B. Ex. 18.6 a.

b.

Direct

Materials Conversion

2,000

3,000

30,000 30,000

1,800

B. Ex. 18.7

Direct

Materials Conversion

0

(7,200)

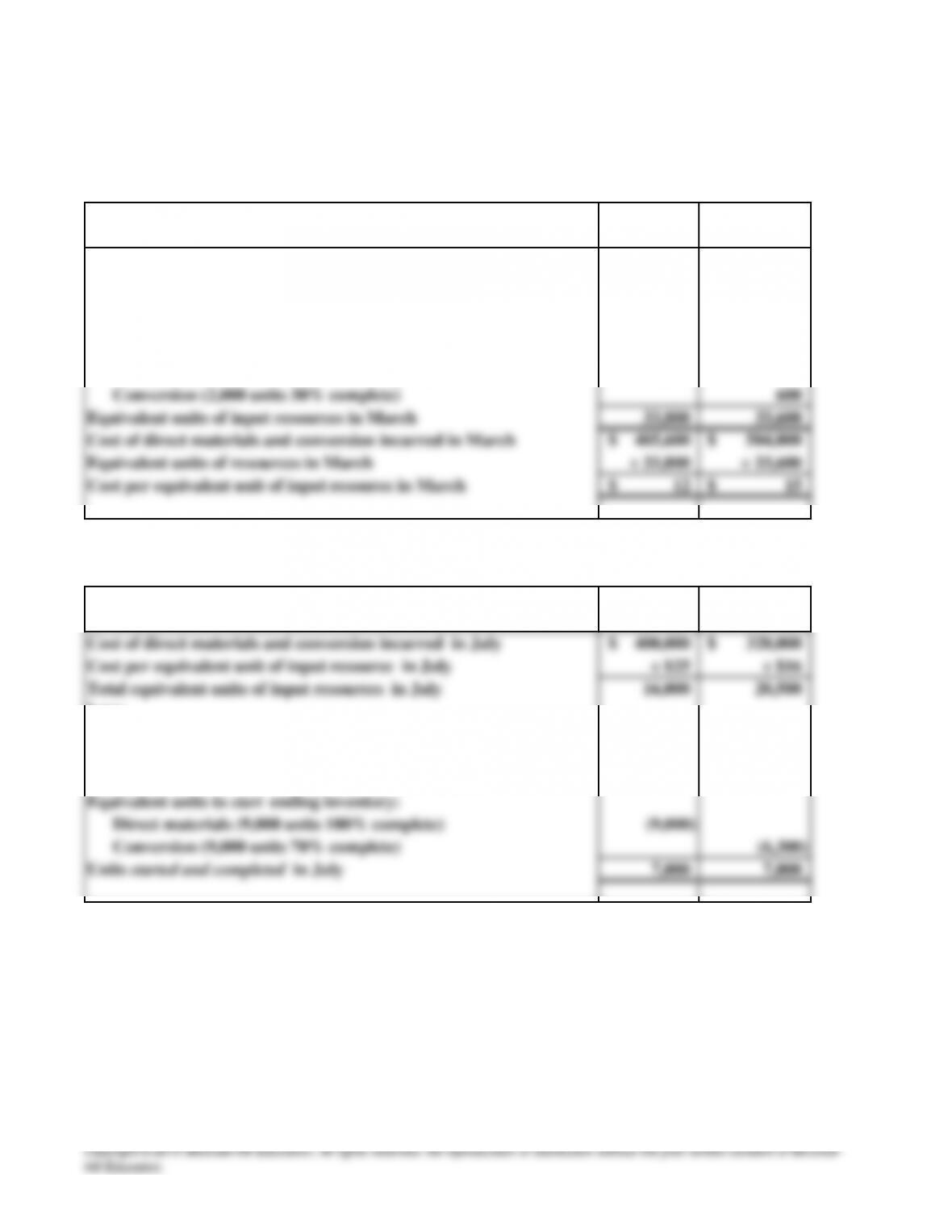

Direct materials (5,000 units require 40% to complete)

Conversion (5,000 units require 60% to complete)

To start ending inventory in process, March 31:

To start and complete 30,000 units in March:

To finish beginning inventory in process, March 1:

Direct materials (2,000 units 90% complete)

$12 per equivalent unit of direct material

$15 per equivalent unit of conversion

Computations:

Input resources required

Less:

Equivalent units to finish beginning inventory:

Conversion (12,000 units require 60% to complete)

Direct materials (12,000 units require 0% to complete)

B. Ex. 18.8 $ 50,000

Beginning work in process, September 1

Costs incurred to complete beginning work in

SOLUTIONS TO EXERCISES

Ex. 18.1 a.

b.

Ex. 18.2 a.

Direct Materials

Beg. Work in Process 0

Process costing

Conversion costs

Equivalent Units Produced in January

Labor and

Overhead

0

Ex. 18.3 a. 159,000

89,750

28,975

40,275

159,000

c. 250,000

250,000

120,000

120,000Finished Goods Inventory ……………………

To record the cost of the 10,000 units sold in June at a

unit cost of $12.

To record the transfer of 13,250 completed units to

finished goods during June at a unit cost of $12

($159,000/13,250 units

Accounts Receivable ………………………………..

To record the sale of 10,000 units in June at $25 per

unit.

Cost of Goods Sold ………………………………….

Sales ……………………………………………

Work in Process Inventory …………………..

To record the costs assigned to production during

June.

Work in Process Inventory ………………………..

Direct Materials ………………………………

Direct Labor …………………………………..

Manufacturing Overhead …………………….

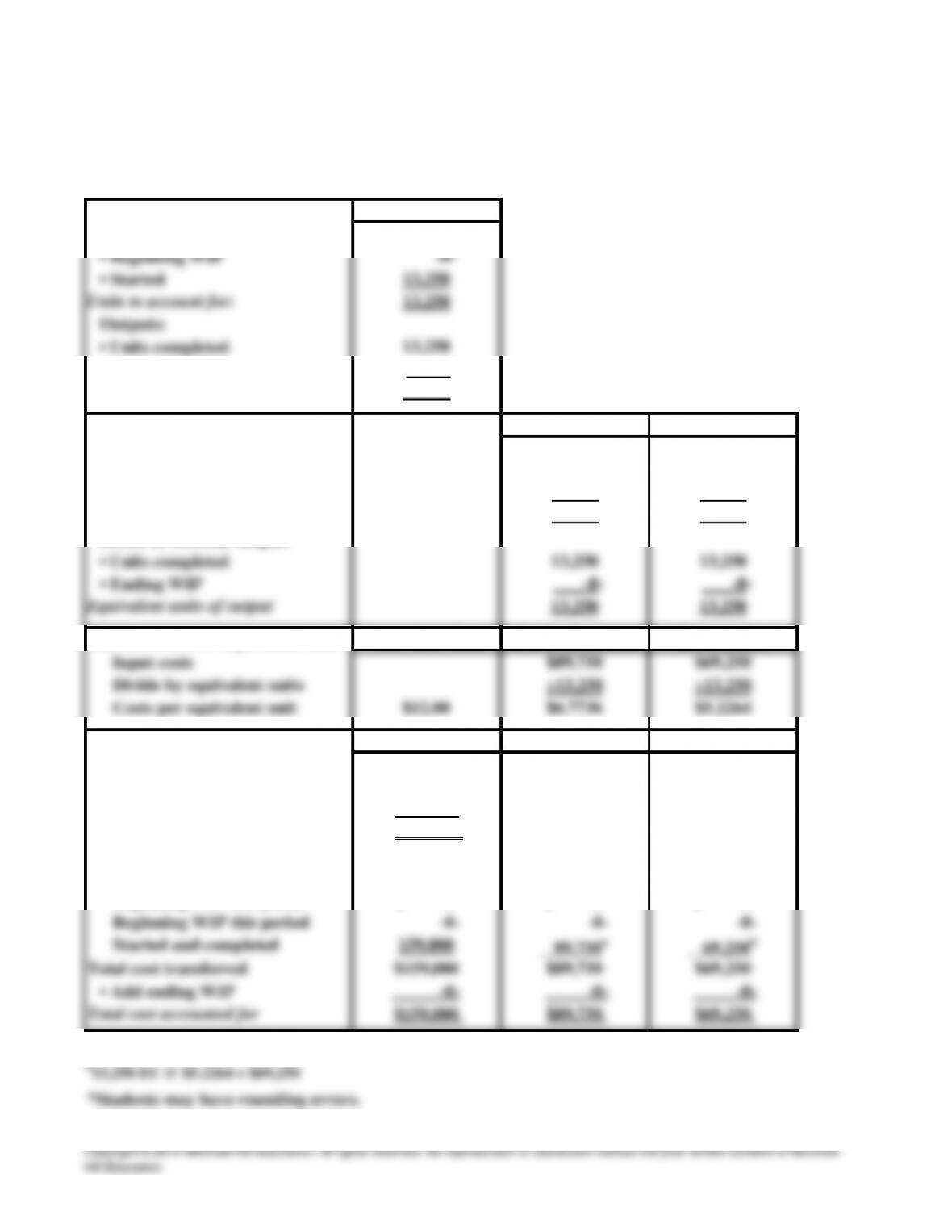

Part I. Physical Flow Total Units

Inputs:

•Ending WIP -0–

Units accounted for: 13,250

Part II. Equivalent Units Direct Materials Conversion

Based on monthly input:

•Beginning WIP -0- -0-

•Units started 13,250 13,250

Equivalent units of input 13,250 13,250

Based on monthly output:

Part III. Cost Per Equivalent Unit Total Unit Cost Direct Materials Conversion

Part IV. Total Cost Assignment Total Costs Direct Materials Conversion

Costs to account for:

•Cost of beginning WIP $ -0-

•Cost added during the period 159,000

Total cost to account for $159,000

Costs accounted for:

•Cost of goods transferred

Beginning WIP last period $ -0- $ -0- $ -0-

a13,250 EU @ $6.7736 = $89,750

Ex. 18.4 Shamrock Industries

Production Cost Report

For the Month of June

Ex. 18.5

a.

March

Beg. WIP 4,900 (7,000 × .7)

Equivalent full units of production:

April

1,920 (4,800 × .4)

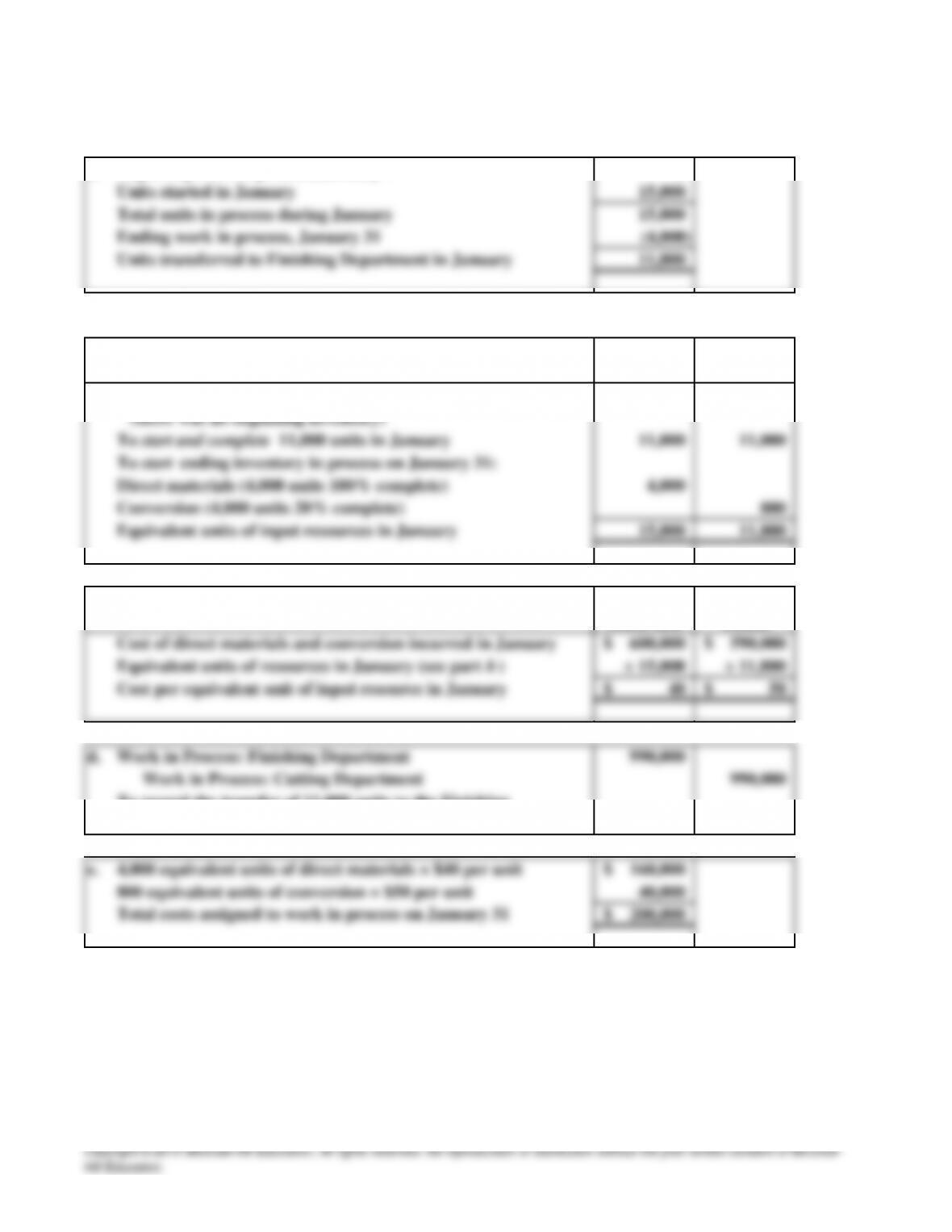

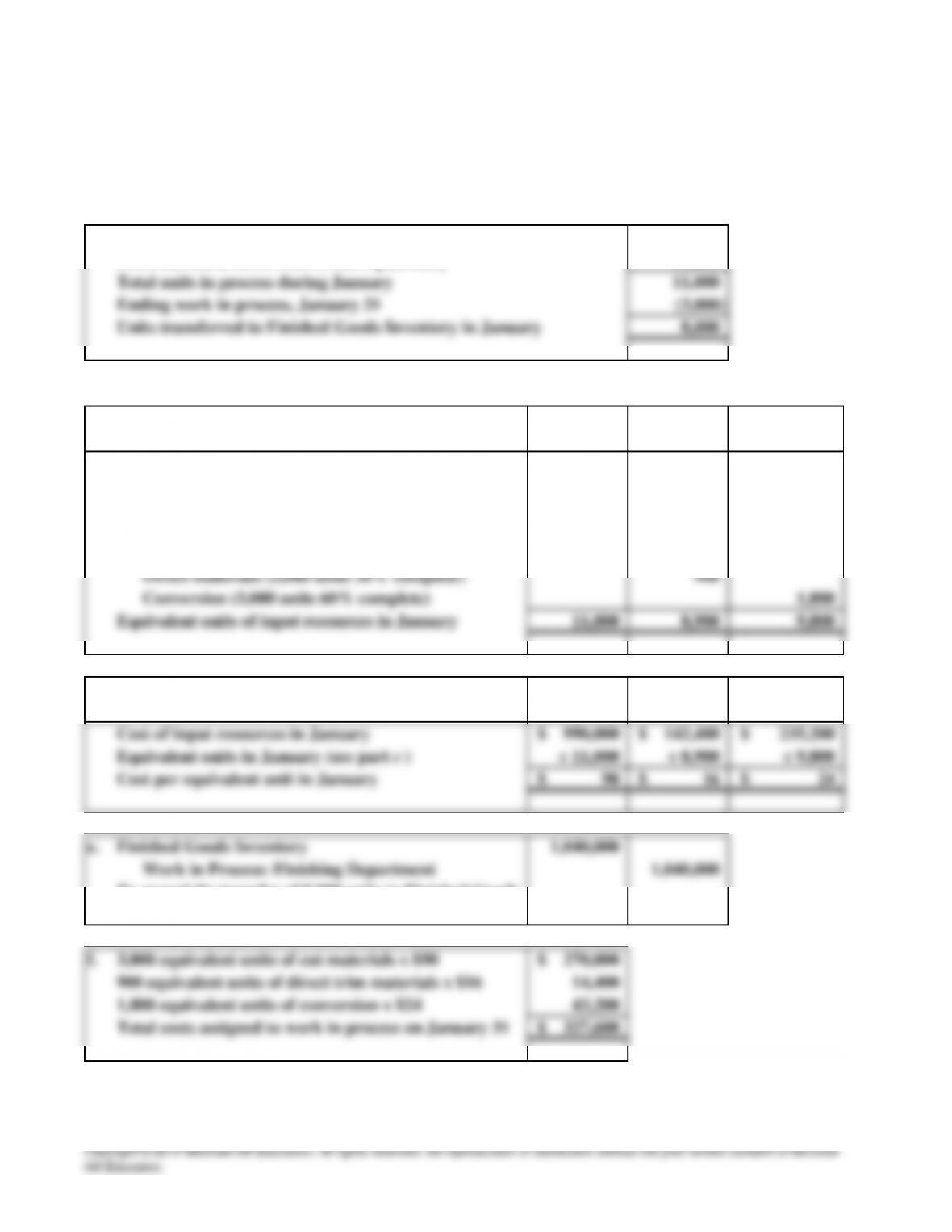

Ex. 18.6

a. 0

Beginning work in process, January 1

a.

b. 0

11,000

c. Cut Direct Trim

Materials Materials Conversion

00 0

8,000 8,000 8,000

3,000

d. Cut Direct Trim Conversion

Materials Materials Costs

To start and complete 8,000 units in January

100% complete)

To start ending inventory in process on January 31:

Cut material transferred in (3,000 units,

Ex. 18.7

Input resources required

To finish beginning inventory (there was none)

The number of units started by the Finishing Department equals the number of units transferred

in January from the Cutting Department, or 11,000 (see Exercise 18.6, part a).

Beginning work in process, January 1

Units started (transferred in) during January

Note: All of the units transferred were started and completed in January.

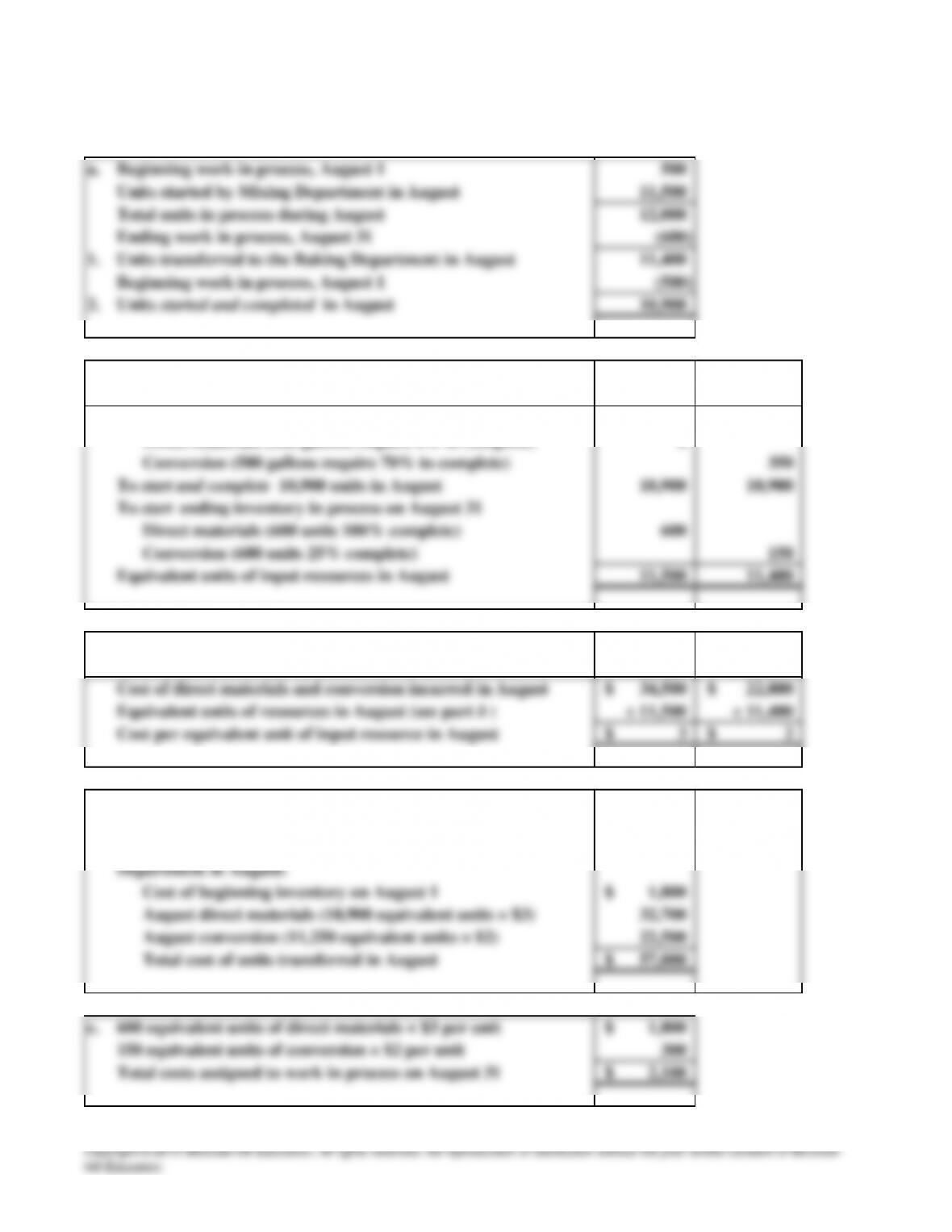

Ex. 18.8

a.

11,400

d. Mixed Direct Conversion

Materials Materials Costs

57,000

34,185

Ex. 18.9

One gallon of mix is required for each cake Baked by the Baking Department.

In August, 11,400 gallons of mix were transferred in (see Ex. 18.8, part a. ).

Units (cakes) started:

(see Ex. 18.8, part d)

Cost of batter mix transferred in

Cost of direct materials incurred in August