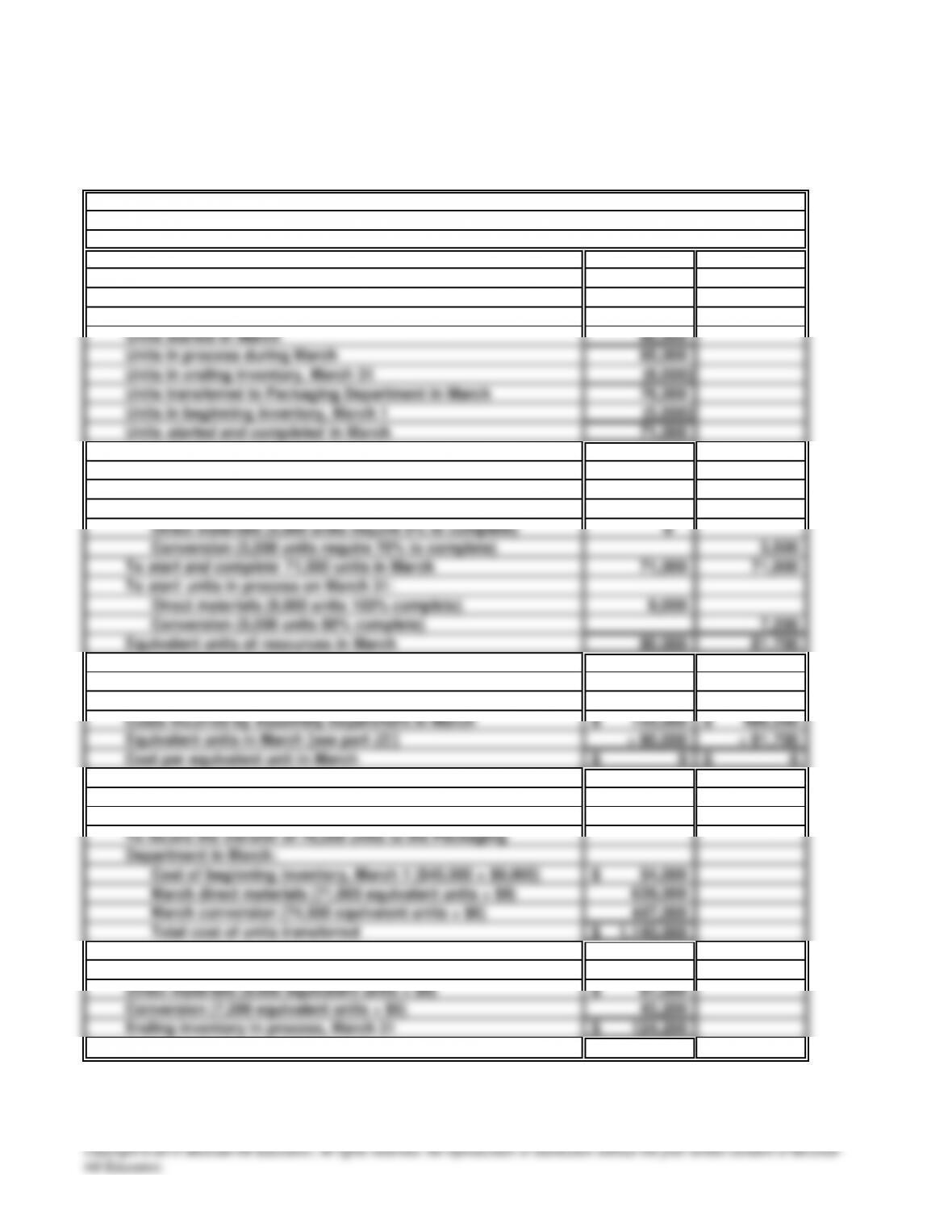

(4) 1,980,000

Work in Process: Packaging Department 1,980,000

(5)

Finished Goods Inventory

To record the transfer of 60,000 units

Inventory in March:

Work in Process: Packaging Dept., March 31

to the Finished Goods

SOLUTIONS TO CRITICAL THINKING CASE

S

CASE 18.1

SHOULDN’T WE DO THINGS DIFFERENTLY?

I will first address our use of process costing. It is true that our beer is brewed in batches,

which could be identified as jobs. But once the beer is bottled, the concept of the batch becomes

insignificant. As we produce only one line of beer, we would not charge a different price, nor

record a different cost of goods sold based upon the batch from which particular bottles came.

Thus, information about the costs of different batches would serve little purpose. What we

really need is information about the per-unit cost of various brewing processes. This enables us

to quickly identify the causes of changes in our total unit cost.

Next, we assign all manufacturing costs to units completed during the period because it is more

convenient than computing equivalent units, and produces essentially the same results. If you

compute our equivalent units, you will find this measurement to be nearly identical to the

number of bottles produced.

30 Minutes, Strong

Mr. Brown:

Thank you for your recent memo. I am glad to see that you have become familiar with our cost

accounting methods and have constructive suggestions. You are correct that we could use job

order costing and, also, that we could base our unit cost computations upon equivalent units,

rather than upon units completed. But let me explain briefly why we are currently doing what

we

do.

CASE 18.2

METAL PRODUCTS, INC.

a.

20 Minutes, Medium

The cost per equivalent unit of cut materials transferred into the Assembly Department in

February and reported as beginning inventory on March 1 was $25 per unit ($25,000 ÷ 1,000

units). The cost per equivalent unit of cut materials transferred into the Assembly

Department in March was $20 per unit. Thus, the cost of cut materials decreased by $5 per

unit.

CASE 18.3

PROCESS COSTING AT PEPSICO

ETHICS, FRAUD & CORPORATE GOVERNANCE

a.

25 Minutes, Easy

There are approximately ten processes involved in the production of Pepsi: (1) Ingredients

and packaging materials are received and inspected; (2) Ingredients and packaging materials

are moved into production; (3) Production codes are printed on containers; (4) Containers

CASE 18.4

WRIGLEY COMPAN

Y

INTERNET

a.

Melting

Mixing

b.

One configuration of processing departments could include a “Production Department” and a

“Finishing Department.” The Production Department would handle the activities of grinding,

30 Minutes, Medium

A sample flowchart of the activities involved in manufacturing chewing gum could be

constructed as follows: