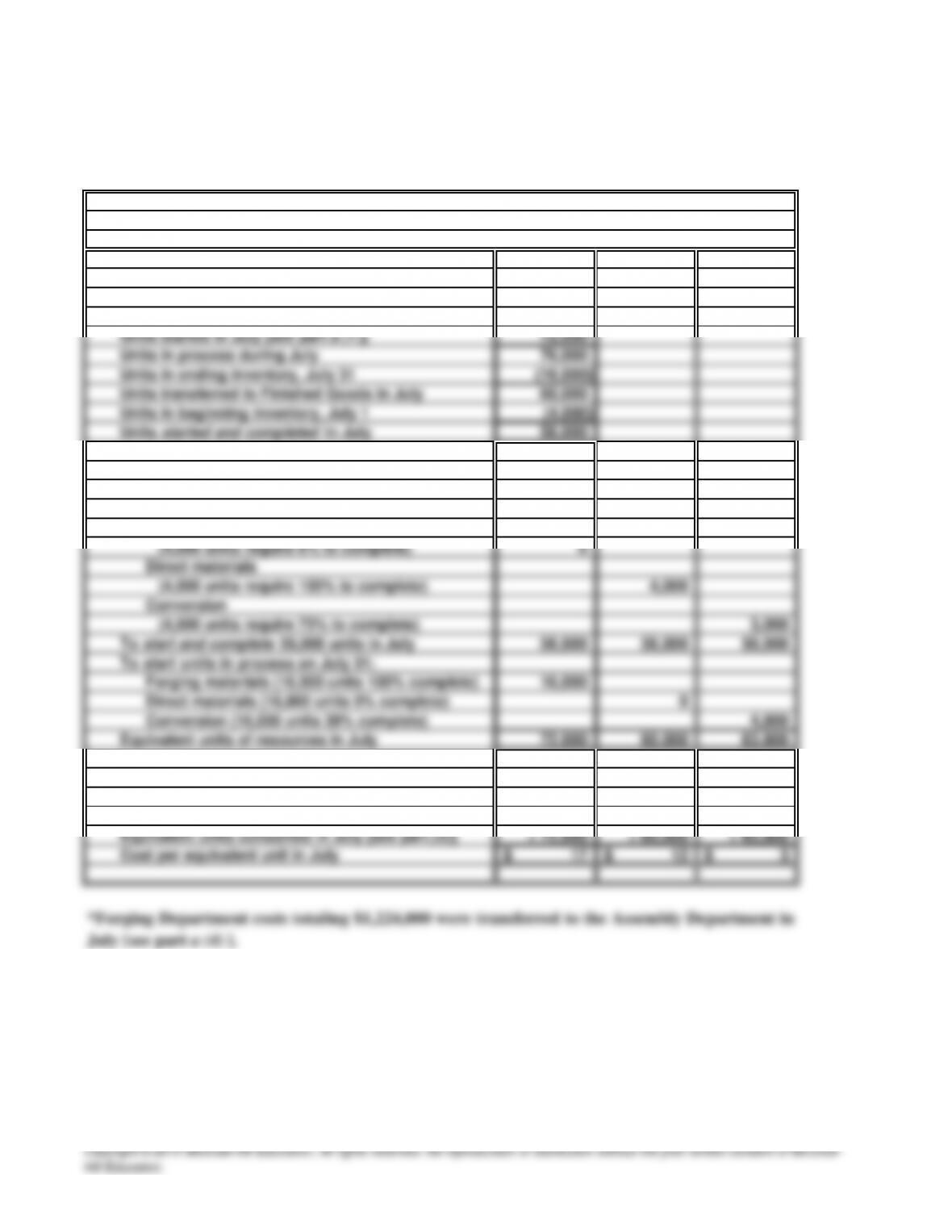

PROBLEM 18.8

A

WILSON DYNAMICS (continued)

b.

(1) 4,000

(3) Forging Direct Conversion

Materials Materials Costs

Costs charged to Assembly Department in July* 1,224,000$ 720,000$ 191,400$

Requirements for the Assembly Dept. in July

Flow of physical units: Assembly Department

Units in beginning inventory, July 1

Cost per equivalent unit in July

PROBLEM 18.8

A

WILSON DYNAMICS (concluded)

(4) 1,920,000

Work in Process: Assembly 1,920,000

Finished Goods Inventory

To record the transfer of 60,000 units to the Finished Goods

SOLUTIONS TO PROBLEMS SET B

20 Minutes, Easy PROBLEM 18.1B

STREET SMARTS

a.

5,000

(

1,000

)

4,000

Body Wiring

Materials Materials Conversion

Body materials

(1,000 units require 0% to complete) 0

Wiring materials

(1,000 units require 0% to complete) 0

(

)

Step 1: Determine flow of physical goods

Units transferred out in March

Beginning inventory in process, March 1

Units started and completed in March

To finish beginning inventory, March 1:

Step 2: Determine equivalent units

Input resources required

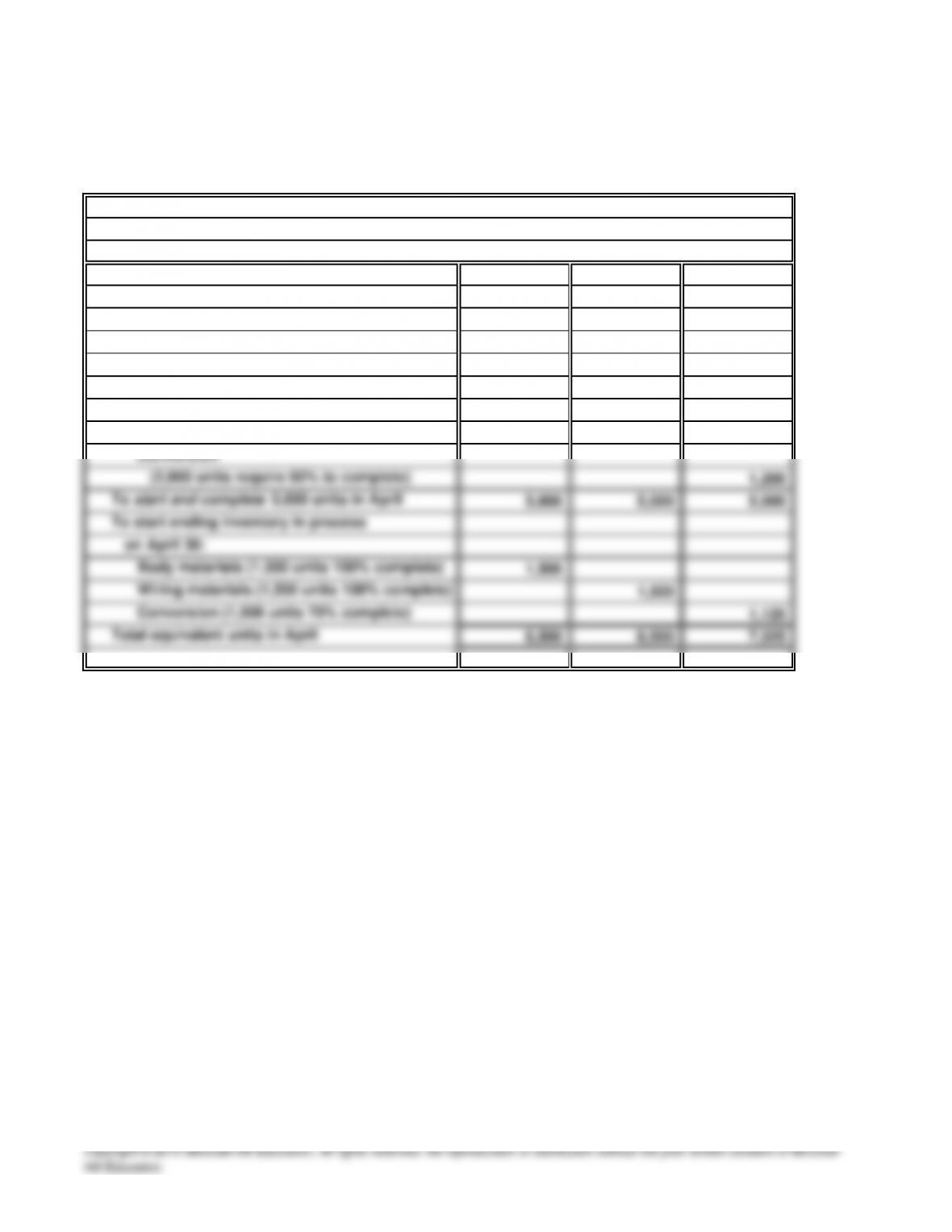

PROBLEM 18.1B

STREET SMARTS (concluded)

Body Wiring

Materials Materials Conversion

Body materials

(2,000 units require 0% to complete) 0

Wiring materials

(2,000 units require 100% to complete) 2,000

Conversion

Step 2: Determine equivalent units consumed

Input resources required

To finish beginning inventory, April 1:

20 Minutes, Easy PROBLEM 18.2B

MOWTOWN MANUFACTURIN

G

a. (1)

$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units]

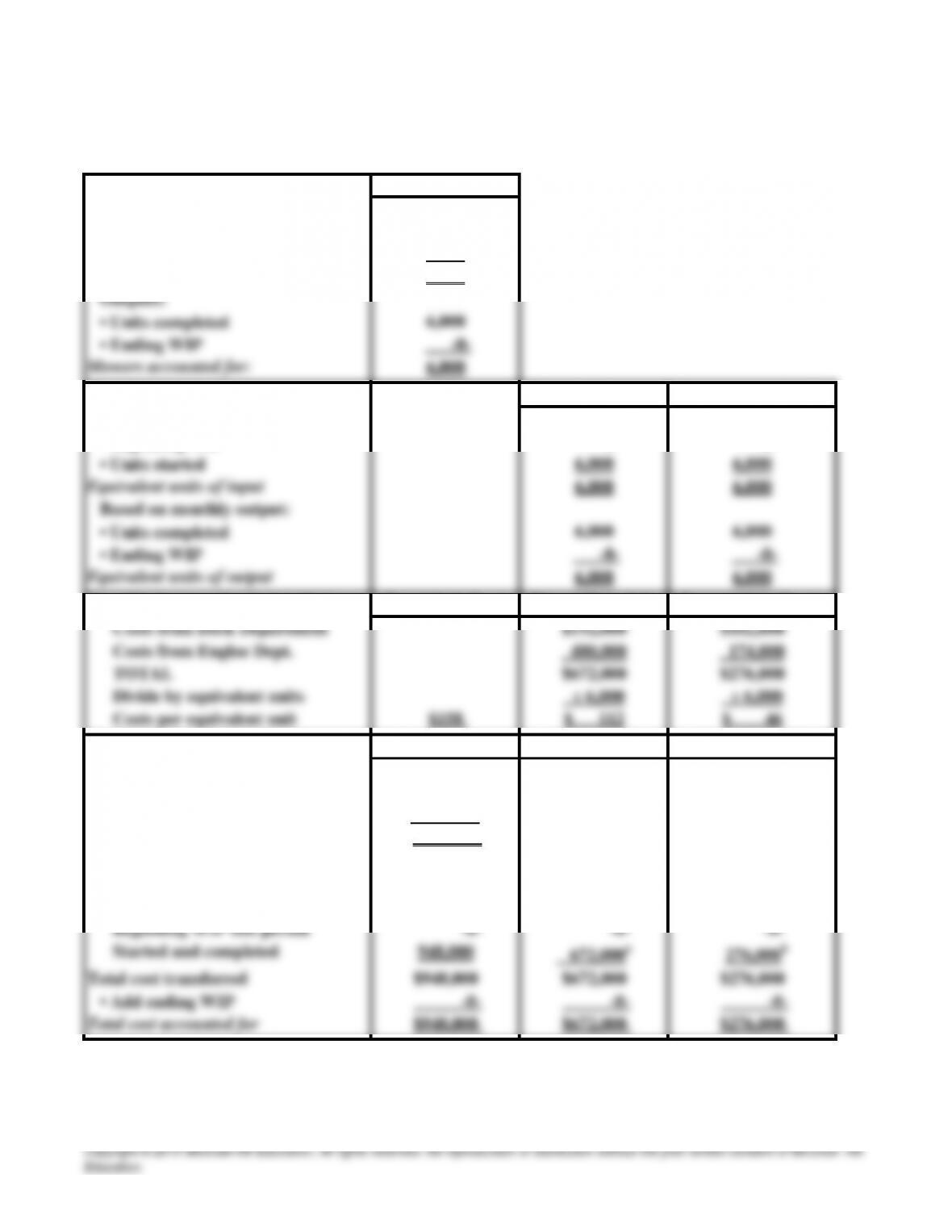

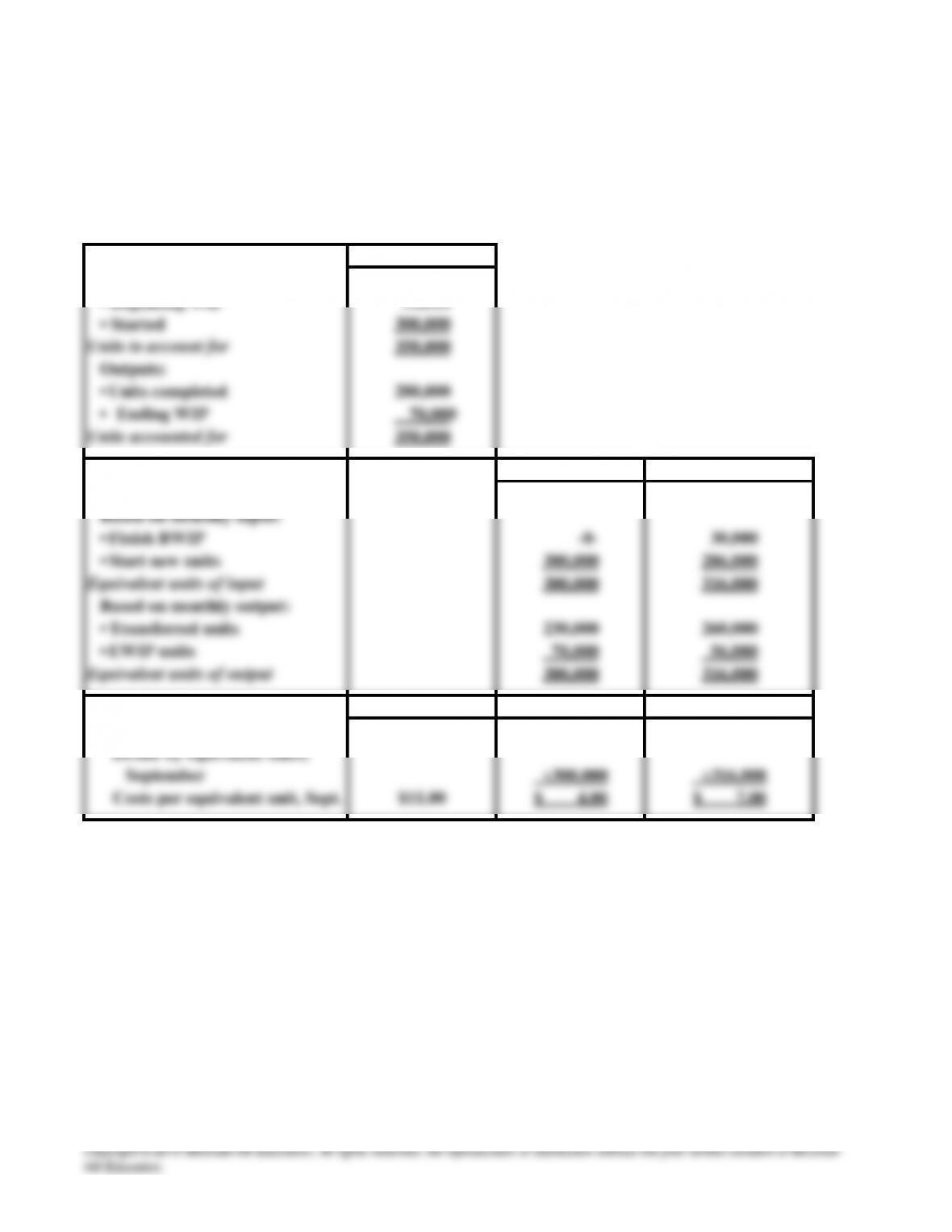

30 Minutes, Medium PROBLEM 18.3B

MOWTOWN MANUFACTURING

Part I. Physical Flow Total Units

Inputs:

• Beginning WIP -0-

•Started 6,000

Mowers to account for: 6,000

Part II. Equivalent Units Direct Materials Conversion Costs

Based on monthly input:

•Beginning WIP -0- -0-

Part III. Cost per Equivalent Unit Total Unit Cost Direct Materials Conversion Costs

Part IV. Total Cost Assignment Total Costs Direct Materials Conversion Costs

Costs to account for:

•Cost of beginning WIP $ -0-

•Cost added during the period 948,000

Total cost to account for $948,000

Costs accounted for:

•Cost of goods transferred

Beginning WIP last period $ -0- $ -0- $ -0-

a6,000 EU @ $112 = $672,000 b6,000 EU @ $46 = $276,000

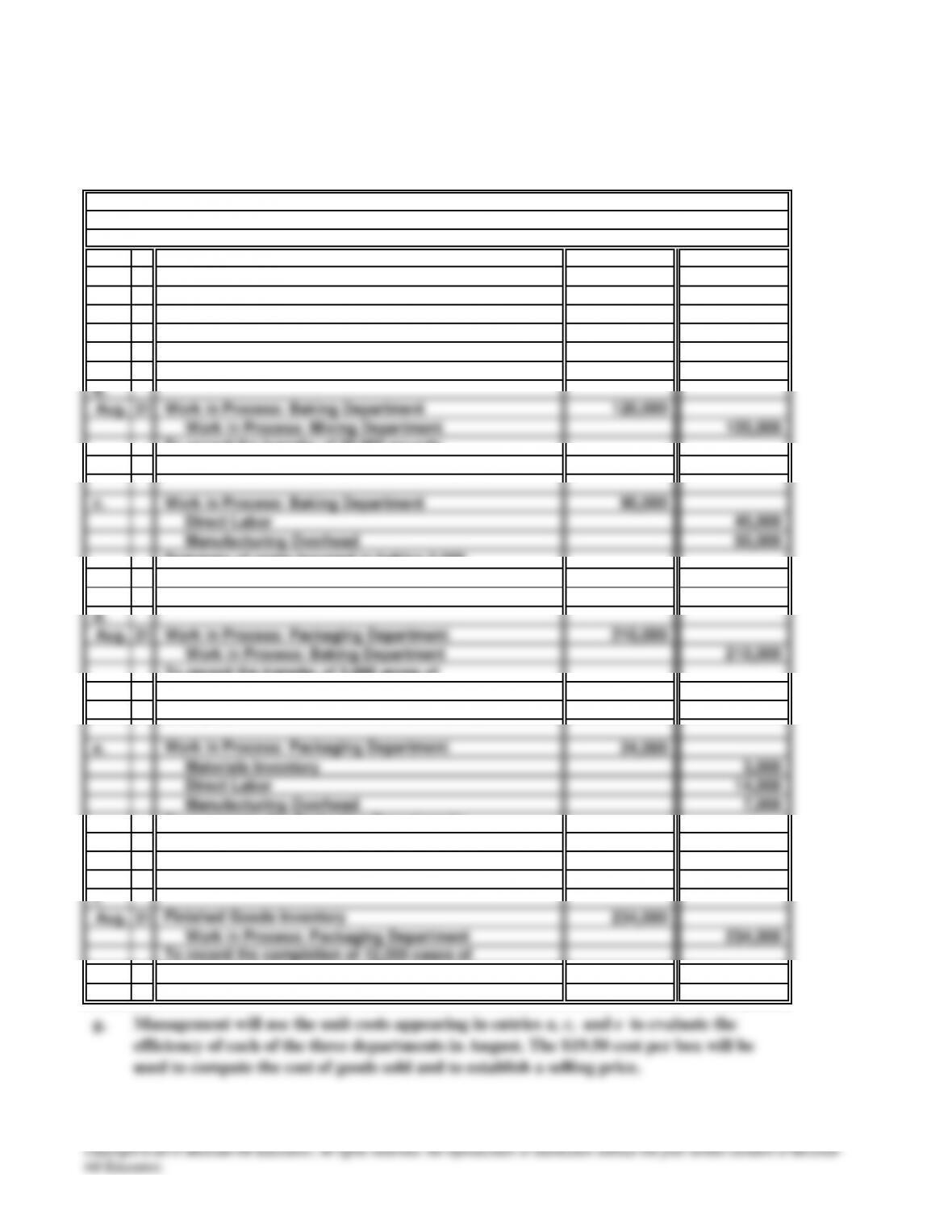

PROBLEM 18.4B

SNACK HAPP

Y

a. 120,000

Materials Inventor

y

25,000

Direct Labo

r

60,000

Manufacturin

g

Overhead 35,000

g

30 Minutes, Medium

Work in Process: Mixing Department

Summary of costs incurred in mixing 20,000 lbs.

of batter in August. Cost $6 per lb.

(

$120,000/20,000 lbs.

)

.

r

35 Minutes, Medium PROBLEM 18.5B

BALFANZ COMPAN

Y

a. Direct

Materials Conversion

0

Input resources required

To finish beginning inventory, September 1:

Direct materials (50,000 units require 0% to complete)

35 Minutes, Medium PROBLEM 18.6B

BALFANZ COMPANY

a. Production Cost Report

Part I. Physical Flow Total Units

Inputs:

•Beginning WIP 50,000

Part II. Equivalent Units Direct Materials Conversion

Consumed

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials Conversion Costs

Input costs in September $1,200,000 $2,212,000

Finishing Department, Month of September

PROBLEM 18.6B

BALFANZ COMPANY (concluded)

Total Costs Direct Materials Conversion Costs

$ 270,000

3,412,000

$3,682,000

b.

Management can compare production cost reports from month to month to help control costs

and assess efficiency of their processes. For example, the equivalent units can be tracked over

time to understand and evaluate capacity utilization. In addition, the cost per equivalent unit

can be evaluated over time to determine if costs are out of control for either direct materials

or conversion costs. For example, if material costs are rising per equivalent unit over time,

management could investigate if suppliers are charging more or if the production process is

creating more scrap and waste and needs to be adjusted.

d70,000 EU @ $4 = $280,000

e56,000 EU @ $7 = $392,000

a30,000 EU @ $7 = $210,000

• Cost of goods transferred

Costs accounted for:

Total cost to account for

Part IV. Total Cost Assignment

Costs to account for:

•Cost of beginning WIP

•Cost added during the period